Immediate Upside? WHK Reveals Future Revenue Growth

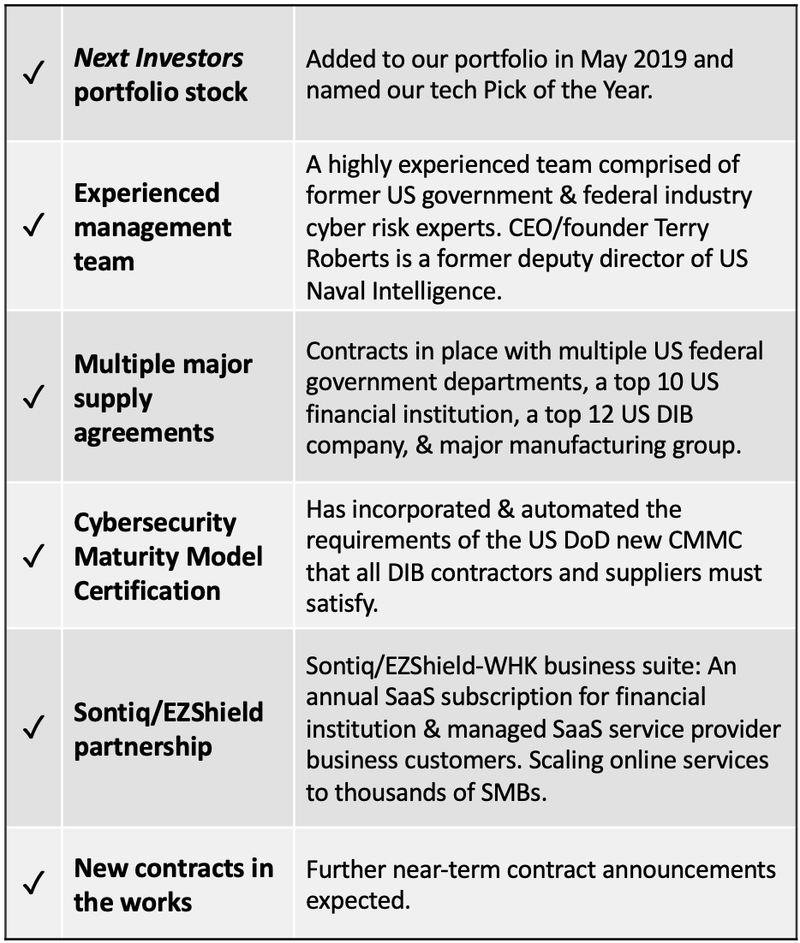

One of our favourite long-term portfolio stocks, WhiteHawk Ltd (ASX:WHK) has just delivered its quarterly report to the market, and the results show WHK is on the right path to sustained growth.

WHK is based in the US, and offers cybersecurity technology to US Federal Government agencies, large corporations, right through to small businesses.

The US Government is set to spend over $18BN on cybersecurity in 2021. It’s incredibly hard to qualify as a contractor or sub-contractor to US Federal Government agencies, especially in the cybersecurity sector, but that is exactly what WHK has achieved over recent months.

This is a testament to its highly experienced management team, led by Ms Terry Roberts, a former Deputy Director of US Naval Intelligence.

On the back of these important contract wins (including the recent US$1.5M contract extension), the coming quarters will see WHK’s financial performance continue to improve – and therein lies the upside in WHK for new investors.

We added WHK to our portfolio in May 2019. We invested at 6.4 cents and increased our position at 11.3 cents and then again at 13.3 cents. We are high conviction, long-term holders of WHK, and are looking for continued, sustained growth in company value over the coming months.

Our other portfolio stocks include MyFiziq (ASX: MYQ), which has risen from 11.5 cents when we first invested in it and brought it to readers’ attention in April 2020 to $1.03 today, having been as high 1,200%; and Vulcan Energy (ASX: VUL), which we first brought to readers’ attention in February this year when it was 18 cents. It is now trading at $1.27, up over 600%.

We continue to hold large positions in both of those companies.

While those stocks have had large share price runs over recent months, WHK hasn’t yet – and we think it could be one of the most undervalued in our portfolio right now.

Here are our key takeaways of WHK’s Quarterly:

The company recorded US$320k revenue in the quarter – but that’s not the whole story and doesn’t quite do the performance in the quarter justice.

It is important here to dig a bit deeper and read between the lines, to understand just how well WHK is doing and how important its contracts are to its future growth.

The number we are really looking at is the invoicing amount – which in Q3 was US$948k – almost double Q2 invoicing that was US$502k.

