EXR to drill for gas in Queensland - Next Door to Shell and Santos

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 3,180,000 EXR shares and the Company’s staff own 100,000 shares at the time of publishing this article. The Company has been engaged by EXR to share our commentary on the progress of our Investment in EXR over time.

Our 2019 Energy Pick of the Year, Elixir Energy (ASX:EXR) is in the early stages of planning a significant gas drilling event expected to occur in late 2023, on a recently acquired gas project in Queensland.

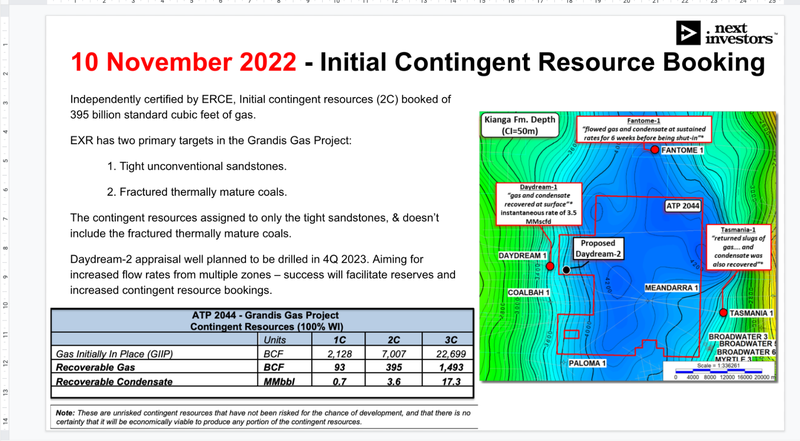

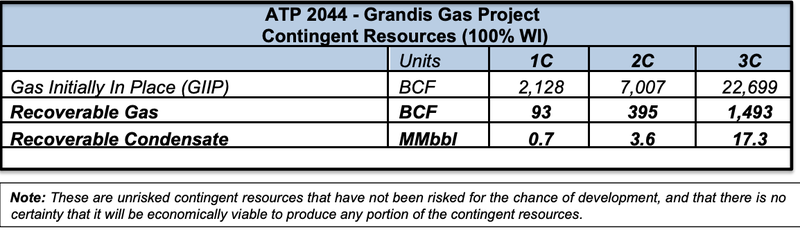

Yesterday EXR released a “contingent resource estimate” showing 395Bcf of potentially recoverable gas — within its initial 3.3 Tcf unrisked mean prospective resource.

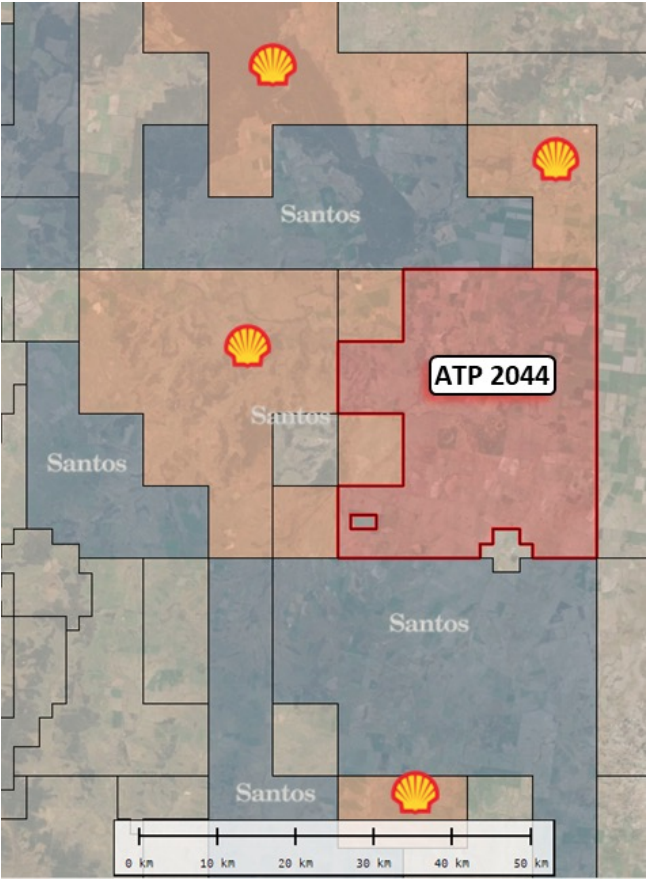

Importantly, the project is right next to existing processing and export infrastructure, and acreage held by energy majors like Shell and Santos.

