MAN announces 3.3Mt maiden lithium resource - Lithium brine projects attracting market attention.

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 10,360,000 MAN shares at the time of publishing this article. The Company has been engaged by MAN to share our commentary on the progress of our Investment in MAN over time.

A large US lithium resource has just been defined.

...just as sentiment for lithium starts to improve.

A few weeks back we saw Rio Tinto pay $9.9BN for Arcadium Lithium and its brine assets.

(lithium brine hopefuls Galan, Lake and Vulcan have all risen between ~20% to ~100% from the day this was announced)

Mandrake Resources (ASX:MAN) is also going after lithium brines - in the USA.

MAN has just released its maiden JORC mineral resource estimate at its lithium project in Utah, USA.

A 3.3Mt Lithium Carbonate Equivalent (LCE) at an average of 86 mg/L lithium.

The resource is more than 2x bigger than MAN’s neighbour $105M Anson Resources.

But MAN has a much smaller market cap at ~$16M.

MAN also had $14.9M cash in the bank at 30 June - meaning the company’s enterprise value is just ~$1.1M.

We increased our Position in MAN a few months ago - it’s been a lithium winter so valuations are quite attractive - and we anticipate a lithium turnaround at some point.

(like we were doing with advanced stage silver stocks when nobody really liked silver... which worked out for us).

We also had some great success with a “bottom of the lithium cycle” lithium brine pick up just before the last lithium run - in Vulcan.

MAN’s resource was defined with very little cash spent.

A low cost well sampling program at the start of the year, combined with plenty of historic data, has now led to a large lithium resource.

MAN is yet to conduct its own direct well exploration, and will target a well re-entry program to increase the size and concentration of the resource.

While grade is important to almost all mining projects, what makes or breaks a lithium brine project is how suitable it is for processing/extraction technologies.

Where traditionally evaporation ponds have been used to extract lithium from brines, the location of MAN’s project is not ideally located for this, so it will need to rely on novel DLE (direct lithium extraction) technologies.

On that front - MAN is working with two different DLE tech providers:

- Rio Tinto backed ElectraLith - who have managed to produce 99.9% pure battery-grade Lithium Hydroxide from MAN’s brines.

- Bill Gates backed Electroflow - who have shown 92% recoveries and the ability to convert MAN’s brines into lithium hydroxide without any chemical pre-treatments.

MAN will work with both DLE technology providers to see which works best on its brines.

A partnership like this is a big cost saving for MAN as it doesn’t need to come up with the DLE technology itself.

MAN can do what all junior mining exploration companies do best, find and extract minerals - leaving the chemical wizardry to the experts.

MAN’s resource much bigger than its $105M neighbour

MAN has a regional peer - Anson Resources - with a defined resource only half the size of MAN’s.

Anson is capped 5 times more than MAN - we suspect this is because the assets have advanced further than MAN - we think what it does show is the upside in MAN as they progress its project.

We think this defined resource also sets MAN up nicely to advance additional commercial discussions.

MAN has quite a bit going for it in Utah from a valuation, operational and jurisdictional point of view:

- USA is actively trying to grow its lithium industry to compete with China.

- Utah a great place for developing resources - Utah is a mining friendly state and MAN’s project is near infrastructure to support the project.

- Big lithium resource that can grow - MAN’s resource is more than twice as big as Anson Resources which is capped at $105M.

- Potential for further upside from re-entry programs - MAN is targeting reservoirs with higher lithium concentrations in a cheap re-entry program. This could expand the resource and improve its concentrations.

- Strategic partnerships with two DLE tech providers, one of which has been backed by Bill Gates backed Electroflow and the Rio Tinto backed Electrolith

- MAN is almost trading at cash backing (prior to today’s news) - the market is placing almost no enterprise value on these assets.

We are now just waiting for lithium sentiment to turn back to neutral/positive after it recovers from the hangover caused by a face melting run a couple of years ago.

We saw how quickly sentiment can flare up from indifference/apathy with gold and silver just this week.

While many early stage companies moved to acquire "hotter" commodities during the lithium winter, MAN stuck to its guns during the lithium winter.

