Orphan Drugs Explained

Published 01-JUN-2023 17:28 P.M.

|

6 minute read

Orphan drugs are drugs that are used to treat rare diseases that affect a small number of people.

An orphan disease is defined by the FDA as diseases or conditions that affect less than 200,000 people in the US.

Treatment for these diseases are often overlooked by the pharmaceutical industry as there may not be enough patients to justify the costs of research and development.

There are around 7000 different rare diseases out there and these people need treatment.

To incentivise drug development for orphan diseases, governments around the world provide incentives like market exclusivity, high pricing and fast tracked approvals.

In this article, we will explore why we think companies developing orphan drugs can be good investments and the challenges that these companies face.

The most famous example of an orphan drug company on the ASX is Neuren Pharmaceuticals (ASX: NEU), who has successfully commercialised a treatment for Rett Syndrome.

An example of an orphan drug company in our Portfolio is Dimerix (ASX: DXB), who is developing a drug for a rare kidney disease called FSGS.

Are orphan drugs profitable?

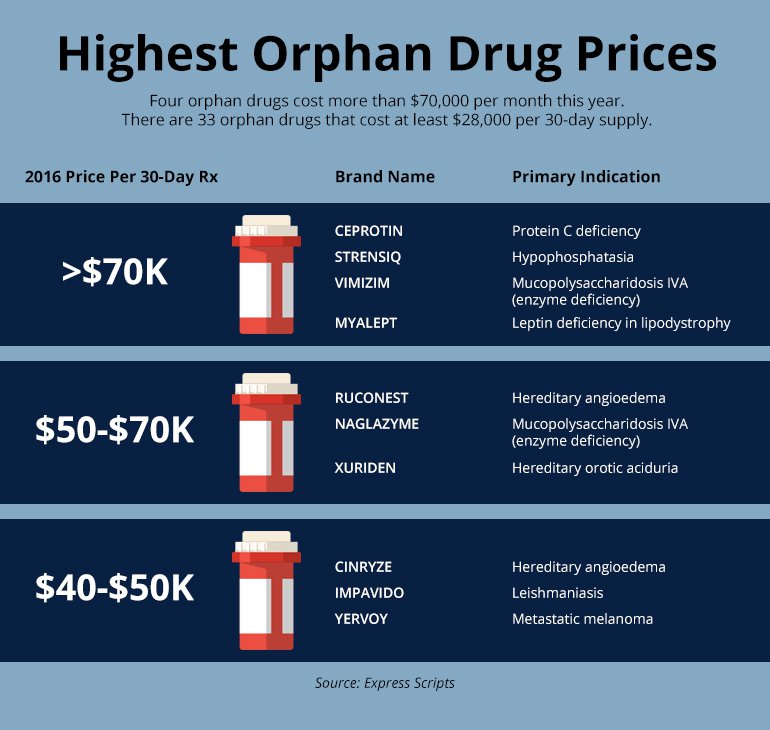

Yes, orphan drugs have become lucrative business opportunities because these drugs command orphan drug pricing.

The average price for an orphan drug is US$32,000 per year per patient (according to a 2021 study published in the journal Rare Diseases & Journal of Orphan Drugs).

This amount is not paid by mums and dads, but rather governments and insurance agencies subsidising the treatment.

Drug development companies will generally negotiate with payers (in this case governments and insurance agencies) to set a price for the orphan drug.

Ultimately, drug development companies want to set the price as high as possible for their treatments, to recoup the costs of clinical trials and deliver shareholder value.

The key factors in negotiating drug prices include:

- Cost of the drug (including R&D costs)

- The availability (if any) of alternative treatments

- The rarity of the disease

- Competition by other drug companies

Payers will also consider other factors when negotiating prices, such as the patient's overall health, the drug's side effects, and the drug's impact on the patient's quality of life - often referred to in metric form as QALYs (quality-adjusted life years).

Once approved, setting the price for the drug can be a big catalyst for a company if it exceeds market expectations.