This is an appraisal well - EXR will be drilling to see if they can flow gas at sustained commercial rates, just 3km from Shell’s previous successful well.

We like having a pipeline of future drilling events in our portfolio, and this one is now firmly pencilled in in our calendars.

As always, we will be looking for a price run up in the lead up to drilling, which is still ~12 months away so likely has not been priced in yet.

From a macro perspective, EXR is preparing to drill for gas at the right time.

Russia’s move to shut off the flow of gas to Europe has ushered in unprecedented uncertainty around global gas supply.

Far from a short-term issue, the war in Ukraine has caused a fundamental shift in global gas markets — irreparably damaging the reputation of Russia, previously the world’s largest gas exporter.

Gas customers around the world want to be confident that their supply is secure.

So with a cloud forever now hanging over the dependability of Russia, international buyers are placing a significant premium on security of supply from elsewhere.

That means higher gas prices are making gas assets that were previously uneconomical due to low gas prices suddenly attractive.

Particularly those assets in stable countries, like Australia, which has shown to be a reliable supplier to Asia for decades.

The ongoing Australian east coast gas crisis is also far from over, with extra supply urgently required by industry.

Recognising these changing market dynamics, EXR was quick to react, acquiring a Queensland gas asset that’s close to major infrastructure, and neighbouring majors Shell and Santos.

As we flagged above, yesterday EXR booked an initial contingent resource — that is, potentially recoverable gas — of 395 Bcf for the asset, based on work done by its neighbour Shell ten years ago. Earlier, upon acquiring the asset, EXR prepared an initial prospective inferred resource of 3.3 Tcf.

EXR said that it is looking to drill its first appraisal well in 12 months’ time — leaving plenty of time for further newsflow that could help de-risk the project ahead of drilling.

As always, with early stage gas exploration wells, we expect there to be a run up in share price as the drill event approaches late next year.

EXR considers the location of this asset — now named the Grandis Gas Project — in the Taroom Trough in the Bowen Basin, to be one of a handful of low risk locations in the world with access to spare liquefaction plant capacity.

And it’s in good company with majors Shell and Santos holding the licences that are next door to and surround EXR’s project area.

With its initial well, EXR will be aiming for increased gas flow rates from multiple zones, with success to facilitate reserves and increased contingent resource bookings.

This acquisition came somewhat out of left field for us.

Since we first Invested in EXR in mid-2019, the company has focused coal seam gas exploration at its giant landholding in Mongolia. Later, the company began investigating an opportunity to produce hydrogen on that same land under a MoU with a subsidiary of Japanese multinational Softbank.

However, we don’t see this new Queensland asset as detracting from EXR’s Mongolian projects.

Rather, this looks to be a well thought out strategic addition that could deliver a meaningful cash injection if successfully progressed and sold.

EXR’s team has previous experience in this area of Queensand, particularly its Chairman Richard Cottee (a Queensland gas pioneer, who as MD, steered Queensland Gas Company from $20M market cap to $5.7BN).

Add to that the current shakeup of global gas markets and EXR finding the right asset at the right price.

Our Big Bet

“EXR to achieve a $1BN market cap through successfully advancing one or more of its three projects: its Mongolia gas project, Mongolia green hydrogen project, and/or its Queensland gas project.”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our EXR Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

For a summary of EXR’s progress over time on this project and its others, see our EXR Progress Tracker:

And here you can hear the EXR story (across all three EXR projects) from EXR MD Neil Young who presented to the Noosa Mining conference yesterday — the presentation can be viewed here.

