KAU - mining the Nova zone

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 4,665,000 KAU shares and the Company’s staff own 35,000 KAU shares at the time of publishing this article. The Company has been engaged by KAU to share our commentary on the progress of our Investment in KAU over time.

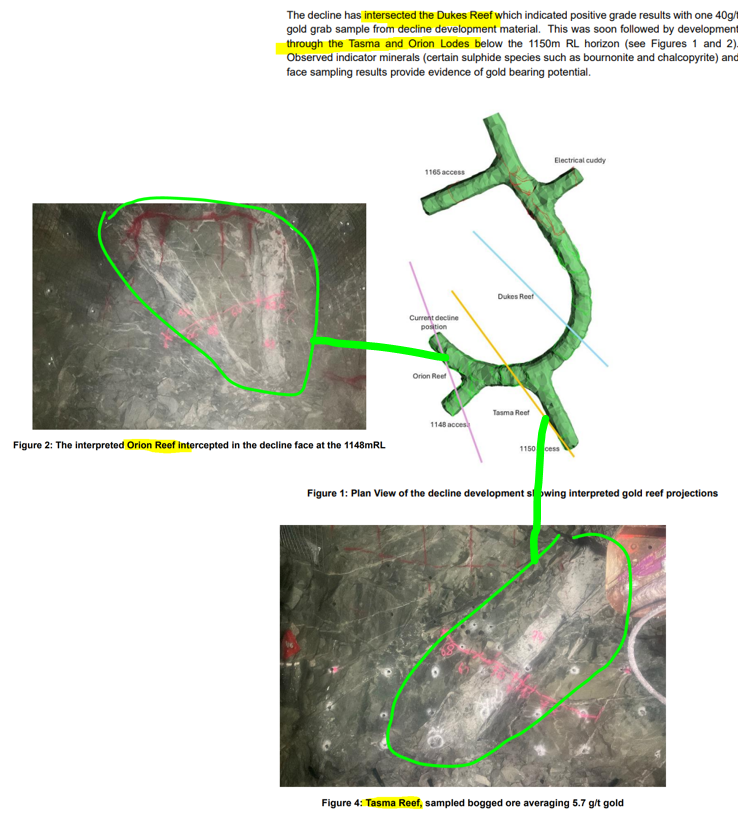

4,700g/t gold in a grab sample...

8.7g/t gold during stoping...

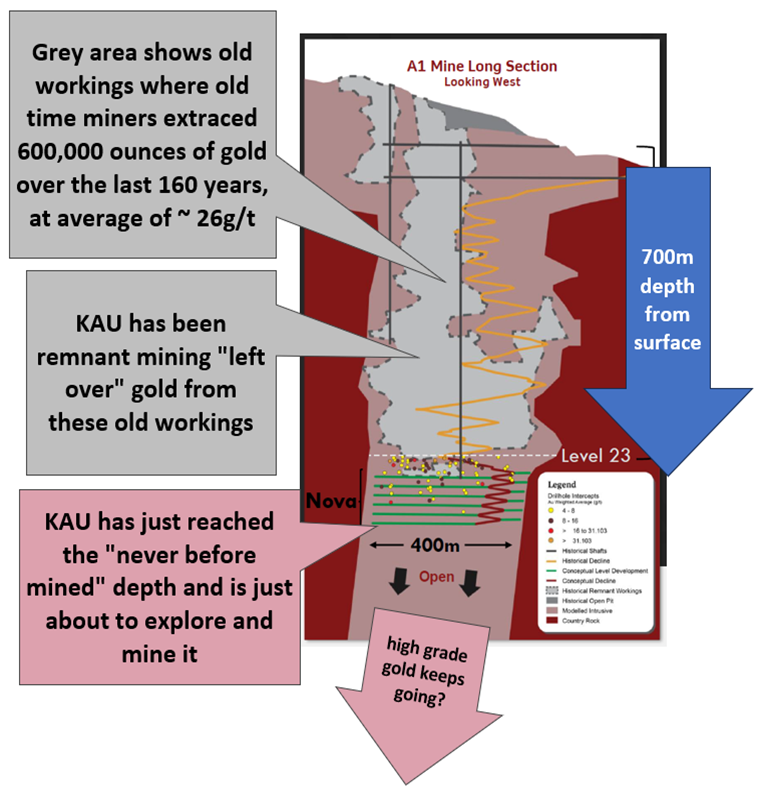

Our gold PRODUCING Investment Kaiser Reef (ASX:KAU) is now 20m into the never before mined, high grade parts of its A1 gold mine.

