KAU: Now comes the good part…

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 4,665,000 KAU shares and the Company’s staff own 35,000 KAU shares at the time of publishing this article. The Company has been engaged by KAU to share our commentary on the progress of our Investment in KAU over time.

We Invested in $43M capped Aussie gold producer Kaiser Reef (ASX:KAU) to see them mine and sell gold...

... from a new high grade gold zone that they discovered...

... in the never before mined depths of their historic A1 gold mine...

... that produced 600,000 ounces over its life.

KAU has previously managed to produce and sell ~3,000 ounces of gold in a quarter (a couple of times) in the last 2 years from its A1 mine in Victoria.

3,000 ounces in a quarter is around AUD ~$13M revenue at today's gold prices of AUD $4,425.

And this was just from gold ore LEFT OVER by the old time miners in the A1 mine, after they mined and sold the highest grade ore they could get their hands on.

The theory is that this high grade gold extends further down - and KAU has done deeper exploratory drilling and made gold discoveries that confirms this theory - that’s why it's committed to investing in going deeper.

The tens of millions of dollars KAU sold the “left over” gold for over the last few years has been re-invested to reach new depths of the historic A1 mine that old timers just couldn’t reach with technology of the time.

This is where we want to see KAU find, mine and sell more ultra high grade gold.

(We Invested in KAU at 15c back in October 2024 - AFTER the majority of this investment had been made - thanks to those that came before us)

KAU just released a quarterly report which shows they should soon start mining these never before mined depths - where more high grade gold has been discovered with KAU’s recent exploration drilling.

Mining of remnant ore has been slowed down in favour of making the final push to mine new ultra high grade gold.

As a result, KAU is now “15m BELOW historic workings” - the company is in and amongst the fresh, never before mined, part of the A1 mine.

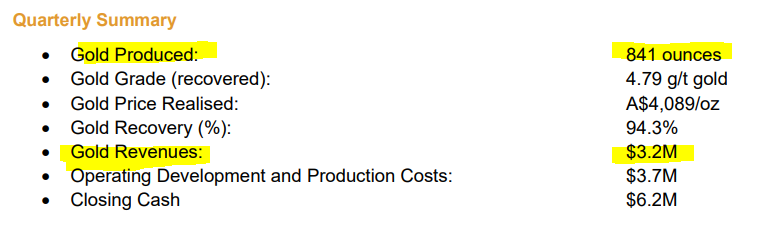

But even while it ‘slowed down’ processing of remnant ore to prioritise getting to the unmined levels, KAU still managed to produce and sell 841 ounces at an average price of $4,089/oz for $3.2M in revenue.

(Source)

And they have about $0.5M in unsold bullion sitting with them, as well as $6.2M cash at the quarter’s end.

While gold is at record high prices, and rising.

So over the coming months we want to see:

- More high grade drill results from the never before mined depths

- Complete the development work to increase production on new high grade reefs

- Increase production by mining new high grade reefs.

- Official discovery of a new high grade gold reef

- Gold price keeps rising or stays at current levels

If KAU can deliver just TWO consecutive 3,000 oz quarters and the gold price stays at current levels, that's ~$26M revenue to $43M capped KAU.

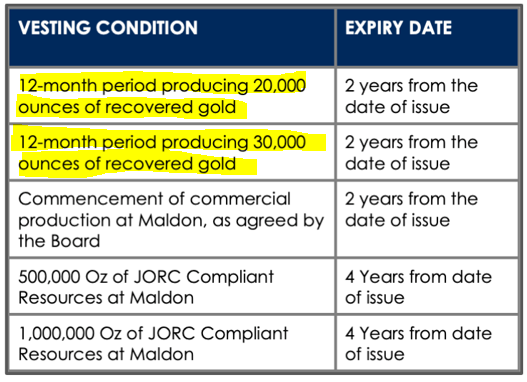

We also note a couple of interesting KAU director incentives:

The first is two consecutive quarters of 6,000 ounces by December 2025.

(if achieved that’s ~$53M revenue to KAU over 6 months at current gold price)

Another performance milestone is for KAU producing 20-30k ounces of gold over a 12 month period.

(if achieved that would be ~$84M to $126M in revenues at today's gold price...)

...more on these performance milestones later.

Obviously with higher production and materially increased revenue, there should come a higher KAU share price.

KAU is currently capped at $43M and now on the cusp of mining the never before mined depths at A1, giving the board and management a chance to deliver these production numbers to hit their performance incentives in the coming quarters...