We also know is that in the month of October alone, US$861k in receivables will be collected by the company.

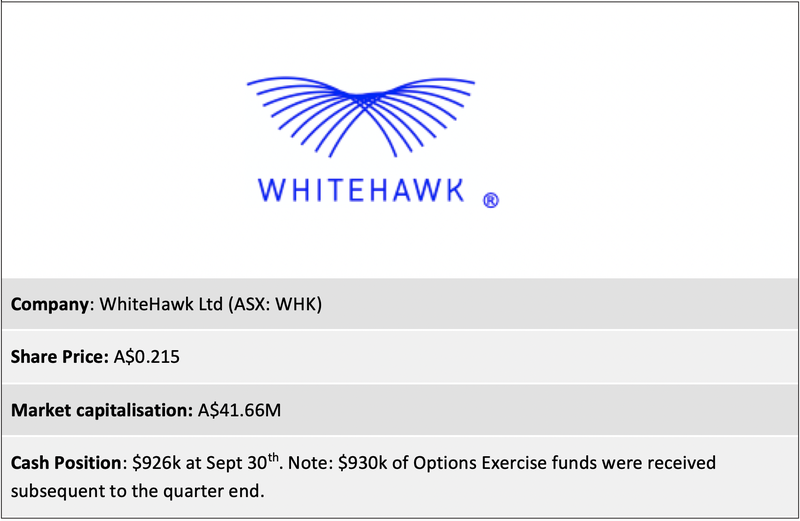

The cash on hand at 30 September 30 was US$926k (A$1.3M), and that doesn’t count the A$930,931 in option exercise funds that were received after Sept 30th.

Cash burn remains low at US$185k per month even as they deliver to their contracts.

So all in all, it’s been a very positive quarter for WHK, and the company’s balance sheet looks in good shape.

Major Contract Wins

WHK has accumulated several large cybersecurity contracts with multiple US federal government departments and has major ties to US corporations and SMEs.

The company’s recent US$1.5 million (A$2.1M) contract extension with a US federal government department, had a dollar value alone more than WHK’s entire 2019 revenue.

The contract is Phase 2 of WHK’s current contract with the US Department of Homeland Security (DHS) CISA, as sub-contractor to Guidehouse (formerly PWC Federal).

This contract, which kicked off this month, is to develop, test and refine the QSMO (Quality Serviced Management Offices) Cybersecurity Marketplace.

The contract extension, under an existing seven-year cybersecurity contract, represents a 375% increase on the US$400K awarded to WHK under the contract in 2020.

The focus of this contract has evolved from cyber risk technical and management services, to now lead developer of a comprehensive online Cyber Security Marketplace, with an automated cyber risk review and solution option mapping, for a breadth of US Federal Government entities.

This is an important development for WhiteHawk as revenues across the group are rapidly ramping up, having more than doubled to approximately US$585,000 in the first half of 2020.

In August, WHK was also awarded the first sole source US Federal Government CISO Cyber Risk Radar contract.

The contract spans 150 suppliers, with options for an additional 150 suppliers a year for a base year. Four option years are also included for a base price of $580,000 with an option of up to an additional $600,000.

With contracts in place and revenues coming in, we are confident that WHK will continue to sign agreements that add to its bottom line and keep shareholders engaged.

As we alluded to above, we are holding this stock for the long-term as we see enormous upside, especially as cybersecurity becomes more and more important in a world where cyberattacks are on the increase and seemingly part of everyday life.

And more ... It’s been a big quarter for WHK

Just two weeks ago, WHK kicked off five new cybersecurity proof of value (POV) engagements and contracts.

The POVs are for a total of up to 100 vendors across three key sectors — the US government sector (a US agency and a department), the manufacturing sector, and two with the Defence Industrial Base (DIB).

WhiteHawk will provide continuous cyber risk monitoring and prioritisation for the remainder of 2020, plus two Cyber Risk Scorecards (one immediately and one at the end of the POV) for each vendor/supplier.

WhiteHawk’s previous US Government Cyber Risk Radar POV, implemented early in 2019, resulted in a five year Software as a Service (SaaS) contract, as announced in July 2020.

That contract is worth up to US$5.9 million (A$8.2M), or US$1.18 million (A$1.64M) per year over the five-year term.

Of further note, is WHK’s incorporation and automation of the new US Department of Defense (DoD) Cybersecurity Maturity Model Certification (CMMC) mapping into its online client services and Cyber Risk Scorecard.

WHK is automating and scaling two key product lines. Its Cyber Risk Scorecard product line, which is now 100% automated, and its platform services and scorecard.