Basically, this means KAU have now dug a tunnel (big enough to drive a truck into AND haul gold ore out of) into never before mined depths of the historical high grade A1 gold mine.

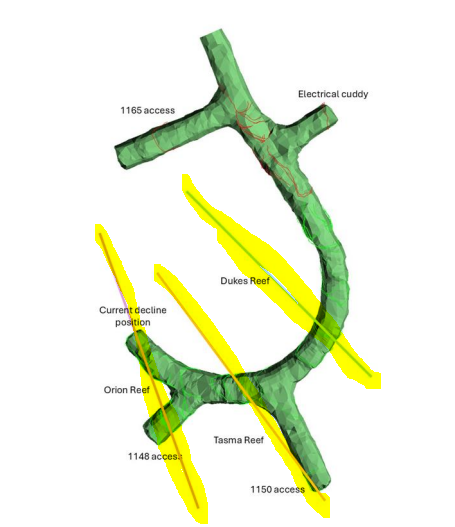

A full 20 vertical meters lower than ever mined before:

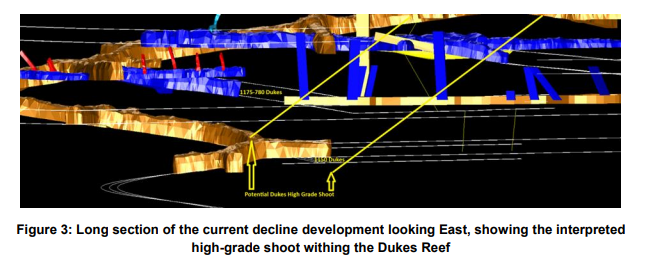

And this new tunnel extension (called a decline) has already intersected 3 potential high grade gold reefs for KAU to mine (plan view of the tunnel extension intersecting the gold reefs):

The A1 mine is where KAU has previously managed to produce and sell ~3,000 ounces of gold a quarter for a few quarters running.

(a 3,000 ounce quarter at today’s gold prices would be ~$13M revenue quarter for ~$40M market cap KAU)

Those past 3,000 ounce quarters were all from REMNANT ORE - parts of the mine where the high grade stuff had already been mined out.

(It's basically like getting your partners leftovers when out a restaurant, all the best stuff is already gone)

For decades different owners of the project mined and produced gold from remnant mining.

KAU is the first modern owner of the project to go mining in parts of the mine that have never been mined.

IMAGE UPDATE: KAU says it is now ramping up gold PRODUCTION from the never before mined levels.

KAU’s idea is that the high grade gold “reefs” continue at depth beyond where the old timers stopped mining.

Today, KAU officially announced that “ramping up of production” had started.

Up until now most of the work KAU was doing was building out infrastructure (ie digging a giant tunnel) to get to those never before mined areas of A1.

After today, it’s all about ramping up production to levels that at current gold prices turns KAU into a profitable producer .

And the blue sky upside for KAU is if they find one (or multiple) new high grade gold reefs that they can quickly mine, process and sell into record gold prices.

(KAU is already producing and selling gold at its 250ktpa gold processing plant)

The big bonus from today’s announcement was the mentions of grades while the development works were happening.

KAU said they had grab samples (rock chips) that returned gold grades of up to 4,700g/t AND the average grades when stoping was ~8.7g/t gold.

Stoping is when a company digs into parts of the project where they are looking to extract minerals from underground - so the 8g/t average grades are a really good sign.

(for context, KAU’s last quarter had average production grades of 4.7g/t - so doubling the grade & increasing production volumes would be huge for KAU).