So this should position MAN for a strong run when lithium sentiment returns

Today we will check in on the current lithium environment in general, then focus in on MAN’s asset and newly defined JORC resource.

Sentiment check - What's happening in lithium today?

Rio Tinto is buying, China is cutting production... is this the bottom of the lithium market we have been waiting for?

The past 18 months has felt like “lithium winter”.

The frenzy of 2020 and 2021 off the back of a soaring lithium price saw new projects, new regions and new technologies emerge in the lithium space.

However, now the lithium carbonate price trades at US$10,500, nearly a 90% fall from its peak in 2021.

The supply side of the equation has reacted, with many of the large lithium producers cutting production.

And on the junior end of the market, exploration companies have “returned to the drawing board” with new projects, chasing the next shiny commodity.

Lithium sentiment of the past 18 months:

BUT, there are signs that the lithium market is set to turn, and potentially the lithium bulls will come back too.

What does the Rio Tinto $9.9BN acquisition have to do with MAN?

Two weeks ago Rio Tinto announced the acquisition of Arcadium Lithium for A$9.9BN in an all cash deal, representing around ~8.5% of the mining giant’s market cap.

(Source)

This deal, by one of the world’s largest mining companies, is a big, bold bet on lithium.

But in particular, a big bet on lithium brine (and subsequently DLE).

DLE is a technology that converts the lithium pulled from underground brines into usable lithium carbonate for batteries.

This technology is novel, and is yet to be used at scale.

However, if DLE technology works, then it could be cheaper AND more environmentally friendly than other forms of lithium production such as hard rock mining.

After the deal was announced, Rio CEO Jakob Stausholm said “(DLE) is actually the solution to provide the lithium that the world needs... There's a lot ahead of us and we haven't explored it fully, yet it's the right technology".

When one of the largest miners in the world bets on a technology, it helps to pay attention.

As mentioned earlier in today’s note, MAN is working with two DLE tech providers:

1. ElectraLith - a DLE provider that is backed by Rio Tinto - to produce battery grade lithium hydroxide.

2. Electroflow - a DLE provider backed by Bill Gates’ $2BN “Breakthrough Energy” (BE) Group. The same group that backed Lilac Solutions which is being used on some of the biggest brine projects in the world.

To date, ElectraLith has been able to produce 99.9% Lithium Hydroxide with MAN’s brine and Electroflow have produced Lithium Hydroxide with 92% recoveries.

Next, MAN will undertake a well re-entry program to secure more brine for testing which will inform a maiden Scoping Study over the project.

We are looking forward to this one as it will give us a first look at potential economics around the project.

How lithium stocks are reacting to recent sentiment signals

Since the announcement by Rio Tinto, the share price of some of the beaten up lithium companies that were popular in the 2021 bull market started to run again.

In particular Vulcan Energy Resources (which is still our best ever Investment), Lake Resources and Galan Lithium:

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

We think this is just the market reacting to big M&A interest in the sector.

When share prices are falling, selling invites more selling and investors usually rush for the exit, no one really thinks about “fundamental values” of companies when this is happening.

Sometimes it takes a big M&A deal (or a few - long time readers would know of the $560M Latin Resources and Pilbara Minerals deal) to wake investors up to the fact that the selling may have gone too far.

All of a sudden investors start running the numbers on companies with bombed out share prices and realise there is actually value in the projects they own - value that might attract M&A interest from a big company like Rio Tinto.

This sort of trading indicates to us that the bottom of the market may be in or at least getting very close - especially in those companies with brine/DLE assets.

Chinese lithium production cuts

Another indicator that we may have hit the bottom of the lithium cost curve was the production cut in CATL’s Chinese lepidolite mine:

(Source)

Lepidolite is a fancy way of saying “low grade hard rock” mine.

It has been a bit of a mystery to the western world how these low grade mines could continue to operate profitably in China.

Given the vertical integration of China’s EV supply chain, it is believed that these mines are run at a loss and profits are made further downstream.

Lepidolite mines, like the ones that CATL just paused, contribute to the annual lithium demand picture, and keep other projects higher on the cost curve honest.

However, with these mines now cutting supply it is an indicator that we have hit the bottom for lithium (particularly if these mines were running at a loss to begin with).

