New investor interest in WHK’s Artificial Intelligence for Cyber Security Tech

Disclosure: S3 Consortium Pty Ltd (The Company) and Associated Entities own 14,706,087 WHK shares and 5,200,000 options at the time of publishing this article. The Company has been engaged by WHK to share our commentary on the progress of our Investment in WHK over time.

The Artificial Intelligence (AI) boom is all over the news.

The AI investment rush appears to be on...

Nvidia (that sells microchips for AI) is up 400% in the last 12 months and is now valued at almost $2 trillion dollars - its the world's 4th most valuable publicly listed company.

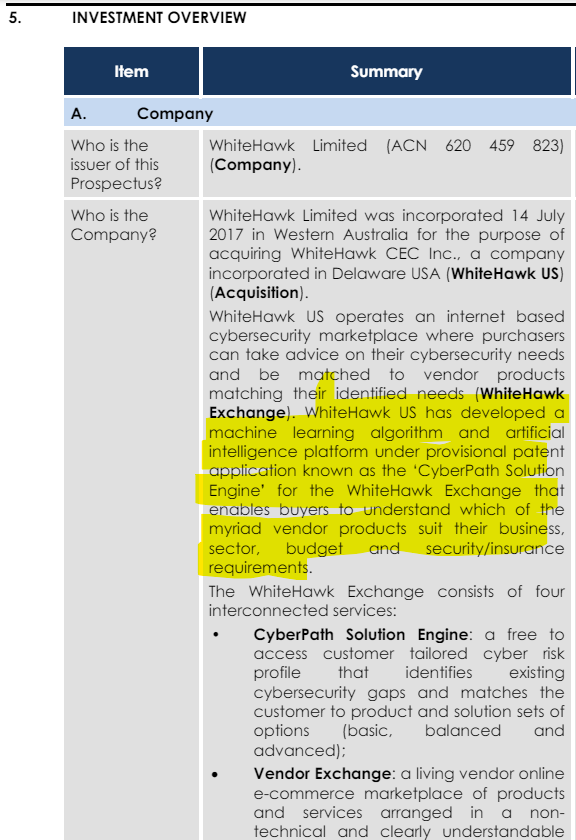

Our long term micro cap Investment WhiteHawk (ASX:WHK) has been developing and selling AI and machine learning products for cyber security since before its IPO in 2017.

Way before AI became the world’s most popular investment thematic.

There are few true AI plays on the ASX.

WHK is leveraged to the AI investment thematic, which might explain the rapid surge in interest in the stock over recent days.

Most companies are now trying to figure out how to sprinkle AI into their products and investor presentations...

Meanwhile, WHK has been working on AI since 2017 under CEO and Founder Terry Roberts’ leadership.

Roberts has a long history with AI dating back to at least 2009, when she was executive director of Carnegie Mellon University’s Software Engineering Institute (Source) which we believe was recently renamed to the SEI Artificial Intelligence Division.

Carnegie Mellon was the university that developed the first AI computer program in 1956. (Source)

WHK’s AI based cyber security tech has been quietly developed over the last 6 years AND is already in use by US federal government departments, US defence contractors, Fortune 500 companies...

On annual recurring revenue contracts.

And two months ago, WHK announced an “AI based cyber risk contract extension with a top 5 global social media company” worth US$1.2M annually.

At the start of last week WHK was capped at just ~$5M (we’ll explain why below).