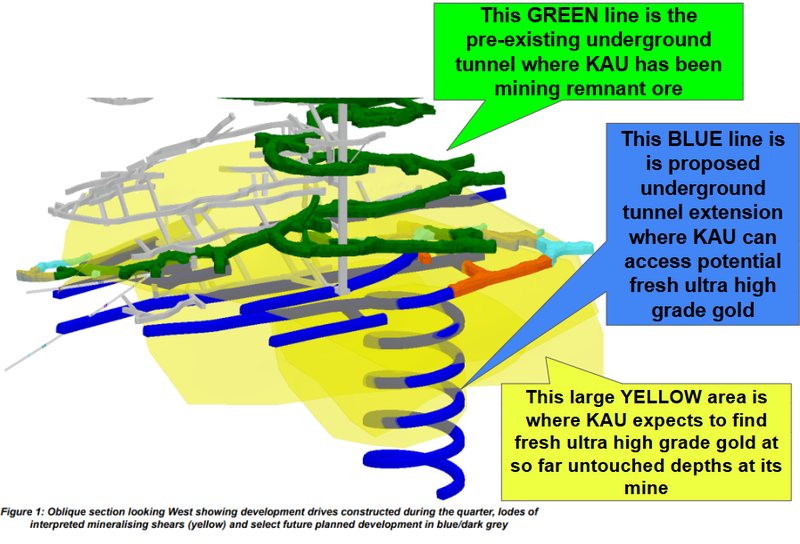

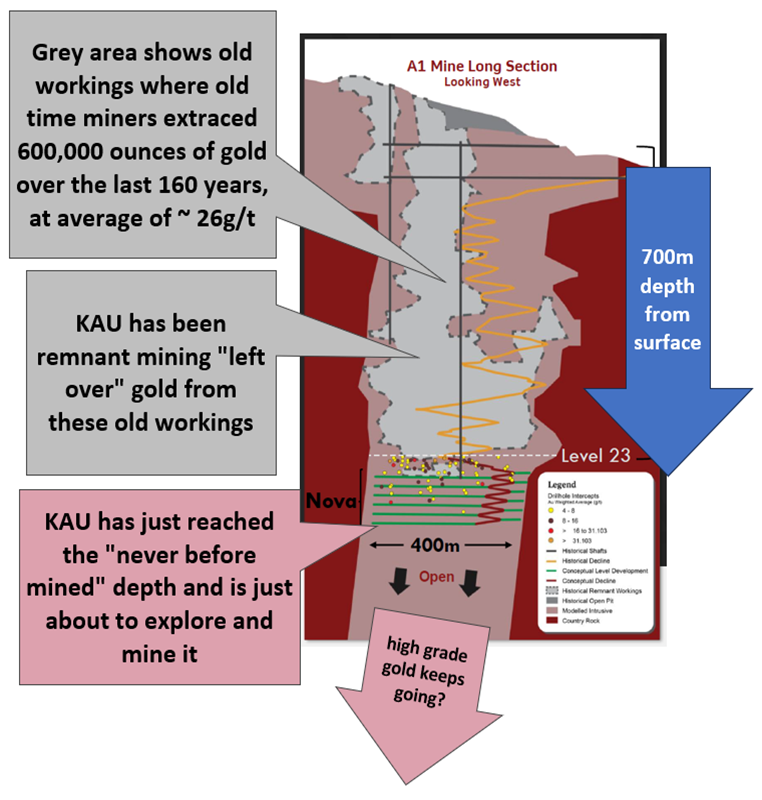

This image from the just released quarterly shows just how close KAU are mining potentially ultra high grade, never before mined depths at A1:

And we simply DO NOT know what KAU might find in the deeper part of a mine that historically produced 600,000 ounces of gold.

This is where the blue sky upside is for KAU - if they find more and more ultra high grade reefs like the ones historically mined above...

... the company’s share price could materially re-rate from its current level.

We will find out over the coming months.

Discovered in 1861, KAU’s A1 gold mine has produced over 600,000 ounces of gold.

The average historical grade out of the A1 mine was 25g/t gold.

This is an extremely high grade.

But the old-time miners couldn’t reach the deepest levels with the mining technology of the time...

(Photography technology has also come a long way since then too...)

KAU has put in years of work and spent tens of millions of dollars to reach the deepest and never before mined levels of the A1 mine.

