How big is it? CND resource estimate due - TotalEnergies next door

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 33,040,455 CND Shares and 11,925,000 CND Options at the time of publishing this article. The Company has been engaged by CND to share our commentary on the progress of our Investment in CND over time.

The tedious (but essential) work is pretty much done now.

Could a giant prospective gas resource emerge from this corner of the globe?

TotalEnergies is lurking nearby...

Our 2023 Energy Pick Of The Year Condor Energy (ASX:CND) has just finished re-processing legacy 3D seismic data across its giant Peruvian offshore oil and gas block.

This relatively low cost re-processing work vastly improves data quality, enhancing the oil and gas prospectivity.

The work was essential for a resource estimation across its three main prospects.

We think the new resource estimation will be the next major catalyst for CND - and it will help refine future drilling targets.

Ideally we can see the kind of numbers in the resource estimate that can attract greater interest in their huge offshore oil and gas project in Peru.

Aside from its three main prospects getting the ‘resource estimate’ treatment, it also has over 20 prospects / leads which lie outside of the areas that were subject to seismic reprocessing.

There’s already interest from the supermajors in this part of the world.

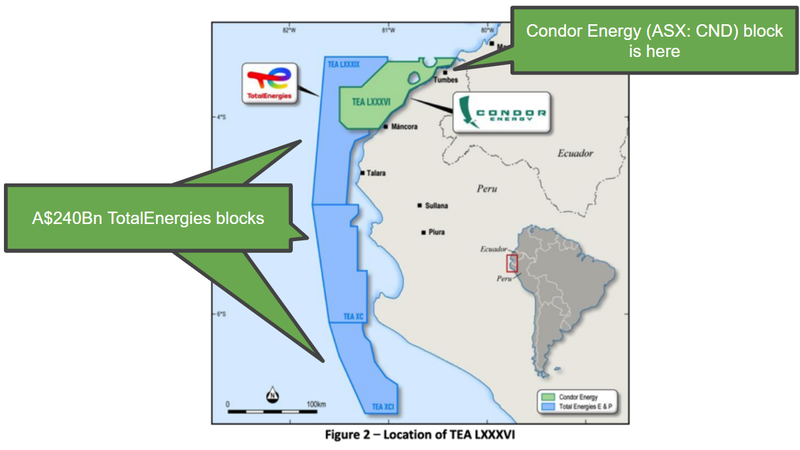

TotalEnergies, the ~$240BN capped French supermajor, sidled up next door to CND’s block earlier this year.

TotalEnergies basically surrounds CND’s block - see the blue shaded area on the map below:

$79BN capped Occidental Petroleum has finished undertaking a US$23M offshore seismic program in Peru too - through its subsidiary Anadarko. (Source)

Peru is undoubtedly one of the last major frontiers for big oil and gas exploration projects.

And CND has been steadily getting its ducks in a row, well ahead of the supermajors.

CND is capped at $17M and had $2M in the bank at the end of the last quarter.

Given recent work has been low cost desktop work, CND is in a decent spot.

At one of its three key prospects (Piedra Redonda) CND already has:

- a 404 billion cubic feet of gas (Bcf) contingent resource at one target (historical discovery) and

- a 2.2 trillion cubic feet (TCF) prospective resource.

Those are big numbers - but we now want to see a prospective resource across its three main prospects in the Tumbes basin, Peru.

Ultimately, CND will need to attract a partner to drill the asset, which would be some time off.

Between then and now we anticipate CND will steadily de-risk the asset, and with that should hopefully come a growth in CND’s valuation in the lead up to drilling.

We don’t know exactly when a resource estimate will drop, but it should be a share price catalyst as it will allow potential partners the ability to assess the merits of CND’s asset versus others around the world.

CND now has all the pieces of the puzzle to put that resource estimate together after extensive desktop work on the project.

Aside from gaining an understanding of the scale of the asset, the ultimate goal is to work out the best target to drill from a risk/reward perspective.

CND’s project covers 4,858km^2 of acreage right next door to projects that TotalEnergies picked up in May of this year.

The fact an energy supermajor has picked up ground all around CND, we take to be an excellent sign.

CND’s acreage sits across two separate basins (Talara and Tumbes) that have historically produced ~1.6 billion barrels of oil and are home to oilfields still producing at ~3,000 barrels of oil per day right now.

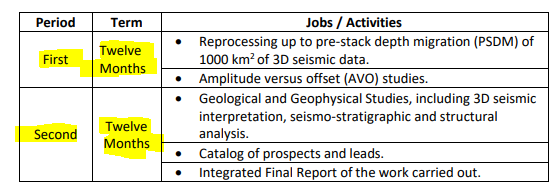

CND is currently working on the project under a Technical Evaluation Agreement (TEA), which sets out the work CND has to complete over 24 months.