Why invest in orphan drugs?

Orphan drugs only affect a very small portion of people, which means that governments have created incentives to encourage the development of these drugs.

These incentives are important as they open up the opportunity for biotech companies to pursue potentially lucrative markets that otherwise wouldn’t exist.

Let’s take a look at some of the key reasons why a company would develop an orphan drug:

Fast Tracked Approvals

Orphan drugs are often eligible for fast tracked approvals.

This means that the company will not always need to undertake the entirety of a Phase III clinical trial in order to get the product to market.

This can save the company time and money.

Orphan drug trials (in for example the field of oncology) may even be halted early on ethical grounds when an interim analysis demonstrates clinical superiority of the orphan drug in terms of an intermediate outcome measure such as progression-free survival.

Put simply, if the drug works and is safe for a life threatening disease like cancer, then it is best to get it to market as soon as possible.

Use of Surrogate Endpoints

Orphan drugs can also use “surrogate” outcomes to measure if a clinical trial is successful.

For example, a company developing a treatment for a rare kidney disease doesn’t need to wait for the patient to reach dialysis or death, they can use a “surrogate endpoint” to measure kidney function.

This is where a proxy is used for efficacy data - i.e a measure of kidney health such as estimated Glomerular Filtration Rate (eGFR) for instance.

This makes running a clinical trial much more practical and affordable for those companies.

Market exclusivity

Once the US FDA grants orphan drug designation to a drug, it also gets seven years of market exclusivity.

This exclusivity can give the company a competitive advantage, preventing other generic treatments from entering the market, and help ensure that it can recoup its research and development costs.

Lack of competition

For a disease like Alzhimers, that affects lots of people, there are lots of companies out there trying to find a treatment.

This competitive tension doesn’t exist as much with orphan diseases, because by their nature they are niche and rare.

This reduces the “competition risk” for the company, as it often will have a clear runway through to development without as many competitors chasing the same goal.

It will also generally increase the price of the drug, as there are often no alternative treatments to most orphan diseases.

High unmet medical needs

Rare diseases are often associated with high unmet medical needs, which means that there is a significant need for effective treatments.

By investing in a company that is researching orphan drugs, investors can help support the development of new treatments that can improve the lives of patients who are currently under-served by the healthcare system.

What are the challenges in developing orphan drugs

The development of an orphan drug is an expensive and complex process that involves extensive research, clinical trials, and regulatory approvals.

Orphan diseases have limited patient populations which throws up many challenges with regards to research and development.

These challenges include:

Regulatory Hurdles

Outside of the standard regulatory challenges for early stage biotechs, the key regulatory hurdle that the company faces is whether or not the drug is indeed an orphan drug.

The company will need to get “orphan drug designation” from a government agency like the FDA by proving that there are less than 200,000 people with the disease.

Recruitment Challenges

Because of the limited patient population, running clinical trials can be very expensive and very difficult.

Companies that develop treatment for orphan diseases will often target a disease that is not so unique so as to make it difficult to recruit patients into the clinical trial.

However, the disease has to still be rare enough to qualify for orphan drug designation.

The limited patient population may also affect recruitment.

With a limited pool of candidates to treat, recruitment can often be delayed or stalled.

Clinical trial costs

It is challenging enough to run one clinical trial from a central site, but because of the limited patient population companies will often need to run clinical trials across many sites, and sometimes many countries.

It can be expensive and challenging to coordinate a multi-jurisdiction clinical trial, with individual ethics approval needed in each jurisdiction.

Financing Risk

Developing drugs for rare diseases can be expensive, and there is always a risk that the company may not be able to secure sufficient funding to support its research and development efforts.

This can lead to delays in the development of drug candidates or even the termination of the program.

Conclusion

Ultimately, like all investments in early stage biotech, developing orphan drugs can be expensive and take years.

However, orphan drugs do have certain advantages over traditional drug development pathways that investors and companies can take advantage of.

With these advantages comes some specific risks around recruiting for, and selling to, limited populations of affected people.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.