MNB one step closer to first production with $14M from development bank

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 8,645,000 MNB shares at the time of publishing this article. The Company has been engaged by MNB to share our commentary on the progress of our Investment in MNB over time.

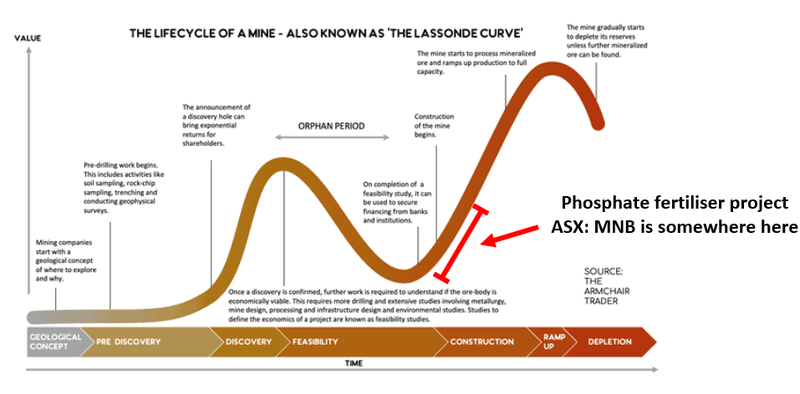

We have been investing in junior resources stocks for over 20 years, and it is extremely rare to see a mining project move into production.

Our 2022 Wise-Owl Pick of the Year, Minbos Resources (ASX:MNB), is looking likely to be the first company in our Portfolio to do just that.

MNB is just entering the “exciting” part on the Lassonde Curve... (more on this in a second).

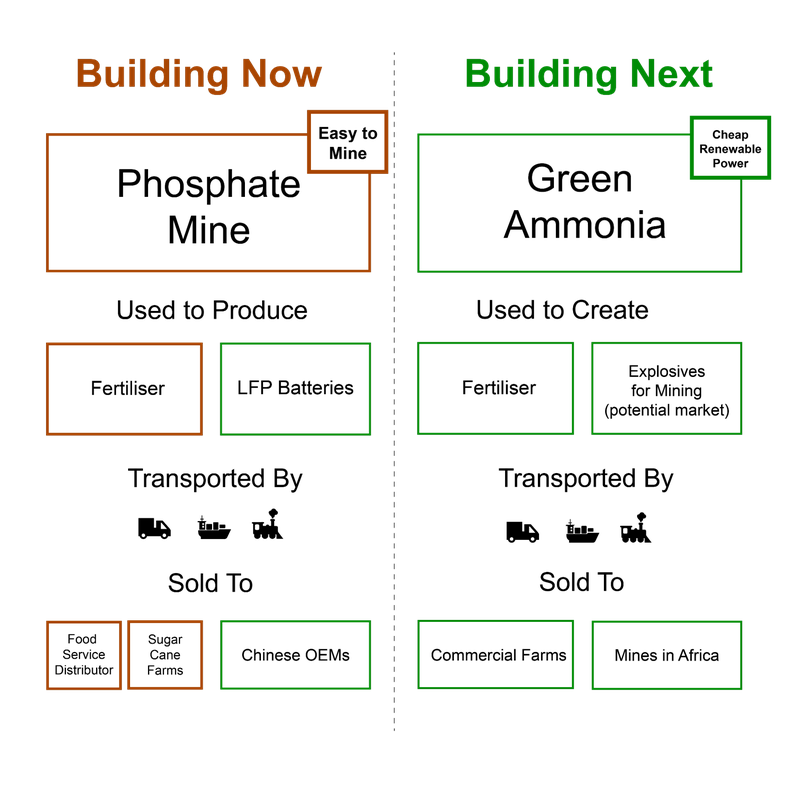

MNB has two key projects in Angola:

- Fertiliser project (in construction) - a phosphate (fertiliser) project that has an offtake agreement with the largest agri-distribution business in Angola - expected to be in production in the next few months.

- Green ammonia project (feasibility stage) - a feasibility stage green ammonia project powered by some of the cheapest green energy (hydroelectricity) in the world.

Today, it is all about the fertiliser project, with MNB announcing a term sheet for $14M of debt funding from the Industrial Development Corporation of South Africa.

At this stage of the project, MNB is close to earning revenue by producing and selling phosphate/fertiliser products.

That is why we like its decision to go down a non-dilutive funding route, through debt financing on “competitive” terms.

