EMD: USA signs exec order to fast-track psychedelic medicine research and access. EMD is already doing it.

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 13,743,293 EMD Shares and 5,822,221 EMD Options and the company’s staff own 138,889 EMD Options at the time of publishing this article. The Company has been engaged by EMD to share our commentary on the progress of our Investment in EMD over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs. Any forward-looking statements are uncertain and not a guaranteed outcome.

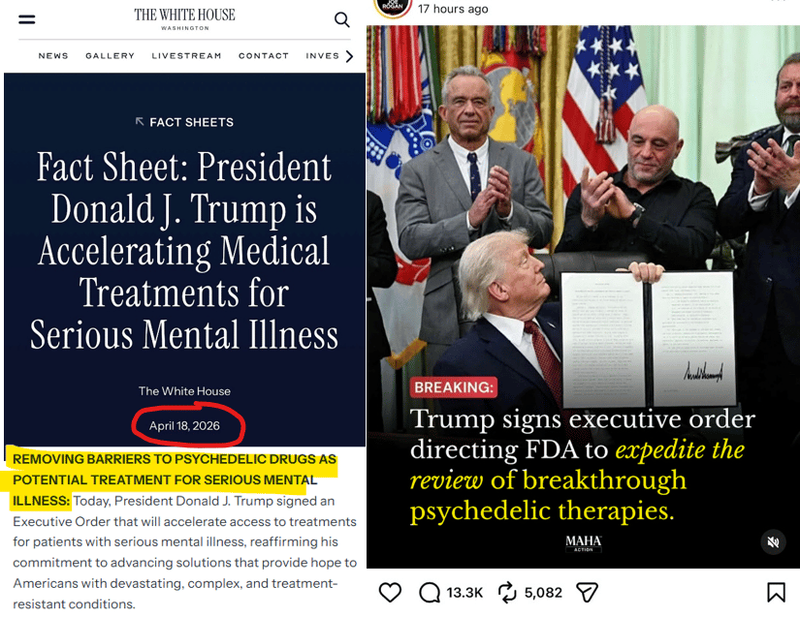

Over the weekend, in the White House, US President Trump signed an Executive Order that accelerates access to psychedelic based treatments for patients with serious mental health conditions.

This is now official US policy:

Psychedelics like psilocybin and MDMA are showing they can "reset" the brain's stuck patterns - offering breakthrough relief from serious mental health conditions and addiction where traditional meds have failed for decades.

The US effectively banned psychedelics nationwide in 1970 with the passage of the Controlled Substances Act (CSA) - the lead up to this is actually a very interesting story, but one for another day.

Now, USA drug companies have been given the green flag to go fast and hard on developing new psychedelic treatments for serious mental health issues, putting the treatments through clinical trials (phase 1, 2 and 3) and seeking FDA approval to get them to end users.

More than 50 psychedelic-assisted therapy programs are currently in global clinical development.

For most companies developing a new psychedelic treatment, clinical delivery (safely getting it to patients) rather than drug development, is expected to become a major bottleneck to patient access. (source)

Clinical trials to get a new psychedelic treatment approved require:

- intensive psychotherapy,

- long treatment sessions,

- recruitment of vulnerable patient populations,

- purpose-built environments, and

- a highly trained, multidisciplinary workforce.

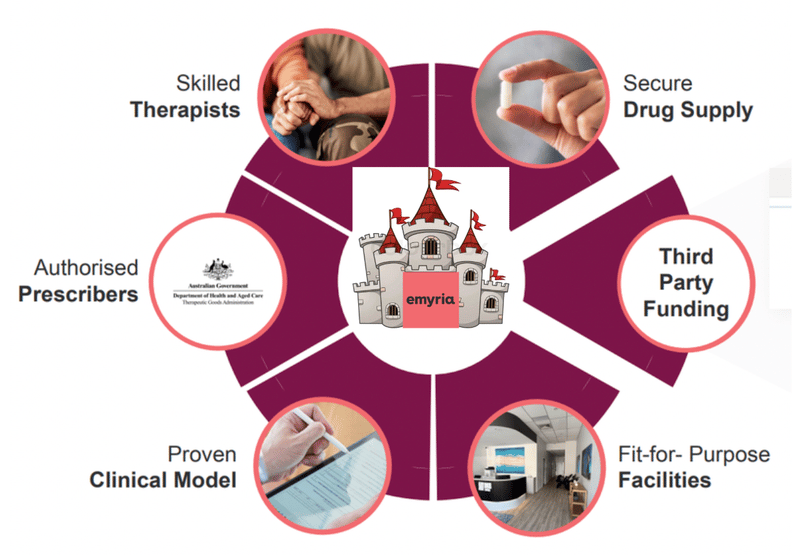

Our Investment Emyria (ASX:EMD) is the only company in the world that has years of experience operating private, legally-authorised clinics delivering psychedelic therapy for mental health at commercial scale.