Where fresh, never before high grade gold should be waiting for them.

Two weeks ago KAU announced drill hits of .20m at 65.1g/t gold and .80m at 32.7g/t gold from the never before mined depths.

Further exploration drilling is ongoing and we eagerly wait for more results.

KAU latest quarterly says they are now “developing into” the never before mined part of the A1 mine, that the old time miners couldn’t reach:

(Source)

‘Developing into’ essentially means getting all the infrastructure sorted to start mining - digging mining access for trucks, miners and other equipment, sorting out ventilation underground - in order to extract the gold from never before mined depths.

The assumption is that if there was an average gold grade of 25g/t pulled out from the 700m above, that there should be more high grades in the depths that the old time miners could not reach.

We actually drove down to the deepest part of the existing underground tunnel when we visited the A1 mine back in October last year, to see it with our own eyes:

After a dark, bumpy, ride, once at the bottom:

For now, KAU makes millions of dollars per quarter processing and selling gold from remnant ore - left over by the old time miners who just took the highest grade, easy to reach ore.

(KAU own 100% of a 250,000 tonne per annum gold processing plant)

The newly mined gold ore then gets trucked to KAU’s 100% owned gold processing plant, the gold is extracted and sold (at record high gold prices):

So over the coming months, KAU could start mining a new ultra high grade gold reef in never before mined depths of a mine that historically produced over 600,000 ounces of gold.

We are also watching for more high grade gold hits as KAU continues exploratory drilling into the never before mined depths.

While KAU has invested in the millions to reach these new depths, they still make millions per quarter by processing and selling remnant ore left by the old time miners.

What would success look like for KAU?

It isn't easy to predict what a good few quarters or year looks like for KAU - but we have some clues.

KAU has been producing from remnant ore (parts of the mine where the good stuff had already been mined) and was still managing to produce ~3,000 ounces in some quarters.

We did a quick look back at the last 18 months, peak production was ~3,372 ounces in one quarter.

(again... that was just from remnant ore, where the high grade ore was previously mined out)

You can see the gold price KAU is selling for is gradually increasing, however KAU’s production is also slowing - as it focuses on development of the mine to access the higher grade sections.

(the tunnel to get to the lower levels is only a certain size for trucks and equipment to come in and out safely, so you can’t mine remnant ore AND go full pace at deepening the tunnel at the same time, there is a trade off)

KAU is aiming to shortly start to increase its production numbers over future quarters - and be able to sell this increased gold production for that higher gold price.

Now with KAU “15m below historic workings” the company is almost near the fresh, never before mined, part of the A1 mine.

(Source)

We also noticed the commentary in yesterday’s quarterly where management are saying KAU are “ahead of production areas”, meaning we shouldn't be too far away from seeing production rates pick up.

(Source)

(and hopefully gold grades improve by a lot...)

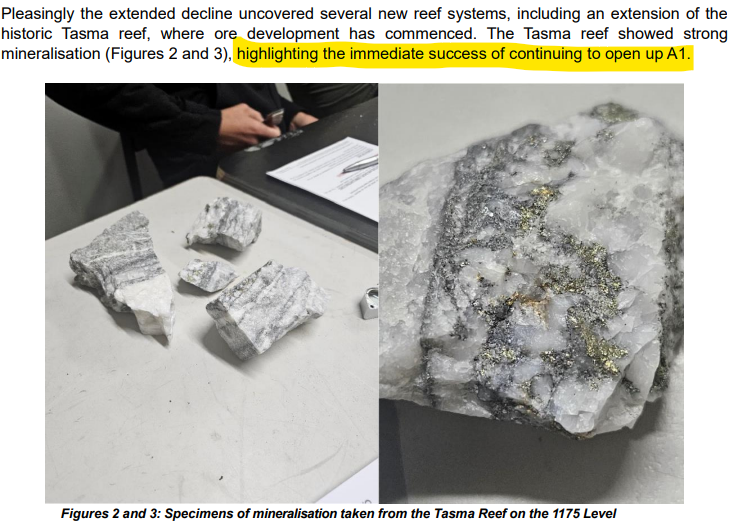

In yesterday’s KAU quarterly we also got a look at some samples of quartz veins that have visible gold in them from a gold reef at depth:

(Source)

This gives us a taste of what could be further down as KAU transitions from remnant ore to fresh rock like above at depth.

We should soon start seeing some more drill results from A1’s deepest levels.

