GEN: Mining Convention signed. Project financing next

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 4,595,000 GEN shares and 2,250,000 GEN Options at the time of publishing this article. The Company has been engaged by GEN to share our commentary on the progress of our Investment in GEN over time.

It's finally signed.

The President himself oversaw the signing ceremony.

On Monday our green iron ore investment Genmin (ASX:GEN) confirmed it had signed an all important Mining Convention for its development stage, 100% owned green iron ore project in Gabon.

Here’s the President of Gabon, His Excellence Brice Clotaire Oligui Nguema, shaking the hand of GEN Director Mr Pietro Amico at the signing ceremony:

This long awaited sign off of the Mining Convention was the essential agreement required to formalise GEN’s status in Gabon, and help GEN go out to financiers to secure project development capital.

The Mining Convention specifies both GEN’s and the Government’s obligations regarding GEN’s project, including those pertaining to legal, social, environmental, and financial matters, including royalty, tax, and free-carry.

(which is all in line with parameters assumed in the Pre Feasibility Study)

GEN’s Mining Convention sign off is a large de-risking event for major would-be financiers of project development - of which there are at least 4 in the mix - keep reading to see who.

The Mining Convention means GEN has no other major permitting hurdles to get its project developed.

There are three main things that will cause any mining project to fall over at the development stage (before construction): financing, feasibility and permitting.

This week, GEN dramatically reduced one of those three big risks - permitting.

In other news, today GEN shored up its balance sheet with a $3M loan from major shareholder Tembo Capital (more on these guys later) - giving it some runway to execute on the next major goal:

Secure the financing for construction, which is circa US$200M.

This is to deliver a project with a post-tax NPV of US$391M (as per the 2022 PFS).

GEN still maintains a 100% ownership of the asset so does have some flexibility in how it tackles financing options.

We understand that in the mix to partner with GEN are:

- Chinese company (with which it already has an offtake MoU),

- Non-China steelmaker,

- European trading house, and

- Chinese construction company with a presence already in Gabon.

(Source - Foster’s Stockbroking Analyst Report)

With global pressure for major carbon emitting industries (like the steel industry) to reduce their CO2 output, we think there is strong demand for green iron ore projects like GEN’s.

Especially in China where air pollution is a major gripe with citizens and consequently the government.

(steel factories often have to shut down in the main steel manufacturing province of Hebei for long periods of time to let the air quality improve) (Source)

And GEN’s clean and green iron ore would be a neat solution here:

(Source)

While the broader iron ore market isn’t exactly setting the world alight right now, the fact GEN also has access to cheap, green hydropower should help set it apart from other projects.

And while our Investment in GEN hasn’t been a great success just yet given our Initial Entry Price was 10c (we did Invest again at 5c), and it traded at 4.2c pre-market open today, we think if the company is able to speed up on the financing front things could change quite quickly.

GEN is currently very thinly traded, but there are signs of life in the GEN share price.

Shares ticked up from a low of 2.6c in early March to where it is now at 4.2c pre-market open today, up 62% in the last 4 weeks - albeit on low volumes.

It doesn't take much for the share price to move up... or down.

We think the recent upward trend in the GEN share price is down to three primary factors (in chronological order):

- A new CEO taking the helm (ex Rio Tinto, spent time on Simandou, more on him later)

- The signing of the Mining Convention (earlier this week)

- And progress on the political front in Gabon (elections have moved forward to next month - more on that later)

Today we will provide a deep dive update on where GEN is at, and what we think could happen next.

Major holder Tembo Capital offers $3M loan addressing short term funding risk

As we noted above, this morning GEN got a short term funding boost, in the form of a $3M unsecured loan from its ~50% shareholder Tembo Capital.

Tembo Capital is a private equity mining specialist fund, and is highly experienced in getting successful exits in projects like GEN’s.

As an example, Tembo Capital were major investors in Spartan Resources at the 10c recapitalisation round back in April 2023... Spartan just a week ago got taken out at a $2BN valuation at almost $2 per share.