Which means EMD has the extremely rare combination of infrastructure and expertise ALREADY IN PLACE required to deliver psychedelic therapies safely and at scale.

Specifically, including helping to run clinical trials on innovative new psychedelic treatments.

Like the clinical trials that USA drug companies are now suddenly allowed to do...

This morning, EMD announced a global partnership program where overseas companies that have developed a new psychedelic treatment can access EMD’s clinic networks in Australia:

(Source)

These drug companies (EMD calls them “sponsors”) will pay EMD to use its experience and infrastructure to safely deliver innovative new psychedelic treatment for mental health issues.

EMD says they have already been approached by several major clinical research organisations (sponsors)

AND has already entered a service delivery contract for international drug sponsor, the NASDAQ listed Psyence Group.

Wait, but how has EMD already got so many years of experience operating private, legally-authorised clinics delivering psychedelic therapy for mental health at commercial scale?

Australia became the first country in the world to legalise the medical use of psychedelics for treating mental health conditions in 2023.

Yes, seriously - that certainly wasn’t on our bingo card for this decade and it made world news at the time:

EMD has spent years as a first and fast mover, building out a network of private clinics providing psychedelic‐assisted treatments for mental health in Australia.

When we first Invested in EMD, our bet was that they could leverage a multi-year head start in Australia by refining and scaling the clinical processes treating real patients with psychedelics for mental health, at commercial scale, under a legal framework.

And collect years of real world patient outcome data.

Before the rest of the world was allowed to even legally start.

And now the biggest market in the world, the USA, has just dramatically accelerated the process of developing new psychedelic treatments for mental health.

Which opens up major international drug sponsors to pay for doing clinical trials via EMD’s clinic network.

EMD’s business model is treating real patients with psychedelics for mental health - collecting real world patient outcome data.

All from its 100% owned clinical network in Australia - the only place in the world where this has legally been possible over a few years.

EMD has:

- Active clinics in Perth, Brisbane and Victoria with over 100 patients screened, actively receiving treatment or waiting to start.

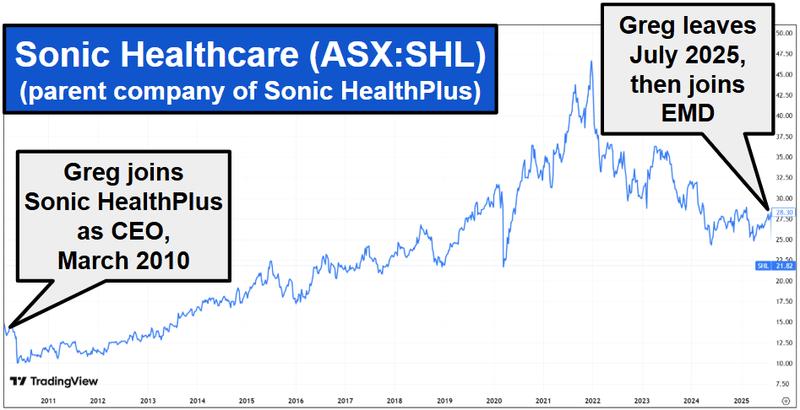

- A chair, Greg Hutchinson, who has experience scaling a clinic business at Sonic Healthcare (he also invested $1M into EMD after he joined)

- Medibank Private and the Department of Veterans Affairs as payers.

And troves of patient data, clinical processes and waiting lists.

Trump’s Executive Order explicitly mentions a need for real-world evidence to go into drug evaluation and approval decisions.

So where are all these massive US drug companies going to get patients on which to safely run their clinical trials?

EMD is a global leader in the space and ready to service them.

EMD has spent years laying the foundations to bring promising, evidence-based innovations to patients facing some of the toughest mental health challenges.

And it is operating clinics right now, and has been doing so for years.