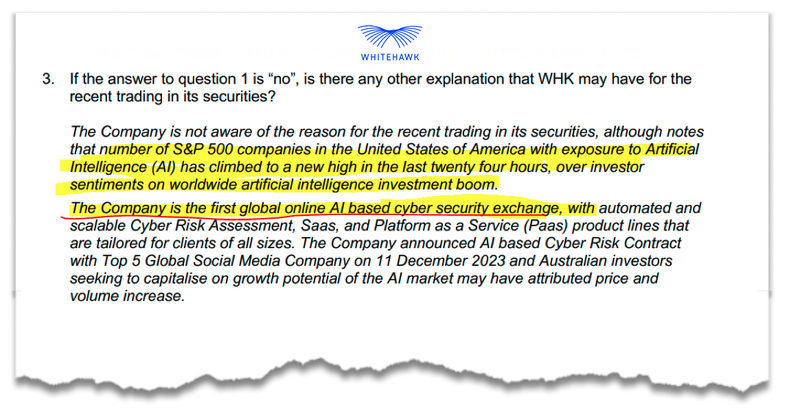

But on Friday, new investors looking for AI exposure seemed to catch on to the WHK story.

WHK saw its two biggest trading volume days in many years and a price rise from ~1c to ~3c on no news.

In a response to an ASX query on the volume and share price rise, WHK noted the sudden interest in AI stocks due to the strength in the AI thematic over the last 24 hours as a possible reason for the significant increase in its share price and volume:

(Source)

WHK took this surge in new investor interest as an opportunity to raise $2M at 2.25c per share this week.

We participated in this placement.

At the cap raise price of 2.25c and including the new shares, WHK is valued at a ~$10M market cap.

We are long term believers in WHK and have Invested many times since the IPO in 2017 (and before that in pre IPO rounds), mostly at a share price above 10c.

As of the last guidance in the middle of last year, WHK had a sales pipeline worth US$22M.

And there was over US$12.5M in potential contracts that could be on the table for WHK’s Cyber Risk Radar product alone.

We don’t expect them all to convert into revenue, but even if a portion do, it will be materially significant to WHK’s bottom line.

(And the “new large contracts” could be the proof point the market has been waiting for.)

A quick scan of the management commentary in the most recent quarterly shows some large ($1M plus) deals are in the pipeline and partner channels that have taken ages to develop are now finally showing signs of materialising as major deals for WHK.

Here is a quick summary of what jumped out at us from the quarterly:

- Cyber Risk Radar quote for $1M, pending procurement decision in March 2024 - one of WHK’s main products, this $1M contract would provide a good foundation for WHK’s 2024 revenue.

- Critical Infrastructure Cyber Risk Assessment (CIRA) Program contract for USD $1.9M expected in May/June 2024 - recent US news reports have focussed on how foreign adversaries are targeting the US critical infrastructure, which we expect to be a continuing theme. We think this avenue to a major contract is promising and could lead to additional sales for WHK.

- New Distribution Channel and Sales Partnership with Carahsoft Technology Corp - Carahsoft is a big private government IT solutions provider with US$11BN in revenue and some deep reach. We’re hoping this could drive further sales for WHK.

Basically what we need WHK to do in the coming months is sign these new contracts...

And start to announce revenue from the channel partnerships they have been developing over the last couple of years.

Here is a quick summary of WHK’s partners:

- [NEW] Carahsoft - With US$11BN in annual revenues this is the 45th largest private company in the US. The U.S. Department of Defense is one of Carahsoft’s largest customers. Along with a broad swathe of federal, state and local agencies.

- Dun & Bradstreet - A software analytics and business insights company with deep reach into the US public sector. US$2.16B in annual revenues.

- Peraton - Peraton is a massive US government IT services contractor with US$7BN in annual sales revenue. Peraton has a bid for a Veterans Affairs Supply Chain Risk Management (SCRM) contract awaiting award with WHK.

We think the market should reward WHK if it finally delivers on the above, and the stage is set with the AI boom to do this in 2024.

Contracts and partnerships aside, it looks like WHK’s long term AI work has been discovered by the broader market...

Why had WHK been trading at such a low share price before last week? What happens next?

WHK’s share price had been trending down over the last 18 months, initially due to a general tech sentiment drop at the start of 2022.

This was then followed by selling pressure from impatient holders due to delays to new, large contracts that the market was expecting, which left a gap in 2023 revenues.

This is understandable.

WHK’s large contract revenues can be lumpy and take years to secure.

Delays can cause impatient investors to sell and chase companies with more immediate catalysts.

