HAR moves more uranium resource into “indicated” category as uranium price remains high

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 3,025,000 HAR shares at the time of publishing this article. The Company has been engaged by HAR to share our commentary on the progress of our Investment in HAR over time.

That uranium price looks to be holding firm at a level not seen for 15 years.

Uranium mines are restarting.

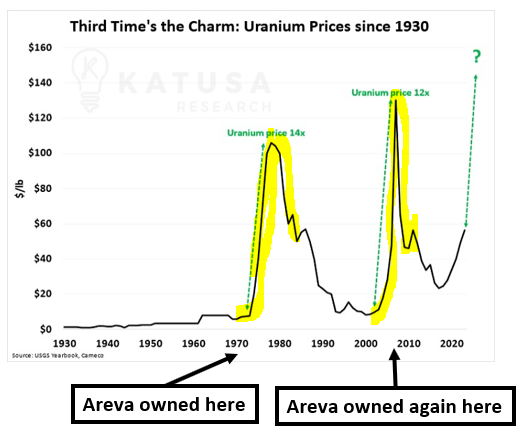

...and the French multinational nuclear company Orano (formerly AREVA) is putting money into getting more production online.

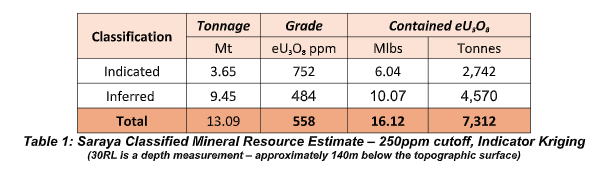

Today our early stage uranium Investment Haranga Resources (ASX:HAR) announced an upgraded resource at its project in Senegal.

The company has advanced around 37% of its 16 million pound uranium resource from the “inferred” to “indicated” classification.

This basically means HAR has established a higher confidence in the resource and the project is now more suited for development studies - which is part of the process of becoming an actual mine.

Importantly, the new resource has a headline grade of 752ppm (parts per million) for the indicated classification.

For reference, 752ppm is generally considered a high grade, with other mines in Africa like Paladin Energy’s Langer Henrich mine operating commercially at around 500 ppm in Namibia.

Today’s results allow for commencement of more advanced project development studies and planning for further resource expansion drilling.

HAR also says there is potential for significant exploration upside.

And there is a further resource update to follow the receipt of laboratory assay results.

Over the past six months HAR has undertaken an RC drilling program, publishing xRF results from 29 holes with assays to confirm these results soon.

There were two main goals of the RC drill program:

- Upgrade the existing JORC resource through infill drilling

- Make a new uranium discovery by following up on high priority targets

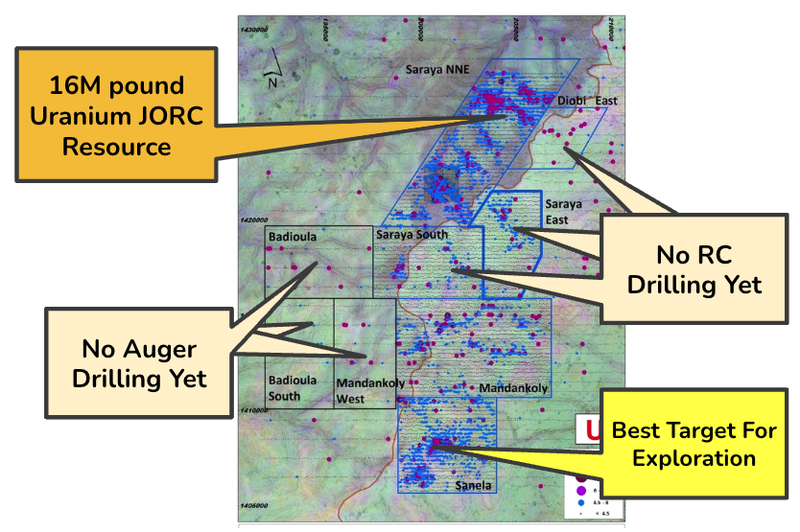

Of the 29 holes drilled, 18 of them were allocated to the Saraya target (which is where the previously inferred ~16Mlb resource is located).