With supply scant, we think that any sudden spur of demand could turn prices quickly.

How quickly can lithium prices bounce back?

For lithium, demand is driven by the batteries in electric vehicles (EVs).

In 2023 there were 92.7 million new cars sold, and only 15% of those were EVs.

Although the majority of car manufacturers have pushed back their ambitious timelines to reach 100% electric vehicles by 2030, we still think that the long term outlook for EVs remains strong.

And although ramp up is much slower than anticipated, policy drives urgency and urgency drives demand.

We see the future as electric, even if it takes five, ten or twenty years...

This means that there will be a big future for lithium too, as miners set up the production for the anticipated electric vehicle demand in the future.

Just like Rio Tinto, we think that this could be the bottom of the market for lithium companies, and we hope that MAN can ride that wave.

Our MAN “Big Bet

“MAN returns 1,000%+ by making a lithium discovery significant enough to move into development studies, or attract a takeover offer.”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved, and it will require a significant amount of luck. There is no guarantee that it will ever come true. Some of these risks we list in our MAN Investment Memo.

More on MAN’s JORC resource

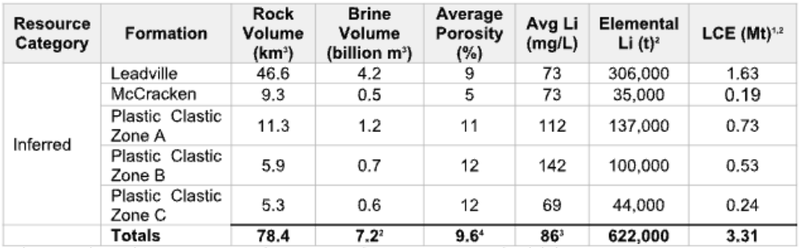

So, today, MAN published the results of its lithium JORC resource.

An inferred mineral resource of 3.3Mt Lithium Carbonate Equivalent (LCE) at an average of 86 mg/L lithium.

MAN built its resource from the data, logs and cores of old oil wells - and will soon conduct a well re-entry program to improve the JORC resource size and concentration.

So this looks like it could be just the start.

There are six key things to evaluating a brine project and the JORC resource:

- Lithium Content

- Lithium concentration

- Extraction technology (evaporation pond OR DLE)

- Project Location

- Ability of Brine to Flow (porosity)

Let’s take a look at each one in closer detail.

Lithium Content

The JORC resource published showed 3.31Mt of LCE.

This is bigger than neighbouring company Anson Resources which has a JORC resource of 1.5Mt.

Size matters when it comes to a JORC resource - as the bigger the resource - the more valuable the asset.

Lithium Concentration

MAN’s resource has an average lithium concentration of ~86mg/L.

As we mentioned earlier, when it comes to brine assets, grade (concentration) isn't the only thing that matters.

What matters more is whether or not a project can be processed into final saleable lithium chemicals.

As for how the market values these assets - other assets with similar grades trade at market caps a lot higher than MAN’s.

For example, there’s the $98M capped E3 Lithium, which has a project in Canada.

E3 Lithium has a concentration of 75.5mg/L (source), and Anson Resources’ more advanced project has an average concentration of ~112ppm.

We also note there is plenty of scope to increase MAN’s concentrations - which is what we want to see from MAN’s upcoming well re-entry program.

MAN’s resource has been put together off historical data that was initially used for oil & gas exploration NOT for lithium...

So, with a more targeted approach we hope that MAN can improve on this number.

Extraction Technology

Even more important than lithium concentration is the quality of the extraction technology.

MAN is using a DLE (or direct lithium extraction) process, and working with two different technology providers to yield the best results.

One backed by Bill Gates (Electroflow) in the US, the other backed by Rio Tinto (ElectraLith) in Australia.

As we mentioned before, both have already shown they can process MAN’s brines - with ElectraLith producing 99.9% pure battery grade lithium hydroxide.

Both DLE providers have indicated that they will be building pilot plants to process MAN’s brines.

This partnership is a big cost saving for MAN as it doesn’t need to come up with the DLE technology itself.

MAN can do what all junior mining exploration companies do best, find and extract minerals.

Leave the “technical magic” to the experts.

