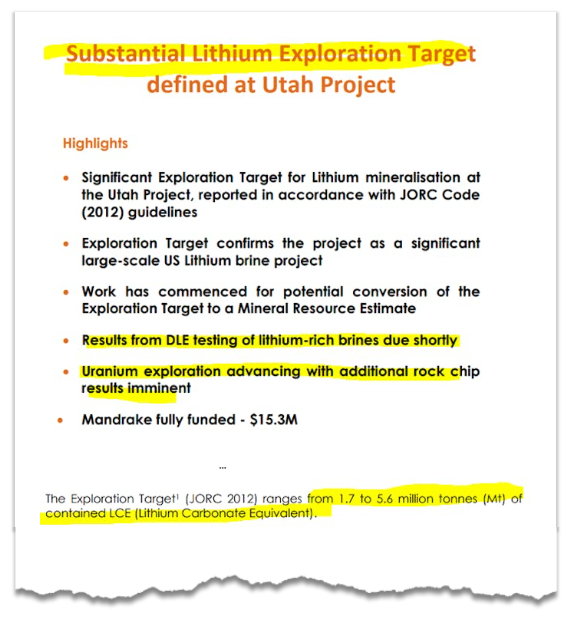

MAN announces 1.7M to 5.6M ton exploration target as lithium sentiment improves.

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 2,860,000 MAN shares. The Company has been engaged by MAN to share our commentary on the progress of our Investment in MAN over time.

The lithium market is edging up off its lows.

Lithium stocks are showing back to back green days.

(Source)

A great backdrop for our Investment Mandrake Resources (ASX:MAN) to announce its lithium exploration target...

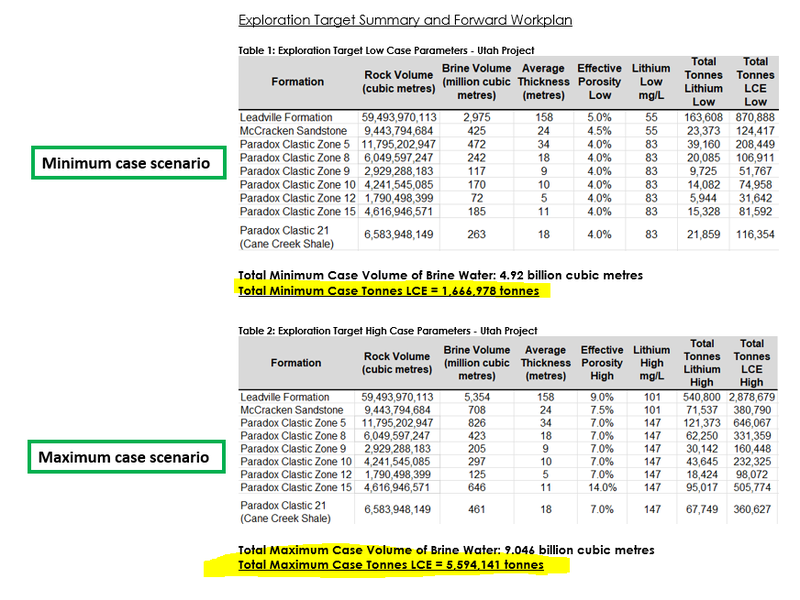

It's between 1.7mt and 5.6mt of contained LCE (Lithium Carbonate Equivalent).

(Source - layout modified from original to highlight exploration target)

This lithium target news comes just two weeks after MAN announced rock chip samples that it submitted to be tested for URANIUM were deemed too radioactive to be handled by the assay lab.

MAN’s radioactive uranium rocks had to be sent to a better equipped lab.

We are expecting uranium grades from those samples any day now...

Anything above 1% uranium would be exceptional.

But back to the 1.7mt and 5.6mt of contained LCE exploration target MAN just announced.

