HTG: Appoints new CEO (ex Raytheon, Optus Space & Satellite) to accelerate defence strategy

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 61,250,000 HTG Shares at the time of publishing this article. Some Shares are subject to shareholder approval. The Company has been engaged by HTG to share our commentary on the progress of our Investment in HTG over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs. Any forward-looking statements are uncertain and not a guaranteed outcome.

(Note: While HTG gave the market guidance that a new defence focussed executive team was in the works, this new defence focussed CEO appointment happened a lot quicker than we were expecting...)

Last week we added the defence (military tech) stock Harvest Technology Group (ASX:HTG) to our Portfolio.

We Invested in HTG now because it is pivoting its commercially tried, tested and revenue generating “communications link resilience” tech to an urgent new defence problem:

“Communications link resilience” in the battlefield for remote operated drones, robots, boats and vehicles.

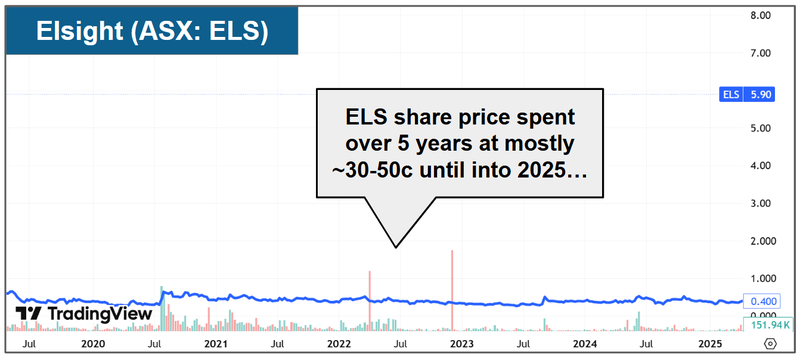

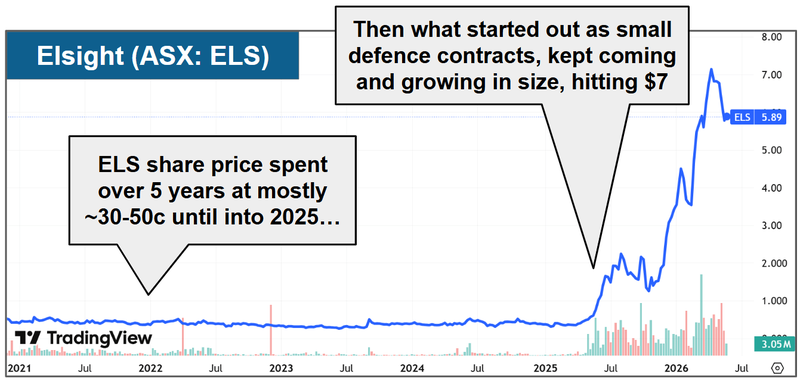

12 months ago, another ASX company Elsight pivoted its own “comms resilience tech” into defence and went from 30c to (now) over $7.50.

The past performance of Elsight is not and should not be taken as an indication of future performance of HTG.

Today HTG has further accelerated into defence with the appointment of a new defence focussed CEO Veronica Bainton (ex-major US defence contractor Raytheon, ex-Optus Space and Satellite)

(Source)

“Veronica joins Harvest with an extensive background in defence, space and national security, underpinned by deep expertise in defence procurement, Australian Industry Capability (AIC), sovereign capability development, and government and industry engagement”

HTG is currently trading at 1.8c/share.

The HTG CEO and Exec chairman are now on new incentive packages, which fully vest if the HTG share price gets to 10c (this is a stretch target, more on this in a second).

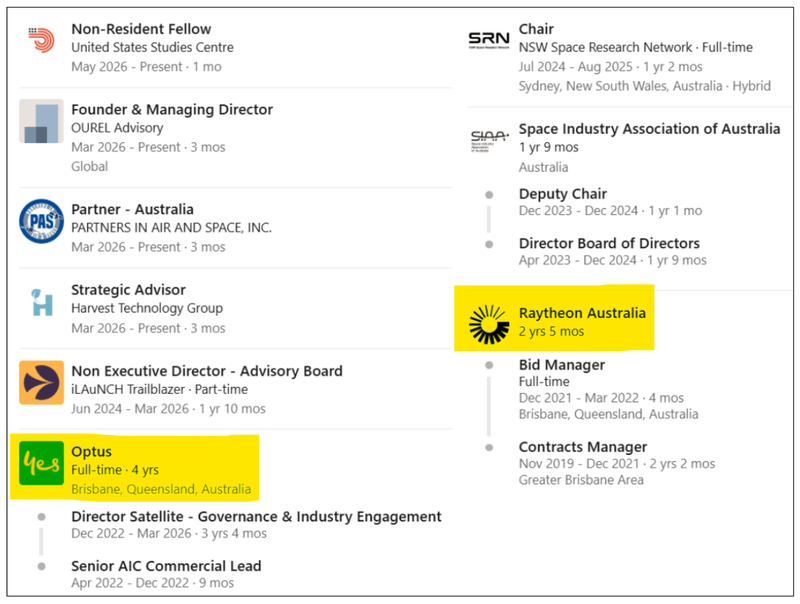

New HTG CEO Veronica has spent most of her career in sectors related to HTG’s defence pivot:

- Optus Satellite & Space Systems, where she led Team AUSSAT's bid for JP9102, the Australian Defence Force’s biggest ever satellite-communications program (~$4BN).