But this is the challenge when selling to giant complex organisations like US federal government departments, US defence contractors and Fortune 500 companies.

The sales cycles are long.

BUT once WHK does sign up a big customer they become sticky long term users, and the contract values are generally large.

This is the benefit of large, difficult to obtain contracts - the lifetime customer value is high.

We are hoping that the huge volumes in the last two trading days will have given stale WHK shareholders a chance to exit and it has refreshed the cap table into a position where positive contract news will be rewarded if it is finally announced.

We have seen companies in the past show a lot of promise, develop great technology over many years, but the share price languishes due to taking a long time to sign new customers, shareholders lose patience and sell.

... then the share price makes a big comeback once the contracts finally start coming in and the shareholder register is refreshed.

This is what we want to see happen with WHK in 2024.

We are hoping WHK will pull off a OneView Healthcare style run from the share price lows after this capital raise.

OneView Healthcare has achieved a remarkable turnaround since our first Investment in the healthtech company in 2021 up ~440% and showing strong signs of momentum.

(with OneView, we were fortunate enough to be the incoming new fresh shareholders)

Like with OneView, the key for WHK will be to see a couple (ideally a few) long awaited, big contracts to be announced.

These are big sticky customers that take a long time to make decisions and this can make holding these companies difficult during quiet periods.

BUT it can also make for quick strong re-rates when the contracts do materialise.

WHK has a long history with AI

Driving WHK’s sales pipeline conversions will be CEO and Founder, Terry Roberts.

Terry has a deep understanding of AI and was the executive director of the Carnegie Mellon Software Engineering Institute from 2009 to 2015.

There, she established the Carnegie Mellon Cyber Intelligence Consortium and the Emerging Technology Center whose work continues today - with a special focus on AI.

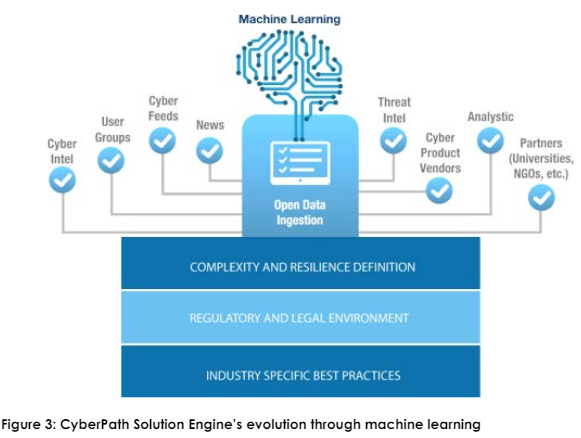

Since WHK’s founding, AI has been baked into the company’s software.

Below is an example schematic of WHK’s AI/Machine Learning product as it operated as of the 2017 WHK IPO when the company hit the boards (drawn from prospectus):

(Source)

Indeed, the 2017 prospectus listed this CyberPath Solution Engine (now renamed) as a key part of its value proposition:

(Source)

AI has been the key driver for investment in the tech industry since 2022, with OpenAI leading the charge with a massive US$80BN valuation (source).

Recently, the AI thematic got a massive boost with Nvidia publishing its earnings report last week and setting the record for the largest single day jump in $ terms for a stock.

There were sky high expectations on Nvidia’s revenue projections, and it beat them.

Single handedly pouring fuel on the positive sentiment in the market.

Nvidia almost hit a $2 trillion market cap to become the third most valuable US-listed company.

(Source)

Cybersecurity still remains a top priority for many companies with CEOs labelling it as the “top headache” in a survey conducted last year by KPMG (source).

Ultimately, the macro environment remains very strong for WHK, the key is for the company to now execute on some of its big contracts.

To win a US federal government contract, you may need a product like the ones WHK offers...

The US federal government is moving more quickly to defend itself against cyber attacks in the wake of a number of high profile attacks.