(... and it was the conversion of a loan from Tembo to Spartan that helped build that position, a similar loan to what they have just done with GEN)

So they have a history of being in the right names when they are unloved and at their low points...

Today’s Tembo loan deal means some of the short term cap raise pressure is taken away from GEN.

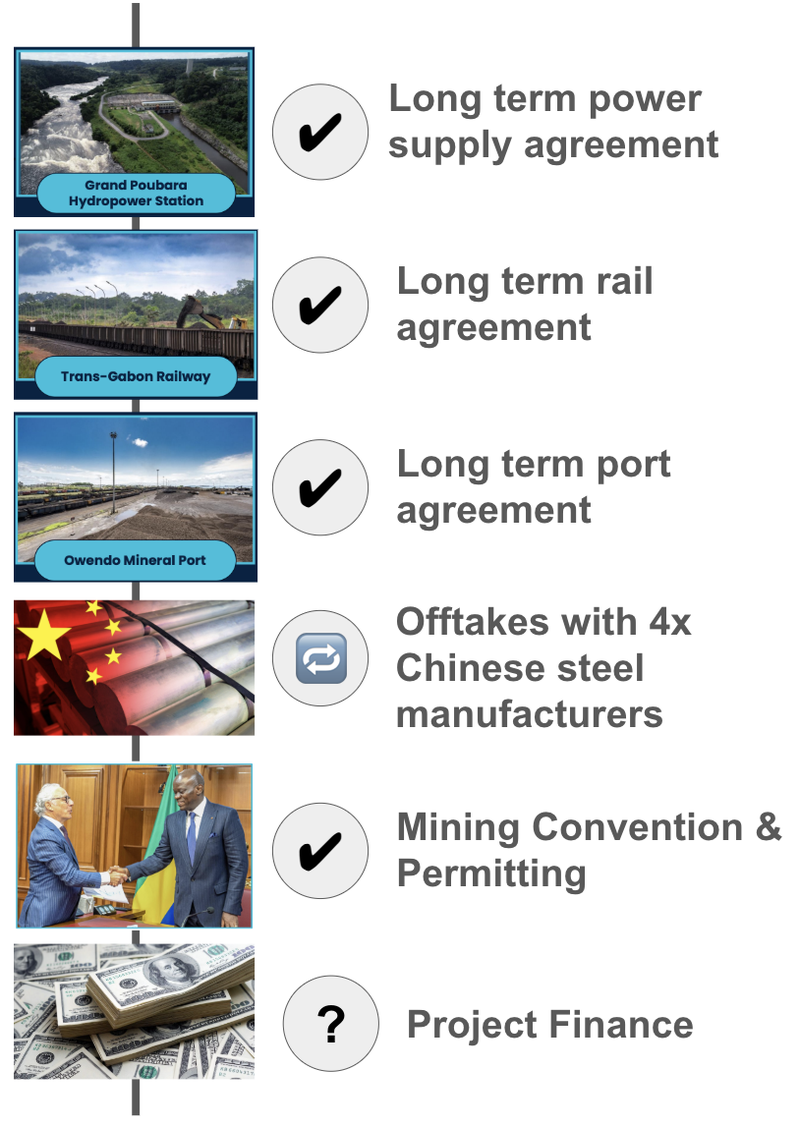

Financing, financing, financing: What the Mining Convention means for GEN...

Essentially the Tembo loan has bought GEN some time to deliver on its much bigger project financing goals.

And as we saw earlier, with that Mining Convention in hand, hopefully these negotiations will progress faster now.

Rail and port access has all been formally agreed along with green hydropower at low prices.

With a Mining Convention signed, GEN is in a much stronger position to talk with potential financiers of the project.

Here’s what GEN has already ticked off - there’s a few still missing but significant progress is being made:

For the last ~12 months GEN’s been warming up potential financiers.

Now it has an agreement signed with the Gabon government that outlines all of the regulatory parameters to govern GEN’s project.