As Director, Governance and Industry Engagement at - Senior contracts and commercial roles at Raytheon Australia (the local arm of US defence contractor RTX)

(Satellite comms are now central to modern battlefield operations)

Also during her career she has held positions of:

- Chair of NSW Space Research Network and roles on the board of the Space Industry Association of Australia

- Plus senior commercial and compliance roles at gold miner Newcrest Mining.

In our HTG initiation note last week we pointed out that Exec Chair Jeff Sengelman, the former Australian Army two star Special Forces General, said his plan was to build a new, defence focussed executive team.

We had assumed this hiring process was still going to take some more time - starting following HTG’s recently completed $6.5M capital raise.

(can’t hire an elite executive team with no cash in the bank...)

But it looks like HTG has been running the process in parallel.

The new defence-focused HTG CEO starts TODAY, and has already been acting as an advisor to HTG for the last 3 months, so it looks like it's not a cold start. (source - LinkedIn)

So we have a quick post capital raise CEO appointment, starting today, with a 3 months head start as a strategic advisor.

A good setup for HTG to be able to deliver some quick traction in the defence sector (no waiting around for months as the CEO gets their feet under the table).

All we need now is a few new defence-focused partnerships/sales so HTG can hopefully start to emulate what its ASX peer Elsight did...

Elsight started small (a $475k deal in March 2025) (source), which got its tech into the defence ecosystem. Then, within 16 months, that small deal snowballed into 10s of millions of dollars in deals across North America and Europe.

Elsight’s share price went from 29c to $7.61, up over 2,500% as of Friday’s close in ~16 months (more on the Elsight comparison to early stage HTG later):

(source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

This shows the demand for “comms resilience tech” is there. HTG also has this tech.

Over to you Veronica...

Last week, there were reports that the US government was preparing to invest directly into American drone companies.

At the centre of it is the Pentagon's "Drone Dominance" program - a ~US$1.1BN push to stockpile roughly 300,000 low-cost attack drones by the end of 2027.

Drone and defence-tech stocks have gone vertical on the back of it.

Why? Because a ~$20,000 drone can take out a ~$2 million tank.

Overnight President Trump was even posting illustrations of a proposed drone port set to be built on top of his White House ballroom project:

(Source)

And in Ukraine - and more recently in Iran - the US has reportedly been firing ~$4 million missiles to knock down drones worth a few thousand dollars each.

This is the law of attrition - you don't need to win the war outright - you just need to wear down the enemy and make the costs of defending unsustainable.

The more we look into this new and urgent battlefield problem, the more we are seeing it in mainstream media:

Last night we saw an article about a proposed US$3BN sale of Radionor Communications' jamming-resistant radio tech ‘REDBOX’- (source)

3 days ago we saw headlines of Russian banks jamming drones - read our Saturday note about it here: Who wins on the battlefield when everyone's jamming everyone?

We think drones and unmanned, autonomous robots/vessels will be where future battles are won/lost.

But it won't just be about who has the MOST or BEST drones - the winners will be the ones who can keep their drones active and connected enough to execute missions.

Maybe that’s why SpaceX is going for an IPO at a US$2 trillion valuation...

(Starlink and its communication satellites are part of SpaceX)

No communication link - no drone/robot army - no sovereignty?

That’s why we Invested in HTG.

HTG’s tech can help keep everything (including drones, robots, unmanned vehicles) connected in the most contested communication environments.

(battlefields where each side is doing everything it can to jam communications).

HTG’s tech compresses data so HD video, voice and control survive in the lowest quality, most jammed environments - across any channel, satellite, cellular, RF, or any combination.

It's TRL 9 certified (the highest US Department of Defence readiness level - proven in real operations), with 500,000+ operational hours.

We covered all of this in our full HTG launch note from last week.

For years, the company was selling the tech to offshore oil and gas rigs as well as the shipping industry - pretty successfully (making 10’s of millions in revenues).

But the civilian commercial sector is slow - the problem there is NOT the difference between life and death.

We Invested in HTG now, because the company is pivoting toward selling into the defence sector.

Like Elsight did 12 months ago and went from 30c to $7.50 on rapidly growing defence sales.

Where the communication link could be the difference between winning/losing a battle.

Now, with Veronica Bainton in as CEO we think the HTG has the right team to execute that pivot into the defence space.

Veronica has been HTG’s strategic advisor since March - so she’s coming in warmed up and with game time in her legs.

She's spent her whole career in sectors related to HTG’s defence pivot:

- Optus Satellite & Space Systems, where she led Team AUSSAT's bid for JP9102, the Australian Defence Force’s biggest ever satellite-communications program (~$4BN).

As Director, Governance and Industry Engagement at - Senior contracts and commercial roles at Raytheon Australia (the local arm of US defence contractor RTX)

- Newcrest Mining. Plus senior commercial and compliance roles at

Here is her CV:

(source)

