New Investment ASX:GEN: Green iron ore for green steel - first production in 18 months

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 3,750,000 GEN shares and 1,250,000 GEN options at the time of publishing this article. The Company has been engaged by GEN to share our commentary on the progress of our Investment in GEN over time.

Today we are announcing our first new Portfolio addition for 2024.

This company is a development stage stock set to get into production in the next 18 months.

We think its green product is going to be in demand and preferred in China.

Here’s why:

China’s cities are filled with smog and pollution.

Steel making is a major offender in causing air pollution and carbon emissions.

15% of China’s total greenhouse gas emissions came from its steel mills.

In order to combat this, the Chinese government has mandated the steel industry to significantly reduce its emissions.

China is aiming to achieve “peak carbon” emission by 2030 and become “carbon neutral” by 2060.

Globally, to go electric and switch to clean energy, 3.5 billion tonnes of steel will be needed over 15 years to build energy grids, wind farms, solar farms, nuclear plants and electric vehicles.

It defeats the purpose if the traditional steel making process releases loads of carbon.

One way to make green steel is by switching coking coal and blast furnaces with clean energy like hydrogen - a new technology

Bill Gates and Amazon are both backing ventures creating technologies to process iron ore into green steel - steel made with lower or zero carbon emissions.

BHP, RIO, FMG, Vale are all making investments in green steel too.

However, the quickest, cheapest way to make greener steel is using greener iron ore.

...and that’s where our Investment comes in.

Green iron ore requires less energy to be processed into steel.

Green iron ore needs to be:

- High grade or processed to higher grades using renewable energy

AND

- Have low impurities (less energy required to process it)

The bulk of iron ore used in China is purchased from BHP, RIO and Vale - it is lower grade and NOT considered “green”.

Our new Investment plans to produce and sell GREEN iron ore within 18 months via a starter mine, and it's got a clear pathway to grow its production over time.

Introducing our latest Investment:

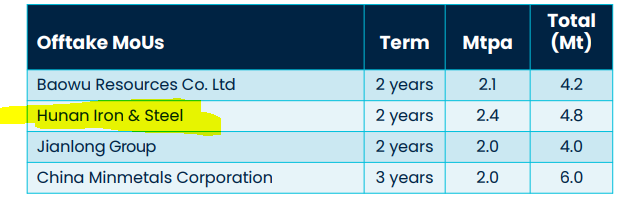

GEN already has FOUR Chinese offtakers signed on via MoU’s...

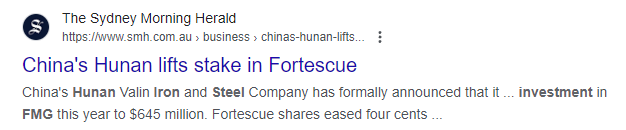

One of these Chinese offtakers (Hunan) is the second largest shareholder of one of Australia’s biggest iron ore miners, the $79BN Fortescue Metals Group.

Some of our biggest wins in the past have been in the decarbonisation, net zero and green investment thematics.

And today we are adding green iron ore to our portfolio - for making green steel.

Today we will be launching our GEN Investment Memo where we share:

- What GEN does

- The macro theme

- Our GEN Big Bet

- What we want to see GEN achieve

- Why we are Invested in GEN

- The key risks to our Investment Thesis

- Our Investment Plan

GEN has just re-listed on the ASX after having completed a recapitalization process at 10c per share, is now debt free, and is emerging with circa $12.6M in cash (pro forma assuming the $28.3M is raised in full).

All permits and mining licences are now in place, rail and port deals are signed, and an “emissions free” energy source has been secured from a nearby hydro-electric dam.

GEN is about to take its next step to finance and build its project over the next 18 months, and become a green iron ore producer...

GEN owns 100% of a construction-ready green iron ore project in Gabon.

GEN already has a mining permit, environmental permitting and access to export infrastructure.

