Market Reacts: EXR flow test result… and what’s next.

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 2,989,000 EXR Shares and 1,743,096 EXR Options at the time of publishing this article. The Company has been engaged by EXR to share our commentary on the progress of our Investment in EXR over time.

A disappointing few days for this stock...

... but has the market over-reacted?

Six months ago, Elixir Energy (ASX:EXR) flowed 2.5mmcf/day from just ONE out of 6 zones at its Queensland gas project.

This was deemed to be a “commercial” flow rate - the deepest unstimulated flow of gas onshore Australia east of the Perth Basin.

Then, after some unexpected delays, EXR went back to flow test the remaining 5 zones...

We expected that if one single zone flowed 2.5mmcf per day, surely the combined 6 zones would flow more...

And so did the market.

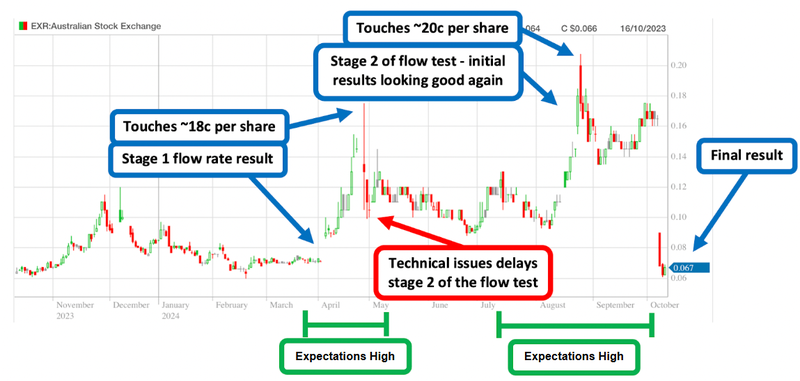

The EXR share price ran from 6.5c to a high of 20c in anticipation of the 6 zone flow rate and how big it could be.

The result of the combined flow rate testing was released on Tuesday.

The stabilised flow rate from five out of the six reservoirs came back at 1mmcf per day.

Less than the initial single zone result...

And you guessed it... the market didn't like it.

The market wanted a “bigger than 2.5mmcf flow rate” and some more epic flaring photos with an even bigger fireball this time around.

EXR gave some reasonable explanations for why the flow rate was down on its previous numbers.

The lower than anticipated flow rate may have been caused by the multiple previous opening and closures of the well.

EXR MD Neil Young will be holding a webinar next Thursday, where we expect to get a much more detailed explanation of what happened, and what the forward plan will look like.

The webinar is next week Thursday the 17th October 2024, 12:00pm AEDT/ 9:00am AWST - the link to register for it is here.

Today we will unpack in detail this week’s news from EXR, and what to expect next.

So, the market wanted at the very least to see a better flow rate than the initial 2.5mmcf per day - and that made sense given EXR was testing flow rates from more zones.

With the lower than expected result on Tuesday, the share price got smacked back down to a low of 6.1c by Wednesday.

Was it oversold on the day?

Probably.

This usually happens in the day or two after a results announcement that doesn’t meet expectations, during “peak uncertainty” while investors try to rapidly digest the breaking news.

When in doubt... itchy trigger fingers come out.

The share price moves of the last few days are a reminder about the risks involved in early stage gas exploration.

These early stage tight gas plays can be tricky to get right, and while it's tough to think about fresh off a negative market result, it's true that success or failure can’t be attributed to a single well.

After the “post announcement sell off”, the EXR share price came back yesterday, trading up to ~7c from a low of 6.1c for the week.

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

With our EXR Investment, we did what we typically try to do with all of our Oil and Gas Investments.

We partially de-risked our Investment as we got closer to the final results from the flow test.

The only difference from our normal strategy this time was that we also added to our position a few weeks before the final result in the 10c placement.

We are currently holding more EXR shares than we were at the commencement of our current EXR Investment Memo #2 which commenced in March 2023.

All in all, in hindsight we probably held onto a little more than we usually would have going into Tuesday’s announcement, but we had high hopes for the result at the time.

So what happens now? Daydream... 3?

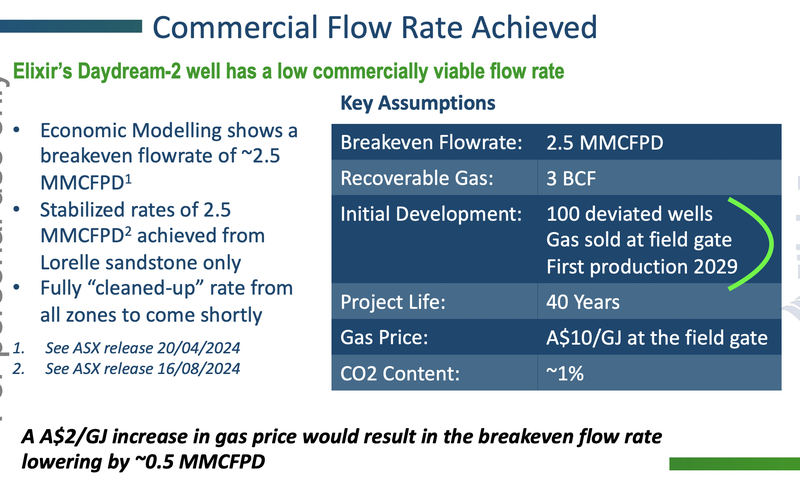

Daydream-2 well will be retained as a potential future gas producer.