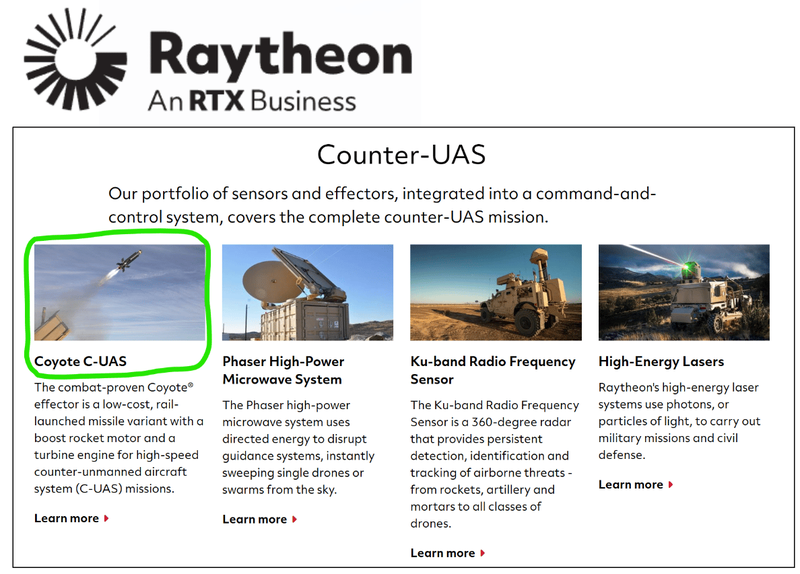

The big one on that list is Raytheon - one of the largest and most valuable aerospace and defence contractors in the world.

And they build just about anything for the military of governments all around the world.

Here is Raytheon’s portfolio most relevant to what HTG is doing:

(source)

We think defence is the hardest industry to crack because a lot comes down to trust and security.

Bringing someone like Veronica on board who has been on the other side of the table, working directly with the defence customers, could help bridge that trust gap for HTG.

Veronica and Jeff together can be the ones that get HTG’s tech into the right rooms, then by demonstrating that the tech works, HTG can turn that into contracts...

HTG’s ASX peer - Elsight - executed its pivot to defence in a similar way.

Elsight started small (a $475k deal in March 2025) (source) which got its tech into the defence ecosystem and eventually snowballed into 10’s of millions in deals across North America and Europe.

Elsight’s share price went from 29c to $7.61, up over 2500% as of Friday’s close in ~16 months (more on the Elsight comp later):

(source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Veronica will now be running the show together with Executive Chairman former Australian Army two star Special Forces General Jeff Sengelman.

Some serious defence pedigree now for a $33.4M capped (post raise) ASX small cap...

How’s this for the HTG Executive Chairman's CV:

- Spent much of his career in special forces

- Earned his SAS Sandy Beret in 1987 at the age of 25

- Commanded 4th Battalion, Royal Australian Regiment (Commando) (2000–01)

- Commanded 6th Brigade (2010–11)

- Deployed on operations to East Timor and Iraq (Working as director of strategic operations with US General David Petraeus)

- Commander Forces Command (2011)

- Deputy Chief of Army (2011–2012)

- Head of Modernisation and Strategic Planning – Army (2012–2014)

- Special Operations Commander Australia (2014–2017, retirement)

(Source)

All we need to see now is a few of these convert into deals, and for the market to start believing in the defence pivot.

HTG already has:

- Secured multiple orders from a significant Five Eyes defence customer for intelligence, surveillance and reconnaissance applications, including the deployment of 60 units to military robotics company Guerrilla Technologies. (source)(source)

(The Five Eyes is an intelligence alliance comprising Australia, Canada, New Zealand, the United Kingdom, and the United States).

- European Union Defence Force (EUDF) for naval fleet use. (source) Supplied telemedicine remote kits to the

- major NATO contractor following successful field trials. (source)

Secured orders from a - US defence contractor currently testing HTG’s technology within its drone product development program. (source)

A - Japanese Self-Defence Force (source), AND Trialled its tech with drones in the

- Brave1 accreditation, which is Ukraine's Government-backed defence-tech cluster (testing foreign vendors in real battlefield conditions) - think of it like Amazon for deliveries but it delivers pre-approved battle tech to locations in a battlefield. Ongoing

(source)

Over to Jeff and Veronica to convert those tests/trials and previous run-ins with potential buyers into deals...

Jeff and Veronica are both incentivised to see HTG re-rate to >10c per share

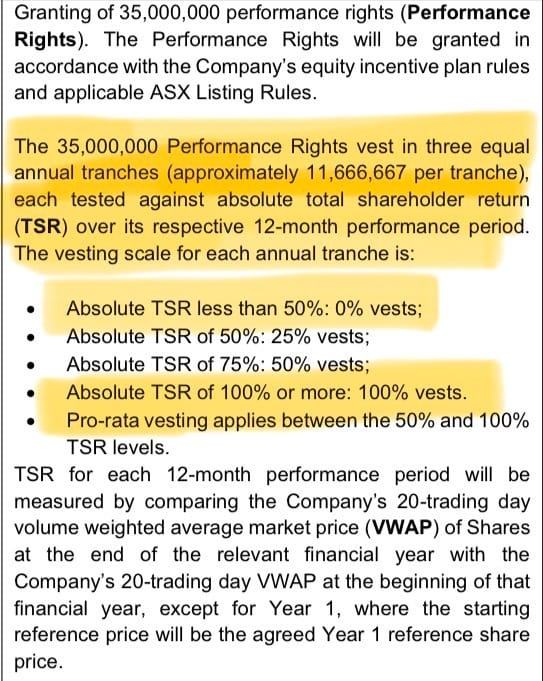

We also noticed in the back of today’s announcement that both Jeff and Veronica are being incentivised primarily with performance rights.

Tied to “total shareholder return” (TSR).

35,000,000 for Veronica and 25,000,000 for Jeff.

For 100% of the annual performance rights to vest HTG’s share price needs to be up at least 100% for the year.

IF the share price isn't up at least 50% then they get nothing...

