EXR’s bigger neighbour Omega set to flow test any day now

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 5,136,850 EXR Shares and 2,567,021 EXR Options and the Company’s staff own 40,000 EXR Shares and 13,333 EXR Options at the time of publishing this article. The Company has been engaged by EXR to share our commentary on the progress of our Investment in EXR over time.

A flow test is set to begin any day now...

A positive result could light up this whole gas region for takeovers - which is already full of big names like Santos and Shell.

We just increased our position in Elixir Energy (ASX:EXR) ahead of its regional peer Omega Oil & Gas’ imminent flow test.

Any good news from that flow test will be good news for EXR and the Taroom Trough as a whole.

Omega’s share price has tripled in the lead up to this flow test.

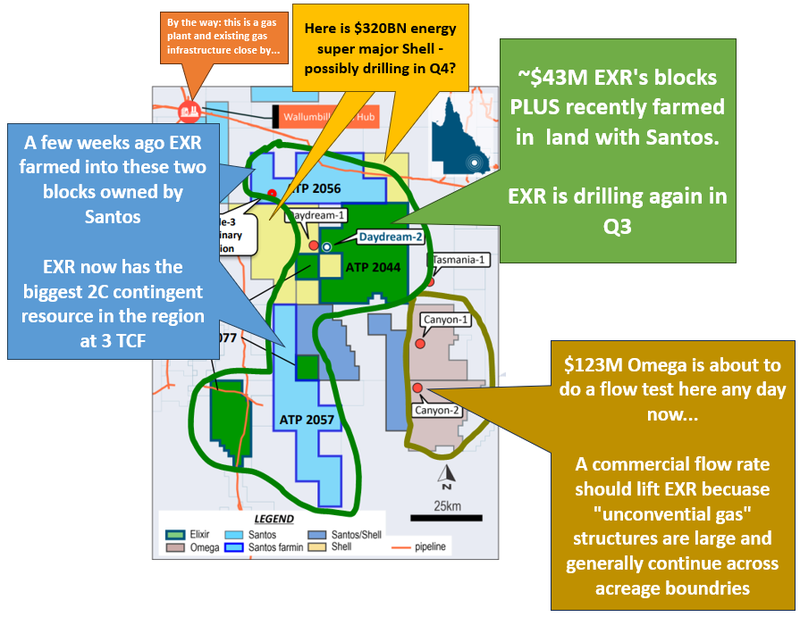

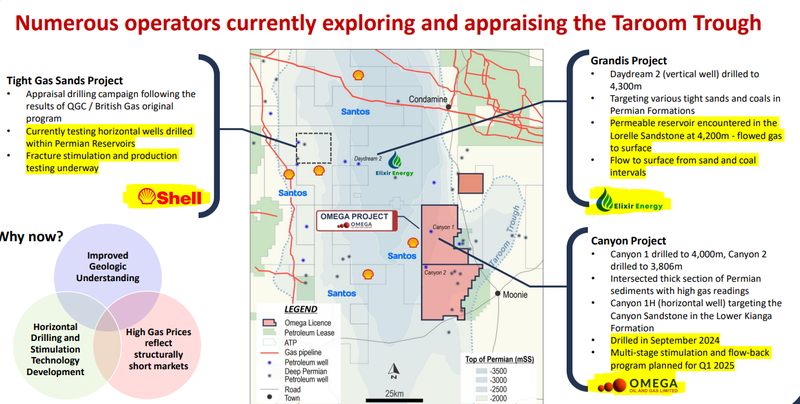

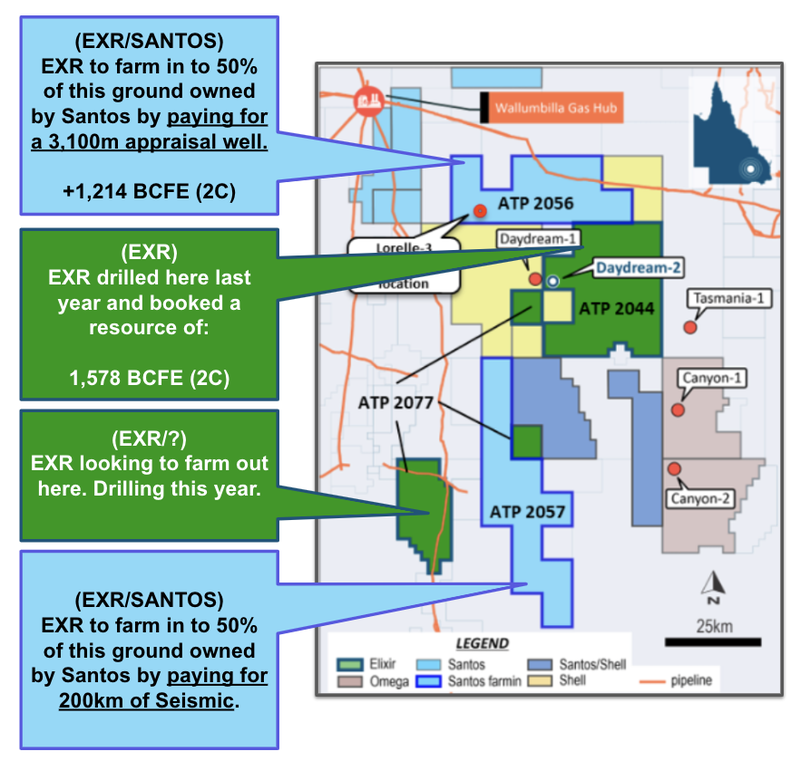

Below is the map of who is who in the Taroom Trough in Queensland, Australia - heavyweights like Shell and Santos are jostling for position beside small caps like Omega and our very own Investment EXR.

There’s a lot of activity happening in 2025, and we think after a couple of years operating here, there’s a lot of opportunity for EXR to leverage its large acreage position.

It is important to note that this region is highly prospective for “unconventional” gas - which is different to “conventional” gas.

Conventional gas collects up in isolated “pockets” under a trap and seal.

Unconventional gas is widely spread out and trapped through a sprawling underground structure.

If a neighbor has success and you are sitting on the same unconventional gas structure, it's highly likely you will have the same gas.