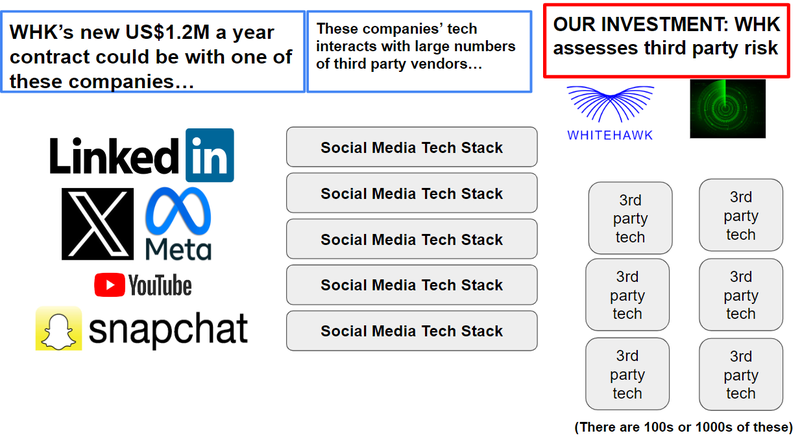

WHK specialises in Cybersecurity - Supply Chain Risk Management (C-SCRM).

Here’s an image which we think represents how WHK’s products and services work:

The same supply chain risks that social media companies face, also apply to US government agencies and their contractors.

Increasingly, these cybersecurity threats are sophisticated and so WHK is using AI and automation to tailor its products and services to the problems at hand.

Indeed, these attackers may themselves employ AI and automation to achieve their goals.

And it all points to a glaring need for products, particularly in the world of US government agencies...

While it may not be a riveting read - we read the following guide by the US’ General Services Administration (GSA) which manages federal property and provides contracting options for government agencies.

This guide is actually really important for WHK’s future prospects.

(Source)

Effective as of January 2024, the guide states on page 7 that -

“Federal executive branch agencies are now mandated to implement C-SCRM practices based on NIST standards and guidance and may choose to support their in-house capabilities by acquiring commercial off-the shelf (COTS) C-SCRM tools and services.”

These standards were updated yesterday:

(Source)

WHK has a key advantage for any company looking to comply with these standards.

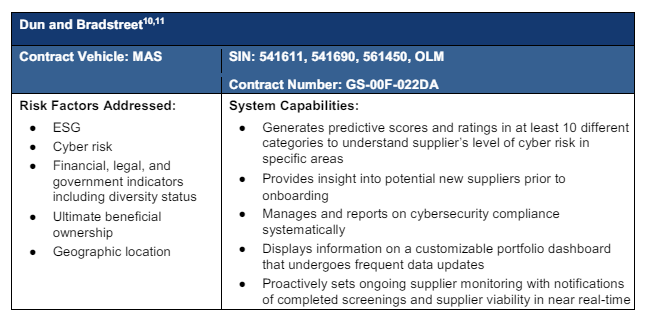

In particular because the guide published lists Dun & Bradstreet as one option for these C-SCRM services:

(Source)

Dun & Bradstreet is one of WHK’s sales channel partners and a key avenue for future big contract wins.

It is also worth noting that it appears as if GSA has moved to require C-SCRM practices apply to federal contractors (source).

While we did not relish pouring over the intricacies of US federal government bureaucracy when it comes to cybersecurity - it did lead to one big conclusion...

The key takeaway:

To win a federal government contract, you may need a product like the ones WHK offers...

WHK just got a new sales partner - Carahsoft

Today, WHK announced that has added a new distribution channel and sales partner called Carahsoft:

With US$11BN in annual revenues this is the 45th largest private company in the US.

The U.S. Department of Defense is one of Carahsoft’s largest customers and advertises itself as “A Top-Ranked GSA Schedule Contract Holder”.

If it's well aligned with GSA (which drives US government procurement of software) we expect Carahsoft will be a great fit to drive WHK’s products into more local, state and federal agencies and their associated contractors.