(nice one, Jeff and Veronica, no lay-up performance rights and a pretty high hurdle set for those rights to vest)

(source)

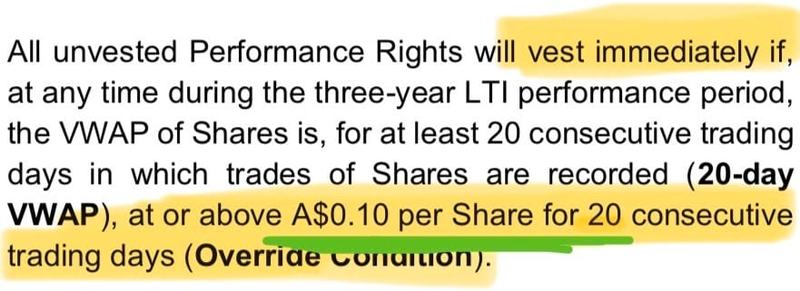

But the big one - for all of the performance rights to vest immediately - HTG’s share price needs to trade at or above 10c per share for 20+ trading days.

(source)

So Veronica and Jeff are incentivised to get it all done across a maximum of three years (with 1/3rd of the rights vesting annually).

OR (with some luck on their side) get it all done ASAP and have the rights vest immediately.

We are long-term investors, so three years is fine by us (of course, if we get to 10c sooner, we will take that too).

So what exactly is HTG’s Tech?

Most of us have never entered into a real battlefield as a soldier relying on communications that could save our lives...

But what many of us mere mortals HAVE done is play video games.

Have you ever been playing an online multiplayer game... and your internet cut out?

It doesn’t matter how much you were “winning” at the time...

Without internet, you can’t see what is happening in the game OR make your character take any action.

You are a literal sitting duck that can’t see or respond to anything... and you will lose.

Even a 1 second lag can mean the difference between pressing a button in time.

Or has your Playstation controller battery ever died while battling the final boss... and you lose?

Many of us have been here

(or for the old multiplayer Nintendo it’s like your mate pulling out your controller cable when they were losing so they could get you)

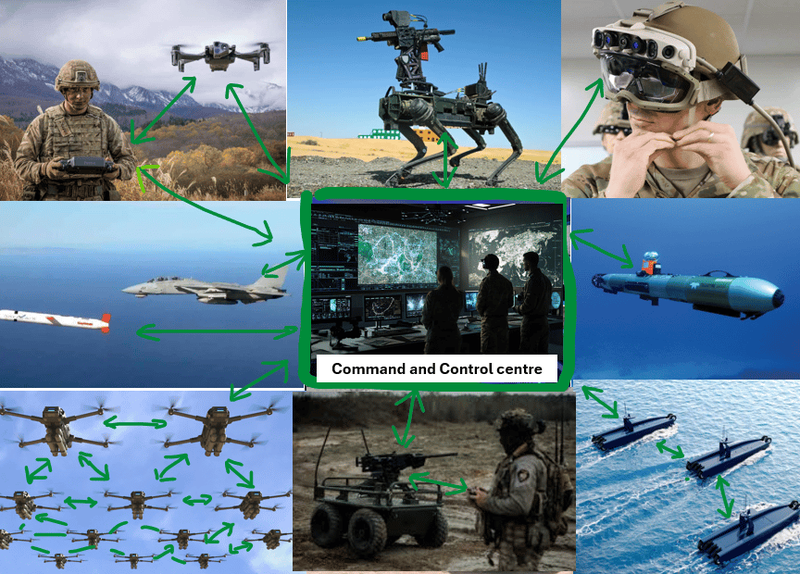

Now apply that same logic to a high stakes battlefield where you are relying on remote controlled, unmanned drones, robots, boats and vehicles....

Plus vital information coming from the central command.

Stable and resilient comms links are critical.

We certainly aren’t battlefield comms experts, but here are just some of the places where we think resilient two way communications are critical to co-ordinate on a battlefield (shown with green arrows):

So how are comms done on a battlefield?

- Satellite

- Cellular (3G/4G/LTE/5G)

- Radio (HF, VHF, UHF)

- Wi-Fi / Ethernet / any IP network

- Private networks

But guess what?

The enemy is doing everything they can to block, scramble, shut down and mess up ALL comms channels, all the time, as much as they can.

(equivalent of cutting off your internet or pulling out your controller cable mid-game - the fastest way to hobble you and win)

How do they disrupt comms?

Physical destruction of towers and ground stations, RF jamming, fibre and sub-marine cable cuts, state-ordered shutdowns, GNSS spoofing, cyber attacks on management/ground infrastructure, signal interception, DDoS and congestion flooding, supply chain compromise

(plus about 50 more ways - too many to list.)

And as the use of remote operated and unmanned drones, robots, boats and vehicles surges in the battlefield...

stable, reliable, resilient comms in contested environments become EVEN more critical.

Again, HTG’s Nodestream tech compresses mission-critical data to survive the thinnest, most degraded pipes (comms links).

HTG’s Nodestream tech squeezes HD video, voice, telemetry, and control data through ANY connection that happens to be available: satellite, cellular, RF, or any combination.

When conventional systems break due to congestion or electronic warfare, HTG’s Nodestream maintains real-time visibility and control.

Every "fire-and-forget" smart weapon in the world depends on a working comms link or GPS signal.

Jam the link, lose the weapon.

In 2024, ~US$112,000 Excalibur GPS-guided artillery shells in Ukraine saw accuracy fall from 70% to 6% as Russian electronic warfare jammed their satellite guidance. (source)(source)

(so much that the US stopped sending these to Ukraine - all because of comms jamming)

(source)

Even Australia's National Defence Strategy now explicitly calls "assured access to space-enabled communications" foundational to military effectiveness.