So how did an ASX small cap company land itself in global leader status?

Because Australia was the first country on the planet to downschedule MDMA and psilocybin for prescribed therapy use.

(source)

We don't get to say this often about Australia, but for psychedelic therapies, Australia is the global leader.

And EMD is the company that leans the hardest into that first-mover position.

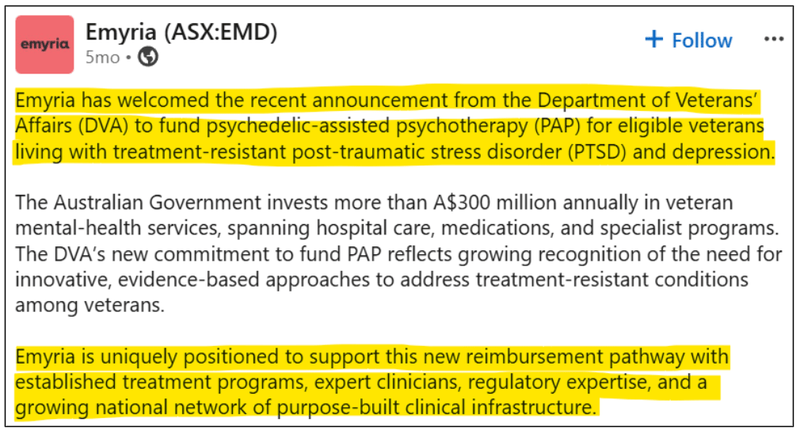

The big kicker is the Executive Order’s first order of business is to treat Veterans in the US. (source - Executive Order) (source - Fact sheet)

EMD in Australia,is the primary beneficiary of the world’s first payer agreement from the Australian Department Of Veterans’ Affairs.

Australia’s DVA now funds eligible veterans to receive specialized, evidence-based care programs, including psychedelic-assisted psychotherapy (PAP) for PTSD and treatment-resistant depression.

These treatments are delivered through EMD’s specialist-led programs, including their Empax clinics and partnerships with Avive Health, which provide intensive mental health services.

(source)

So EMD also knows how to treat the exact patient pool that the US is looking to target first.

In Australia the veteran community now has access to this type of treatment so is already beginning to see the benefits.

In America there were 15.4 million American adults with a “serious mental illness” (SMI) as of 2022 (source)

Plus 23.4% (61.5 million people) of American adults experienced some form of mental illness in 2024 (source).

(which shows the size/scale of the opportunity in the US relative to Australia)

That template - protocols, outcome measures, payer integration, patient pathway - is exactly what US counterparties (VA contractors, US clinic operators, even state-level programs funded by the $50m ARPA-Hallocation) will need to stand up quickly.

EMD is one of very few companies globally that has actually done it.

Any future EMD announcement of US partnerships, licensing discussions, or data-sharing arrangements with US institutions could be big news.

EMD is currently in scale-up mode

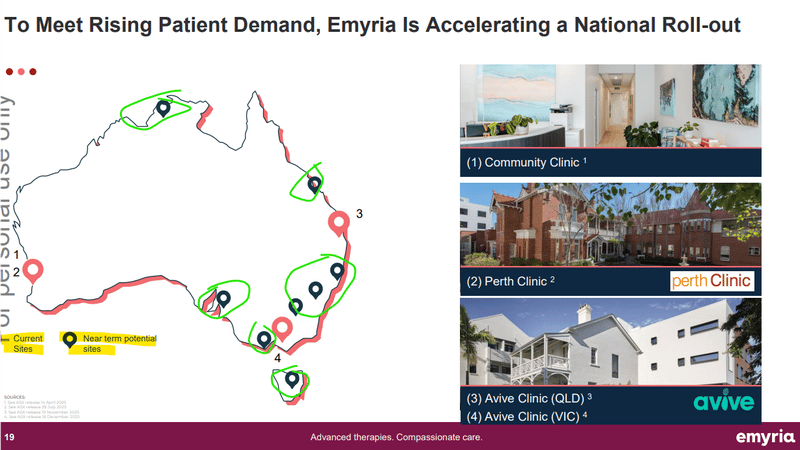

EMD is currently going about opening up new clinics all around Australia to meet increasing demand.

EMD is capped at $39M and had $10.5M cash in the bank at 31 Dec 2025.