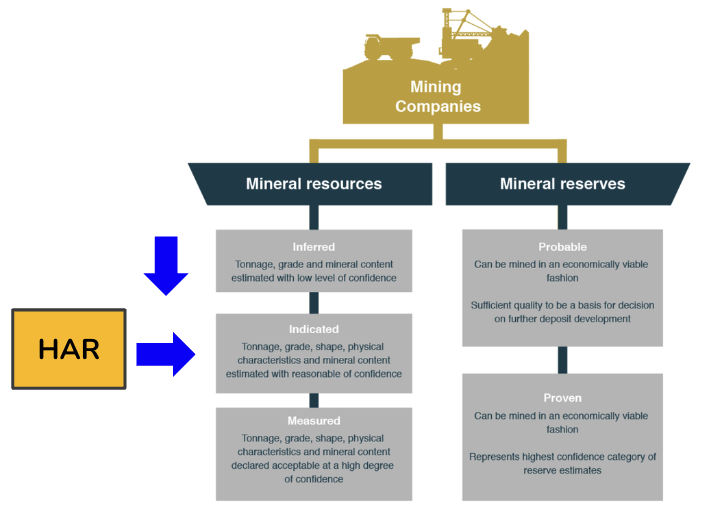

Upgrading the JORC resource is important for larger investors who focus on later stage companies.

The higher the classification of the resource, the more “certainty” in the deposit.

Institutional investors in later stage companies and larger players looking to make a takeover bid want the maximum amount of certainty in the deposit before investing.

So upgrading the classification works towards the long term future for HAR’s project.

The other nine holes were allocated to three other targets.

Unfortunately the exploration dice didn’t come up at the first two - No significant mineralisation was found but the third target, Sanela did manage to hit some uranium mineralisation:

Although the mineralisation at Sanela wasn’t enough to declare an official “discovery”, it does warrant further drilling, which we hope to see in HAR’s next drilling program.

In short, although HAR was not able to immediately declare a new discovery, it did uncover valuable information about its project and there are plenty more targets to test.

Our HAR Big Bet

“HAR re-rates to a +$100M market cap on significant resource growth and/or a transaction with a major player in the nuclear fuel supply chain”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our HAR Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

HAR upgrades classification of its JORC resource, metwork solid

Today HAR announced that it had upgraded the shallow part of its JORC resource from the inferred to indicated category.

This added certainty about the presence of uranium mineralisation should hold the company in good stead as it goes about development studies.

Development studies need to also take into account how to get the uranium out of the ground - which is where metallurgical testwork (or metwork) comes in.

Last month, HAR announced that it had achieved >96% uranium extraction from metwork testing which is quite strong for a first pass at metwork.

It’s a comparable recovery to other producing projects - which is a good early sign. (Read the Quick Take)

The exploration potential of HAR’s project

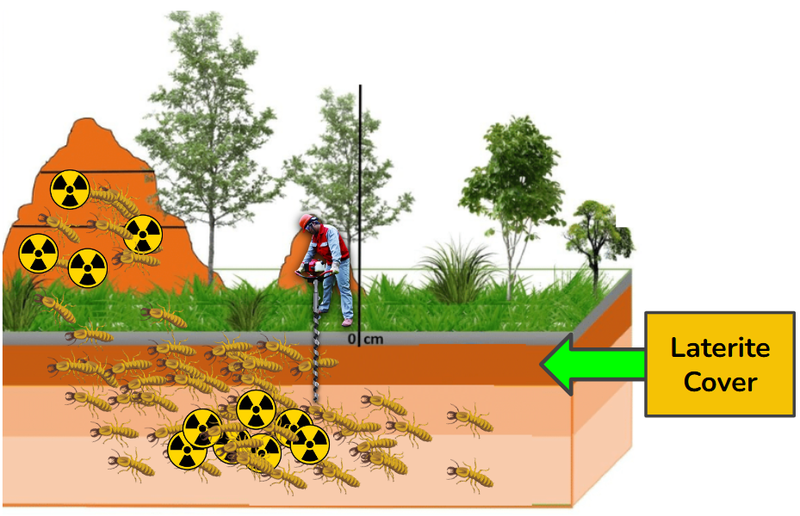

85% of HAR’s project is covered and obscured by “regolith”.