Hence why as EXR shareholders, we are watching Omega’s flow test very closely.

The Taroom Trough is fast becoming a globally significant gas region.

(the Australian east coast gas crisis is never far away from the news - development of the gas resources in the Taroom Trough could be one solution here)

EXR has a smaller market cap than Omega but a bigger contingent resource booking.

(Omega has been running up in anticipation of their flow test that is starting any day now)

EXR is currently capped at $43M, meanwhile Omega is three times bigger at $123M.

Omega has a 2C contingent resource ~1.7 TCF, however EXR has a 2C contingent resource of almost double that, coming in at ~3TCF.

Omega has that big flow test due to start any day now - and EXR has a well planned for Q3.

In the short term we will have all eyes on the Omega result - what is good for Omega will be good for EXR...

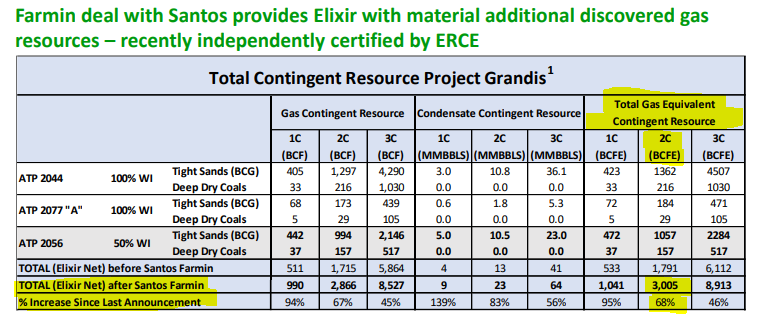

Before we go too far, it's worth explaining how EXR came to grow its resource size so much recently.

A few weeks ago EXR signed a deal with the $22BN gas major Santos, adding to its ground position.

The deal sees EXR become one of the biggest landholders in the Taroom Trough from an acreage perspective.

Again, this farm-in deal means EXR now has a net 2C ~3 trillion cubic feet (TCF) of gas contingent resource to its name.

Which importantly, puts it ahead of neighbour Omega Oil and Gas who is capped at $123M and is about to flow test its first horizontal well in the region.

By the way, Omega is backed by Tri-Star Group who are pioneers of the Queensland gas industry.

They drilled Queensland’s first commercial coal seam gas well in the 1990s and laid the foundations for the $80BN Liquefied Natural Gas industry in the state.