Things like royalties, tax rates etc, which will now give financiers a complete picture of how a developed project would operate.

Project financing companies are often waiting on the sidelines to see an agreement struck between the mine and the government.

This is particularly true for mines in Africa, where project certainty is a key risk.

With this news this week, the final de-risking hurdle is complete for GEN and the company is now in the “final investment decision” stage.

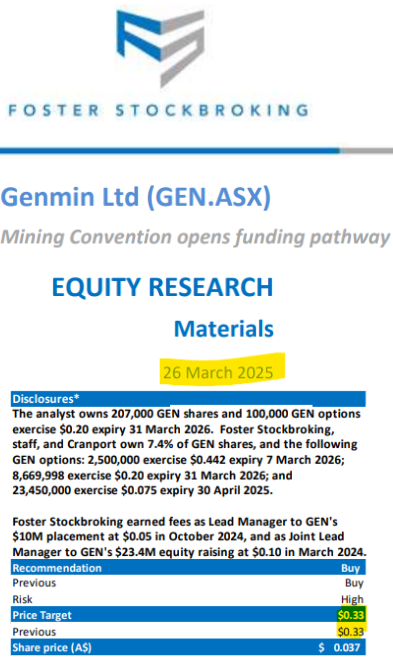

Yesterday, Foster Stockbroking analyst Mark Fichera published a report on GEN with a 33 cent price target (GEN is currently priced at 4.2c).

You can read the full report here: ASX:GEN Fosters Report, 26 March 2025

While that price target does look compelling given GEN’s current share price, we should be clear that analyst price targets are based on a number of assumptions that may be incorrect - they (or us) don't have a crystal ball.

It’s definitely possible GEN does not reach these share prices. This is a small cap mining stock. Never invest on a price target alone, and always do your own research.

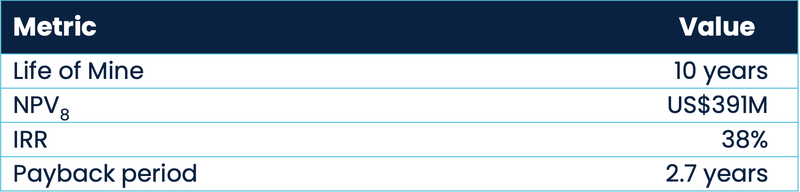

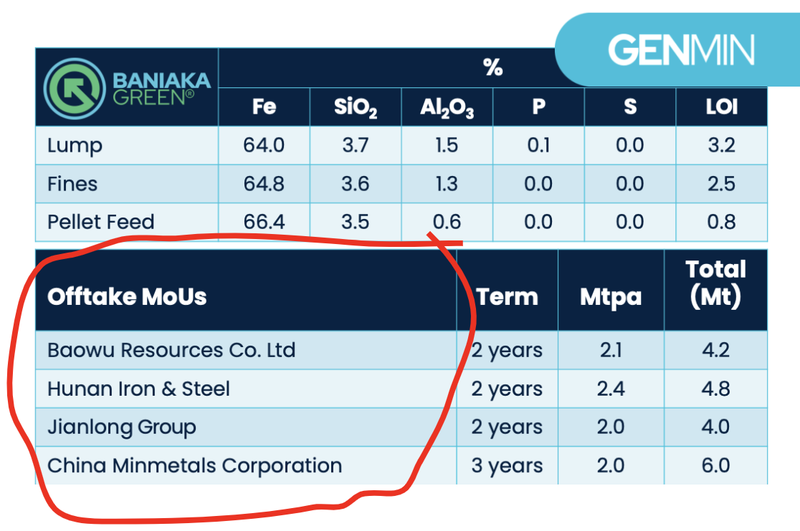

GEN’s iron ore project metrics

GEN owns 100% of a construction-ready iron ore project in Gabon.

The project has a 2022 Pre Feasibility Study (PFS) which outlines a Net Present Value (NPV) of US$391M from CAPEX of US$200.8M.

The US$391M NPV is for a 5Mtpa iron ore operation that would run for ~10 years.