MNB has signed an offtake deal with Carrinho Group for 66% of Stage 1 production over the next 7 years, and is close to signing an offtake with Biocom - the largest sugarcane farm in Africa.

The project economics for MNB’s fertiliser project are:

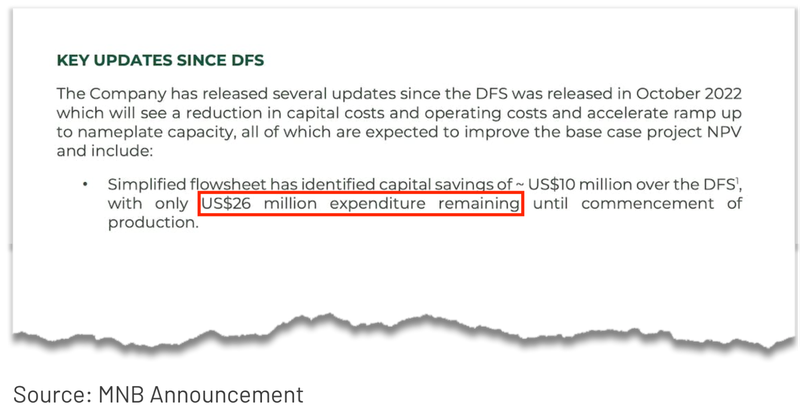

- CAPEX of US$48.5M - Most of this has been paid for already with MNB confirming today it had only US$26M left to get the project into production (before today’s US$14M debt facility is spent).

- Net Present Value (NPV) of US$203.4M (base case) - That figure was based on a long-term average phosphate rock pricing of US$422 per tonne — the 15-year average price.

- NPV of US$399.4M (upside case) - using spot prices for phosphate fertilisers in October 2022.

- Post-tax internal rate of return (IRR) of 61%

- Payback period of 3.6 years

With first production from its fertiliser project now just months away, MNB’s market cap sits at $76.7M, ~1/3rd of its fertiliser project’s NPV, before accounting for its green ammonia project.

MNB has also commenced a concept study on whether it is feasible to produce “yellow phosphorus” from its deposit for use in LFP batteries (the ones used in most Chinese electric vehicles), with the results expected soon.

This type of phosphate is currently considered a “waste product”, so any ability to utilise it will be an upside to the current economics of the project.

MNB has already started the preliminary work to develop the mine, including land clearing and commencing the resettlement process.

With production not far away, here is where we see MNB on the Lassonde Curve:

MNB’s share price has been trading sideways for about six months now, as MNB published in a recent presentation that the project schedule was delayed by around ~3 months to maximise non-dilutive funding options.

Now, with a US$14M debt financing facility in place (subject to final DD) we expect the construction activities to ramp up soon.

According to MNB’s April quarterly, the company has sought around ~US$30M in debt funding with today’s funding covering about half of that required for the project.

Today MNB said it had just US$26M in expenditure left before its project would be in production.

We expect more funding to come with MNB looking at other funding opportunities.

This may include a joint venture flagged by the company with interested parties in the P4 study, as well as cash advances from offtake partners.

Getting its phosphate project into production forms the basis for our MNB “Big Bet” which is as follows:

Our MNB Big Bet:

“MNB delivers a 10x return by building a profitable phosphate project AND progressing its green ammonia project to construction phase.”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our MNB Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

Minbos Resources

ASX:MNB

MNB, Storming Towards Production

Minbos is one of our favourite Investments.

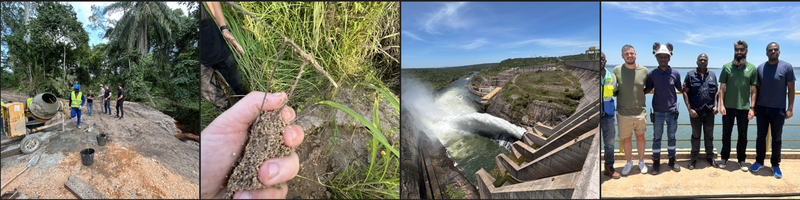

Earlier this year, we flew up to Angola to see the project ourselves:

Since we visited in February, MNB’s project has come a long way in a short amount of time.

A few weeks ago the company provided an update on its phosphate products, that are ready to sell into the market:

As long time investors, It was very cool to see the branding and packaging on the products that MNB will soon sell into the market.

The project seems to be becoming very, very real.

We have been Invested in MNB for over three years now and have been following the company's journey to turn its Angolan phosphate deposit into a fully fledged fertiliser business.