Another example, in Ukraine, Starlink has been called a "vital layer in Ukraine's overall communications network" by the Pentagon. (source)

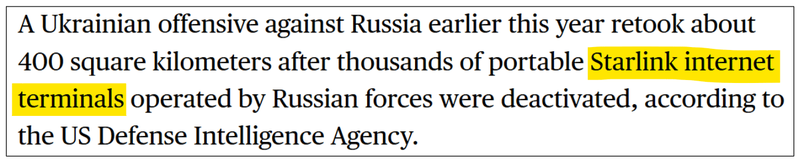

Russian jamming systems are creating electronic interference so dense that drone video feeds dissolve into static.

When Ukraine deactivated Russian-held Starlink terminals earlier this year, the Ukrainian army recaptured ~400 km2 of territory in the weeks that followed.

(source)

Combine HTG’s tech with something like Starlink then connect that all to drone swarms - you get where this is going.

(HTG’s tech was actually first developed to strengthen comms through weak satellite links for ships and oil rigs way out in the ocean, so HTG’s satellite game is very strong) (source)

Here is everything HTG has explicitly set as its target market for its Nodestream technology - and yes, it’s remotely operated and unmanned drones, robots, boats and vehicles... and the command and control centre:

(source)

HTG reminds us of $1.7BN Elsight

A similar story to HTG that’s done very well recently is Elsight Ltd (ASX: ELS).

We think Elsight is a good measure of “what success could look like” for HTG.

And most importantly verifies that there is an urgent demand from the military/defence sector for comms resilience tech.

Elsight plays in a similar (but slightly different) field to HTG.

Elsight owns a drone connectivity platform that lets unmanned aircraft stay connected across LTE, 5G and satellite networks simultaneously.

Elsight’s tech works in drones and unmanned systems basically as a smart modem - taking whatever connection is available at any given time and then combining them into a single, more reliable connection.

So Elsight's strategy is essentially: "Use MORE networks to guarantee a connection."

HTG’s tech is more about bandwidth optimisation/compression technology - squeezing high-quality video, audio and data through a single weak, slow or unstable connection.

HTG’s tech is more so designed for when networks are being jammed or contested (like they are on battlefields).

So HTG's strategy is essentially: "Use LESS bandwidth so even one single bad connection works... on ANY type of connection that happens to be available"

Both spent years deploying and refining their tech in the civilian commercial space - now both are applying their tech to a new and urgent battlefield problem.

(interestingly, HTG and Elsight’s tech are complementary and looks like they can be used together/ combined)

We actually Invested in Elsight’s IPO back in 2017 at 20c (we only put in a few thousand dollars and sold way too early - still kicking ourselves about that one).

That one went to $4 pretty quickly after the IPO in 2017 - then fell all the way back down to 25c in 2019.

Then for the next 5 years the stock traded mostly sideways while they thrashed around in the commercial space where there just wasn't any real urgency to solve the comms strengthening problem.

Only 12 months ago, ELS was still trading at ~30c with a pretty modest $2.1M in revenues squeezed out of the commercial sector for FY24.

(source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

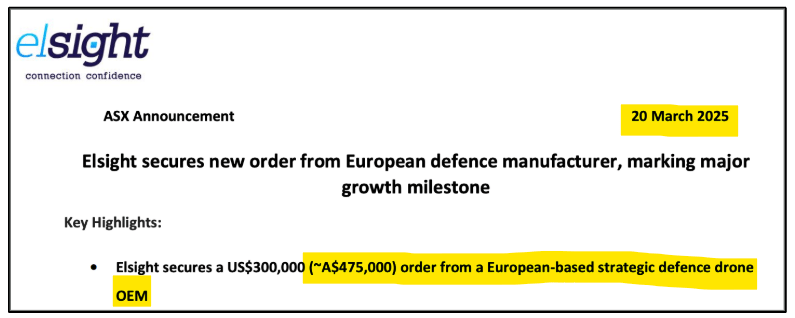

Then in March 2025 Elsight signed what at the time looked like a pretty small deal... with a European defence manufacturer for $475k:

(source)