EMD already has:

- A clinic in Perth at full capacity (and currently being expanded) - now with 5 approved psychiatrists (up from 2), 39 trained therapists, and a 4th treatment room about to come online

- A clinic operating in Brisbane - with first insurer-funded patients nearing completion

- A clinic opening in Victoria at Avive Health's Mornington Peninsula hospital - expected to open Q2 2026, AND

- source) Over 100 patients screened, actively receiving treatment or waiting to start - (with a further 67 patients booked for screening in Q1 2026 - nearly double the numbers we were seeing a few months ago). (

All while EMD is looking to grow its national footprint - especially across the east coast of Australia. (source)

Here is a slide from EMD’s most recent presentation showing the “near term potential sites”:

(source)

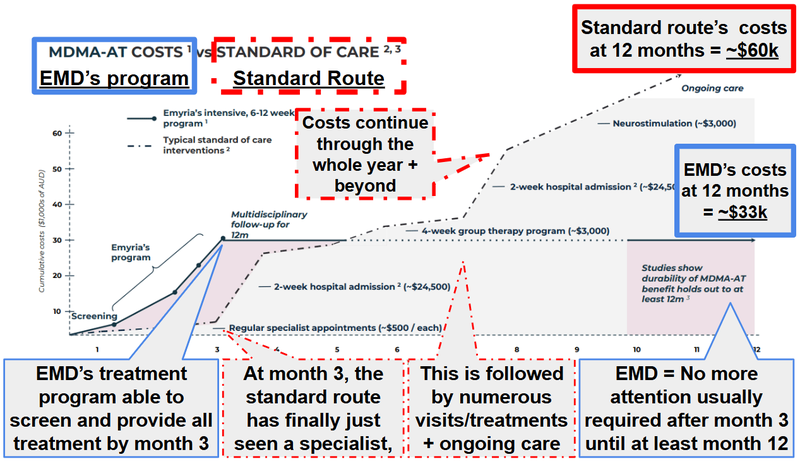

EMD’s treatment costs ~$20,000-$30,000 (including three days of dosing and all pre dosing and follow-up therapy sessions).

The treatments can be covered by those payer agreements with Medicare and the DVA we mentioned earlier, so the patient is not directly out of pocket.

Plus the ceiling payers will be willing to pay could change as the therapies become more mainstream.

(source)

At the moment, EMD has capacity for 50 dosing days per week, having grown from just 4 dosing days per week, just ~6 months ago when it was operating a single clinic in Perth.

This growth in capacity is also translating into increased revenues - EMD’s latest quarterly showed $906k in cash receipts - up 93.6% on the previous quarter. (source)(source)

And those recent figures barely include (if at all) the Brisbane clinic which only began treatments “in late December” (so at the end of the quarter).

The growth model is pretty simple to follow - the more clinics EMD opens (or expands existing clinics), the more dosing that can happen, which ultimately means more revenues.

(EMD coming into NSW and VIC two most populated states in Australia inside the next few months)

The VIC preparations nearing completion ahead of its opening expected this quarter and NSW has already launched a recruitment campaign earlier this month.

And now EMD has launched its global partnership programme it can unlock higher services revenue (sponsor-funded clinical delivery typically commands attractive rates).

We already know EMD’s therapy works

The reason we like EMD’s first mover advantage is because the company will have years of data and a treatment protocol that's been perfected in the clinic.

(and because EMD is showing that its treatment actually works - really well)

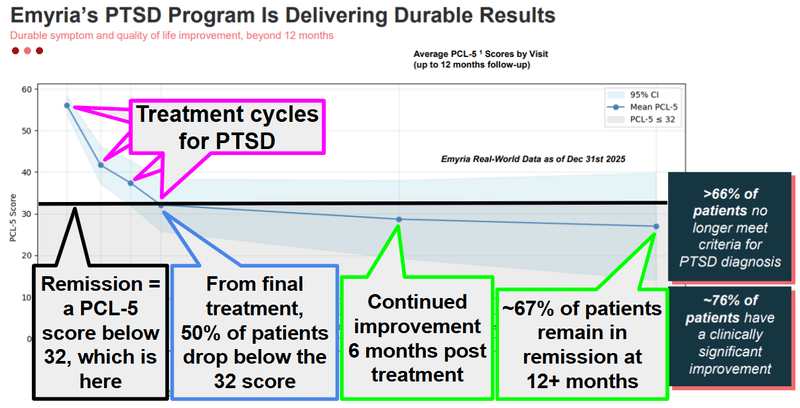

Back in February, EMD published real-world data showing that its PTSD treatment program produces durable, lasting recovery.