EXR’s Queensland gas asset

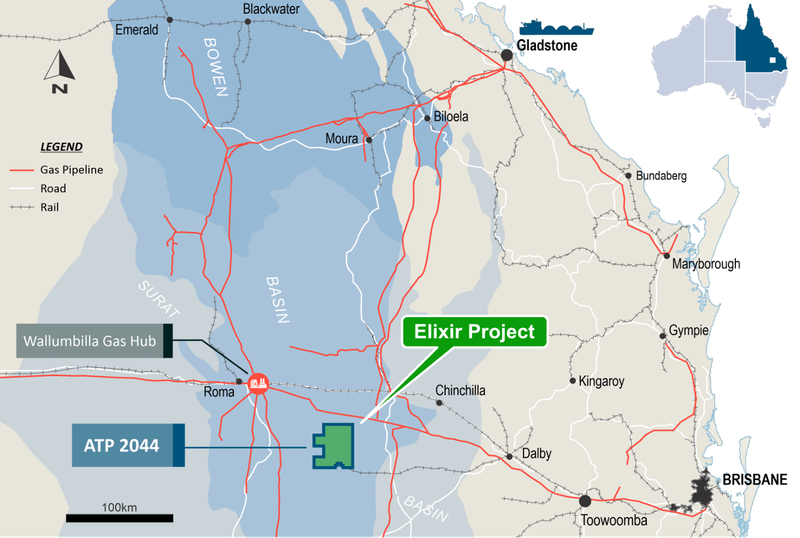

EXR’s latest asset, ATP 2044 — now named the Grandis Gas Project, is located in an existing oil and gas province — the Taroom Trough in the Bowen Basin.

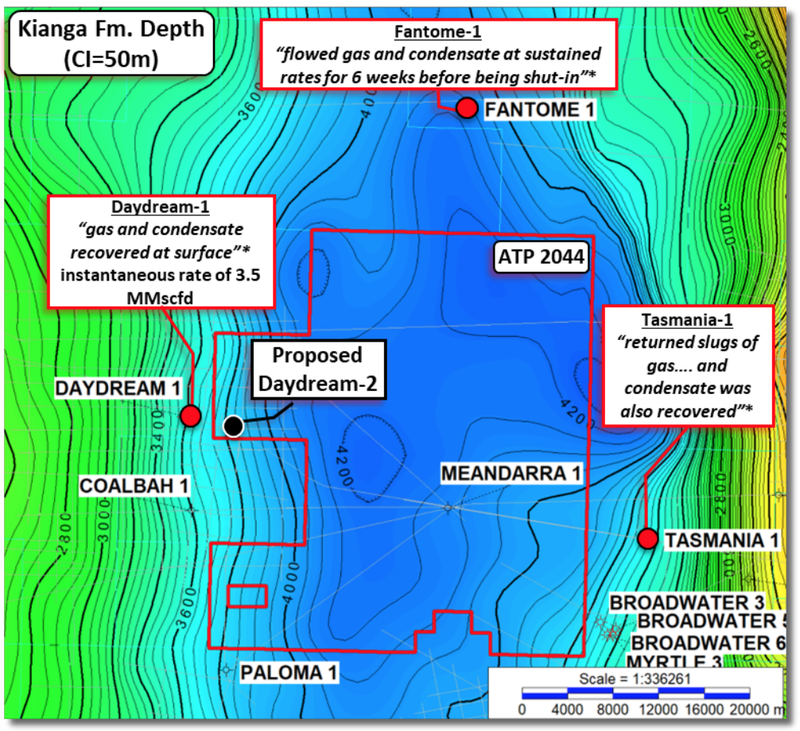

Importantly, ten years ago BG Group (now Shell) drilled the Daydream-1 well, located just over the border of EXR’s licence area and about 3 kilometres from EXR’s proposed appraisal well. That well flowed an instantaneous rate of 3.5 MMcfpd.

Here’s the gas and condensate recoveries from nearby wells:

Daydream-1 — two kilometres west of EXR’s permit area

The project is just 35km from the Wallumbilla Gas Hub — the most important gas hub in Australia. It is also adjacent to existing and proposed pipelines, and is not far from the Gladstone port and LNG facilities, providing ready access to East Australian and international gas markets.

We’ll get into the details of yesterday’s announcement shortly, but you may be wondering how EXR came to have such an asset on its books, considering its previous exclusive focus in Mongolia.

There are a number of reasons why this all came together and EXR was able to pick up this asset that’s surrounded by majors.

The first point is that this acquisition was relatively cheap for EXR — it paid $500k in cash, along with $3M worth of EXR shares, and a royalty over future hydrocarbon liquid production (even though it is primarily a gas play).

Secondly, small companies have the ability to move quickly.

EXR is a small and nimble operator that recognised the potential to add a mature gas play amid the current global energy market upheaval, and was able to quickly execute on a deal.

EXR’s technical and commercial teams were already familiar with the Taroom Trough, so their existing understanding of the play allowed EXR to swoop in and pick up the asset.