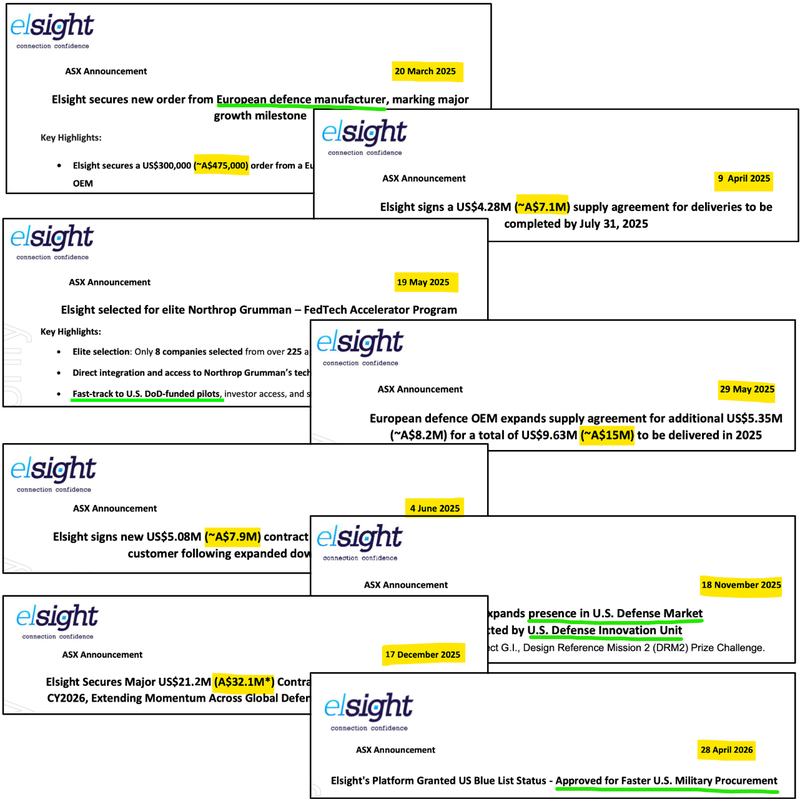

That single deal, which looked small in March 2025, opened the floodgates to much bigger US/European deals - over 7 individual contract wins worth tens of millions of dollars.

Here are some we took screenshots of while doing our due diligence on our Investment in HTG:

(source)(source)(source)(source)(source)(source)(source)(source)

We think that just goes to show how once you get one foot into the door in defence procurement, things can snowball pretty quickly.

Elsight has now in the last 12 months had:

- Lockheed Martin integrated its Halo tech into its Indago4 quadcopter.

- Northrop Grumman brought Elsight into its FedTech Accelerator (8 picked from 223 global applicants).

- The US Department of War's Drone Dominance Program added Elsight to its engagement list.

- European defence drone customer wrote ~A$32M of contracts in 2025 (a 600% jump on Elsight's entire FY24 revenue). A single

Now, Elsight’s market cap is ~$1.3BN and its share price at its peak was up almost 20x.

(source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

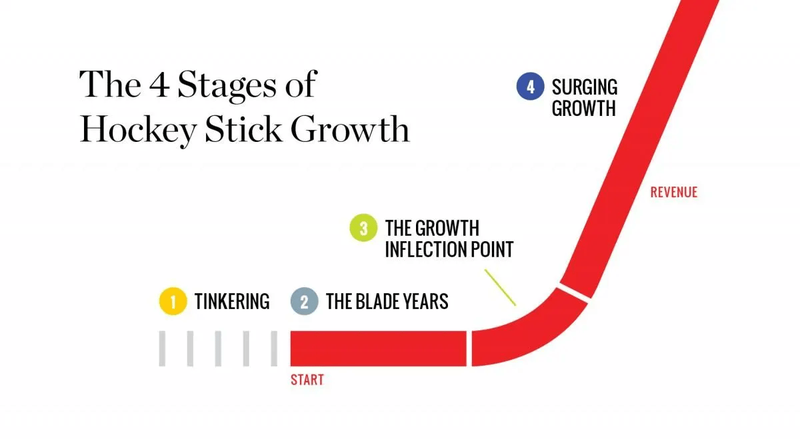

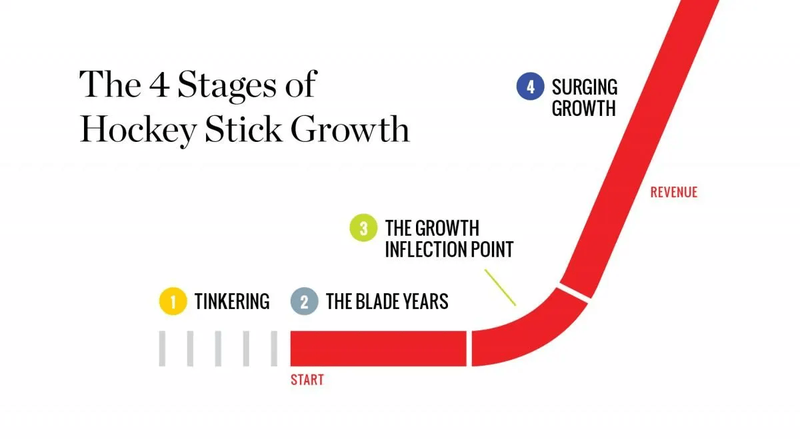

Elsight’s revenues (and share price) then tracked the “hockey stick growth” chart that is typical of SaaS style businesses:

We are Invested in HTG to see it try to execute on a similar playbook.

Hopefully, we are coming in just before that big hockeystick moment... while acknowledging there’s no guarantee of future sales momentum.

(source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

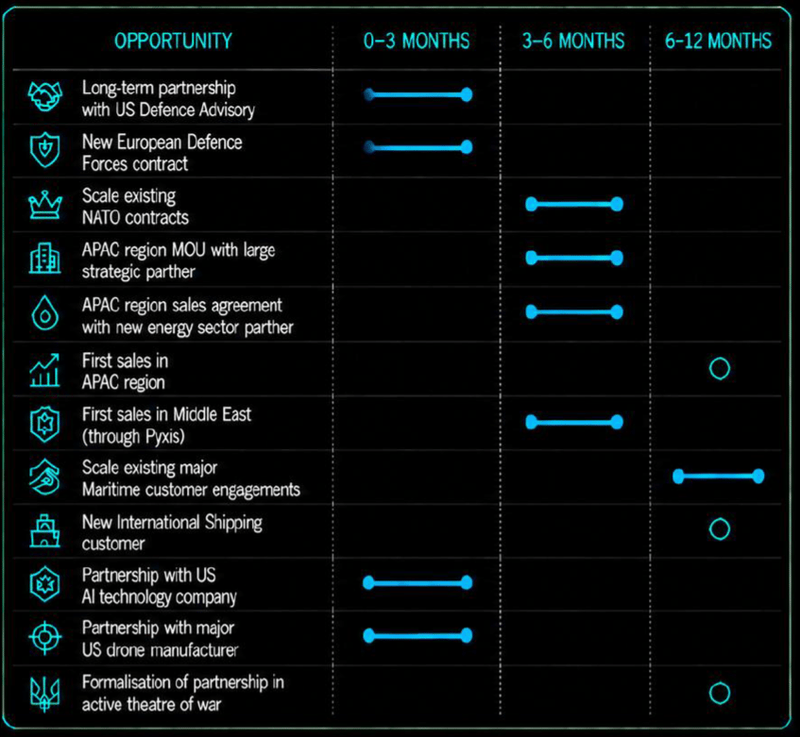

Where could HTG’s deals come from?