A TEA is an oil and gas contract that provides the exclusive right to negotiate a Licence Contract with Perupetro (the Peruvian national oil firm) over the TEA area.

In exchange, CND will complete a 2-year work program where the company does a lot of desktop work, maturing leads and defining resources.

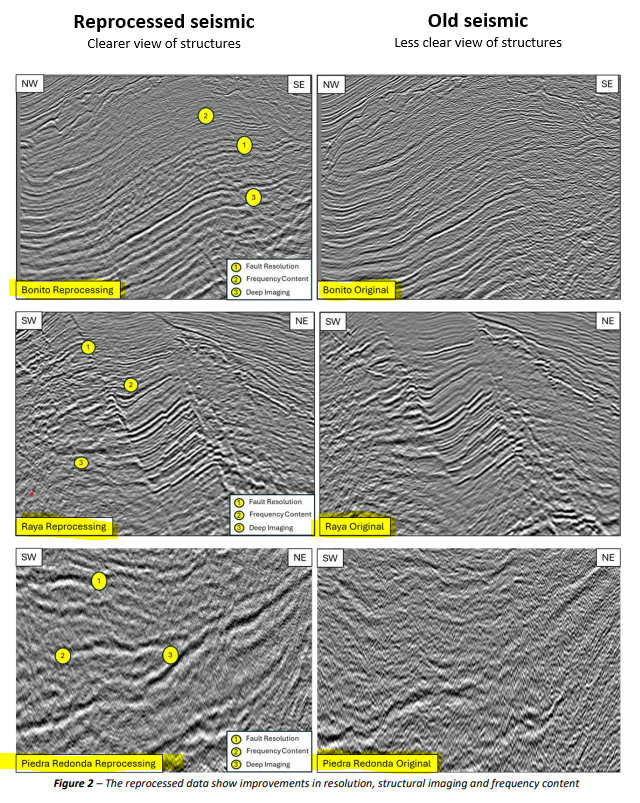

Today CND finished the seismic reprocessing part of its TEA work program - precursor to resource upgrades/estimates/updates.

Resource modelling is currently underway, so we should get news on that front pretty soon.

After today’s news, CND is roughly half way through its 24-month TEA period - this also gives a good snapshot of upcoming work:

CND’s project is pretty advanced relative to other offshore exploration projects - it has a confirmed gas discovery sitting inside its permit area.

AND CND has another 20+ leads that could end up being where we see CND choose to drill first

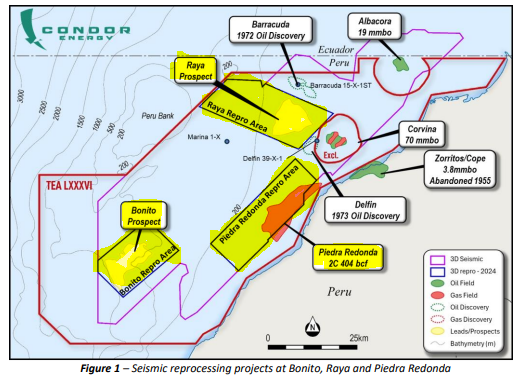

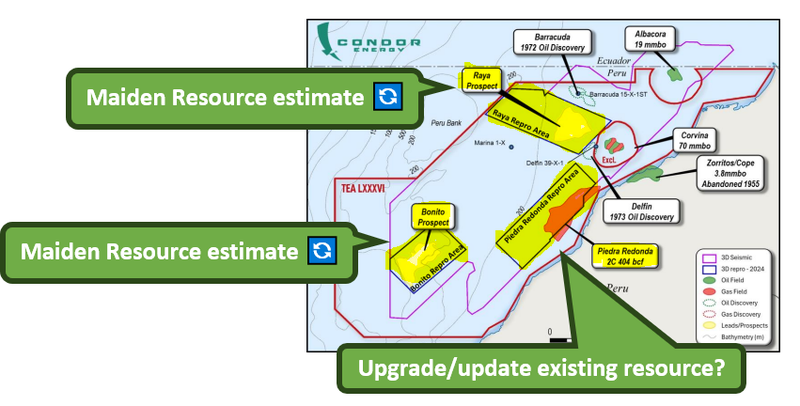

CND’s three focus areas

Today’s news confirmed that all the 3D seismic reprocessing had been completed across the three key prospects CND is working up.

CND’s three key prospects are:

- Raya: No prospective resource yet

- Bonito: No prospective resource yet

- Piedra Redonda: 404 billion cubic feet contingent and 2.2 trillion cubic feet prospective resource (on a 100% ownership basis)

Across Raya and Bonito, CND is yet to define a prospective resource.