The process costing from Electroflow and ElectraLith will directly inform MAN’s project Scoping Study which will evaluate the feasibility of a commercial lithium hydroxide production.

Project Location

MAN’s project is based in Utah, USA.

The US is desperate for more domestic production of critical minerals, and MAN has already secured $1M in grant funding from the Department of Energy.

Last month, MAN’s neighbour Anson Resources, signed a Letter of Intent for a US$330M loan from the Export Import bank of the United States.

This shows how interested the US is in more domestic lithium.

We think that the US government may continue to support MAN’s project, and MAN has two outstanding grant applications with a third application to be submitted in November.

Porosity

Porosity is a measure of how easily the brine can flow.

When porosity is higher, this generally means it is easier to pump brine to the surface.

MAN’s overall porosity results are 9.6%, which is roughly in line with other much larger capped companies’ brine projects.

Overall take - good start, and more upside

Ultimately, we would say that this result for MAN hits our “Base Case” scenario.

Although the defined concentration is low now, the contained lithium carbonate was large.

MAN has achieved this resource spending very little cash, and the resource sets the stage for additional improvements as focused work really fires up.

The resource provides a good platform for MAN to improve on with a well re-entry program and deliver on a Scoping Study.

It may attract interest from partners in the US now that the resource is defined.

To learn more about evaluating lithium brine projects read: 🎓Lithium projects explained: Brines

What is next for MAN?

MAN has a slew of newflow to come, and we think that the next nine months will be telling for the company.

MAN is well funded, with A$14.9M in the bank, to deliver on all of the following milestones.

Well Re-Entry Program

With the well re-entry program MAN will target the highest lithium concentration reservoirs, to hopefully upgrade the lithium concentration in the JORC resource.

This program will be specifically designed with this goal in mind, and is a more targeted approach compared to the evaluation of historical data used to establish the Maiden Resource.

🔲 Program commenced

🔲 Well re-entry results published

🔲 Brine processing results published

🔲 JORC Resource Upgrade

🔲DLE Pilot Plant Testing

MAN intends to supply bulk brine samples to its two DLE tech providers to test out pilot plants for the production of battery grade lithium.

🔲ElectroFlow results

🔲ElectraLith results

🔲 Scoping Study (Complete H1 2025)

Expected to be complete in the first half of 2025, MAN’s initial Scoping Study will give us a first look at the potential economics of any lithium brine project over the area.

🔄 Further Government Funding

MAN has two outstanding grant applications with the US Government and a third application to be submitted in November.

What could go wrong?

The two key risks we see for MAN in the short term are “Exploration risk” and “Processing risk”.

From our February 2023 Investment Memo:

Exploration risk

MAN’s lithium project is still relatively early stage considering the company just recently got a hold of its leases. There is always a risk that the company’s exploration programs yield no notable drill results and there is no economically viable lithium resource over its ground.

Source: “What could go wrong” section - MAN Investment Memo 24 Feb 2023

Exploration risk is still a key risk to our MAN Investment Thesis.

MAN is yet to drill its own well and is doing most of its work based on data from old oil and gas wells.

There is always a risk that when MAN go in and drill their own wells, the data does not correlate with what MAN is seeing to date OR that results aren't as strong as previously expected.

As a result exploration risk is still something we note going forward.

Processing risk

MAN’s lithium project is hosted in brines. This means that for the project to be processed economically the company needs to find a suitable processing technology for its type of material. Typically this is a type of Direct Lithium Extraction (DLE) technology.

Source: “What could go wrong” section - MAN Investment Memo 24 Feb 2023

As MAN moves away from development and towards feasibility studies a new risk will emerge, which is “feasibility risk”.

There is no guarantee that the project is economically feasible.

However, if MAN is able to mitigate processing and exploration risk, then it will help support a more feasible project.

A Scoping Study will provide a detailed and independent account of the project economics, and hopefully help to evaluate the extent of the “feasibility risk” over the project.

Our MAN Investment Memo

In our MAN Investment Memo, you can find:

- MAN’’s macro thematic

- Why we Invested in MAN

- Our MAN “Big Bet” - what we think the upside Investment case for MAN is

- The key objectives we want to see MAN achieve

- The key risks to our Investment thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.