It's hard to say for sure what sort of production rates to expect from KAU - but we do have some clues...

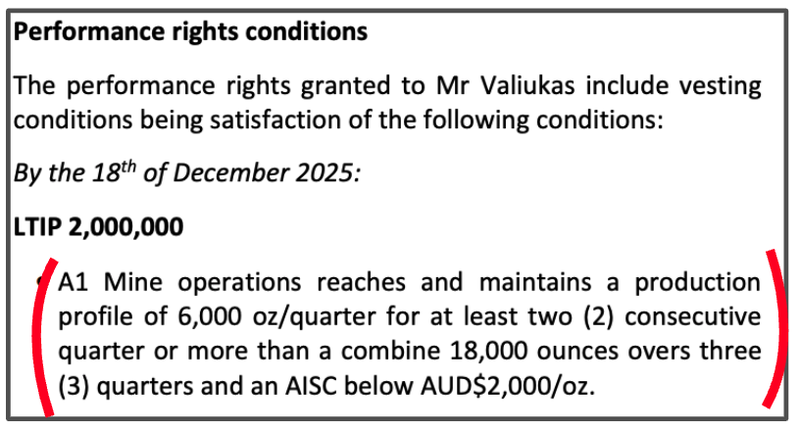

The director incentive rights are a good way of knowing what KAU is looking to target internally...

We did a quick look back at the last 18 months, peak production was ~3,372 ounces in one quarter - and remember this is just from the remnant ore.

(At current gold prices that would be a $15M revenue quarter...)

(That performance was from remnant ore, where the high grade ore had already been taken out)

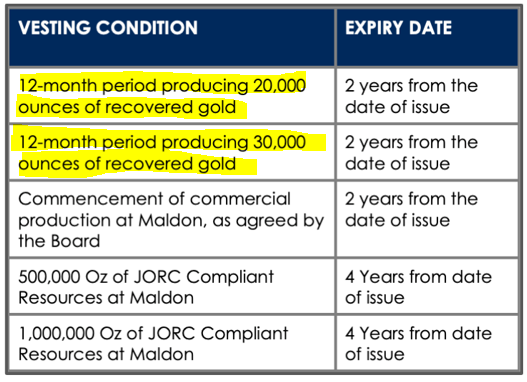

To get an idea of what success might look like for KAU we think the director incentive’s are a good indicator of what KAU is looking to achieve internally:

The first performance hurdle is two consecutive quarters of 6,000 ounces PER QUARTER by December 2025.

(if achieved that’s ~$53M revenue to KAU over 6 months at current gold price - KAU’s market cap is currently $40M)

(Source)

Another performance milestone is for KAU producing 20-30k ounces of gold over a 12 month period.

(if achieved that would be ~$84M to $126M in revenues at current gold prices - again, where KAU is capped at just $40M)

(Source)

Hopefully, today’s announcement about “production ramp-up” being underway is the precursor for KAU to set to deliver those milestones in 2025.

If we can get a strong few quarters while the gold price is at all time highs then we would expect the market to show a lot more interest in KAU.

What else did we pick up in today’s announcement?

A big part of today’s announcement that the market may have missed is an update on all the infrastructure upgrades KAU has completed over the past few months.

For us its a good sign KAU has done a lot of work in the background, setting up the company to make the most of the never before mined parts of its A1 mine.

Here were a few of our key takeaways:

1. Development of the decline is now 20m vertically into the high grade Nova Zone and KAU has hit three potentially high grade gold reefs that it can start producing out of