GEN’s plan is to eventually scale the project up to ~20Mtpa.

(4x times the size of the project established in the 2022 PFS).

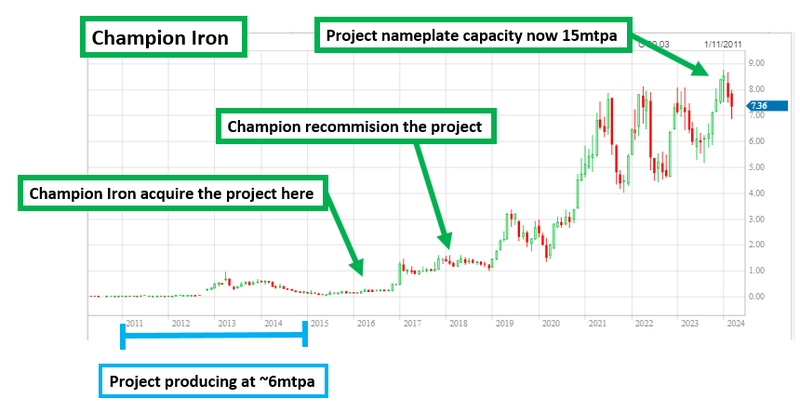

By the way, ASX listed Champion Iron did something very similar in recent years, scaling from a ~6Mtpa operation (in 2011-2014) to ~15-20Mtpa that it operates today.

During that time Champion’s peak share price return was over 3,800%.

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Before the scale up to 20 Mtpa, first we want to see GEN finance the initial 5Mtpa operation.

Who will fund GEN’s project?

So as we have noted above, with the Mining Convention in hand, financing talks should get moving a lot quicker.

Financing could be a mix of debt, equity or offtake prepayment.

The most obvious first point of contact is GEN’s existing relationships with Chinese steel giants.

GEN already has 4 offtake MoUs in place with Chinese companies, three of which are in the top 15 biggest steel makers in the world.

(Source)

These four MoU offtakes cover ~18Mt of iron ore over GEN’s first three years of production.

(We note they are for now, just ‘Memorandums of Understanding’ at this point - not binding)

We see the Mining Convention as a major catalyst for GEN, and its ability to secure financing from a range of different players, and start to move those ‘MoUs’ into more formal binding offtake agreements that are more bankable.

What can happen to a company’s share price after a Mining Convention gets signed?

A Mining Convention opens up a lot of doors for a company, as seen with another African mine developer in our Portfolio, Canyon Resources (ASX: CAY).

It took Canyon almost four years to secure a Mining Convention with the Cameroon government, and it was a key risk point for the company.

Like in Gabon with GEN, Canyon Investors such as ourselves had to wait patiently for CAY to sign a Mining Convention with the Cameroon government.

But once the ball started rolling, and in a strong macro environment, below is what happened to the CAY share price.

From July of last year onwards, CAY’s share price tacked up a rise of more than 300% in the next six months as CAY secured a cornerstone investor and knocked down development milestones in a red hot bauxite market.

Past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

But yes, this is iron ore... not bauxite

Now granted, the macro environment for iron ore is not so strong right now...

But the iron ore price does seem to have stabilized around the US$100 mark.

And we all know commodity markets move in cycles...

Iron ore makes steel, and steel is the lifeblood of developing economies.

Which means that its demand is directly linked to increased urbanisation in emerging economies, particularly in places like China and India.

Trump has imposed, threatened, retracted and then imposed again a 25% tariff on steel.

It is unclear exactly how long these tariffs will be in place and what the long term outlook for steel and iron ore will be.

But for GEN it is all about focusing on the things within its control... financing, feasibility and permitting.

And we hope that the demand from growing, urbanising economies in places like China, South East Asia and in particular India, will carry the steel and iron ore demand long into the future.

GEN’s new CEO takes the reigns to bring project through development

Spearheading GEN in this next stage of development is the new CEO Andrew Taplin who started last month.