Omega’s new chairman, and EXR’s chairman also share some history...

Last week Omega’s appointed Martin Houston as its new Chairman.

Houston was the former COO of BG Group - which in 2008 acquired a company called QGC for ~$5.3BN...

QGC was the company EXR’s chairman Richard Cottee built as Managing Director from a $20M capped junior all the way through to the $5.3BN takeover back in 2008.

(Source)

Eventually in 2016 the combined entity (BG Group) was acquired by supermajor Shell for US$52BN.

(Source)

Now, just under a decade later, the two chairs are active in the same region again.

AND their old friend Shell is active next door to both companies...

(Source)

EXR is currently capped at $43M - EXR has a 2C ~3TCF contingent resource.

Omega is capped at $123M - Omega has a 2C ~1.7 TCF contingent resource.

Omega has the big flow test due to start any day now and EXR has a well planned for Q3.

In the short term we will have all eyes on the Omega result - what is good for Omega will be good for EXR...

Primarily because the gas underground isn’t limited by acreage boundaries, if Omega can prove commerciality on its ground it will be an indirect implication that EXR’s ground has similar commercial potential.

AND hopefully it brings much deeper pocketed eyes to the region...

We already know Shell is active in the area.

Last year there were mainstream media articles talking about Shell’s wells in the Taroom Trough being flared.

(Source)

There were also recent rumours Beach Energy were looking at the region - and that our EXR was attracting suitor attention...

(but EXR might be considered ‘too small’ for a takeover - major companies want to buy bigger de-risked companies - therein lies the opportunity for small cap investors)

(Source)

We have seen the American shale billionaires come into the Beetaloo Basin in the NT which is a similar type play to the Taroom Trough in QLD where EXR is.

We think the Taroom Trough (IF it can prove up commercial flow rates) could eventually move up a similar trajectory.

Some of the big experienced execs working at both EXR and Omega must also agree given their focus on the region.

And a positive (and hopefully exceptional) flow test from OMA in the coming weeks will lift all the surrounding players.

(remember that the type of gas being targeted in the Taroom Trough is unconventional gas, which is trapped across sprawling underground structures that span across acreage boundaries)

The key difference between the Taroom Trough and the Beetaloo is that the Taroom Trough is much closer to existing gas infrastructure and can tap into domestic and international markets a lot quicker.

Whatever happens, we think the next 6-9 months will be big for the Taroom Trough.

That’s why we Increased our Investment in EXR at the most recent capital raise (3.5c per share).

And all eyes are on neighbouring OMA to (hopefully) deliver a positive flow test over the coming weeks.

EXR also just signed a farm-out deal for its Mongolian assets where it is free carried on all exploration/development work through to a Final Investment Decision (FID).

The deal also has a clause which could see EXR’s share in the project get taken out for US$30M in the event the farm-in partner wants to exercise that right.

We see this as bonus upside where EXR has no capital commitments on the Mongolia assets, which have taken a back seat over the last couple of years.

Later in today’s note we will share our new EXR Investment Memo which will outline:

- What does EXR do?

- The macro theme for EXR

- Our EXR Big Bet

- What we want to see EXR achieve

- Why we are Invested in EXR

- The key risks to our Investment Thesis

- Our Investment Plan

But first, a little more on the deal EXR signed with Santos last week...

EXR farms IN to Santos ground - no its not the other way around

A few weeks ago now, EXR signed a 50/50 JV agreement with Santos.

The deal will see EXR increase its total resources within the Taroom Trough by roughly 66% or ~1.2TCF.

EXR is making a big bet here.

Normally a farm in agreement will see the larger player farm into the smaller explorer to support drill financing.

But this deal is the other way around.

It is clear that EXR thinks the ground in the Taroom Trough will be valuable in the years to come.

It also means EXR puts its foot on additional “cheap” (for now) gas resources.

The Santos deal means EXR is getting an extra ~1.3 TCF of contingent gas resources for little/no upfront expenditure and instead getting to add value to that resource by carrying Santos for a well and some seismic...

(One 3,100m appraisal well in ATP 2056 and 200km of seismic in ATP 2057 is planned).

We like the deal in general despite it being unusual in that the junior is farming into the major's ground.

Given our risk-reward appetite, we especially like its timing... just before a major flow testing program in the region, which could increase the value of real estate in the region.