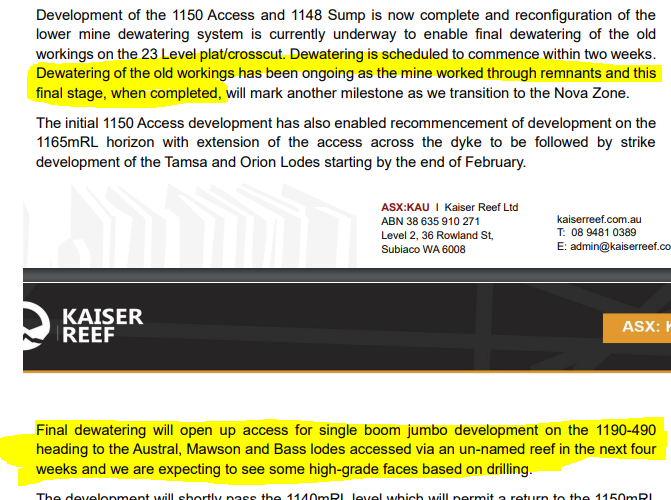

2. KAU close to accessing four new gold lodes in addition to the ones announced today - we noticed dewatering was in the “final stage” and KAU would be accessing these new structures within the next four weeks.

3. Ventilation upgrades being completed - this will mean KAU can move straight into mining once decline development is finished.

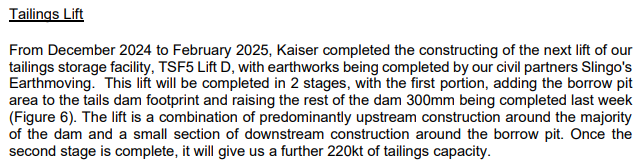

4. Tailings capacity increase being completed - this will mean more capacity to process material at the Maldon plant without needing further infrastructure upgrades.

5. Mill foundations strengthened - KAU upgraded the foundations for its plant, again a good sign that if processing ramps up the mill will be in good shape to handle the increased throughput.

Production is the main game but exploration is also a big part of the KAU story

In the short term it's all about getting KAU to squeeze out as much cash from the A1 mine as possible while reaching the fresh deeper high grade sections.

BUT we think exploration at another Victorian asset is also a big part of the KAU story.

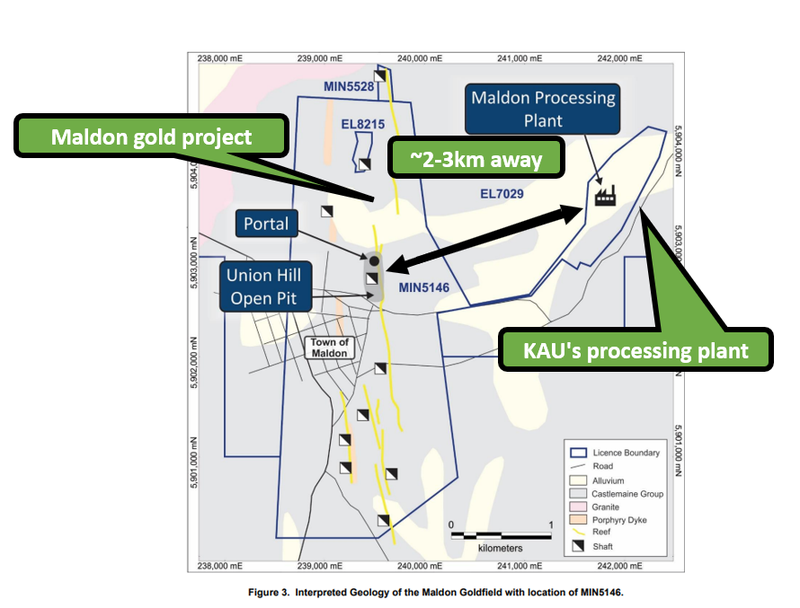

In addition to the A1 mine, KAU owns the Maldon project.

This project has historically produced 2.1Moz of gold since 1854 and has been placed on care and maintenance over the last 7 years.

If KAU is able to unlock the exploration potential and make a discovery at Maldon we think it would be transformational for the company, especially considering how close it is to the company’s processing plant.

Having a processing facility becomes far more important when it is combined with exploration success....

Just ask Spartan Resources investors...