EMD showed that two thirds of patients were in “remission” - not just at the end of treatment, but 12+ months after treatment ended.

(Remission means a significant decrease in or disappearance of the signs and symptoms of a disease by a particular treatment).

And that patients were continuing to improve even after EMD’s therapy was complete.

Improvement post therapy is a strong signal because it tells us that EMD’s treatments aren’t just suppressing symptoms temporarily - it's leading to genuine, lasting recovery.

In a cohort of patients with severe, treatment-resistant PTSD who had tried everything else and failed, ~67% no longer met the criteria for a PTSD diagnosis more than a year after EMD's psychedelic-assisted therapy.

~76% showed clinically significant improvement.

(source)

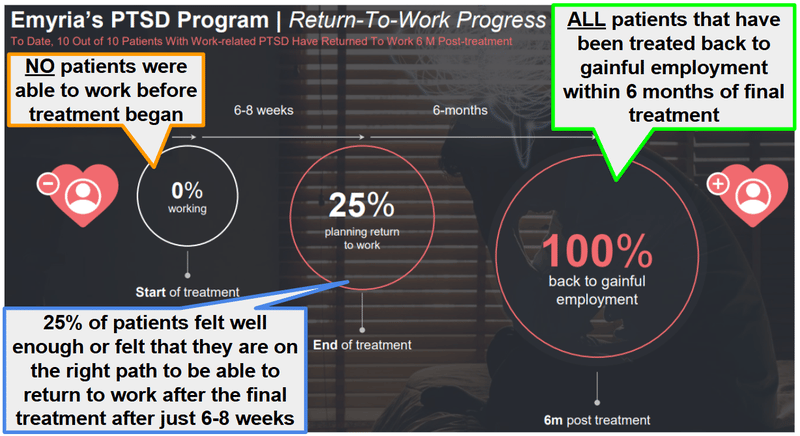

The one case study we found super interesting was of “Kate” - a first responder with cumulative workplace trauma. She was on permanent disability for nearly 5 years, tried every therapy under the sun, and was completely stuck.

Six months after EMD's MDMA-assisted therapy, she returned to work.

More than 12 months after treatment, she remains in remission.

(EMD reported 10/10 patients with work-related PTSD returned to work within 6 months of finishing treatment)

(source)

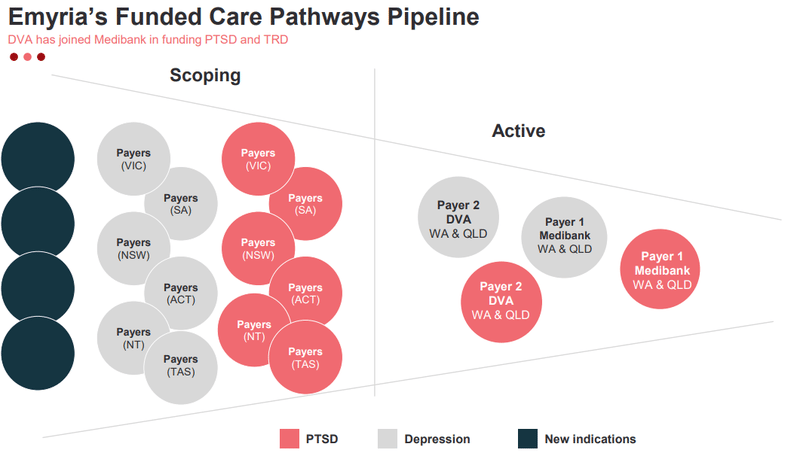

The two big wildcards for how fast EMD’s expansion plays out are:

- How many “payers” emerge for EMD’s treatment protocol - EMD’s already got Medibank and the Department of Veterans’ Affairs onboard as payers. EMD just needs to convince more institutions (e.g. insurance and/or government organisations) to fund the treatment for patients who need it.

- The indications that get legalised for psychedelic treatments - at the moment EMD can treat PTSD and Treatment Resistant Depression. The more indications that get legalised, the more EMD’s addressable market grows.

The payers ultimately create demand, and the “new indications” point towards blue sky upside - the more conditions EMD can treat, the bigger the market becomes for the company.