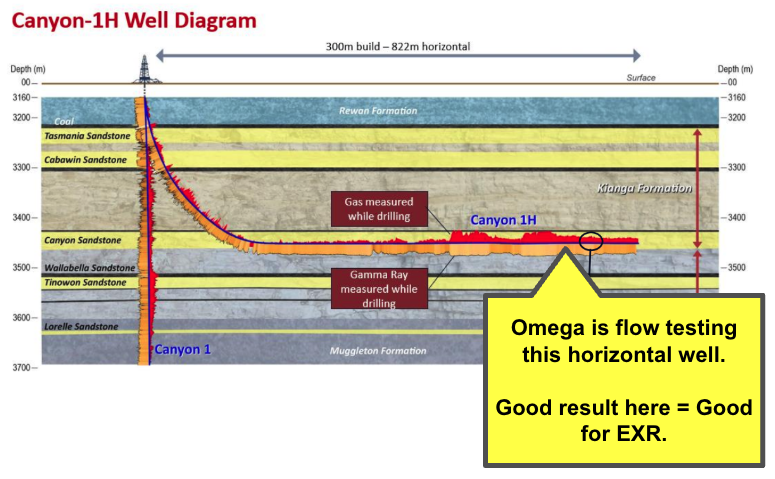

As mentioned earlier, in a few weeks time, EXR’s regional peer Omega will begin a “fracture simulation and flowback program” (a flow test) from its first horizontal well in the region.

Any positive results here should rub off on EXR given it is the smaller regional peer.

The market is interested in that upcoming flow test too.

(This is great for EXR given its market cap is currently ~1/3rd of Omega)

Omega’s share price has tripled in the last 12 months and is trading close to all time highs going into the program, plus it just banked $7M in cash at 31c to shore up the balance sheet:

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

In a recent webinar, EXR’s MD Neil Young gave a pretty good rundown on the Santos deal and why the Taroom Trough is gaining interest - especially with the Omega activity planned for this year.

EXR’s Chief Scientist Greg Channon also gives a pretty good rundown on the technicals of the ground being farmed into from Santos.

Check out that webinar here:

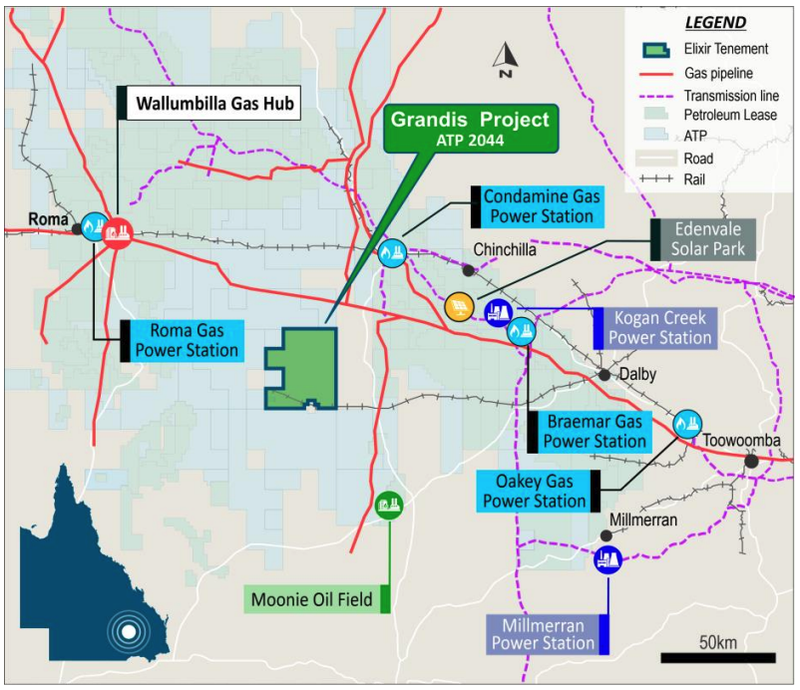

EXR in a region that can tap into domestic and international gas markets

We briefly wrote about it earlier, but the big differentiator for the Taroom Trough as a whole is how easily it can be tied into existing infrastructure.

The region (if unlocked technically) is right next to already built gas pipelines, road and rail:

Most importantly, the infrastructure means any gas produced in this part of Australia can be diverted to both the domestic market & international LNG markets.