At Piedra Redonda, CND has already managed to define a contingent and prospective resource.

That prospect currently has a 404 billion cubic feet contingent and 2.2 trillion cubic feet prospective gas resource (on a 100% ownership basis).

That resource was put together based on data from two old wells which flowed gas at 8.2 million standard cubic feet of gas per day.

We covered that news a few weeks back here:

CND announces details of historical gas discovery - and it has already flowed...

We think that on its own, the numbers CND has put out from Piedra Redonda are enough to underpin CND’s current valuation.

The contingent resource means CND already has a 404 billion cubic feet gas discovery (historical) and its market cap is just ~$17M...

Across its two other prospective areas, CND hasn't put out resource estimates yet - that’s where the next bits of newsflow for CND will likely come from.

By reprocessing 3D seismic data, CND is able to get a better understanding of the structures underground and can push this into its resource estimation models.

(Source)

To the untrained eye these just look like squiggly lines, but to highly experienced geophysicists - and to potential farm in partners, this more refined work is extremely helpful.

Now that this work is done, over the coming months across each of its three main prospects we want to see CND:

- Raya: put out a maiden prospective resource

- Bonito: put out a maiden prospective resource

- Piedra Redonda: upgrade/update its existing 404 billion cubic feet contingent and 2.2 trillion cubic feet prospective resource

Why we like where CND is right now

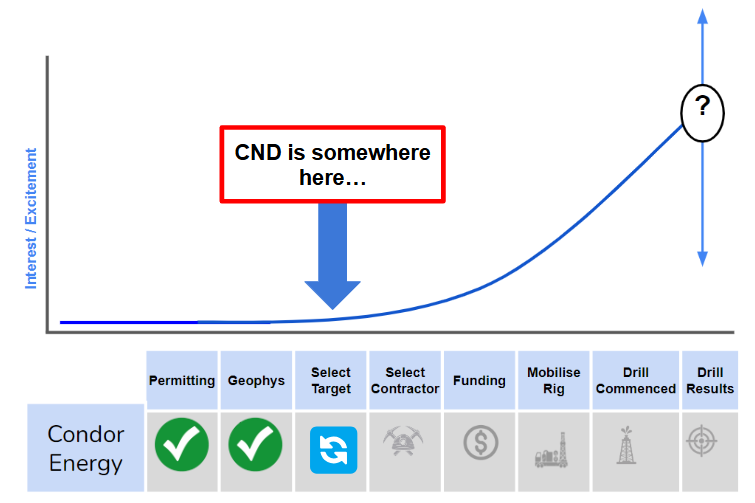

One of the main reasons we announced CND as our 2023 Energy Pick Of The Year was because of where the company sat relative to our tried and tested Oil and Gas Investment Strategy.

For those who have been following our Investments for a while with oil and gas explorers we tend to follow a five step investment plan.

Of course, before we show you our plan, we need to stress that there’s never a guarantee of success with speculative oil and gas investing. We recommend consulting with a professional financial advisor before choosing to invest in small cap stocks like CND.

Our general plan is to Invest early, and eventually, as a drilling event draws closer over the coming years we expect to see broader investor interest increase, and with that, growth in the company’s valuation.

- Invest early, as the company is in the early exploration work stage.

- Increase our Investment, as the company de-risks the project through permitting, geophysics and target generation.

- Top Slice, if the share price runs in anticipation of exploration results

- Free Carry, into results while still maintaining a large position to be leveraged for a discovery

- Evaluate our position post-drilling.

CND has briefly already traded ~100% above our Initial Entry Price of 1.9c per share.

Right now CND’s market cap is ~$17M - at the end of the two year TEA (remember CND is halfway through this period), we are hoping for CND’s valuation to be a lot higher (no guarantees though).

This will be due to the work put into the assets and the in ground value that could reasonably be inferred.

It's a similar strategy to the one we followed with another one of our Portfolio companies, Invictus Energy, which shares a common director with CND - Scott Macmillan...

With IVZ our Initial Entry Price was ~3.5c back in September 2020.

Over the years IVZ acquired seismic data, defined prospective resources and then drilled out a discovery - at its peak IVZ’s share price was up >1,000% from our Initial Entry Price:

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Again, CND’s market cap is still only ~$17M, similar to where IVZ was way before its first drill program.

CND is still at least 12 months away from any drilling so there is plenty of time for CND to churn through any market selling leading up to the first drill program.

Here is where we think CND is:

Note: This is a guide to potential market sentiment/interest not share price performance. Lots can go wrong and small cap investing is high risk. Past performance of other companies is not an indicator of the future performance of CND.