The following slide from EMD’s most recent presentation illustrated those two points pretty well:

(source)

What we want to see over the coming months is more of those circles move from the “scoping” stage into the “active” stage.

Now US payers are a genuine possibility

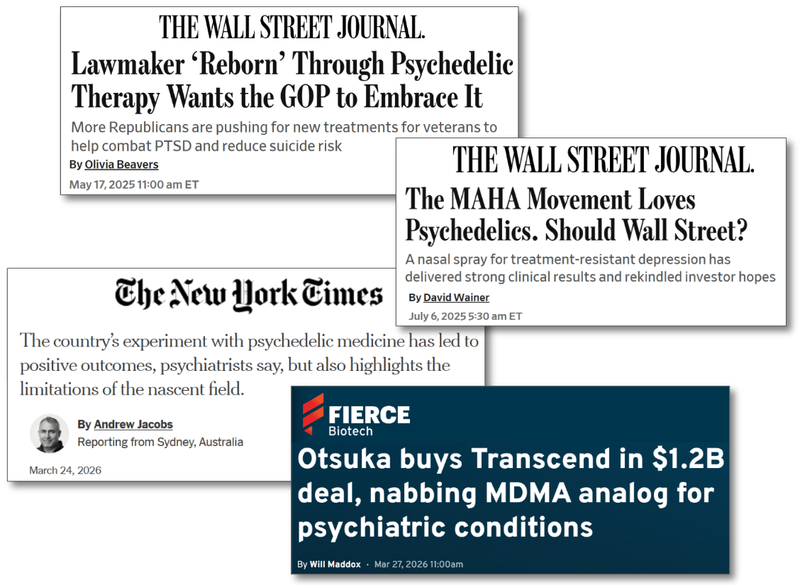

The US has been building up to the weekend’s Executive Order news.

Over the past few months.

- Wall Street Journal has been running sustained coverage on psychedelic therapy. (source)(source)(source) The

- New York Times ran a feature on 24 March specifically on MDMA-assisted therapy for PTSD - and the fact that Australia is the country leading it (source). The

- All In podcast dropped a 37-minute episode on psychedelics that hit nearly half a million views in 10 days. (source) The

- source) Big Pharma got off the sidelines - on 27 March, Japanese major Otsuka announced it was acquiring New York-based Transcend Therapeutics for up to US$1.225 billion ($700M upfront + $525M in milestones), picking up an MDMA analog for PTSD that's now in Phase 3. (

(source)(source)(source)(source)

All-In Podcast - Bryan Johnson: I Just Took the Most Powerful Dose of DMT in the World... Here's What It Was Like

Then yesterday, Trump made it official US policy.

On Monday morning (US time), every US biotech with a psychedelic treatment in Phase 2 or 3 is going to sit in a boardroom and ask one question:

"Where do we find real-world evidence on patients actually receiving this therapy outside a trial arm?"

Because the Trump Executive Order specifically directs HHS, the FDA and the VA to "increase clinical trial participation and evidence generation."

Real-world evidence means real patients, in real clinics, receiving real treatment - not carefully managed trial participants.

As mentioned earlier there is one country where that is already legally allowed.

And only one company is already doing it at scale.

That's EMD capped at $39M.

Now a genuine chance to pull off a few payer deals with US organisations OR the US government directly.

Why we like EMD’s first mover status in the psychedelics care space

We think EMD has a defensible market position because it has:

- Authorisation from Australia’s TGA to deliver both Psilocybin and MDMA-assisted care to patients (this is not easy to get)

- A Payer Agreement with Medibank to cover the cost of these therapies to its members (years in the making)

- Data that shows it works and continues to work months after the patient is treated.

- A means to deliver therapies through physical clinics that it owns and operates and access to skilled therapists.

- Purchasing power when looking to secure more drug supply from the market

- Scale potential with an approved protocol from the TGA that it can “franchise” out to other clinics looking to deliver assisted therapies.

- A managing director who has experience in scaling up a healthcare company.

(source)

We are Investing in EMD as we hope it can prove to have a defensible business model within Australia, scaling up its psychedelic clinics and securing funding from major insurers.

Then, if any other jurisdictions around the world legalise psychedelic therapies - EMD takes the model it refined in Australia and rolls it out in that region.

That’s what today’s global partnership programme is about.

The biggest market being the USA, where we are seeing a lot of capital flow into the psychedelics space.