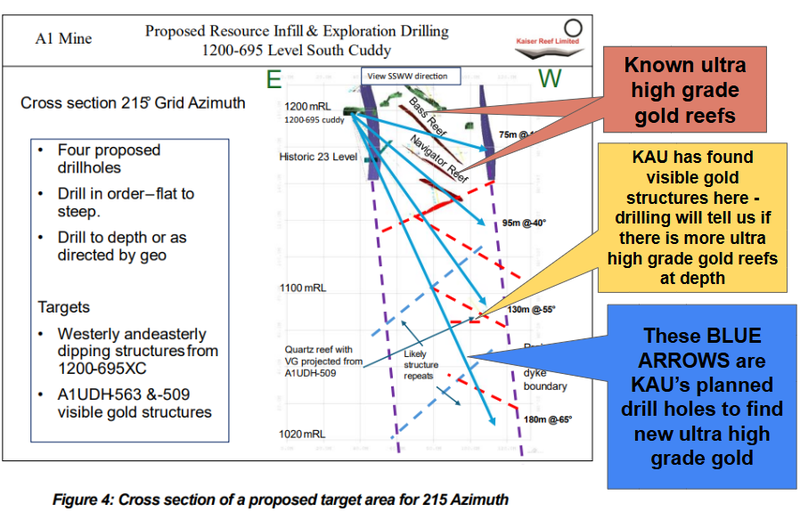

As KAU goes deeper into the fresh depths, KAU is now planning further drilling at these deeper levels - to build on the theory that there are a series of repeating reef structures further down:

Drilling success here would help KAU build confidence that it can significantly increase production - and KAU director performance rights are based on a big increase in production to come.

Here’s more on that.

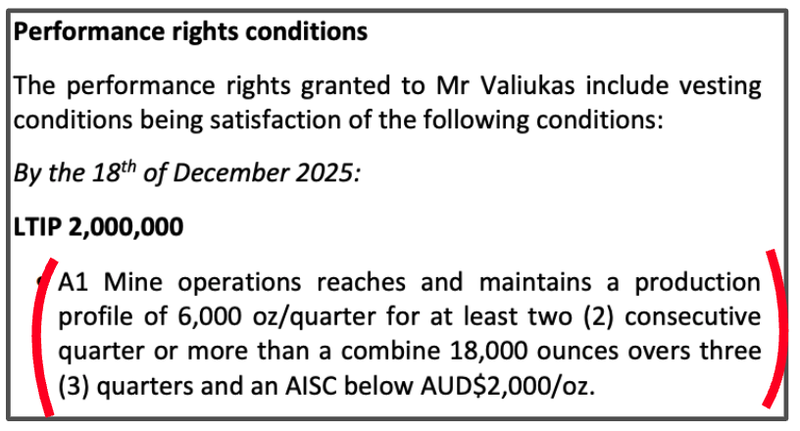

KAU performance rights for board and management provide some clues to future production goals

If the performance rights for the directors are anything to go by then a good 6 months could look like - 18k ounces at a cost of below $2,000 per ounce:

(Source)

At today’s gold prices 6 months with those production numbers would be ~$75M in revenues with costs of ~$36M.

We think that would be transformational for KAU.

Of course, there is no guarantee that KAU will hit those numbers, the above calcs are just to illustrate a potential upside scenario, and run the maths on the incentives driving KAU’s management.

If the company is to hit the performance targets set more recently: 20-30k ounces of gold over a 12 month period then that would be ~$84M to $126M in revenues...

(Source)

Again these revenues are no guarantee to eventuate, this is high risk gold development and anything can happen.

Based on the image in yesterday’s quarterly, KAU looks like it has made it to those new parts of the mine, so hopefully production rates start increasing soon.

Exploration a big part of the KAU story

In the short term it's all about getting KAU to eke out as much cash from the A1 mine as possible while reaching the fresh deeper high grade sections.

BUT we think exploration at another Victorian asset is also a big part of the KAU story.