AND a clean energy supply via hydro-electricity deal to cleanly process its ore to green grade.

The next phase of work is to secure project financing, move into the construction phase, and enter production within the next 18 months.

Here are the 13 key reasons why we Invested in GEN:

- Green steel - Steel production accounts for ~6-9% of global carbon emissions and as an industry, is one of the single biggest polluters in the world. “Green steel” is the industry's response to decarbonisation which means demand for green iron ore, like GEN’s, will increase in the future.

- Mine built and producing in next 12-18 months - GEN is aiming to have its project in production and generating cashflows within 18 months.

- Ready to build - all permits in place - In January 2024, GEN received a 20 year, large scale mining permit in Gabon, which provides certainty of tenure at the project. From our experience Investing in Africa, this is a big step forward for any company to take.

- Access to existing infrastructure - GEN has already negotiated 1) a 20 year agreement for green hydroelectric power, and 2) an integrated port and rail logistics solution that will take GEN’s products along the Trans-Gabon Railway to Port Owendo on the west coast of Gabon.

- China push to use green steel - The Chinese government is proposing to become carbon neutral by 2060. To do that the government is looking to decarbonise the industries that are generating the most pollution. Currently steel production accounts for ~15% of all carbon emissions in China - driving the government's desire to push for the growth of a green steel industry.

- GEN already has 4 x Chinese offtakers - GEN has four offtake MoUs for future production in place, three of which are in the top 15 biggest steelmakers in the world. These four non-binding offtake MoUs cover ~18mt over GEN’s first three years of production — effectively all of its production during that period.

- Offtake with Hunan, the early backers of FMG - Hunan Valin Steel was one of the early backers of FMG back in 2009 with a >$500M direct investment into FMG. Hunan’s stake in FMG is worth about ~$6.7BN. Hunan currently has an offtake MOU in place with GEN.

- $76BN FMG just produced iron ore in Gabon - Back in December 2023, FMG shipped its first batch of iron ore from a pilot operation at its first overseas mine in Gabon.

- Tembo Capital owns 50% of GEN - Private equity mining specialist fund Tembo Capital is GEN’s biggest shareholder. Tembo was the same group that led the recapitalization of Paladin Energy out of administration before relisting the company. Paladin now trades at a market cap of ~$4.1BN. Tembo’s Managing Director John Hodder (and also GEN board member) invested $1.65M in GEN’s placement at 10c per share

- GEN just went through its own recapitalisation - GEN just raised $13.2M via a placement at 10c per share and ~$10.5M from an entitlement offer. Tembo Capital took up ~$8.3M in that entitlement offer through cash and loan conversions.

- US$391M NPV with just US$200M in CAPEX - GEN has a pre feasibility study completed showing a Net Present Value of US$391M, Internal Rate of Return of 38% and payback period of just 2.7 years. To get the project into production, GEN needs US$200M in CAPEX.

- Potential to 4x iron ore production to 20mtpa - GEN’s development strategy is to get the mine into production through a 5mtpa starter mine. GEN also has the capacity to increase the mine capacity to ~20mtpa.