There are two major markets for this gas to sell into

- International markets through nearby LNG Plants - there are three LNG plants in Gladstone near EXR’s project that have never operated at full capacity and could take more gas feedstock to ship to international markets.

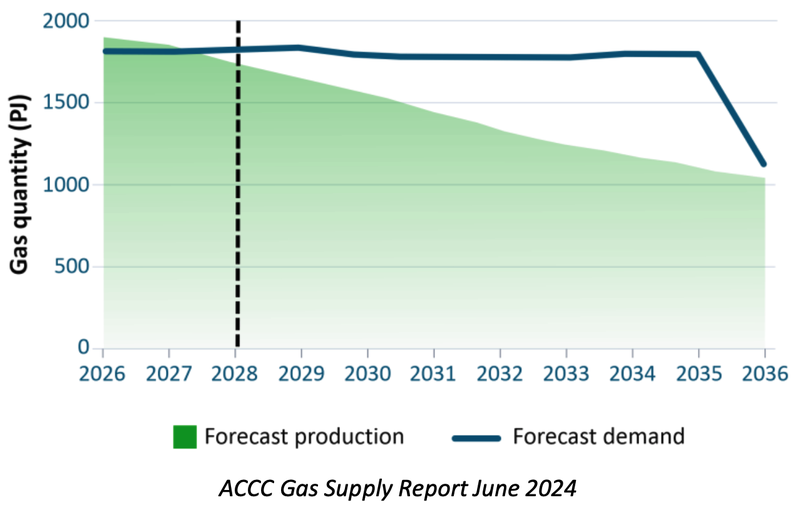

- Domestic market (east coast of Australia) - EXR’s project sits next to the Wallumbilla Gas Hub, which distributes gas to the east coast market. The east coast of Australia is forecast to be short gas in 2028 and expected to start experiencing supply shortages beyond 2026.

More on the East Coast Gas Crisis in Australia

Australia is in desperate need of natural gas.

As the throughput from coal fired power stations declines, more and more gas will be needed to fill the energy gap.

Although Australia is the third largest exporter of natural gas, there is talk of the country needing to IMPORT gas just to meet domestic demands:

(Source)

An interesting litmus test for the Australian government is whether it will extend the licence for Woodside’s LNG operation in the North West Shelf through to 2070.

If this operation goes ahead it will be a strong signal to the gas industry that Australia is serious about natural gas as crucial to Australia’s energy future.

We think that gas will play a big role in the energy mix for Australia going forward.

But due to environmental concerns natural gas exploration and development, particularly on the East Coast, has been lagging behind.

Last year the Australian Energy Market Operator (AEMO) event put out a statement titled “Gas market outlook signals need for new investment” which says supply shortages could start as early as the 2025 winter months.

If EXR is able to make a significant and commercial gas discovery in the Taroom Trough, we think that Australia will look at this project, and the entire basin as a strategic necessity in its energy future.

Our new EXR Investment Memo

Last week EXR signed a farm-out agreement for its Mongolian assets.

With that move it looks like EXR is fully focused on its QLD gas asset.

Given that shift in focus we thought it is a good time to review and update our EXR Investment Memo.

Our new Memo is primarily built around the QLD assets and includes::

- What does EXR do?

- The macro theme for EXR

- Our EXR Big Bet

- What we want to see EXR achieve

- Why we are Invested in EXR

- The key risks to our Investment Thesis

- Our Investment Plan

Investment Memo: Elixir Energy (ASX:EXR)

Opened: 24 February 2025

Shares Held at Open: 5,136,850

Options Held at Open: 2,567,021

What does EXR do?

Elixir Energy (ASX:EXR) is advancing an onshore gas project in the Taroom Trough in Queensland.

What is the macro theme?

Natural gas is a critical part of the energy mix.

Particularly in Australia, there are forecasts to be natural gas supply shortages off the East Coast due to a decade of underinvestment in gas projects to feed the domestic market.

Our Big Bet for EXR

EXR to achieve a $500M market cap through successfully advancing its Queensland gas project.

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved, and it will require a significant amount of luck. There is no guarantee that it will ever come true. Some of these risks we list in our EXR Investment Memo.

Why did we invest in EXR?