When investing in small cap exploration companies it's rare to see a company move into production, but seeing these designs from MNB shows just how close the company is.

The company launched the product brand at an industry workshop in Angola, which was attended by over 200 delegates as well as representatives from Agricultural, Economic and Mining ministries.

Key to the workshop was to showcase MNB’s new product and initiatives that have been developed (together with the IFDC - International Fertilizer Development Center) to improve crop yields for farmers.

MNB will be launching a free app that helps farmers to better use its product and deliver higher crop yields:

Why are MNB’s initiatives to support farmers so important?

Essentially, the amount MNB can sell its product for is directly proportional to the effectiveness of the fertiliser on crop yields.

The better the fertiliser is used, the more money MNB makes from its products.

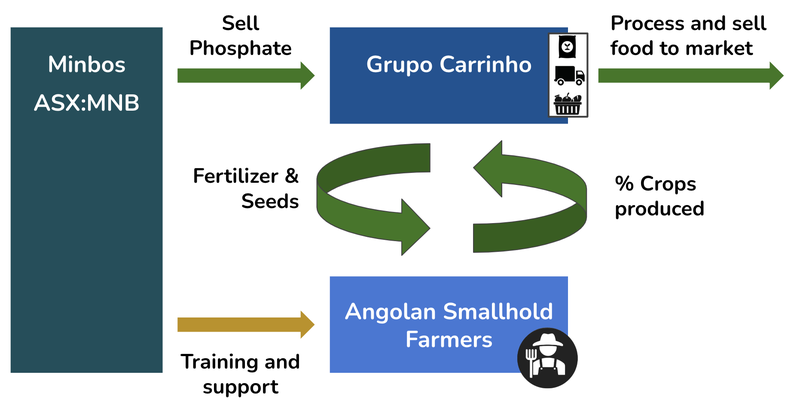

MNB has signed an offtake deal with Carrinho Group for 66% of Stage 1 production over the next 7 years.

Carrinho Group is an integrated agri-distribution business that has the resources and infrastructure to service the millions of small hold farmers in the country.

On the supply chain, Grupo Carrinho supplies fertiliser and seeds directly to the Angolan smallhold farms that MNB are looking to support.

Here is how the deal will work:

To read our full take on the Carrinho offtake read: MNB Signs Offtake MoU for 66% of Stage 1 Phosphate Production

This deal forms part of MNB’s grand ambitions to turn Angola into the agricultural hub of Africa.

In order to do that it needs to help farmers, at a grass-roots level.

As the agricultural industry grows, so does MNB’s value to the country.

In the presentation released together with the announcement, MNB showcases the benefits of its product specific to the Angolan climate. Click here to see the full presentation.

As you can see here from a field trial with Biocom (one of the largest sugarcane farms in Africa) MNB’s product is far superior to existing fertilisers:

In MNB’s last update, it announced that “Biocom requested formal documentation for an offtake”... so expect details soon.

We think that this launch is the start of something big for MNB and Angola as the company looks to move into production in the next few months.

More on today’s funding deal

Today, MNB announced that it has an indicative term sheet (subject to final DD) for a $14M funding facility to help construct its phosphate/fertiliser plant.

MNB’s financing partner is the Industrial Development Corporation of South Africa.

The IDC is a self-financing national development financing institution which has investments across mining, agriculture, manufacturing, tourism, and telecommunications.

The IDC has been around since 1940, but in the 90s expanded to include investments outside of South Africa.

Think of it as the South African version of say, the European Bank for Reconstruction and Development, another international development bank which has also invested in some of our other Portfolio Companies.

IDC’s ability to fund projects is quite expansive for a development bank operating in Africa.

During the 2022 financial year alone they provided ~A$1.3BN in funding for projects across Africa so we think IDC is more than well equipped to take on a project of MNB’s size.

The IDC has invested in a range of projects, with a particular focus on energy, infrastructure and agriculture - notably helping fund South Africa’s largest LNG project two months ago.

Importantly, this funding comes not from a Chinese nor an American party - leaving MNB with optionality to secure the remaining funding.

Angola in particular, has become somewhat of a political beneficiary of the East vs West control over influence in the region.

When we visited the country, a lot of the major port infrastructure was Chinese, with the “Belt and Road Initiatives” putting its stamp on the country.