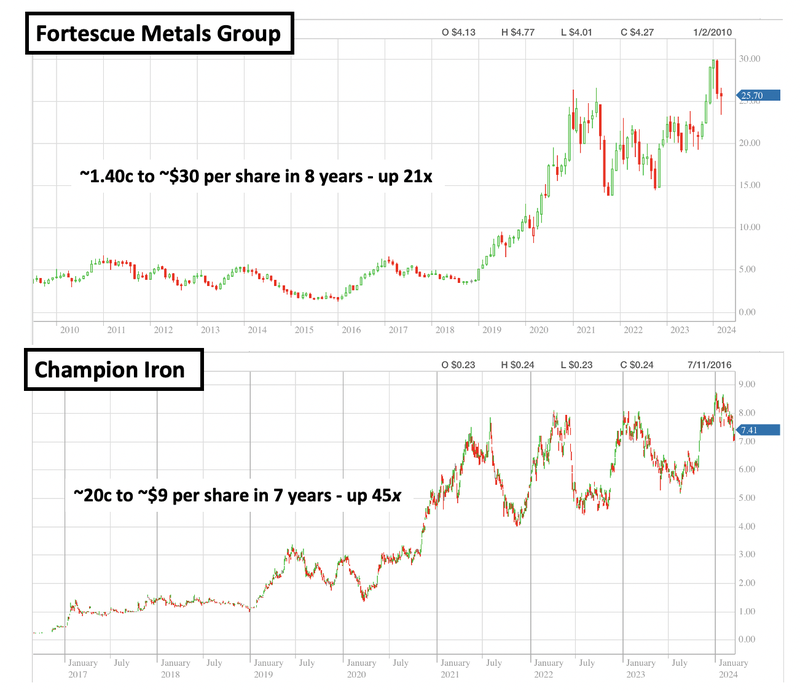

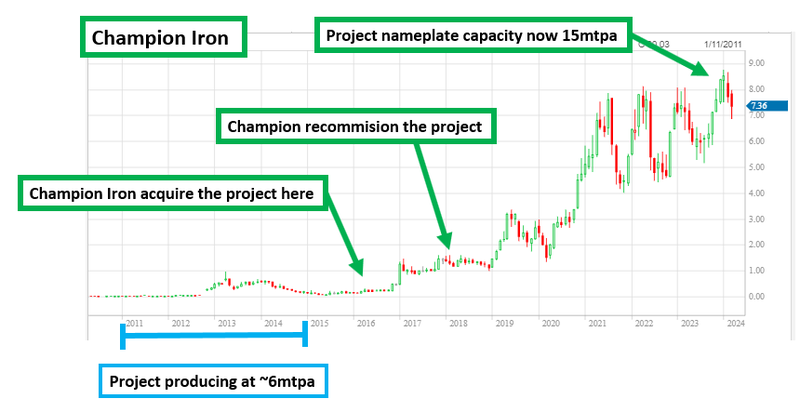

- Similar initial start up to $3.7BN Champion Iron - Champion Iron’s project was initially producing at ~6mtpa between 2011-2014 before being ramped up to a ~15mtpa operation. By the end of the scale up Champion’s share price went up by ~3,800%. GEN’s plan is to start at 5mtpa and ramp up to 20mtpa over time.

A big part of our GEN Investment thesis is based on GEN’s exposure to the green steel macro thematic.

The world is pushing hard to transition toward green steel - and it has big implications for Aussie favourites like Fortescue, Rio and BHP.

We think that should play into GEN’s hands as this transition takes place.

Green steel has been making news over the last month:

So what is green steel anyway? And why the rush?

(Source)

Put very simply, green steel swaps out the energy intensive blast furnaces with energy efficient processing tech, low grade iron ore with higher grade ores that require less processing AND then replaces fossil fuels with renewable energy.

BHP, RIO, FMG and Bill Gates are all investing in green steel tech...