Ultimately, we are hoping that as CND sets out big targets and defines a drill program the share price re-rates in line with our Big Bet as follows:

Our CND Big Bet

“CND defines a multi-billion barrel prospective resource and sees its market cap re-rate by 20x prior to drilling”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our CND Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

What’s next for CND?

Here’s the key points:

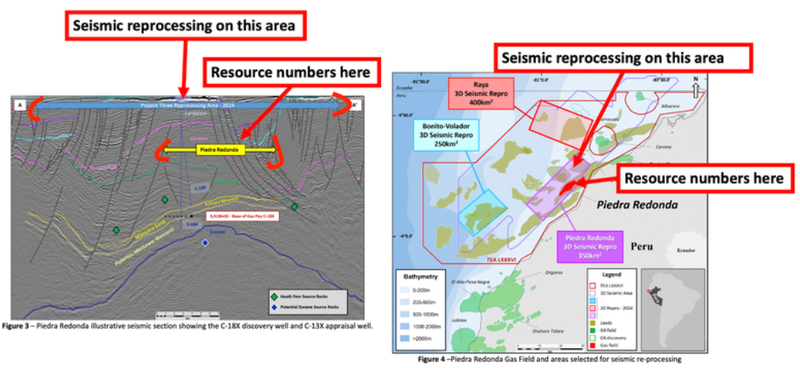

Target #1 (Bonito-Volador prospect) 🔄

At Bonito, CND just completed ~250km^2 of 3D seismic reprocessing.

Next, we want to see CND define a maiden prospective resource for the target area.

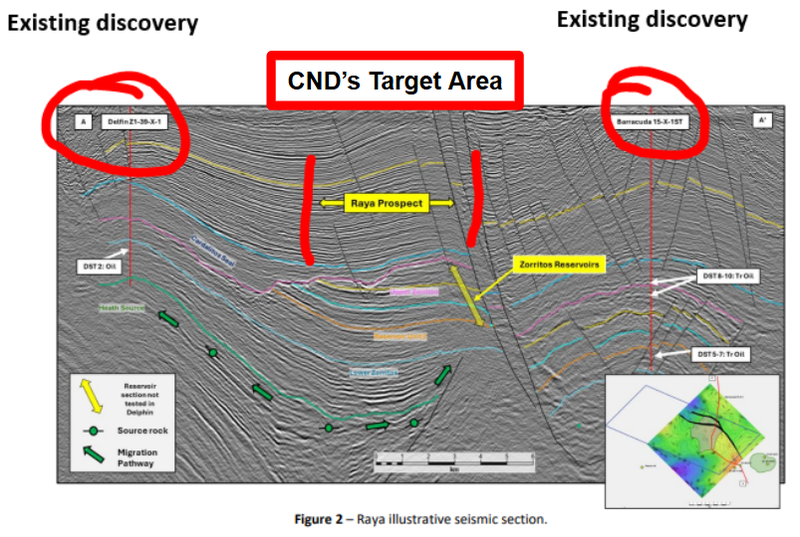

Target #2 (Raya prospect) 🔄

At the Raya prospect, CND just completed ~400km^2 of 3D seismic reprocessing.

CND picked Raya as one of its three main targets primarily because this part of its project had the potential for similar “stratigraphic and structural traps” to the two nearby discoveries.

The two discoveries are - Barracuda and Delfin, which were both confirmed oil discoveries.

Here we want to see a maiden prospective resource estimate again.

Target #3 (Piedra Redonda) 🔄

At Piedra Redonda CND just completed ~400km^2 of 3D seismic reprocessing.

As mentioned earlier, CND already has a 404 billion cubic feet of gas (Bcf) contingent resource and a 2.2 trillion cubic feet (TCF) prospective resource for Piedra Redonda (on a 100% basis).

That resource comes from only a small part of the overall area covered in Piedra Redonda.

Now with the 3D seismic data reprocessed we are hoping CND is able to increase the estimates from this project.

What could go wrong?

Every speculative oil and gas investment carries risk. CND is no different.

Below are some of the more obvious risks that we can see at the moment (of course there’s always risks no one can imagine).

Given that CND operates under a two-year “Technical Evaluation Agreement”, the company faces no short-term exploration risk as it is not required to drill test its asset.

As a result we think the key risk in the short term is “market risk”.

For the duration of the two year TEA, we expect CND’s share price to be impacted most by overall market sentiment and underlying oil and gas prices. Lower oil and gas prices could pull capital away from high risk explorers like CND.

To see more risks to our Investment Thesis, check out our CND Investment Memo here.

Our CND Investment Memo

In our CND Investment Memo, you can find:

- CND’s macro thematic

- Why we Invested in CND

- Our CND “Big Bet” - what we think the upside Investment case for CND is

- The key objectives we want to see CND achieve

- The key risks to our Investment thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.