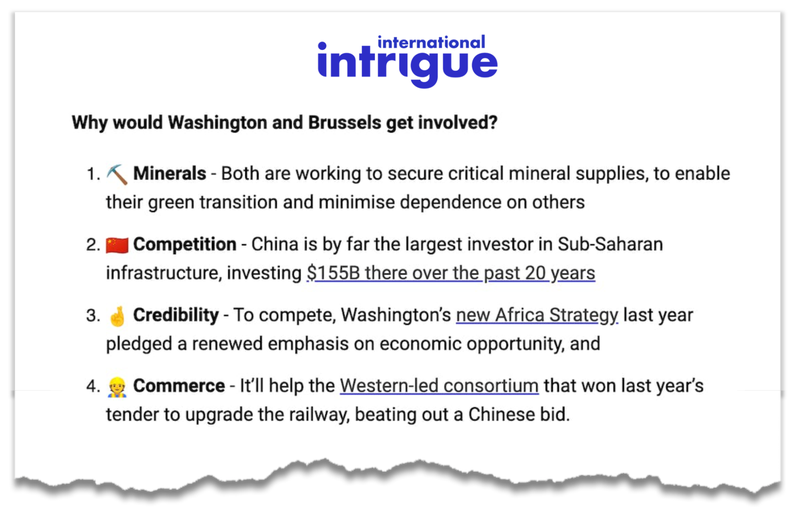

Recently, the US has sought to invest in the region, with the Biden Administration announcing support for a rail link in the Lobito corridor, calling it a “game changing regional investment”.

This is basically a giant railway funded by the US and the EU that links key mining regions in Africa including Angola, the DRC and Zambia.

The goal is to improve logistics for landlocked countries to export key mineral resources to the rest of the world.

There are four key reasons that the US want to invest in the region:

(Source)

We think that this interest in the region can only be beneficial for MNB, as the company has the necessary connections with the Angolan government as well as the ability to walk in both camps.

With today’s funding agreement coming from a South African development fund, MNB has left all doors open for future funding opportunities.

What’s next for MNB’s fertiliser project?

🔄 Funding for the remainder of CAPEX on the project

MNB has announced that it will require US$26M to fund the project through to production.

With the US$14M secured today, it leaves a further ~US$12M of funding left.

🔄 First production

MNB published that the timeframes have been moved back by around 3 months in order to give the company more room to secure financing. We are expecting first production in early 2024.

🔄 Results of P4 Study

MNB has commenced a concept study into whether its phosphate waste product is suitable for P4 in LFP batteries (the types used in Chinese electric vehicles).

MNB has a Strategic Cooperation Agreement in place with a syndicate of Chinese new energy materials investors - controlled by the Chairman of CATL.

This study is due by the end of the year with the outputs expected to form part of a joint venture with interested parties.

What’s next for MNB’s green ammonia project?

🔄 Pre Feasibility Study (PFS)

MNB is now working on a PFS for its green ammonia project, which will provide us with more information about the operating costs, revenues, and Net Present Value (NPV).

Ultimately the feasibility study will determine whether or not the project is commercially viable.

🔄 Environmental Impact Assessment

MNB kicked off the EIA last month, with the company expecting to complete the study half way through next year.

🔄 Market feasibility study

MNB intends to undertake a market feasibility study on opportunities to sell its green ammonia in Angola and to take advantage of the recently announced Lobito Corridor rail link (Angola, Democratic Republic of Congo and Zambia).

🔲 Binding power agreement Angolan power network operator

We want to see MNB convert its Memorandum Of Understanding (MoU) with Angola’s National Electricity Transmission Network (RNT-EP) into a binding power agreement.

We expect this to come after feasibility studies are completed.

🔲 Sign technical, offtake, and investment development partners

Much of the world's ammonia is produced using fossil fuels which makes MNB’s green ammonia project unique.

As MNB’s project advances, we are hoping potential offtake and development partners start to become more interested in the project and a deal is signed with MNB.

What are the risks?

With the funding agreement announced today (still subject to final DD) MNB has de-risked almost half of its project CAPEX requirements.

Key risks now for the company include “delay risk” and “commodity pricing” risk as the company moves closer to production.

MNB’s revenue will be directly tied to the TSP price, if the TSP price drops below the levels that the company anticipated in its DFS, then the project may be less economic than expected.

To see all of our risks for MNB read our MNB Investment Memo.

Our MNB Investment Memo

Click here for our Investment Memo for MNB, where you can find a short, high level summary of our reasons for Investing.

In our MNB Investment Memo, you’ll find:

- Key objectives for MNB

- Why we are Invested in MNB

- What the key risks to our Investment thesis are

- Our Investment plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.