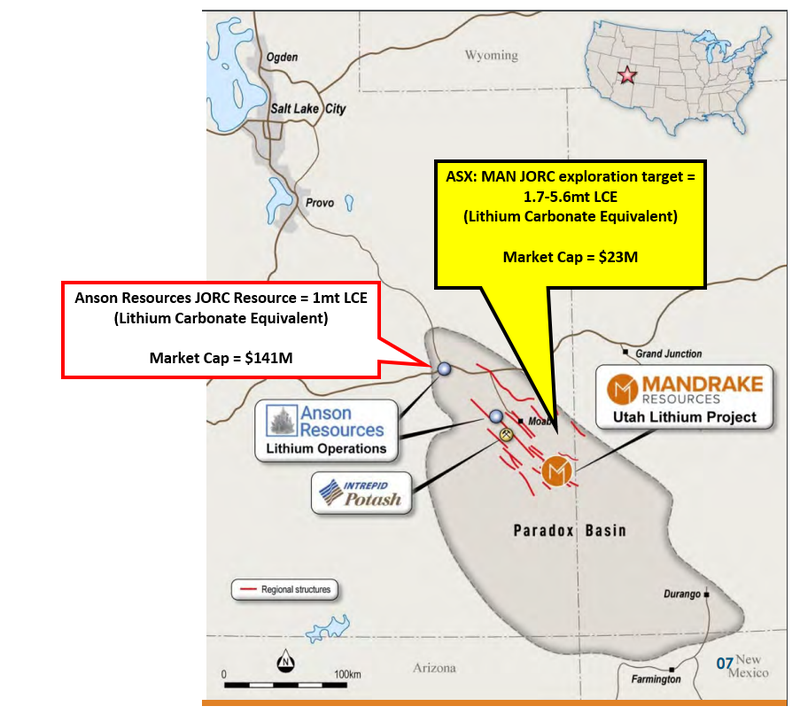

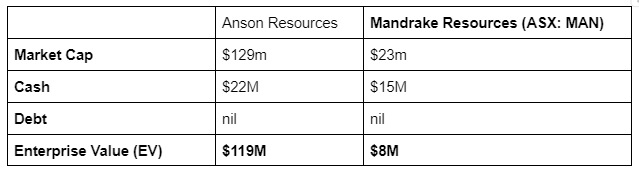

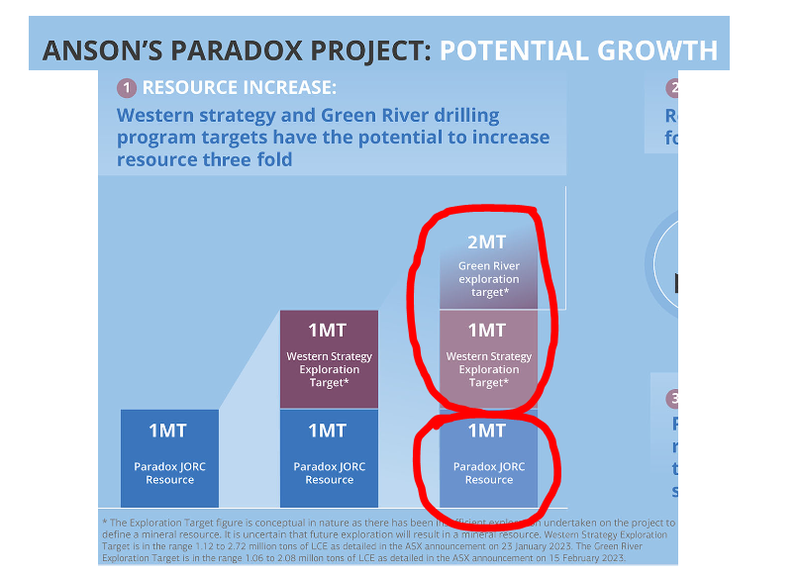

For context, the $141M capped Anson Resources, ~100km from MAN, has a JORC resource of ~1mt contained LCE and exploration targets of a further ~3mt of contained LCE.

So MAN could, at minimum, define a JORC resource bigger than Anson and, in the best-case scenario, have one that is ~5.7x its size.

MAN is currently capped at $23.4M and has $15.3M in cash - an Enterprise Value of $8.1M.

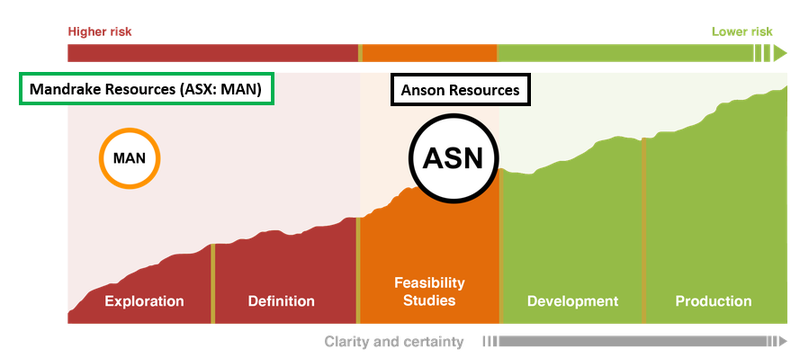

The key difference between the two companies is that MAN is pre-resource definition whereas Anson Resources is already post DFS and is a lot closer to development for its project.