Taroom Trough in Queensland attracting some big names

EXR’s project sits in a part of QLD where majors like Shell and Santos are active. Another one of EXR’s regional peers is Omega Oil and Gas which is backed by Tri-Star Group who are pioneers of the Queensland gas industry.

Tri-Star drilled Queensland’s first commercial coal seam gas well in the 1990s and laid the foundations for the $80BN Liquefied Natural Gas industry in the state.

Any work developing the region by Shell or Omega will be good news for EXR.

EXR’s project is an existing discovery with ~3 trillion cubic feet in contingent resources

EXR already has booked 2C contingent resources of ~3 trillion cubic feet (TCF) of gas.

IF the projects and resources in the region are unlocked technically (by showing commercially viable flow rates) then EXR’s contingent resource could become very valuable, very quickly.

Strong board and management team

EXR’s board and management team including Chairman Richard Cottee and managing director Neil Young have a history of success in gas in Queensland.

EXR’s Chairman Richard Cottee took Queensland Gas Company from a $20M capped junior through to a $5.3BN takeover back in 2008 by a company called BG Group.

EXR’s Managing Director Neil Young was ex-Santos management, and Director Stephen Kelemen ran Santos’ Coal Seam gas portfolio.

Gas from the Taroom Trough can go to domestic & international markets

The region already has developed infrastructure meaning gas production can be directed to both the domestic market & international LNG markets.

- International markets through nearby LNG Plants - there are three LNG plants in Gladstone near EXR’s project that have never operated at full capacity and could take more gas feedstock to ship to international markets.

- Domestic market (east coast of Australia) - EXR’s project sits next to the Wallumbilla Gas Hub, which distributes gas to the east coast market. The east coast of Australia is forecast to be short gas in 2028 and expected to start experiencing supply shortages beyond 2026.

East coast gas exposure in Australia

Australia is in desperate need of natural gas, there are major shortages forecast for 2028 and beyond, and very little new supply coming online. EXR’s project is located near existing piping and gas infrastructure that can tie into the east coast gas market if commercialised.

(Bonus) Free carried upside from Mongolian assets:

EXR just signed a farm-out deal for its Mongolian assets where it is free carried on all exploration/development work through to a Final Investment Decision (FID).

The deal also has a clause which could see EXR’s share in the project get taken out for US$30M in the event the farm-in partner wants to exercise that right.

We see this as bonus upside where EXR has no capital commitments.

What do we expect EXR to deliver?

Objective #1: Drill first well this year (Santos JV)

As part of its 50/50 deal with Santos EXR has to drill a 3,100m appraisal well on ATP 2056 which already has a 2C contingent resource of ~1.3 TCF.

Here we want to see EXR book more resources.

Milestones:

🔲 Drilling permitted

🔲 Drilling funded

🔲 Drilling commenced

🔲 Drilling complete

🔲 Book additional resources

Objective #2: Farm out agreement on 100% owned ground

EXR is looking for a farm-in partner to drill an exploration well over its 100% owned ATP 2077 block.

Milestones:

🔲 Secure Farm-In Partnership

🔲 Drilling exploration well at ATP 2077

🔲 Drilling results

Objective #3: Regional progress

This objective is less specific to things EXR can control but we think it is important for the EXR story overall.

We want to see EXR’s regional peers progress their projects and prove up commercially viable flow rates across the region.

Milestones:

🔲 News from EXR’s peer Omega Oil and Gas

🔲 News from Shell

🔲 News from Santos

🔲 BONUS - New entrants into the region

BONUS: Objective #4: Progress on Mongolian assets

Any news from EXR’s Mongolian assets will be an unexpected bonus for us especially now that the project has been farmed out.

What could go wrong?

Funding risk

To drill its Queensland appraisal well, EXR must still secure funding, which it is now pursuing but is not always guaranteed on favourable terms.

Exploration risk

If EXR drills an appraisal well, there is no guarantee that it finds anything interesting. There also could be mechanical issues that affect the outcome of the drilling.

Partnership Risk

EXR is looking for a partner for its exploration wells. There is no guarantee that EXR finds a farm-in partner for the project.

What is our investment plan?

We have been Invested in EXR for nearly 6 years now, and the share price can deliver some solid runs when the company is delivering success.

We are holding on to see the Taroom Trough project play out over the coming couple of years and will assess as the company approaches and delivers key catalysts in line with our hold conditions.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.