Taplin has 30 years of experience, including 25 years at Rio Tinto inside its iron ore and copper divisions.

We see Taplin as well suited to this phase of GEN’s journey towards developing a green iron ore mine.

Experience in operations and logistics is important at this juncture.

Within Rio Tinto’s iron ore division, Andrew worked at the Pilbara operations, Iron Ore Company of Canada (Labrador City) and spent four years at Simandou as an expatriate residing in Guinea, Conakry.

(Yep, the very same ginormous Simandou mine that is owned by Rio Tinto and took up its very own expansive booth at the world’s largest mining convention, Mining Indaba in Cape Town).

Simandou is a mammoth iron ore project in Africa, so we expect Taplin to bring great experience to the role as GEN seeks to obtain financing for its green iron ore project in Gabon.

We like that Taplin's background includes significant West African experience and French language skills.

Gabon is a French speaking country - it’s a big plus to be able to speak the language.

With GEN at a pivotal stage of the development cycle, project funding will be key.

If GEN is able to secure the funding for its mine, we think that it will then take ~12-months for the company to get to first production.

Our GEN Big Bet

“GEN re-rates 1,000% by scaling up its production over time from its iron ore project in Gabon”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our GEN Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true

Gabon politics update

GEN signing the Mining Convention signals the company’s connection with the state of Gabon and the wider community.

If there are any changes to the state of political affairs in Gabon, we expect this Mining convention to remain in place.

(although there is always a risk that this doesn’t happen).

A little background into the current state of play in Gabonese politics...

In 2023 there was a peaceful military coup that ended the Bongo family's 56-year rule - leading Gabon down a path towards democratic rule.

An important step in this transition was the constitutional referendum held on November 16, 2024, wherein a total of 91.64% of voters approved a new constitution. (Source)

This constitution introduces significant reforms, including the establishment of a seven-year presidential term, renewable once. (Source)

Gabon's “transitional government” has scheduled presidential elections for April 12, 2025, and the current transitional leader, President Brice Oligui Nguema will be running. (Source)

(This is the President and party that GEN signed the Mining Convention with)

The election has recently been moved forward by roughly four months, which we think is a sign that Gabonese people are eager to ratify its new democratic position.

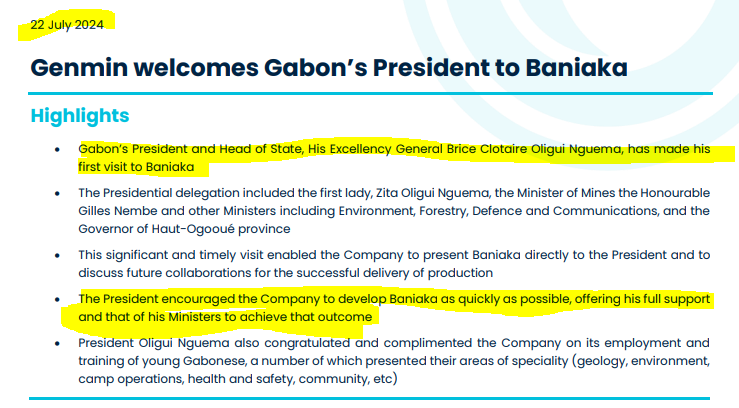

Nguema has already visited GEN’s site and declared the project as vital to the national interest:

Read our full take on the visit here: President visits GEN’s green iron project - offers support and encourages rapid mine development.

Should the upcoming elections in Gabon next month go well, we think this could help make financiers feel more comfortable with providing funds for GEN’s project.

Gabon however is a west African state, and risks could materialise however (see risks section).

What’s next for GEN?

Project financing update (US$200M CAPEX financing)

We want to see GEN show a pathway to getting its project financed and into construction.

Milestones

🔲 Confirm funding strategy

🔲 Secure debt financing

🔲 Secure equity financing

🔲 Secure binding offtake agreements

🔲 Secure prepayments for offtake or other strategic capital partners.