Regolith is basically rocks, sediment, dust, debris, etc... that sit on the earth’s surface and make it hard to identify the source of mineralisation.

In the exposed 15% of the project area (no regolith), the previous owners of the project were able to identify surface mineralisation and discover and develop the resource at the Saraya Prospect (where HAR upgraded the resource today).

This regolith in all the other areas makes it difficult to identify further areas of mineralisation through traditional means of discovery.

But HAR has been using a clever work around...

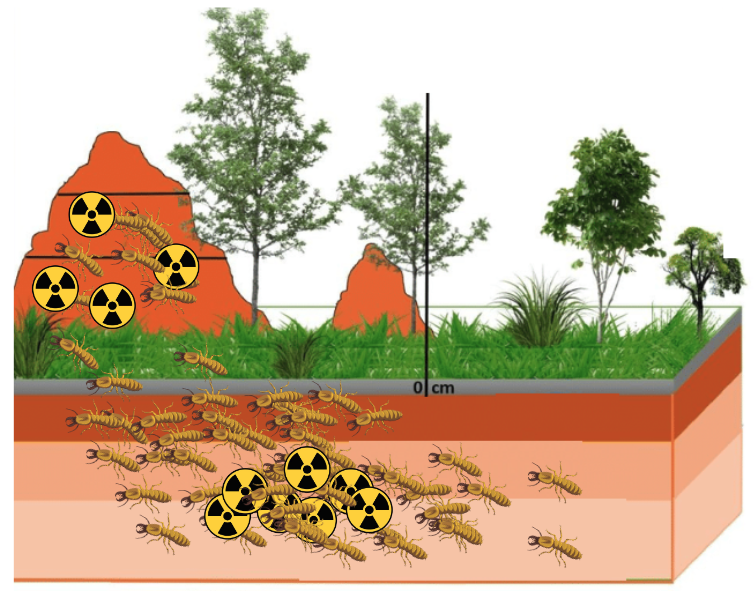

HAR utilised the approach of using termite mounds and auger drilling to identify high prospect targets.

(yes - actual termite mounds)

Like with all early stage exploration, uranium mineralisation may or may not be there...

However, if HAR is willing to put in the work, fund exploration and get a bit lucky, it could make a significant uranium discovery.

So, this is what HAR’s target generation and exploration strategy looks like:

- Stage 1: Termite Mound Sampling (Regional)

- Stage 2: Termite Mound Sampling (Infill)

- Stage 3: Auger Drilling

- Stage 4: RC Drilling

Stage 1 & 2 involve termite mound sampling.

Essentially soil from termite mounds are tested for uranium anomalies because termites bring up particles from deeper geological layers that are not accessible from conventional soil sampling:

These are like the “Regolith Eaters” in our favourite board game Terraforming Mars:

HAR is able to use these mounds to identify any uranium that termites may have pulled from under the surface of the regolith.

HAR is not able to use conventional means of soil sampling because of the regolith and laterite cover which obscures the underlying geological features.

To breach this laterite cover, and better understand what is going on below, HAR will undertake stage 3, an auger drill program.

(an auger drill is a hand held drill, sort of like a jackhammer but for drilling)

Important to note is that termites move around.

So where uranium is found in the mound above the surface, may not be where the uranium exists directly below.

It’s essentially a puzzle.

To make the puzzle clearer, auger drilling is used with shallow holes, generally 5-15m, to better understand the geological features below.

Once the auger drill program is complete, the company will have high priority drill targets to undertake RC drilling, which allows for a much deeper drill program to better identify and uncover the uranium resource.

For HAR the regional termite mapping uncovered around eleven prospects.

From these eleven prospects six auger drill targets were defined with three of them being tested with the RC rig...

Of the three tested, one prospect showed promising signs of mineralisation, with the Sanela prospect being the most interesting exploration target for HAR.

Because of the regolith obscuring the geology of the project uranium mineralisation could come from anywhere.

We think there is strong exploration potential here, HAR just has to drill it.