Here’s how GEN plans to feed the global push into green steel

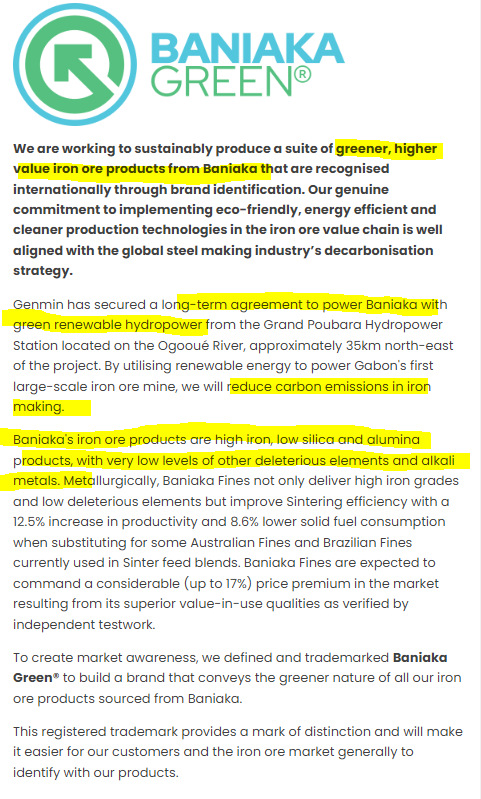

GEN’s future product, “green” iron ore they have branded as “Baniaka Green”, is higher grade meaning less coal and energy is needed in the blast furnaces to turn it into steel.

(it will be processed to a higher grade before sale using clean hydro-electricity from a nearby hydro dam)

The higher purity significantly reduces emissions and pollution from steel production.

Baniaka Green iron ore also contains less of the typical impurities found in most iron ore, which means it requires less energy to refine.

Which in turn means China’s steel manufacturers are less likely to be subject to environmental protocols, where they have to shut down until the air quality improves.

Here’s a quick summary of GEN’s high grade green iron ore, which GEN has named and trademarked as “Baniaka Green”:

(Source)

We think GEN’s product will be different and better.

Because it has less “hard to refine” elements it will take less energy to process into steel - and also save steelmakers money - which as a result should attract a premium price.

The benefits of GEN’s product compound when taking into account that it will be processed to a higher grade before sale using readily available renewable energy.

GEN has a long term power supply deal for renewable energy from the nearby hydro-electric dam.

We think the appetite for GEN’s green iron is already clear - GEN has 4 different offtake MOUs from some of China’s biggest steel manufacturers.

This is strong evidence that its product is already sought after in the Chinese market.

We are Invested in GEN as we have seen the potential upside in iron ore stocks before:

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

GEN has just re-listed on the ASX after a long suspension - it has so far raised ~$23.2M at 10c (cash and loan conversions), which is the level we just Invested at.

GEN is now debt free, and if it can place all of the remaining entitlement offer shortfall, it can bring in another $4.9M, then it would have ~$12.6M in cash in the bank.

After clearing its debts, and topping up its cash balance, GEN has runway and momentum to achieve its goal of production in the next 18 months.

The main hurdle with getting mines built and into production is securing the capital costs to build the mine - what's commonly termed the CAPEX (short for capital expenditure).

GEN’s CAPEX is US$200M, which is expected to deliver a NPV of US$391M on its 5 Mtpa starter mine.

(There’s a pathway to expand this production capacity by 4x to 20mpta over time - more on that below.)

We expect funding to come from a mixture of debt and equity - and securing this funding will be a major part of the GEN story over the coming 12 months.

To help with financing and prove its project is backable, GEN has already attracted offtake MOUs from 4x major Chinese steel producers.

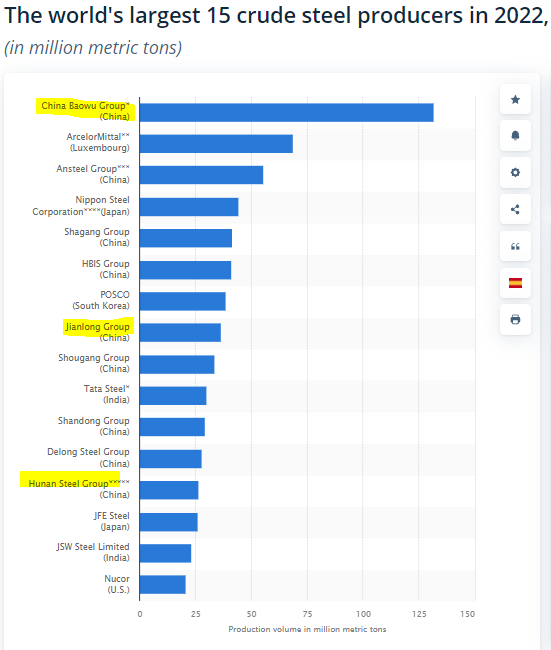

Three of these offtakers sit in the top 15 steel producers globally:

One of those potential offtakers is Hunan Iron & Steel - the same Chinese steel maker that backed ASX iron ore success story Fortescue Metals Group back in 2009.