Convert offtake MoU’s into binding agreements

In the near term we are looking for GEN to make progress across its offtake MoUs.

With 4 non-binding MoUs for offtake already secured, we think GEN will be looking to make these offtakes binding and in doing so, firm up the financing picture.

We expect there would be some competitive tension around GEN’s premium product - and things could move quickly once any of these 4 MoUs are converted into a binding agreement.

Milestones

🔄 Binding offtake #1

🔄 Binding offtake #2

What are the risks?

When we first Invested in the company we had hoped that it would be financed and in construction by now.

In the company’s FY2023/24 annual report it stated that they had the goal of “project financing closing on or around mid-2024 to enable the build to commence” (Source).

But, for GEN “delay risk” has materialised, and the company will look towards later this year to secure project financing.

Unfortunately the delays have also meant GEN’s share price has come off a fair bit from our Initial Entry Price.

With a new CEO at the helm, and the mining convention in hand, we are hoping that GEN can renew its focus on project financing.

To illustrate how delays affect GEN’s value we can look towards GEN’s capital expenditure over the last few years.

GEN is at the point in its development lifecycle where it has a large working capital overheads which includes the cost to manage a large in-country team.

Last quarter it spent slightly less than $3M in operating expenses, primarily to maintain a large in-country team.

This is important for projects at the development stage as it forms part of the negotiation process with securing the mining convention, building relationships with the communities and maintaining talent.

The challenge is that if the company has construction delays the cash balance clock tends to run out quickly.

In order to buy more time, the company typically needs to raise capital on market, diluting existing shareholders at a lower price.

This was the case with GEN who raised $10M at 5c in October 2024.

In addition today GEN topped up the bank account via a $3M loan from major shareholder Tembo Capital.

More delays, without a reduction in overheads, will see GEN run out of this cash again quickly, which means that the company has a narrow window in which to secure all of the milestones to get the project into construction.

Financing and delay risk

The development of Baniaka will require ~US$270M in debt and equity funding (a number that estimates on CAPEX working capital and corporate expenses), to be raised in financial markets.

Financial markets are inherently uncertain and readily influenced by global macro-economic events at the time.

GEN may experience delays in procuring the funding and consequently development of Baniaka through exposure to the sentiment in financial markets, which may adversely affect GEN’s value and share price.

Source: What could go wrong? GEN Investment Memo 2nd April 2024

The other important risk to highlight from today’s announcement is the jurisdiction/political risk.

Gabon, while significantly wealthier than many West African countries on a per capita basis, has jurisdictional and political risks that are associated with the region.

Notably, GEN’s Mining Convention was signed with a transitional government that is yet to be elected.

While we see the Mining Convention as mitigating jurisdiction and political risk at this stage, if the leader of the transitional government is not elected then there is a chance that a new government may have different views about the importance of GEN’s project.

Alternatively, elections could go poorly and the country become politically destabilised, impacting the attractiveness of GEN’s project to financiers.

It’s important to note that GEN negotiated the Mining Convention with the current Gabon mining code (laws) in mind.

This should mitigate some of the risks in the case of a change in government, but it could still materialise.

Elections will now be held next month, which we will be paying close attention to. \

Jurisdiction risk/political risk

In August 2023, a military coup affecting regime change occurred in Gabon.

A transitional, appointed rather than elected, government has been put in place with elections scheduled to be conducted in August 2025.

While the population of Gabon has generally supported the coup - there are uncertainties about the future political climate of Gabon.

For example, delays in holding elections and returning to an elected civilian government may lead to economic, political, and social risks materialising that adversely impact GEN’s ability to develop Baniaka and subsequently produce, export and sell iron ore products.

Source: What could go wrong? GEN Investment Memo 2nd April 2024

Our GEN Investment Memo

In our GEN Investment Memo, you can find:

- GEN’s macro thematic

- Why we Invested in GEN

- Our GEN “Big Bet” - what we think the upside Investment case for GEN is

- The key objectives we want to see GEN achieve

- The key risks to our Investment thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.