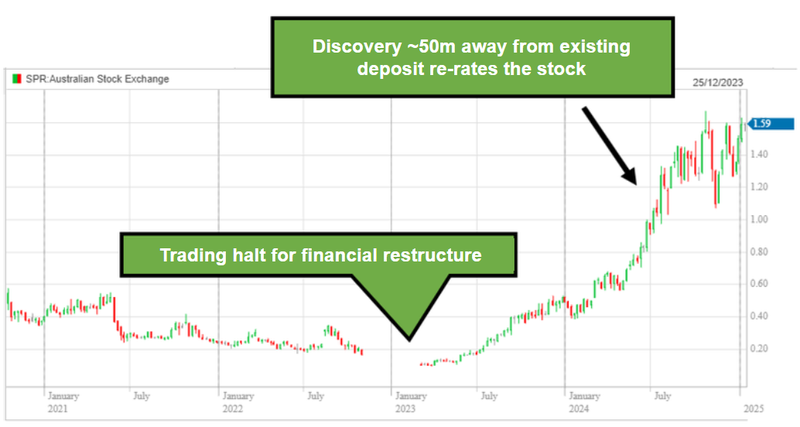

The perfect example of a company making a game changing discovery next door to its processing plant is ASX listed Spartan Resources (formerly Gascoyne Resources).

Spartan’s project in WA was also placed into care and maintenance (and even went into administration) - similar to KAU’s Maldon project...

In 2022 Spartan Resources drilled ~50m away from its existing JORC resource (which had been producing gold for years) and made a seriously high grade discovery...

That discovery took the Spartan share price from ~10c to $1.59 and a market cap over $1.7BN.

Past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Ordinarily a discovery like Spartan’s would be enough to re-rate a company’s valuation, but the reason why we think Spartan is trading at the valuations it is at today is because of the value of all the processing infrastructure that is already in place.

Spartan (with some minor tweaks) can optimise its plant to process the new discovery without having to foot a giant CAPEX bill to build a whole new plant.

We think that's part of the reason why $3BN Ramelius Resources has shown an interest in the company too. (Ramelius own 19.99% of Spartan...)

We think KAU (with a lot of exploration luck) has the potential to deliver something similar to this too...

KAU has a processing mill ready to go.

All it takes is one monster hit...

The ideal scenario will be KAU generating cash flow from its A1 mine to fund all of the exploration...

This is a big part of our KAU Big Bet which is as follows:

Our KAU Big Bet:

“KAU re-rates to a market cap greater than $300M by increasing gold production at its A1 Mine and/or making new discoveries at either of its two gold projects (A1 or Maldon)”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our KAU Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true

What’s next for KAU?

Over the next 6 months we are most interested in seeing KAU drill out and develop its A1 mine.

Here are the two objectives we will be tracking in the short term:

Exploration drilling at A1 Mine

We want to see KAU drill out the never tested sections of the A1 mine and make new high grade discoveries.

Milestones:

✅ Drilling commences

🔄 Drilling results

Increase production from the A1 Mine

We want to see KAU mine out the never before touched sections of the A1 gold mine.

Milestones:

🔄 Decline construction progress

🔄 Mining of virgin ground commence

🔲 Increased average gold grade processed

What are the risks in the short term?

The key risk for KAU in the short/medium term is “development/delay risk”.

KAU is constantly spending cash on operating its processing facility AND on declining development work.

IF decline development is delayed or takes a lot longer than expected it could mean KAU goes longer periods without production revenues.

We think the market could perceive this as a negative and start to price in future capital raises.

Development/delay risk

Should any or all of the above risks materialise, KAU could wind up stuck in “development purgatory” where newsflow dries up and the project remains stagnant for a prolonged period of time, hurting the share price. Additionally, if delays occur in terms of material newsflow, the market could turn on KAU.

Source: What could go wrong? - KAU Investment Memo 21 October 2024

We list more risks to our KAU Investment Thesis in our Investment Memo here.

Our KAU Investment Memo

You can read our KAU Investment Memo in the link below. We use this memo to track the progress of all our Investments over time.

Our KAU Investment Memo covers:

- What does KAU do?

- The macro theme for KAU

- Our KAU Big Bet

- What we want to see KAU achieve

- Why we are Invested in KAU

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.