All licence commitments have now been met for ATP 2044 (this is what the area of the project is called), and EXR will now apply for the licence to be deemed a retention lease. In Queensland this is called a ‘Potential Commercial Area which has a maximum term of 15 years.

EXR is already planning Daydream-3 which is good to see.

At this stage it's too early for us to speculate on what Daydream-3 would look like and the timing of it, and it will be interesting to see how EXR chooses to progress the project.

EXR’s MD Neil Young mentioned in this week’s announcement, “We expect our discussions with potential partners will now likely be accelerated”.

EXR still maintains a 100% working interest in the project - which means it could look to farm down a portion of it at some point in the future.

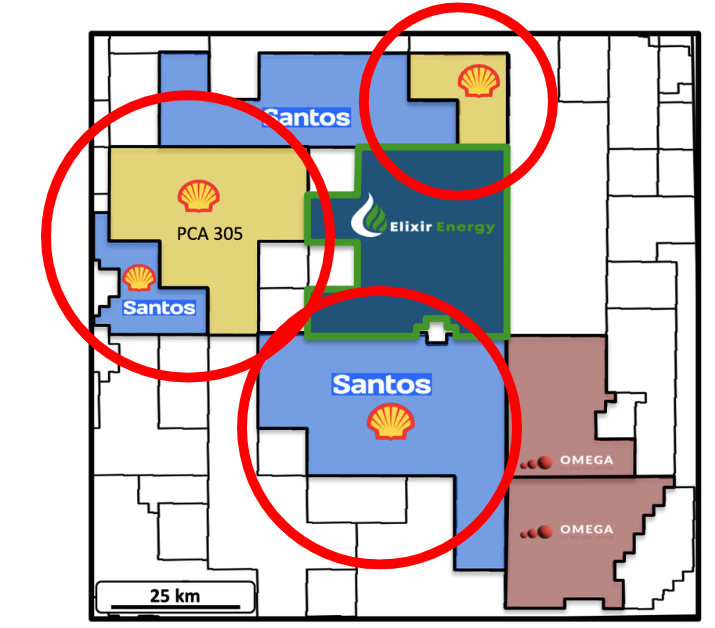

Remember Shell and Santos have ground next door to EXR.

(We know from media reports that Shell is fairly active in its drilling and exploration of the same Taroom Trough)

We think whatever comes from those discussions will ultimately form the basis for the size/scale of the next program.

It makes sense that a major partner would prefer to make a decision with more data then less.

From a technical & data perspective we think EXR is in a stronger position now than it was before the flow test results (regardless of the result) to get a partnership deal done.

Taking a step back, over recent months EXR has managed to:

- Increase the 2C contingent resource by 328% to 1.47 trillion cubic feet of gas.

- Increase the overall prospective resource by 180% to 3.6 trillion cubic feet of gas.

- Flow gas from five out of six stimulated zones

- Deliver what the company considers a commercial flow rate.

All of these technical milestones are big for a small cap company like EXR AND exactly what the majors are looking for in their data rooms.

(Energy majors are sophisticated, slower moving beasts that don’t judge the potential of an entire basin on a single flow rate result like smaller speculators do)

It's also important to note Daydream-2 was EXR’s first well on this project.

The goal was not to get the asset into gas production but rather to show a major partner that the asset is capable of being brought into production with the right expertise/approach (and funding).

The development scenario of ~100 deviated wells, which EXR flagged in a recent presentation, was always going to require some sort of major farm-in partner at some point.

(Source)

An analyst note we saw this week from Taylor Collison’s Andy Williams was especially interesting, it pointed out:

- The comparisons between the Taroom Trough and the Beetaloo Basin

Taylor’s analyst said that the “play stands at the same point that the Beetaloo Basin operators did some three years ago” where most of the market believed it would never come to market.

Now the Beetaloo is looking like it will get into first production by mid-2025.

- Pipeline/infrastructure advantages of EXR’s project

The report also mentioned all the existing infrastructure in the Taroom Trough relative to the Beetaloo which adds to potential for the play to work.

Interestingly, Taylor’s maintained their “Speculative Buy” on EXR with a “NAV range of $0.27-0.58/share”.

This is a significant premium to today’s price, but also note that price targets are based on a number of assumptions that may not eventuate. Never invest on an analyst price target alone.

We are long term Investors in EXR, having been Invested in the company for many years now.

We continue to back EXR MD Neil Young and the team to advance its Queensland gas project and realise the true value of the asset.

So for now, we just wait to see where the market will end up pricing EXR after the knee jerk sell off has finished.

And, as sophisticated technical O&G investors understand and process the results.

... as anticipation for the next drill and flow test builds.