We are Invested in MAN to see it prove up its resource, run feasibility studies and progress its project to the same point Anson finds itself in.

As MAN works up its project, we are hoping it bridges the gap in terms of valuation to a level similar to Anson’s (and we hope higher).

Right now, Anson’s Enterprise Value (EV) is ~15x higher than MAN’s.

We expect to see MAN re-enter its first well in the coming months and to deliver a JORC resource as soon as the re-entry programs are finished.

We are hoping that coincides with a run in the lithium price & positive sentiment in the sector overall...

Of which we are starting to see green shoots:

(Source)

We see plenty of upside in MAN’s valuation in a scenario where sentiment in the lithium market is positive and MAN delivers major catalysts to the market.

Not to mention the uranium aspect to the MAN story - those rock chip samples are due soon.

We think MAN now has four major catalysts that could re-rate the company:

- JORC Lithium resource 🔄

Today’s exploration target is the first time we have seen the size/scale potential of MAN’s project compared to its peers.

Ultimately though, we want to see MAN convert the exploration target into a maiden JORC resource.

This would give the market a reference point to value MAN appropriately to the other players in the US lithium brine space.

We will see how the market reacts to this catalyst, and even though lithium prices remain depressed, we’ve seen firsthand how much interest there is in the US for new lithium projects.

Read: Arkansas Lithium Summit - lithium come back?

- Re-entry/drill program for Q1/Q2 2024 🔄

MAN’s re-entry/drill program will form the basis for the drill results that feed into a JORC resource estimate.

The potential upside for the drill program could come from the lithium concentrations MAN intercepts during its drill/re-entry program.

At the moment MAN’s exploration target has concentrations ranging from 55 to 101 mg/L.

Neighbour Anson’s resource is based on an average concentration of 124 mg/L. (Source)

BUT there is historical data from a nearby well that shows there is a chance MAN could intercept concentrations a lot higher than the market may expect.

The historical Peterson 88-21 well which was drilled in 1959 sits <1.6km outside of MAN’s acreage and showed lithium concentrations of ~340 mg/L.

That shows concentrations ~340% higher than the maximum used in MAN’s exploration target.

Meaning that IF MAN is able to deliver concentrations anywhere close to the 340 mg/L levels then it could mean a much bigger JORC resource then even the market expects.

- DLE testing results 🔄

The third major catalyst could be with respect to DLE partnerships.

In a late January announcement where MAN announced the discovery of lithium on its project, said larger bulk samples have been sent to two Direct Lithium Extraction (DLE) providers, Electroflow and an “advanced Australian based DLE firm.”

And furthermore, the results are due “shortly”, in Q1/Q2.

When it comes to lithium brines in the US, DLE tech working can make or break a project. So we think the DLE news could be a big de-risking event for MAN.

The market generally reacts well to DLE news too.

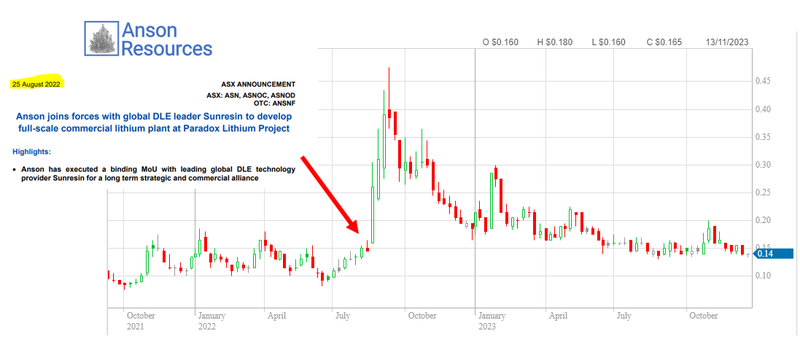

Back in June 2022, Anson announced an MOU with Sunresin for a partnership on applying DLE to its project.

Following that news, Anson’s share price went from ~14c to just under 50c per share.

At the end of that run, Anson’s market cap peaked at ~$490M.

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

If MAN can get its brines to work with either of the two DLE providers, this could help re-rate MAN’s valuation, particularly if the JORC resource comes in above expectations along with an improving lithium price.

- NEW: Imminent uranium exploration wildcard 🔄

MAN has moved quickly to explore for uranium on its extensive land holdings in Utah, at a time when the uranium spot price is near 16 year highs.