At the time, Hunan invested >$500M into FMG, becoming FMG’s second-largest shareholder.

(Source)

Over the next 15 years, that investment turned into a multi-billion dollar position for Hunan.

(It is also worth noting that FMG recently shipped its first “non Australian” batch of iron ore from a pilot project in Gabon - the same country GEN’s project is in)

For now, Hunan’s involvement in GEN is just an MoU for an offtake.

But we would like to think given Hunan has already had success backing iron ore producers like FMG and it might not be afraid to back GEN in a capacity beyond an offtake.

We will have to wait and see though - ultimately over the near / mid term we want to see GEN convert its current offtake MoUs into binding contracts.

GEN is also heavily backed by private equity mining specialist fund Tembo Capital which has a history of picking up advanced assets in recapitlisation rounds and taking them to the next level.

Tembo owns ~50% of GEN, and has a board seat taken up by Tembo’s Managing Director John Hodder who himself took $1.65M in GEN’s placement at 10c per share.

That kind of significant skin in the game is quite rare - and an indication of where Hodder and Tembo see GEN going in the future.

Tembo has a history of coming in at recapitalisation rounds with a lot of success...

Tembo was also behind the restructuring of Paladin Energy, whose market cap was ~$80M while the company was in administration.

Now Paladin still trades on the ASX and has a market cap of ~$4BN - all in under 6 years.

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Tembo clearly knows a good opportunity when it sees one, and are specialists in investing in development stage companies - and importantly holding them through to a successful exit.

We are hoping the money invested and high ownership of GEN will mean it's a priority for Tembo to deliver a successful investment outcome here.

Of course, that successful outcome requires that the mine gets funded and into production.

Once financed, GEN’s plan is to develop a starter mine operating at ~5mtpa.

(this is where the company forecasts to see production and revenue within 18 months)

GEN’s 5mtpa operation has an NPV of US$391M - GEN’s market cap today is $68.5M at 10c per share.

The plan is to scale up the project by 4X to ~20mtpa eventually.

It's a similar approach to the one implemented by Champion Iron at its Canadian iron ore project.

Now, Gabon is not Canada, and we think that partly explains why GEN could be trading at such a steep discount to other advanced stage iron ore companies.

Gabon remains as one of the wealthiest countries in Africa.

However, Gabon recently went through a peaceful coup - and a transitional government is currently in place with an election scheduled for 2025.

So while there are jurisdictional risks (see Investment Memo Risks section below), and elections in 2025 will be an important event for both GEN and Gabon - we’ve been Investing in Africa for many years and have had some great successes there.

We want to see GEN follow a similar path - and Champion Iron provides the model for what GEN could accomplish.

And it all comes down to scale up.

Champion’s project between 2011 & 2014 was producing at ~6mtpa.

Over the next decade Champion took the asset and scaled up its production capacity.

Now Champion produces at ~15mtpa and has seen its share price re-rate by >3,800%.

We are Invested in GEN and we hope the company can achieve similar success over the next 3-5+ years.

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

We’ve also spent some time reading a recent MST research report on GEN which outlines the potential upside to GEN’s valuation. It was a good in depth summary of GEN and it produced the following price target:

(Source)

While that price target of 51c does look interesting, we should be clear that analyst price targets are based on a number of assumptions that may be incorrect. Analysts (including us) don't have a crystal ball and no one can accurately predict future share prices. It’s definitely possible GEN does not reach this share price. Never invest on a price target alone, and always do your own research.