(AbbVie spent US$1.2B to acquire Gilgamesh's psychedelic drug program. Johnson & Johnson's ketamine nasal spray Spravato is tracking toward a US$1.6B annual revenue)

EMD benefits from all the capital being poured into drug development because:

- More R&D money means better drugs (shorter dosing times, fewer side effects) that EMD can eventually use in its clinics.

- More attention on the sector means more regulatory momentum globally.

- And EMD is already years ahead in building the operational infrastructure to actually deliver these therapies to patients.

When the US eventually opens up to psychedelic-assisted therapies in clinical settings, EMD will have years of real-world data and a refined business model that nobody else has.

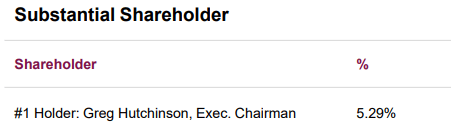

With EMD we are backing Greg Hutchinson, EMD's Executive Chairman (and biggest individual shareholder - owning 5.29% of the company).

(source)

Greg’s been there and done it before scaling Sonic HealthPlus to over 7,000 active clients across 40+ clinic locations.

That parent company, Sonic Healthcare, is now capped at ~$10.2BN.

(source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Our EMD Big Bet:

"EMD re-rates to a +$300M market cap by making a breakthrough with one or more of its clinical trial programs (MDMA, psilocybin, ketamine, CBD) while rapidly growing the footprint of its mental health treatment clinics."

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our EMD Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

What we want to see next:

Here is everything we are looking out for over the next few months from EMD:

- VIC clinic treatments commence (Q2 2026 - imminent).

- NSW clinic treatments commence (post the current therapist recruitment drive).

- More payers - EMD is already working with Workcover Australia (including the Australian Federal Police's cohort, one of the highest PTSD-burden groups in the country). A third major payer after Medibank + the Department Of Veterans’ Affairs could also be a meaningful re-rate catalyst

- The BIG new one after today’s news: Any US-facing deal. Given the Trump EO, this is the catalyst we were previously only hoping for - now we think it's a "when" more than an "if."

What are the risks?

Clinic scale ups are not easy to execute especially across multiple geographic locations.

EMD must replicate its Perth success in multiple states, which involves securing new physical locations, establishing more payer relationships plus onboarding qualified physicians.

This may not run smoothly by running into unforeseen issues, so until EMD achieves self-sustaining profitability it remains reliant on external market funding to fuel this growth.

Any delays in the scale up could impact the market’s perception of EMD’s ability to execute its strategy and re-rate the company's share price lower.

Scale up risk

Even though EMD can secure funding for Medibank, there is a lot that needs to go right in terms of scale. This includes securing more sites to operate its services as well as securing more MDMA supply to meet the expected demand. Scaling costs money, and EMD needs to reach a level of profitability before it can scale without continuing to tap the market for resources.

Source: “What could go wrong” - EMD Investment Memo 18 June 2025

Other risks

Like any early-stage clinical services and drug development company, EMD carries significant risk, here we aim to identify a few more risks.

EMD is currently in a rapid scale-up phase and held $10.5M in cash at the end of 2025. Until the company reaches self-sustaining profitability, there is a constant risk that it will need to raise further capital, which would likely result in shareholder dilution.

There is also a significant execution risk involved in expanding a specialised clinic network across different Australian states. If the company struggles to recruit enough highly trained psychiatrists and therapists to staff new locations, the rollout in Victoria and New South Wales could face costly delays.

While the recent US Executive Order has created a massive tailwind, the company’s business model is still highly sensitive to the regulatory environment. Any negative shifts in how the TGA or international bodies like the FDA view psychedelic-assisted therapies could significantly damage EMD’s first-mover advantage.

Finally, the company’s long-term growth depends on more health insurers and government bodies coming on board as "payers." If other major institutions are slow to adopt these therapy protocols, the addressable market may not grow as quickly as the current valuation might suggest.

Investors should consider these risks carefully and seek professional advice tailored to their personal circumstances before investing.

Our EMD Investment Memo

You can read our EMD Investment Memo in the link below.

We use this memo to track the progress of all our Investments over time.

Our EMD Investment Memo covers:

- What does EMD do?

- The macro theme for EMD

- Our EMD Big Bet

- What we want to see EMD achieve

- Why we are Invested in EMD

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.