Our Investment case for HTG is pretty simple

We want to see HTG land contracts or partnerships with customers in the defence or telecom space.

The holy grail would be the Pentagon OR someone like SpaceX (Starlink).

IF HTG can embed its tech into Western defence programs (drones, surface vessels, submarines) then we think the market could start to believe in the defence pivot story for the business.

...and at that point, HTG’s technology enters stage 3 of the tech “hockey stick growth” trajectory - which we as Investors in these type business hope opens up more deals (stage 4):

Here's where we think those deals could come from:

- Converting existing trials - the Five Eyes customer (60 units to Guerrilla Technologies), the NATO contractor, the US contractor testing HTG’s tech in its drone program, the Japanese Self-Defence Force trial - into larger, repeat, paid contracts.

- The US market - an independent US advisory firm concluded HTG has "a credible and differentiated opportunity" in defence applications where comms resilience is a requirement.

- Ukraine, via Brave1 - if accreditation converts into live battlefield deployment that will give HTG a nice way of proving its tech to European (and US) defence contractors.

- The satellite operators (across the US, Europe and Asia Pacific) - Think satellite operators like Starlink (SpaceX).

8 reasons why we are Invested in HTG

Here are the 8 reasons we Invested in HTG, exactly as we set them out in our launch note last week (with two updates after today’s news).

1. HTG’s tech enables remotely operated and unmanned drones, robots, boats, submarines and vehicles

HTG’s tech connects video and audio streams across remotely operated and unmanned drones, robots, boats, submarines, vehicles and infantry - anything that needs stable comms to be effective in contested and degraded communication channels.

(basically a way of bulletproofing network connectivity)

HTG’s tech can also be applied to other remote locations like offshore oil rigs, facilities in the middle of deserts and in parts of the world where connectivity is limited.

2. We are backing the defence focused team

HTG’s Executive Chairman is Jeff Sengelman - a retired 2-star major general who ran Australian Special Forces operations for years.

We think that Jeff’s networks in the highest levels of the AUKUS, Five Eyes and the NATO communications procurement stack can help generate new sales momentum in the defence industry.

We also think HTG’s recent strategic advisor appointment, Veronica Bainton, has the right set of expertise - Ex-Optus Satellite & Space Systems and Raytheon Australia (big US defence contractor).

🚨 UPDATE:

Veronica Bainton is now CEO.

3. Tired, stale shareholder base means opportunity for new Investors like us

Some of our best tech Investments have been companies with existing shareholders that are stale and tired given the years of delays landing the transformational “mega deal” that has been around the corner for years:

- Oneview Healthcare (ASX: ONE) in March 2021 at 6c per share - at its highest point ONE was up ~858%. We Invested in

- AML3D (ASX: AL3) in June 2024 at 6.4c per share - at its highest point AL3 was up ~431%. We Invested in

- Rocketboots (ASX: ROC) in March 2025 at 8c, at its highest point ROC was up ~513%. We Invested in

The past performance of ONE, AL3 and ROC is not an indicator of the future performance of HTG.

We think HTG is in a similar position to where those companies were when we first Invested - where there is fatigue in the current shareholder register and the market is pricing the company for the big mega deal never landing.

4. HTG’s tech has >500,000 operational hours and is TRL 9 certified.

HTG has logged >500,000 operational hours in commercial sectors already - shipping, oil and gas and even part of a NATO trial.

HTG’s tech has been used by companies the size of US$642BN Exxon Mobil. (source)

“Technology Readiness Level 9” (TRL 9) certified is the highest possible US Department of Defence technology readiness level.

It means HTG’s tech is actually deployed and proven in operations rather than "tested in a lab".

HTG’s tech has also been independently verified for defence-grade deployment with NATO-linked field testing and US contractor integration underway.

5. Full focus moving to defence

On the 2nd of April 2026 HTG released the outcome of an independent “Defence Strategy Review”. (source)

Straight after, HTG also commissioned an independent third-party technical validation of its technology with a "respected defence and aerospace advisory group" active across US and allied defence ecosystems.

Then on the 14th of April 2026, HTG announced the "Independent Assessment Supports US Defence Opportunity". (source)

We think this marks HTG’s full pivot to focusing its business on defence.

6. HTG already has defence market traction

HTG has already had:

- source)(source) (The Five Eyes is a premier intelligence alliance comprising Australia, Canada, New Zealand, the United Kingdom, and the United States) for intelligence, surveillance and reconnaissance applications, including the deployment of 60 units to military robotics company Guerrilla Technologies. (source)

Secured multiple orders from a significant Five Eyes defence customer ( - source) Supplied telemedicine remote kits to the European Union Defence Force (EUDF) for naval fleet use. (

- source)

Orders from a major NATO contractor following successful field trials. ( - source)

A US defence contractor is testing HTG’s technology within its drone product development program. ( - source), and Trialled its tech with drones in the Japanese Self-Defence Force (

AND is currently going for Brave1 accreditation, which is Ukraine's Government-backed defence-tech cluster (testing foreign vendors in real battlefield conditions) - think of it like Amazon for deliveries but it delivers pre-approved battle tech to locations in a battlefield.