MST research have been covering GEN for a couple of years, you can see some of their previous analyst reports here:

- MST Access - 11 January 2024 GEN Research Report

- MST Access - 13 November 2023 GEN Research Report

- MST Access - 10 August 2023 GEN Research Report

- MST Access - 13 March 2023 GEN Research Report

- MST Access - 30 November 2022 GEN Research Report

- MST Access - 20 June 2022 GEN Research Report

- MST Access - GEN Initiation Report

As new entrants into GEN, we are hoping that this recent recapitalisation raise is the right one to enter the stock, and look forward to watching GEN progress to production over the next 18 months.

So that we can follow the company’s progress over time and track our Investment, today we will be launching our GEN Investment Memo where we share:

- What GEN does

- The macro theme

- Our GEN Big Bet

- What we want to see GEN achieve

- Why we are Invested in GEN

- The key risks to our Investment Thesis

- Our Investment Plan

GEN Investment Memo

What does GEN do?

Genmin (ASX:GEN) is a green iron ore developer aiming to put its Gabon iron ore project into production.

What is the macro theme?

As a key ingredient for steel, iron ore demand has been persistently strong over the past several years with pricing well above US$80/tonne.

In the long run, we expect demand for high grade, green iron ore will grow as major importers (especially China) and customers seek to utilise cleaner raw materials for the steelmaking process that reduce emissions.

Our GEN Big Bet:

“GEN re-rates 1,000% by scaling up its production over time from its iron ore project in Gabon”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our GEN Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true

13 Key reasons why we Invested in GEN:

- Green steel - Steel production accounts for ~6-9% of global carbon emissions and as an industry, is one of the single biggest polluters in the world. “Green steel” is the industry's response to decarbonisation which means demand for green iron ore, like GEN’s, will increase in the future.

- Mine built and producing in next 12-18 months - GEN is aiming to have its project in production and generating cashflows within 18 months.

- Ready to build - all permits in place - In January 2024, GEN received a 20 year, large scale mining permit in Gabon, which provides certainty of tenure at the project. From our experience Investing in Africa, this is a big step forward for any company to take.

- Access to existing infrastructure - GEN has already negotiated 1) a 20 year agreement for green hydroelectric power, and 2) an integrated port and rail logistics solution that will take GEN’s products along the Trans-Gabon Railway to Port Owendo on the west coast of Gabon.

- China push to use green steel - The Chinese government is proposing to become carbon neutral by 2060. To do that the government is looking to decarbonise the industries that are generating the most pollution. Currently steel production accounts for ~15% of all carbon emissions in China - driving the government's desire to push for the growth of a green steel industry.

- GEN already has 4 x Chinese offtakers - GEN has four offtake MoUs for future production in place, three of which are in the top 15 biggest steelmakers in the world. These four non-binding offtake MoUs cover ~18mt over GEN’s first three years of production — effectively all of its production during that period.

- Offtake with Hunan, the early backers of FMG - Hunan Valin Steel was one of the early backers of FMG back in 2009 with a >$500M direct investment into FMG. Hunan’s stake in FMG is worth about ~$6.7BN. Hunan currently has an offtake MOU in place with GEN.

- $76BN FMG just produced iron ore in Gabon - Back in December 2023, FMG shipped its first batch of iron ore from a pilot operation at its first overseas mine in Gabon.

- Tembo Capital owns 50% of GEN - Private equity mining specialist fund Tembo Capital is GEN’s biggest shareholder. Tembo was the same group that led the recapitalization of Paladin Energy out of administration before relisting the company. Paladin now trades at a market cap of ~$4.1BN. Tembo’s Managing Director John Hodder (and also GEN board member) invested $1.65M in GEN’s placement at 10c per share

- GEN just went through its own recapitalisation - GEN just raised $13.2M via a placement at 10c per share and ~$10.5M from an entitlement offer. Tembo Capital took up ~$8.3M in that entitlement offer through cash and loan conversions.