That included EXR Chairman Richard Cottee, who played a major role in establishing Queensland’s gas industry and famously steered $20 million gas junior, Queensland Gas Company (QGC), to a $5.6 billion takeover by BG Group in 2008.

Interestingly, it was QGC — which by then was owned by BG Group (now Shell) — that first drilled the Taroom Trough.

And lastly, we understand that the project vendor had another asset in the UK, which due to the shakeup in the European gas market, had become quite lucrative to develop, so it made sense to let the Queensland project go and focus its attention 100% on Europe.

Taking a closer look at the project itself, and you can see EXR neighbours in the Taroom Trough include major operators Santos and Shell:

EXR’s ATP 2044 “Grandis Gas Project” and neighbours

It’s helpful that there are so many big operators here in the Taroom Trough — who may also be drilling their own wells over the coming year, possibly before EXR drills — as all this information helps build a better picture of the overall play.

As mentioned, ten years ago BG Group (now Shell) drilled the Daydream-1 well, located just over the border of EXR’s licence area.

That well flowed at an instantaneous rate of 3.5 MMcfpd from an interval covering one-tenth of the gross prospective reservoir section.

Yet at the time that well was drilled, Shell already had enough gas to feed its LNG plant, so were happy to sit on its assets here, presumably awaiting favourable market dynamics, such as what we’re seeing now. For that reason, we wouldn’t be surprised to see Shell begin to drill these assets in the near term.

EXR viewed this project as somewhat of a “hidden gem”, because at a $5 gas price the project economics was never going to stack up.

But today, the higher gas prices, which are anticipated to remain permanently elevated, makes higher cost gas now attractive, particularly if it is coming from a safe jurisdiction.

The ACCC have speculated that it expects the east coast energy crisis to likely last beyond the winter of 2023, and with global factors also keeping gas prices elevated, we may see even more of EXR’s neighbours drill their nearby assets.

Source: Australian Energy Regulator

One additional, and possibly critical, characteristic of the Taroom Trough is that it is very low in carbon dioxide.

This is important because large companies will simply no longer develop gas projects that are rich in CO2 since it requires sequestration, which comes at a cost, or if it is released into the atmosphere it’s not a good look.

Therefore, any project rich in CO2 will simply be dismissed as an acquisition target by the majors.

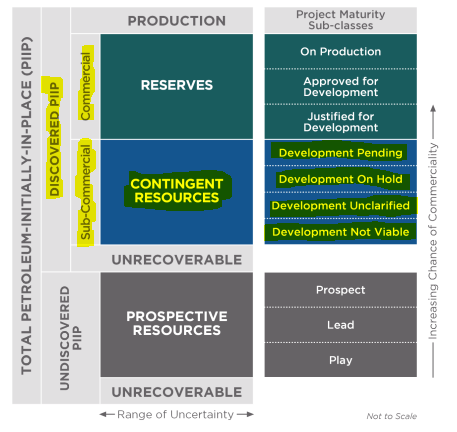

Initial contingent resource booking - 3.3 Tcf inferred prospective resource

On acquiring the project, EXR prepared an initial prospective inferred resource of 3.3 Tcf — which points to the potential scale on offer here.

Since then EXR’s technical team has done a lot of work analysing the data available and realised that the extensive work done by BG Group (now Shell) ten years ago — drilling six deep wells in this same unconventional formation and flowed gas to surface — is already enough to consider some part as contingent or ‘discovered’.

A ‘contingent resource’ is basically one classification below a “reserve” and is used to describe a resource that is able to be developed but is contingent on certain factors.

🎓 Be sure to check our our education article: How to Read Oil & Gas Resources

These generally include things like a need to develop pipeline infrastructure, a power connection or simply a higher gas price.

In EXR’s case it needs a stable commercially viable flow rate.

EXR engaged ERC Equipoise, a leading international oil & gas evaluation firm, which EXR previously engaged in Mongolia, to independently review the work of its technical team and come up with the initial contingent resource figure of nearly 400 billion standard cubic feet of gas — a very meaningful number in any definition.

This was based on the results of previous drilling in the same Taroom Trough play, immediately to the west, north and east of EXR’s Grandis Gas Project area.

However, EXR has two primary targets in the Grandis Gas Project, namely:

- Tight unconventional sandstones.

- Fractured thermally mature coals.

But the contingent resources only apply to the tight sandstones — the origin of the gas flows in nearby wells.