7. ASX listed peer has gone from 30c to $7 per share on defence pivot

A similar story to HTG that’s done very well recently is Elsight Limited (ASX: ELS).

Elsight plays in a similar (but slightly different) field to HTG - it owns a drone connectivity platform that lets unmanned aircraft stay connected across LTE, 5G and satellite networks simultaneously.

Over the last 12 months Elsight’s business has transformed from a pivot to defence - integrating its tech with Lockheed Martin, Northrop Grumman, The US Department of War's Drone Dominance Program and winning orders from inside Europe.

Now, Elsight’s market cap is ~$1.3BN and its share price at its peak was up almost 20x.

(From ~30c to a high of $7 off the back of its defence pivot)

We think HTG has similar potential if it can execute a successful defence pivot too.

The past performance of Elsight is not an indicator of the future performance of HTG.

8. Small $18M market cap - leveraged to a re-rate

HTG is capped at ~$18M, just raised $6.5M and has ~$13M in convertible notes outstanding.

So its enterprise value is ~$24M.

We think HTG’s share price would have been multiples of where it is today IF the capital structure didn't have a convertible note overhang.

We see those notes as one of the reasons HTG is investable at this market cap.

Strip them away, and then we think underlying business should be worth multiples of where it trades today.

We think that IF HTG lands a defence contract big enough to get the share price moving, then the note overhang becomes less of a problem and the company’s share price is allowed to move higher on good news.

🚨 UPDATE:

At last close, on a fully diluted basis (including the shares from the recent placement) HTG's market cap is now ~$33.4M at 1.8c.

With the convertible notes added on top, HTG’s enterprise value is ~$46M.

Ultimately, we are hoping a combination of the reasons above will lead to HTG achieving our Big Bet, which is as follows:

Our HTG Big Bet:

"HTG re-rates to a $200M+ market cap by embedding Nodestream into one or more major Western defence programs, attracting strategic interest from a defence contractor or satellite operator"

NOTE: our "Big Bet" is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including technology adoption risk, defence procurement timing risk, dilution risk, and competition risk - just some of which we list in our HTG Investment Memo.

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

What we want to see next from HTG?

🔄 Land a major US or NATO defence contract

- CEO hire (done - Veronica Bainton appointed) ✅

- 🔄 CFO hire

- 🔄 Convert the existing NATO defence-force trial into a paid contract

- 🔲 Sign a follow-on order with the existing Five-Eyes customer at a materially larger size

- 🔲 Contract with US defence contractors

- 🔲 Contract with EU defence contractors

🔄 Brave1 accreditation & Ukraine live deployment

- 🔄 Secure Brave1 accreditation

- 🔲 Deploy HTG's tech into a live Ukrainian defence-tech use case

- 🔲 Publish independent benchmarking results from Brave1 testing

What could go wrong?

The two key risks for HTG over the short-medium term is “capital structure risk” and “defence procurement timing risk”.

Capital structure risk

HTG has ~$12.8M in convertible notes outstanding with 239M options on issue (with a weighted average share price of ~2.86c per share.

IF HTG’s market cap doesn’t re-rate to a level high enough to absorb/pay off its debts, existing shareholders could be seriously diluted.

On the other hand the 239M options mean there is also a weight on HTG’s share price when those options get in the money - so there will be a period of churn around ~3c per share.

IF the balance sheet/capital structure isn’t cleaned up through execution + cashflows then it could be a drag on HTG’s share price.

Source: “What could go wrong” - HTG Investment Memo 27 May 2026

Defence procurement timing risk

Even when the defence customer is willing to buy, defence procurement cycles are notoriously slow.

NDAA compliance, Defence Federal Acquisition Regulation Supplement (DFARS), security clearances - any of these can add 6-18 months.

HTG's path to revenue depends on procurement clocks that HTG does not control.

Source: “What could go wrong” - HTG Investment Memo 27 May 2026

Other risks

Like any early-stage defense technology company, HTG carries significant risk, here we aim to identify a few more risks.

The company is shifting its focus away from an established, revenue-generating commercial oil and gas sector into an entirely new defense landscape. This major pivot means historical commercial revenue streams could slow down before lumpy defense contracts materialise.

Even with its high military readiness certification, successfully embedding HTG's proprietary technology into the sensitive systems of global defense primes involves massive technical integration hurdles.

Any technical friction or compliance delays during these complex hardware rollouts could quickly derail potential multi-million dollar partnerships.

Finally, the entire investment thesis is heavily exposed to key-person risk, specifically relying on the deep personal networks of the new CEO and Executive Chairman to open doors. If these relationships fail to convert active military trials into large-scale, binding commercial deals, the anticipated hockey-stick growth won't follow.

Investors should consider these risks carefully and seek professional advice tailored to their personal circumstances before investing.

Our HTG Investment Memo

You can read our HTG Investment Memo in the link below.

We use this memo to track the progress of all our Investments over time.

Our HTG Investment Memo covers:

- What does HTG do?

- The macro theme for HTG

- Our HTG Big Bet

- What we want to see HTG achieve

- Why we are Invested in HTG

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.