What EXR achieved with Daydream-2

This has been a 12-month long appraisal program for EXR and the company has learned a lot of new information through its drilling campaign.

The project has been advanced and EXR is in a more informed position compared to 12 months ago.

During drilling and flow testing at Daydream-2 EXR has managed to take the asset a long way forward...

Although the headline flow rate results for 6 zones was not what we were hoping for (based on the initial flow rate from that single zone), EXR did manage to accomplish a lot over the last 12 months.

During drilling and flow testing at Daydream-2 EXR has managed to take the asset a long way forward. As we noted above, EXR managed to:

- Increase the 2C contingent resource by 328% to 1.47 trillion cubic feet of gas

- Increase the overall prospective resource by 180% to 3.6 trillion cubic feet of gas.

- Flowing gas from five out of six stimulated zones and achieving what the company considers a commercial flow rate.

Let’s take a look at each of these in a bit more detail.

2C contingent resource increased 328% to 1.47 trillion cubic feet of gas

EXR has taken resources out of the prospective category and into a higher confidence “contingent category”.

This is good progress, especially considering this is the sort of data a major farm-in partner would look at when considering doing a deal with a small cap like EXR.

Increased the overall prospective resource by 180% to 3.6 trillion cubic feet of gas

This is something that we think a major farm-in partner would be taking a look at.

EXR’s project is right in the heart of the Taroom Trough next to major players like Santos and Shell, as well as Omega Oil & Gas.

Increasing the prospective resource is something that we think a major farm-in partner would look at when deciding whether or not the upside would be worth farming into.

EXR has flagged in the past the possibility of a large player coming to farm-into the project, so it is a “watch this space” from our end.

EXR flowed gas to surface from five of six simulated gas reservoirs...

AND EXR did so at rates it considers “commercial”.

This is important technical data that de-risks the project from an exploration perspective.

Again, we think that this is the type of information that a major farm-in partner could look at in a data room and figure out whether or not they can bring a different approach/expertise to unlock higher flow rates.

Our view is that IF EXR is able to lock in some sort of partnership it will be in a far better position to advance its Queensland gas project which is the basis for our EXR Big Bet as follows:

Our Big Bet for EXR

“EXR to achieve a $1BN market cap through successfully advancing one or more of its three projects: its Mongolia gas project, Mongolia green hydrogen project, and/or its Queensland gas project.”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our EXR Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

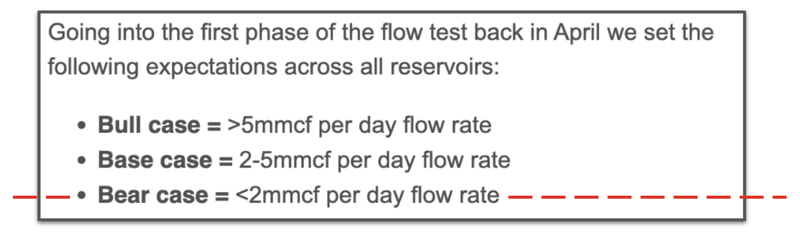

How did EXR perform relative to our pre-flow test expectations?

Going into the flow testing program, we set the following expectations for EXR:

After the first phase EXR flowed 2.5mmcf per day and hit our “base case” expectation.

With only one of the reservoirs tested in that first phase, we thought the company could multiply its flow test after all of the reservoirs were tested together (the market did too).

We covered those results in a previous note here: EXR delivers commercial gas flow rates - 5 more zones still to be tested

That first result was from just one of the six reservoirs EXR had planned to test with this flow test.

As a result, we thought there was a good chance EXR could upgrade its overall flow rate after the second stage of testing was finished.

We expected an upgrade - but instead got a surprise downgrade...

EXR’s final results were:

- A MAX flow rate of 2.6 mmscf per day - this would have put EXR’s result into our “base case” scenario.

- A stabilised flow rate of 1 mmscf per day - this puts EXR’s final results into the “bear case” scenario.

This week’s result hit our “bear” case scenario and the market movements this week reflected this.

What did go wrong

The key risk that materialised for EXR was “Development Risk”.

Although EXR managed to secure a stable flow rate, the flow rate by itself fell below the threshold which EXR had previously said was commercially viable.

Development Risk (Risk Materialised)

EXR has so far managed to de-risk the project from an exploration perspective by flowing gas to surface.

Following the flow test, the focus will begin to shift to moving to the development stage, which is likely to require significant capital investment - ideally from a partner.

Source: Shell flared gas in the Taroom Trough - next door to EXR

Things can and do go wrong with early stage exploration and when a risk materialises, generally the share price will fall - this is what we saw this week.

The key is to understand what is coming up next for the company, and what position it is in from a cash perspective to deliver on the next phase of development.

Our EXR Investment Memo

Our Investment Memo provides a short, high-level summary of our reasons for Investing. We use this memo to track the progress of all our Investments over time.

Below is our EXR Investment Memo, where you can find the following:

- What does EXR do?

- The macro theme for EXR

- Our EXR Big Bet

- What we want to see EXR achieve

- Why we are Invested in EXR

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.