In announcing the sales partnership, WHK said the following in its preliminary final report with regards to what the Carahsoft partnership enables:

“The ability to include our Risk and Expertise Products and Services as part of Carahsoft’s National Association of State Procurement Officials (NASPO) vehicle. NASPO offers procurement vehicles for all states and municipalities – enabling our products to be acquired without direct engagement while also reducing potentially lengthy acquisition processes and approvals.”

We like the sound of that, as the WHK sales pipeline remains large and some of these big contract wins have been so far elusive.

Quicker time to a signed contract, the better.

WHK just raised $2M and an update on the Lind convertible note

WHK just raised $2M via an oversubscribed placement at 2.25c per share.

The new shares are expected to be issued on the 8th of March.

That adds to the company’s cash balance of US$103k at 31 December 2023.

But more importantly it gives WHK some balance sheet flexibility and a more conventional funding source for the company.

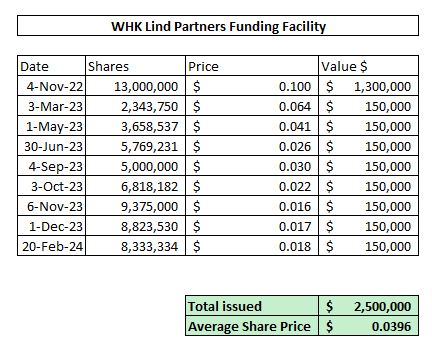

For much of the last year or so WHK has been funding itself using a deal signed with New York based Lind Partners.

That deal was signed in 2022 and saw WHK receive an initial $2M with the option of securing a further $1M.

The Lind funding deal is slightly different to the typical “cash for shares” deals we are used to seeing (i.e. placements).

Instead the deal sees WHK receive the cash upfront from Lind, and then Lind slowly converts the cash amount into WHK shares over a 12-24 month period.

So far, Lind has converted ~$2.5M of the facility into shares at an average price of ~3.96c per share - above the current market price.

WHK also had the right to access another $1M under the funding deal which at 31 December 2023 hadn't been touched yet.

BUT we did notice a conversion of $150k on the 20th of February 2024 so it is possible WHK has drawn down on the extra $1M available to it from Lind.

That could mean more conversions to come as the funds get converted into shares.

What does the funding facility mean for WHK’s share price?

Typically, with deals like this, the financier looks to sell some of the shares converted on market.

We have seen Lind sell down some of its position based on the two ASX notices (20 Jan 2023, 23 March 2023).

We do note though, that WHK has the option to pay for the remaining amounts in cash.

IF WHK can deliver material news, a re-rate in its share price to the upside and lock away a capital raise at a higher share price, generate positive cashflows OR get a lump sum upfront payment from a contract, then the company could just pay out the remainder of the Lind deal.

Ultimately, we want to see WHK deliver news and make that happen.

What could go wrong?

Sales Risk

Large, lumpy cybersecurity contracts, like the ones that WHK is looking to secure, can take longer than expected to eventuate.

WHK relies on the cash generated from these deals to support operations and maintain interest in the story.

If deals are taking longer than expected it puts pressure on the WHK balance sheet as well as investor interest may wane.

Funding / Dilution risk

WHK like all small caps is subject to funding and dilution risk.

Capital raises can lead to dilution and may take place at a discount, reducing the value of WHK shares.

Capital may not be available depending on the market, and may need to be secured through a variety of instruments which can undermine the financial and share price performance of the business.

Market Risk

The market could sell off or a bear market could continue for longer than expected taking the WHK share price down with it.

Competition Risk

The cybersecurity industry is a competitive space. Other companies may step in and take key clients.

Our WHK Investment Memo

Along with the key risks, our WHK Investment Memo provides a short, high-level summary of our reasons for Investing.

In our WHK Investment Memo you’ll find:

- WHK’s macro thematic

- Why we Invested in WHK

- Our WHK “Big Bet” - what we think the upside Investment case for WHK is

- The key objectives we want to see WHK achieve

- The key risks to our Investment thesis

- Our Investment Plan

==============

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.