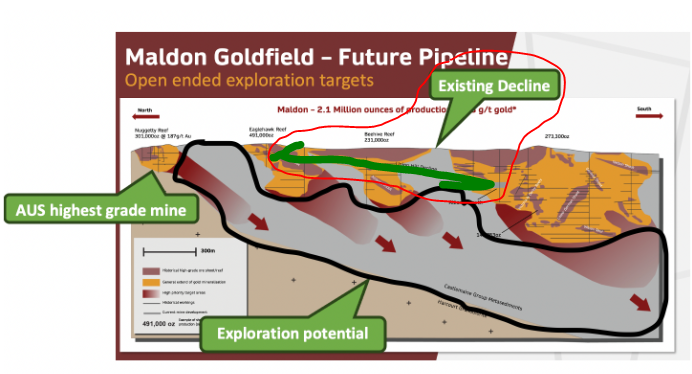

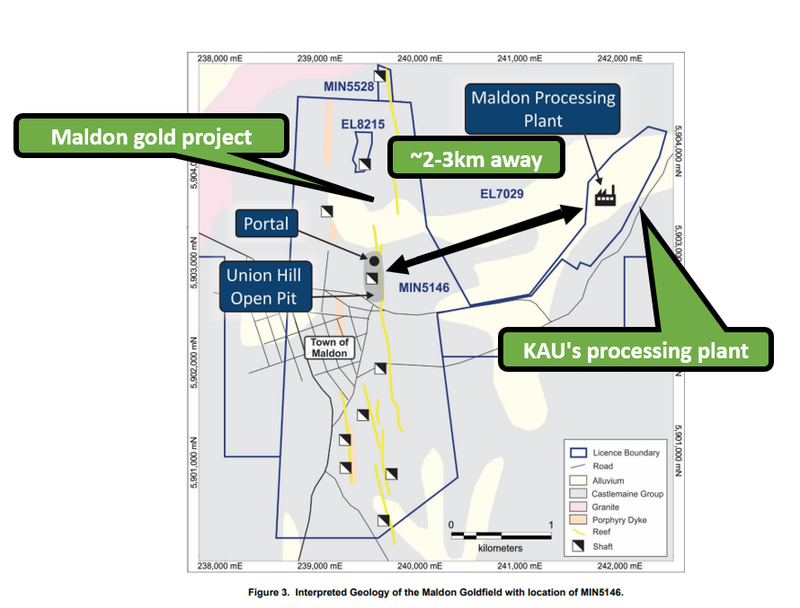

In addition to the A1 mine, KAU owns the Maldon project.

This project has historically produced 2.1Moz of gold since 1854 and has been placed on care and maintenance over the last 7 years.

If KAU is able to unlock the exploration potential and make a discovery at Maldon we think it would be transformational for the company, especially considering how close it is to the company’s processing plant.

Having a processing facility becomes far more important when it is combined with exploration success....

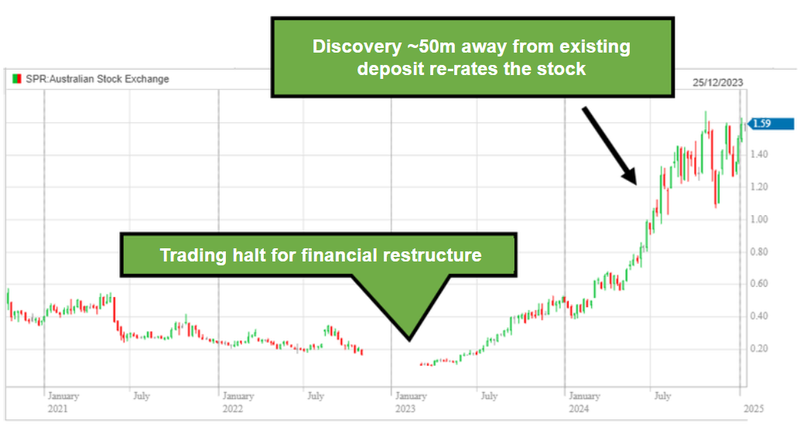

Just ask Spartan Resources investors...

A good example of exploration success being a game changer for a gold company with a processing plant is ASX listed Spartan Resources (formerly Gascoyne Resources).

Spartan went from 10c to $1.59 and is now capped at ~$1.7BN - here’s how:

The company owned the Dalgaranga project which was a relatively low grade operation, producing gold for years in an old gold mill in WA.

After multiple false starts, and attempted restructures, the project was most recently recapitalised in 2022.

After a ‘hail mary’ exploration drill program outside of the existing resource (and existing mine), a huge gold discovery was made.

The kind of gold discovery that most small caps dream of.

In 2022 Spartan Resources drilled ~50m away from its existing JORC resource (which had been producing gold for years) and found high-grade gold intercepts extending the area of mineralisation.

Previous drilling had missed a giant discovery, literally a stone's throw away from its old open pit...

