MMI delivers positive DFS that will see it increase bauxite production capacity

Hey! Looks like you have stumbled on the section of our website where we have archived articles from our old business model.

In 2019 the original founding team returned to run Next Investors, we changed our business model to only write about stocks we carefully research and are invested in for the long term.

The below articles were written under our previous business model. We have kept these articles online here for your reference.

Our new mission is to build a high performing ASX micro cap investment portfolio and share our research, analysis and investment strategy with our readers.

Click Here to View Latest Articles

Metro Mining (ASX:MMI) has completed the Definitive Feasibility Study (DFS) for the Stage 2 expansion of the Bauxite Hills Mine located in Cape York, Queensland.

As reported by Finfeed last week, the release of the DFS, could be a game changer for the company, particularly as it has been successful in upgrading the project’s production capacity to 6 million tonnes per annum.

Read: Metro Mining starts to motor ahead of transformational DFS

The release of today’s highly encouraging DFS comes on the back of an uptick in consensus forecasts for the company, suggesting that analysts have started to factor in the Metro’s strong production outlook.

Today’s DFS could further pique analyst and investor interest.

DFS highlights

The DFS was completed by independent Mining Consultancy MEC Mining, which has history in completing feasibility studies at Bauxite Hills and was supported by several specialist consulting firms.

The Bauxite Hills Mine has been operating for more than 18 months and has produced over 4.3M WMT of ore for sales to various Chinese refineries.

Metro is now focused on completing the Stage 2 expansion of the mine, which will reduce unit operating costs and increase production capacity to 6M WMT pa from 2021 onwards.

There are three key components to Stage 2:

- Construction and mobilisation to Skardon River of a Floating Terminal (FT) with the ability to load 6M WMT pa of bauxite;

- Scale up of the current mining, haulage and transhipment fleets;

- Optimisation and upgrading of the existing port and barge loading facilities

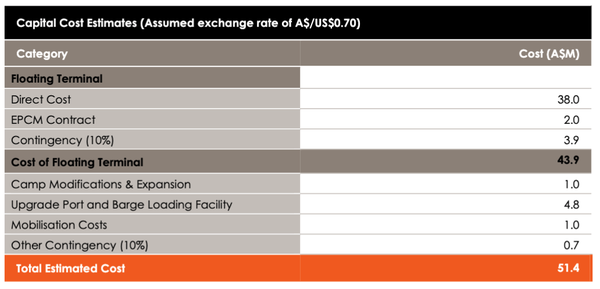

Before we look at these components individually, let’s first take a look at capital expenditure estimates.

Estimates have been undertaken to an accuracy of ±10% and a 10% contingency has been applied across all costs.

The Capital Costs are A$51.4Million, including 10% contingency. CAPEX will be incurred across a 15-18 month timeframe beginning in late 2019 and financing will come from a mixture of operational cashflow and external sources, with Metro in advanced discussions with debt financiers.

Of note in this cost estimate is the significant reduction in unit operating costs by the use of a FT that can load larger, ungeared Ocean-Going Vessels (OGVs), including Cape Size vessels. The FT comprises approximately 85% of the total expansion capital.

Expansion of the accommodation camp, port area modifications and fleet additions (including mobilisation) makes up the remainder of the capital spend.

Life of Mine unit operating costs are forecast to reduce by approximately 18% delivered to China when operating at the 6MWMT pa rate. This will increase operating margins and position Bauxite Hills in the lowest quartile of the global cash cost curve for bauxite producers.

As Metro is the only pure play bauxite producer of any size in Australia exposed to the China market, it presents a unique opportunity for ASX investors especially as project payback is estimated to be less than 18 months.

“The completion of the feasibility study and selection of the preferred design for the FT is a key step to allow execution of the expansion at Bauxite Hills by 2021. It builds on the outstanding production performance and operating experience gained since the mine commenced production in April 2018,” Metro Managing Director and Chief Executive Officer Simon Finnis said.

“We have some further work to do on the final design, and we need to finalise the funding package, and then we will present to the board for their approval. It is pleasing to see the DFS completed and we thank shareholders for their patience.

“The DFS clearly shows that the expansion confirms Bauxite Hills as one of the lowest cost and largest independent producers of bauxite in the market.”

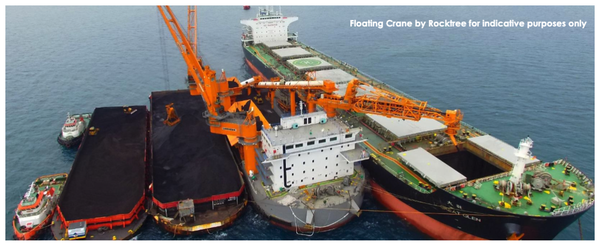

Floating terminal

The main component of the expansion of Bauxite Hills is the construction and mobilisation to Skardon River of a Shiploader or Floating Terminal.

Rocktree Consulting, which has been involved in the design, engineering and construction of more than 20 floating terminals over the past two decades has been key to determining which FT design was best suited to Bauxite Hills, its expanded production rate and the prevailing loading conditions at Skardon River.

The preferred FT design consists of a 100m barge, equipped with two cranes and a materials handling conveyor and stacker system that will have the ability to load up to 40,000 tpd of bauxite.

An ability to load different sized OGVs will enable Metro to realise significant freight savings, whilst maintaining customer flexibility with the ability to still load smaller OGVs.

Further work by Rocktree Consulting over the next one to two months will allow accurate supplier and construction quotations and a more definitive schedule to be developed. The process will include finalisation of the cost of all the equipment, identification of a high-quality shipyard for construction, finalisation of the schedule and construction methodology and a plan for mobilisation to Skardon River.

Transhipment scale up

Metro will supplement its production and logistics chain at Bauxite Hills to ensure mining and transhipment rates match the increased loading capacity.

Twenty-four hour rehabilitation for the mining and haulage fleets will be introduced, whilst the remaining 3500 tonne barges will be replaced by larger 7000 tonne barges. Two further barges will be introduced to generate economies of scale for transhipment.

Port upgrade

Metro will also modify the port area to ensure the capacity to load at the required rate is met.

To do this, it will upgrade the feeder system to provide additional screening capacity and modify the Barge Loading Facility to increase capacity to ~2,000tph.

Furthermore, it will increase ROM stockpile area to allow larger stockpiles to be maintained during the operating season. Additional accommodation units will be installed and camp facilities expanded to manage the larger workforce.

The release of today’s DFS paves the way for Metro to improve the efficiency of its operation, build its customer base in China and determine the optimum way to maximise long-term returns from the project.

The company would seemingly have everything investors are looking for in a mining group — a long life mine, established production, offtake agreements in place, robust margins, profitability and the scope to improve its already strong margins should the anticipated doubling in production occur over the next few years.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.