This now includes a new cyber security model — CMMC, enabling scalability across thousands of companies.

The DoD established CMMC as the cyber resilience benchmark for all Defense Industrial Base (DIB) contractors and suppliers. It is a critical element of the DoD’s overall strategy, designed to improve information protection and cybersecurity.

There are roughly 330,000 subcontractors of the DoD industrial complex for which CMMC will apply to varying degrees.

Other highlights of the quarter include:

- Signed partnership agreement with Global Insurance Group to explore WhiteHawk online platform and virtual Cyber Risk Service options;

- With current DIB Client, kicked off a Path to CMMC engagement Program across 600+ suppliers and vendors, to provide virtual CMMC baseline consults, establish online accounts and maturity models and review their Cyber Risk Scorecard findings and risk mitigation options;

- Completed Phase 2 of Cyber Risk Program via a Global Consulting Firm in direct support of a Global Manufacturer, including: risk validation by Red-Team, a comprehensive risk prioritization and mapping to risk mitigation best practices and solution options;

- Sontiq/WhiteHawk Small Business Suite offerings via Managed Service Provider and Financial Institution to 5,000 to 140,000 SME current customers, as an annual SaaS contract have been delayed (not canceled), one due to COVID business impacts and the other due to changes in company leadership.

All roads lead to revenue growth

All of these deals has led WHK to record consistent revenue in each of the last 9 months.

However Q3 has been notable in that invoicing of US$948,000 is nearly double the US$502,000 in the second quarter of 2020 – suggesting next quarter’s revenue number will be much higher.

WHK has invoiced US$2M in the first three quarters of this year, up from US$600,000 compared with the first three quarters of 2019.

Further to this, WHK will collect $861,000 in receivables in October.

Investors will be pleased that WHK’s lean approach to business saw it maintain cash burn in the third quarter of a monthly average of US$185,000 and repay a $289,000 loan from RiverFort in cash.

WHK also finalised issuance of 13m shares, following a US$686,000 capital raise with Riverfort Global Capital.

To-date WhiteHawk has benefited from premium on sale of shares: this is US$36,000 above the anticipated US$178,000.

The money is to be put towards future growth.

Growing need for cybersecurity

The need for cybersecurity is growing exponentially - Data from the Australian Cyber Security Centre (ACSC) found cyberattacks on Australian businesses are costing the economy $29 billion a year.

Last financial year, an average of 164 cybercrimes were reported to the ACSC on a daily basis. Further, 62% of small businesses admitted to being affected by a cyber security incident.

That is just in Australia – a tiny market compared to the US.

A report released by the White House Council of Economic Advisors estimated that malicious cyber activity cost the US economy between $57 billion and $109 billion in 2016.

The same Council estimated that cybercrimes cost the global economy $3 trillion dollars in 2015 alone, with projected costs increasing with each passing year.

Cybersecurity Ventures estimates the cost will be $6 trillion by 2021.

Cybersecurity is a global problem, and the requirement for workable solutions is growing exponentially.

Everyone from the smallest of SMEs to the US government is currently at risk.

There are many types of threats and all have consequences:

It is these types of threats, that has led the US government to up its cybersecurity game.

Part of its strategy has been to engage companies such as WHK to deliver cybersecurity services.

Looking forward

On top of new contracts and agreements, WHK isn’t one to sit idle with product development. It continues to develop and demonstrate the effectiveness of its Cyber Risk Product Lines including virtual implementation, the timeliness and scalability of the offerings; the effectiveness of the risk identification and mitigation results.

The company is demonstrating its product lines to the majority of its client pipeline across Federal Government, Defense Industrial Base, Financial and Manufacturing Sectors. It has also renewed cyber risk solution conversations with its three public and two private sector channels, effectively updating their understanding and expectations of WHK’s Product Lines, the Digital Age risk problems they address and their scalability and affordability.

Expansion of its ISP And MSP client pipeline is also being undertaken.

WHK has instigated market research conversations with three major ISPs and two major MSPs, with the goal to demonstrate a standard portfolio of cybersecurity solutions.

WhiteHawk’s reputation continues to grow as it delivers cybersecurity solutions to some of the world’s biggest entities, including large US government departments.

We took a major investment in WHK because we believe that this company has some of the best fundamentals going around for a junior cybersecurity company.

Notably, it is backed by a strong team that understands its market.

The recent quarterly demonstrates the company is heading in the right direction financially and with that in mind, investors may soon come to realise just how undervalued this stock may be.

The WHK investment case:

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.