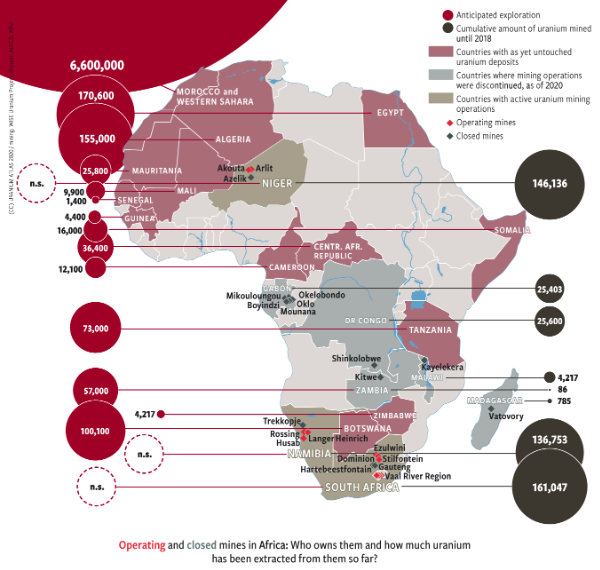

African uranium - risks and rewards

Uranium production in Africa generally comes out of three countries, Niger, South Africa and Namibia.

The continent has significant, untapped exploration potential, particularly in West Africa and countries like Senegal (where HAR’s is located).

There have been two major stories from uranium majors in Africa that highlight the opportunity (and risk) and for uranium companies in the area.

Paladin restarting its uranium mine in Namibia...

and Orano losing its uranium project in Niger.

Here’s what happened:

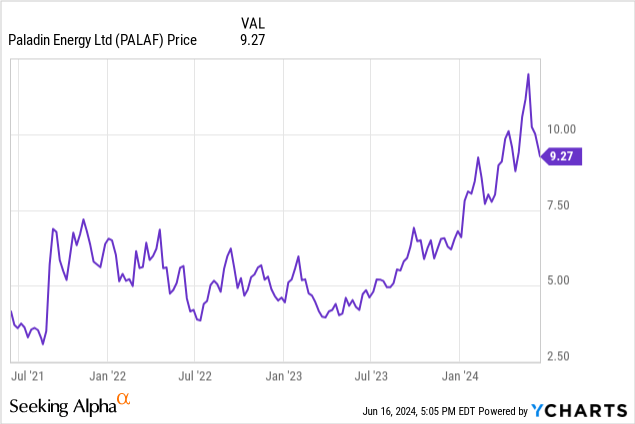

Paladin Energy restarts its Namibia mine

Last month, Paladin Energy (capped at $4B) restarted commercial operations at its uranium mine in Namibia.

The Langer Henrich, located in Namibia, has been in care and maintenance since 2018, and was put on ice after the last uranium bull market subsided.

Now, Paladin has commenced commercial production, producing and drumming its uranium concentrate ready to be shipped next month.

(Source)

On full ramp up, the company expects to produce around 6 million pounds of uranium each year, with around 77 million pounds in the mine plan.

The company’s share price has been climbing for the past few months and is a reflection of the investor interest in uranium projects in the region:

The key driver for the mine restart was the uranium price.

Although the uranium price has cooled slightly to around US$85-$90 per tonne, it is still well up over the past 18-months.

For companies like HAR, at the exploration side of the mining company lifecycle, restarting of mines is a very good sign of interest in the particular commodity and investor confidence in the region.

We think that big companies like Paladin Energy show the strong potential for African mining deposits.

Now, for the risk.

French Uranium company Orano at risk of losing Niger Mine

Orano, is a major French mining company that owns the Imouraren mine in Niger.

Interestingly, it was Orano (formerly Areva) that owned the ground that HAR is now exploring.

Orano did all of the initial reconnaissance and drilling, but shifted its focus to a big discovery in Niger and relinquished the HAR’s project... twice.

In Niger, Orano owns the Imouraren mine with a giant resource size of 109Mt at 0.06% uranium.

In 2023 Orano started to develop a plan to reopen the mine but was interrupted by a coup in the Niger.

Now Orano is at risk of losing its operating permit and have the uranium project taken over by Russian entities:

(Source)

This is a big problem for France, as 20% of its uranium supply is out of Niger and Orano is a major French utilities company.