- US$391M NPV with just US$200M in CAPEX - GEN has a pre feasibility study completed showing a Net Present Value of US$391M, Internal Rate of Return of 38% and payback period of just 2.7 years. To get the project into production, GEN needs US$200M in CAPEX.

- Potential to 4x iron ore production to 20mtpa - GEN’s development strategy is to get the mine into production through a 5mtpa starter mine. GEN also has the capacity to increase the mine capacity to ~20mtpa.

- Similar initial start up to $3.7BN Champion Iron - Champion Iron’s project was initially producing at ~6mtpa between 2011-2014 before being ramped up to a ~15mtpa operation. By the end of the scale up Champion’s share price went up by ~3,800%. GEN’s plan is to start at 5mtpa and ramp up to 20mtpa over time.

What do we expect GEN to deliver?

Objective #1: Final Investment Decision (FID) made on GEN’s project

Milestones

🔲 Reach a successful FID

🔲 Advance toward project financing

Objective #2: Convert Offtake MoUs to Binding Contracts

Milestones

🔲 Binding offtake #1

🔲 Binding offtake #2

Objective #3: Secure US$200M in CAPEX financing

Milestones

🔲 Confirm funding strategy

🔲 Secure debt financing

🔲 Secure equity financing

🔲 Secure binding offtake agreements

🔲 Secure prepayments for offtake or other strategic capital partners.

Objective #4: Construct mine

Milestones

🔲 Construction contracts awarded

🔲 Construction begins

🔲 Construction completed

Objective #5: Ship first iron ore product and become an iron ore producer

Milestones

🔲 This one is fairly simple - we want to see GEN produce and ship its first batch of iron ore.

What could go wrong?

Financing and delay risk

The development of Baniaka will require ~US$200M in debt and equity funding to be raised in financial markets.

Financial markets are inherently uncertain and readily influenced by global macro-economic events at the time.

GEN may experience delays in procuring the funding and consequently development of Baniaka through exposure to the sentiment in financial markets, which may adversely affect GEN’s value and share price.

Jurisdiction risk/political risk

In August 2023, a military coup affecting regime change occurred in Gabon.

A transitional, appointed rather than elected, government has been put in place with elections scheduled to be conducted in August 2025.

While the population of Gabon has generally supported the coup - there are uncertainties about the future political climate of Gabon.

For example, delays in holding elections and returning to an elected civilian government may lead to economic, political, and social risks materialising that adversely impact GEN’s ability to develop Baniaka and subsequently produce, export and sell iron ore products.

Infrastructure access risk

The success of Baniaka (GEN’s primary project) will require initial and ongoing access to, and available capacity on, the Trans-Gabon Railway and at the Owendo Mineral Port.

GEN has signed a long-term, conditional 15-year bulk logistics agreement with Owendo Mineral Port for the provision of rail and port services utilising existing and operating rail and port infrastructure.

There is no guarantee that GEN and Owendo Mineral Port will be able to fulfil the conditions precedent to this agreement in a timely manner, and therefore there is no guarantee that this agreement will come into effect, potentially having an adverse impact on the value of GEN and its share price

Commodity price risk

The iron ore price could fall and no matter what GEN has achieved in terms of its project fundamentally, there is a risk the company’s share price performs poorly because of a poor performing underlying commodity price.

Market risk

Broader market sentiment can get worse and equity markets as a whole trade lower, taking GEN’s share price with it. Alternatively, there could be further sector specific pain ahead where iron ore developers explorers suffer more than the broader market.

Investment Plan

We are Invested in GEN to see it bring its project into production.

Our plan is to hold the majority of our position in GEN for 3 to 5 years which we hope is enough time to see GEN get to first production and start ramping up its production rate (see “our long term bet” above).

After 12 months we will apply our standard de-risking strategy.

We may look to sell up to 20% of our holding if the company delivers on one or more of our Investment Memo objectives and/or the share price materially re-rates.

Any sell downs will be in accordance with our trading and hold policy disclosure.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.