The fractured thermal mature coals, meanwhile, remain an exploration target not yet evaluated by ERCE.

For that reason, establishing flow rates therefore is a key objective for the Daydream-2 well, which EXR plans to drill this time next year.

EXR stresses that success in drilling that well could lead to a “material increase in contingent resources” in the overall licence area.

Well funding options

EXR intends to drill this well in around 12 months’ time, in 4Q 2023, where it is aiming for increased flow rates from multiple zones. The success of which would facilitate reserves and increased contingent resource bookings.

However, drilling costs money.

EXR hasn’t provided any figures around what the well might cost, but we know that unconventional gas drilling can get expensive.

EXR has a reasonably strong cash position for its market cap, with ~$18M in the bank at the end of the last quarter, having successfully executed a share Placement and SPP near the top of the market in April last year, raising ~$26M at 36c per share.

Whilst EXR could go it alone and fund drilling themselves, as is common with oil and gas drilling events, there is always a chance EXR try to bring in a partner for drilling — to assist both in financing and on the technical details.

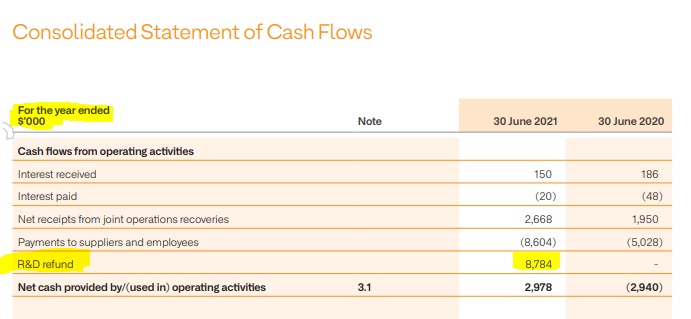

We also note that a number of Australian gas companies have received Research and Development tax credits, including Galilee Energy and Strike Energy. This government programme sees eligible companies entitled to receive a 43.5% refundable offset for eligible R&D costs.

Below is the $8.8M Strike Energy received (disclosed in its 2021 annual report):

Therefore, we expect EXR has a few different financing options and could utilise a mix of equity, debt, credits, or partnerships.

Looking ahead to drilling

Previous drilling by BG Group (now Shell) saw the Daydream-1 well flow an instantaneous rate of 3.5 MMcfpd when it was drilled around ten years ago.

As for our expectations of EXR initial well, Daydream-2 appraisal well, we would be happy to see similar flow rates.

However, in-house reservoir modelling by EXR suggests that flow rates could be improved significantly by:

- Accessing fractured coals as well as sandstones

- Using state of art stimulation techniques

- Focusing on full the Permian section (Kianga and Back Creek Formations)

From there we would hope to see the project attract the interest of majors, particularly those already operating in the region.

There are also gas producers with a presence in Gladstone that will face a need for new backfill for their existing infrastructure, or EXR could see demand from the domestic gas market that increasingly needs gas.

The project area (Source: Energycapture)

What’s next for EXR?

QLD gas project:

EXR intends to drill its first well — the Daydream-2 appraisal well in Q4-2023, about 3 kilometres from the Daydream-1 well that was drilled by BG/Shell 10 years ago.

Ahead of the spud date, over the next 12 months we will be watching for the following newsflow:

- Contracting and commissioning a drill rig.

- Newsflow from adjacent operators including Santos and Shell.

- More details on well financing, whether that be a farm-in partner or something else.

- Locking in land access agreements

Then, once drilling begins we will want to see:

- Drill reach target depth and run well stimulation

- Hopefully see an intersection of thick gas bearing formation

- Most importantly - announcement on flow rates

Mongolian coal bed methane gas project:

EXR has now started the long term pilot production program we have been waiting for at its gas project in Mongolia.

In its September quarterly report, EXR confirmed that the drilling of the two production wells had been completed and that pumping operations would begin in the next month or so.

Over the next few months we will be watching for gas flow rates from this project.

Mongolian green hydrogen project:

EXR, in its September quarterly report, confirmed that the results of a pre-feasibility engineering study into a pilot green hydrogen production project is to be expected soon.

Off the back of this, EXR and Japanese conglomerate Softbank’s subsidiary (SB Energy) will look at potential offtake opportunities.

Importantly, if successful, this work will form the basis to move the EXR and SB Energy partnership from the current non-binding MOU stage into a more firm partnership.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.