Spartan made a new high grade discovery and the company’s share price went from 10c to $1.59 and is now capped at ~$1.7BN.

Past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

The big upside for Spartan Resources is that all of the existing processing facilities are in place, so any value from a gold discovery could be immediately realised.

We think KAU (with some exploration luck) has the potential to deliver something similar to this too...

KAU has a processing mill ready to go.

If it can make a further gold discovery it can follow a similar success pathway as Spartan Resources...

All it takes is one monster hit...

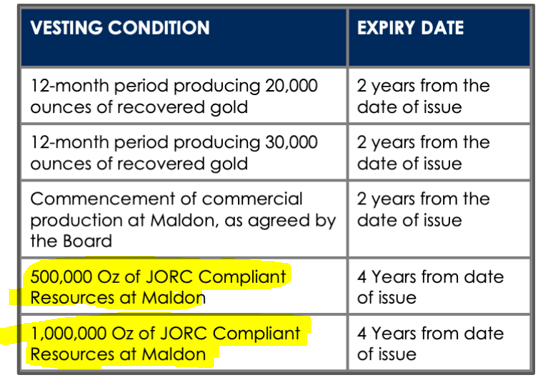

We noticed the performance milestones set recently also included resource definition targets at Maldon, which tells us KAU will soon start putting cash into some exploration here.

If they can make a discovery anywhere near those performance targets then we expect it would have a strong positive impact on KAU's valuation given its processing capacity is only at 20%...

The ideal scenario will be KAU generating cash flow from its A1 mine to fund all of the exploration...

This is a big part of our KAU Big Bet which is as follows:

Our KAU Big Bet:

“KAU re-rates to a market cap greater than $300M by increasing gold production at its A1 Mine and/or making new discoveries at either of its two gold projects (A1 or Maldon)”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our KAU Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true

We have visited KAU’s mine, here is our take...

We have been to all three of KAU’s projects during our due diligence process on the company.

We saw both the A1 gold mine and the processing plant when we visited the site back in March and again in October last year.

Here are a few pictures from the A1 gold mine:

Here are some from the gold processing plant in Maldon:

And here are some pictures from the company’s Maldon Gold project:

You can read all of our notes from our site visits here: Our New Investment is Kaiser Reef (ASX: KAU).

What’s next for KAU?

Over the next 6 months we are most interested in seeing KAU drill out and develop its A1 mine.

Here are the two objectives we will be tracking in the short term:

Exploration drilling at A1 Mine

We want to see KAU drill out the never tested sections of the A1 mine and make new high grade discoveries.

Milestones:

✅ Drilling commences

🔄 Drilling results

Increase production from the A1 Mine

We want to see KAU mine out the never before touched sections of the A1 gold mine.

Milestones:

🔄 Decline construction progress

🔲 Mining of virgin ground commence

🔲 Increased average gold grade processed

What are the risks in the short term?

The two key risks for KAU in the short/medium term are “exploration risk” and “development/delay risk”.

Exploration risk because the company is now drilling at its A1 mine.

If the drilling fails to deliver high grade gold hits then it could impact KAU’s development strategy.

The market may also start to discount the potential of the development strategy which we think could impact the share price in the short term.

Exploration risk

There is no guarantee that KAU’s upcoming drill programs are successful and KAU may fail to find economic silver-gold deposits.

Source: What could go wrong? - KAU Investment Memo 21 October 2024

Development delays are also a risk for KAU.

KAU is constantly spending cash on operating its processing facility AND on declining development work.

IF decline development is delayed or takes a lot longer than expected it could mean KAU goes longer periods without production revenues.

We think the market could perceive this as a negative and start to price in future capital raises.

Development/delay risk

Should any or all of the above risks materialise, KAU could wind up stuck in “development purgatory” where newsflow dries up and the project remains stagnant for a prolonged period of time, hurting the share price. Additionally, if delays occur in terms of material newsflow, the market could turn on KAU.

Source: What could go wrong? - KAU Investment Memo 21 October 2024

We list more risks to our KAU Investment Thesis in our Investment Memo here.

Our KAU Investment Memo

You can read our KAU Investment Memo in the link below. We use this memo to track the progress of all our Investments over time.

Our KAU Investment Memo covers:

- What does KAU do?

- The macro theme for KAU

- Our KAU Big Bet

- What we want to see KAU achieve

- Why we are Invested in KAU

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.