Uranium is big in the Lisbon Valley where MAN is exploring - so MAN is in the right spot. There’s a host of juniors, plus larger players such as Energy Fuels (NYSE: UUUU - $1.5BN market cap).

So far MAN has delivered the following from 6 rock chip samples with grades as high as 0.55%.

Assay results from the remaining three rock chip samples are due this month - these are the rodcks that were rejected by assay labs for being too radioactive so we are keeping a close eye on these results.

Read: MAN uranium samples rejected by assay laboratory for being “too radioactive”

US lithium brines - MAN working on DLE partnerships

We think that US lithium brine is the place to be right now.

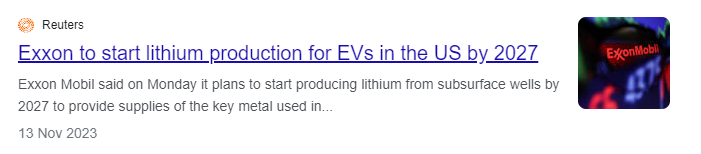

In early 2023, $587BN capped energy supermajor ExxonMobil paid at least US$100M for an early stage lithium brine asset in another part of the US.

Exxon is now looking to get its projects into production by 2027.

(Source)

At the moment the US produces ~1% of the world's lithium and has close to no hard rock resources.

So, we think unlocking the lithium brine projects around the US is the key to securing the domestic US lithium supply.

Tech advancements in the Direct Lithium Extraction (DLE) space are the key to unlocking US lithium brine projects.

DLE is a technology that extracts lithium from brine water pumped from deep underground. The lithium is separated from the brine, and the brine is pumped back underground, closing the loop.

While the technology is relatively novel in the lithium space, similar tech has been applied across the oil & gas industry for decades.

That's why Exxon’s entry into the US lithium brine space was a big turning point for the whole space.

Exxon has been drilling wells, pumping hydrocarbons to the surface and processing them into saleable fuels for decades.

Now it has a US$31BN strong balance sheet it can deploy to cracking the DLE code.

Our Investment MAN entered the lithium brine space some 3 months before Exxon did - yes, ahead of the multi-billion dollar energy supermajor.

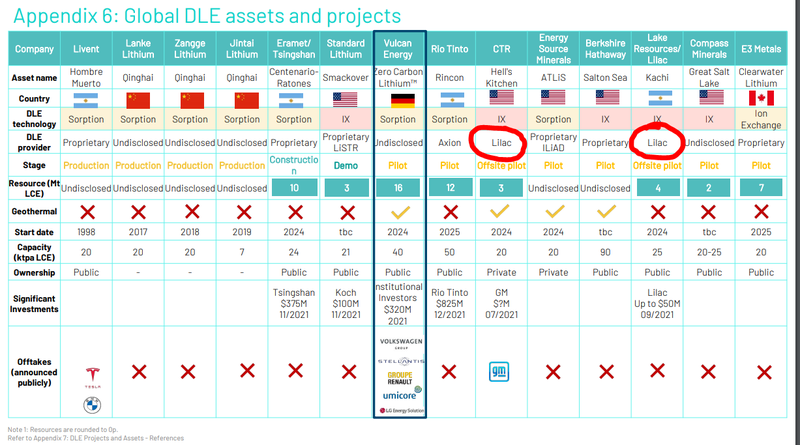

MAN has already signed one partnership with a DLE tech provider (Electroflow) that is backed by Bill Gates’ Breakthrough Energy Group.

Gates’ Breakthrough Energy Group was also behind a US$20M investment in Lilac Solutions - one of the industry leaders in DLE technology - so the group know the space relatively well.

(Source)

Lilac’s tech is being used in some of the biggest brine projects in the world.

MAN currently has bulk samples being tested by two Direct Lithium Extraction (DLE) providers, Electroflow and an “advanced Australian-based DLE firm.”

Depending on the results of that test work, we think that a DLE partnership could be a big catalyst for MAN.

Our Analyst’s take on the US lithium brine space

One of our analysts recently got back from a trip to a DLE research facility in the US, and attended the Lithium Innovation Summit in Arkansas.

These were the learnings from that trip

- The Chinese have been using DLE at commercial scale for a decade - and Western DLE has been around longer than you think +10 years

- DLE could potentially be more environmentally friendly than evaporation ponds or hard rock mining

- The quality of brine is essential

- Analysts and financiers gravitate towards spodumene projects because it is easier to understand with its centralised production - one mine pit, one processing centre

- Modular approach most likely to work with clusters around wells

- DLE at commercial scale in the West will happen sooner than you think, 1-3 years

- Australian spodumene will always be bound for China

- DLE may lead to creation of a midstream product (more lucrative, better for DLE companies)

- Power is the biggest component of operating expenditure (OPEX), jurisdictions with cheap power will work better

For the full breakdown read this note: Arkansas Lithium Summit - lithium come back?