With Niger looking perilous it's no surprise that Orano is working on mine restarts in other countries - notably in Canada:

(Source)

We think the potential supply crunch looming out of Niger could present an opportunity for other, more stable countries in Africa (like Sengal), willing to work with France and the rest of Europe, to provide a reliable source of uranium.

As mentioned above, uranium is only actively produced in three countries in Africa, Namibia, South Africa and Niger.

We think that Senegal could be next on the radar of major countries as a more stable option for Europe.

How does Senegal fit into the picture?

When developing assets in Africa there is always a risk.

But the reward, like seen in Namibia with Paladin Energy, can be big.

As a mining jurisdiction Senegal is relatively stable. With a new mining code dictating the rules of the game since 2017.

The country has cemented a reputation of stability and political maturity since its independence from France in 1960 and operates under a democratic system.

Three months ago Senegal held elections which were complicated initially by some political manoeuvring and candidate eligibility matters.

In the end though it was a relatively smooth finish to the election that saw a new President, Bassirou Diomaye Faye, elected.

Currently we see the political situation in Senegal as a calm, business as usual environment for companies like HAR to operate in.

What’s next for HAR?

🔄 Lab results for Saraya Assays

HAR has published xRF results for its first 28 holes, and we hope that assays confirm (or even improve) upon what is already known.

🔲 Drilling across regional targets

This is the big one.

HAR still has plenty of target areas across its project that haven't been touched with an RC drill rig yet.

New discoveries across any of these could be game changers for the company.

We think this would have the biggest impact on HAR’s share price as it's a situation where expectations are low and the potential to surprise the market is high.

At last quarterly HAR had $1.1M in the bank, so we expect the company to raise money in the coming months to fund the next program of work.

What could go wrong?

Country Risk

HAR’s project is in Africa, and all investments in Africa carry some geopolitical risk.

While Senegal is generally one of the most stable countries in West Africa, the broader region where HAR’s project is located, is considered a high-risk region of the world.

Most recently in the region there was a coup in Niger (2023), and coups in Mali (2021) and Burkina Faso (2022) also occurred in recent years.

Political instability in the region could disrupt HAR’s ability to operate or commercialise its project, or significantly slow progress down.

Senegal recently had an election and the new president, Bassirou Diomaye Faye, has promised to alter the country’s approach to resources - potentially the re-negotiation of oil, gas and mineral contracts with foreign operators.

Reforms made to the regulatory environment for resources could adversely affect HAR.

Exploration risk

HAR is planning to drill exploration targets to grow its uranium resource.

Exploration activities may or may not return any uranium mineralisation or low-grade uranium resource that is uneconomic.

Commodity risk

In recent decades, governments have shunned uranium because of the issues related waste removal and accidents like Chernobyl and Fukushima.

If the adoption of nuclear power is slower than expected then it may impact the future demand for uranium.

Uranium price risk

Share prices of junior explorers like HAR are dependent on strong spot prices for the commodity they are exploring for.

The uranium price currently remains strong, but any retracements or a return to a bear market in spot prices could lead to capital withdrawing from the sector and a fall in share prices.

Funding/Dilution risk

Like most micro cap resource exploration companies, HAR has no revenues to fund exploration and its ongoing costs.

This means the company is reliant on capital raises to fund exploration programs that aim to build significant shareholder value.

HAR had $1.1M as of 31 March 2024, and HAR will need to raise capital to continue its operations at some stage in the future which may incur dilution to current shareholders.

Capital may be hard to come by or cannot be secured at favourable prices, and this can be dependent on broader capital market conditions.

Market risk

If the broader market sells off, investors may shy away from high-risk investment opportunities like junior explorers.

During market downturns, investors will look to pull capital away from the high risk investments. HAR is a junior explorer and may be impacted by these market wide sell offs.

Our HAR Investment Memo

In our HAR Investment Memo, you can find:

- HAR’s macro thematic

- Why we Invested in HAR

- Our HAR “Big Bet” - what we think the upside Investment case for HAR is

- The key objectives we want to see HAR achieve

- The key risks to our Investment thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.