After the trip, we are positive on DLE and the US lithium brine space.

We are hoping that as the industry develops, MAN is able to progress its project to a point where it is domestically significant so that MAN can achieve our Big Bet, which is as follows:

Our MAN Big Bet

“MAN returns 1,000%+ by making a lithium discovery significant enough to move into development studies, or attract a takeover offer.”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved, and it will require a significant amount of luck. There is no guarantee that it will ever come true. Some of these risks we list in our MAN Investment Memo.

More on today’s announcement:

Our key takeaways from today’s news was as follows:

1. MAN’s exploration target ranges from 1.7 to 5.6 million tonnes of contained LCE (Lithium Carbonate Equivalent).

(Source)

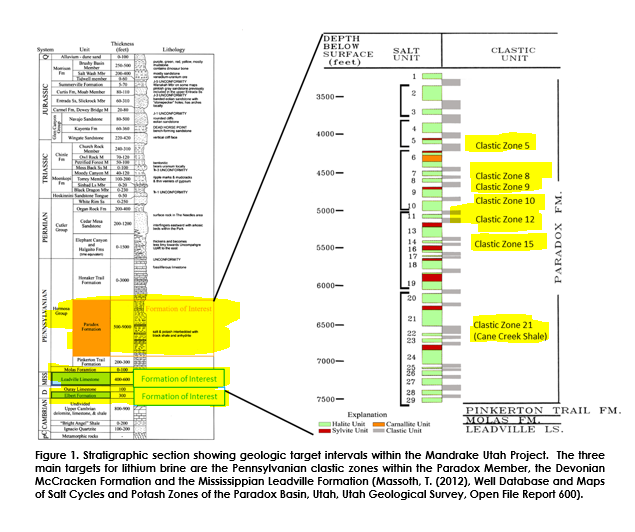

2. The exploration target was made across 9 different potential reservoirs (with potential to intercept more once MAN drills/re-enters existing wells).

(Source)

3. Porosities applied to the exploration target model range between ~4% and 9% - MAN did mention core data from north of its project that could indicate porosities are a lot higher (up to 21.3%). Porosity is important because it gives a good indication of how much brine MAN can flow up to surface in the future. The higher the porosity, the more brines are likely to flow to surface.

(Source)

How does MAN’s exploration target compare to its $141M neighbour Anson Resources?

MAN’s exploration target sits at 1.7mt to 5.6mt of LCE.

Anson’s project nearby has an existing JORC resource of ~1mt of LCE and an exploration target across two other projects in the region of a further ~3mt of LCE.

In total that would put the maximum case JORC resource scenario for Anson at ~4mt of LCE, which is lower than the maximum JORC resource case scenario for MAN.

Overall, we think MAN has put out a strong enough target that it could at the very least be bigger than Anson’s current resource and in the maximum scenario be a lot bigger...

(Source)

What are the risks?

The two key risks we see for MAN in the short term are “Exploration risk” and “Processing risk”.

Exploration risk is relevant because there is always a chance the company finds uneconomic quantities of lithium in the wells it re-enters.

Processing risk is also a factor because, even if MAN does find a decent amount of lithium, there is no guarantee that any of that lithium can be extracted and processed at rates that make MAN’s project commercially viable.

Technology risk is also now a factor - large scale DLE technology has yet to be proven commercially viable and there is a chance that MAN’s new technology partners are unable to make the process work with MAN’s brines.

To see all of the key risks to our MAN Investment Thesis, check out our MAN Investment Memo.

A longer term risk we see is:

Regional regulatory risk/jurisdictional risk - while Utah is a jurisdiction usually known for its friendly approach to extractive industries - we do note some recent mainstream media reports around Anson Resources and potential conflicts regarding Colorado river water rights. Even if these concerns are unfounded, it could still impact perceptions around DLE in Utah, and market sentiment. Whilst its early days for MAN in its exploration, this risk could increase as MAN develops the asset further.

Our MAN Investment Memo

In our MAN Investment Memo, you can find:

- MAN’’s macro thematic

- Why we Invested in MAN

- Our MAN “Big Bet” - what we think the upside Investment case for MAN is

- The key objectives we want to see MAN achieve

- The key risks to our Investment thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.