EMD: Australia leading the way in next major global health breakthrough?

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 13,743,293 EMD Shares and 5,822,221 EMD Options and the company’s staff own 138,889 EMD Options at the time of publishing this article. The Company has been engaged by EMD to share our commentary on the progress of our Investment in EMD over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs. Any forward-looking statements are uncertain and not a guaranteed outcome.

Australia's drug regulator has just made a series of sweeping recommendations...

... expected to make it cheaper and easier to deliver psychedelic therapies to treat mental health issues.

The Therapeutic Goods Administration (TGA) made a series of recommendations two days ago - keep reading to find out exactly what they are...

(source)

The TGA’s recommendations could be game-changers for the economics of our Investment Emyria (ASX:EMD)’s business model.

Capped at $36M, EMD is the only ASX-listed company operating psychedelic therapy clinics at scale.

And one of the market leaders globally.

Thanks to the TGA legalising psychedelic-led mental health therapies in 2023 - Australia is a global leader in the space.

(Australia was the first country in the world to do this, hence EMD has a precious global head start on nailing running and refining the private clinic delivery model.)

The TGA’s four recommendations could make EMD’s regulatory moat that much stronger by:

- Decreasing psychiatrist hours per treatment (meaning lower costs to EMD)

- Expanding who can be a part of the therapy team (again lower costs - but also easier and faster to scale)

- Allowing for therapies to take place outside of hospitals (cheaper for EMD to set up new clinics)

- Allowing EMD to train its own workforce of Authorised Prescribers (very good for EMD, which has a head start in the industry)

By relaxing its original rules, it looks like Australia’s drug regulator is happy with what they have seen from industry so far...

(more details on the changes later in today’s note)

This is the second major regulatory tailwind for EMD over the last six weeks.

Six weeks ago, US President Trump signed an Executive Order to fast-track psychedelic-assisted therapies for mental health.

The Executive Order put real-world evidence (precisely what EMD delivers at its clinics) at the centre of the approvals pathway - specifically directing regulators to "increase clinical trial participation and evidence generation". (source)

(source)

Real-world evidence means real patients, in real clinics, receiving real treatment.

(Not carefully managed trial participants.)

Real world evidence is exactly what EMD delivers RIGHT NOW in Australia.

(and have been doing in private clinics since 2024)

Until recently, EMD’s clinical rollout was mainly focused on Australia.

We think the news out of the US has all of a sudden brought into play the big American pharma companies working on psychedelic drugs for different conditions.

IF the US drug regulators want to see the drugs being developed in LIVE environments, then the service EMD is scaling up - all of a sudden becomes valuable to those pharma companies.

We said this in our last EMD note:

We think the TGA news gives the US pharma companies that much more of a reason to look at Australia (and maybe EMD) as a trusted partner to deliver “real-world evidence”.

From the perspective of a US drug sponsor (or a US payer) looking at where to send a real-world delivery contract today, the picture is:

- Country: Australia is the only place this has been legal at scale for years.

- Operator: EMD is the only ASX-listed company doing it safely, professionally, and legally at a commercial scale.

- Precedent in place: EMD already has the NASDAQ-listed Psyence Group on a service delivery contract - proof there is demand out of the US. (source)

Ultimately, we think the likelihood of US institutions cutting deals with companies like EMD only got stronger this week.

And IF deals get signed, under the new recommendations, the economics could be a lot more favourable to EMD.

The next big catalysts we are looking out for from EMD

We think the two biggest catalysts going forward for EMD will be related to:

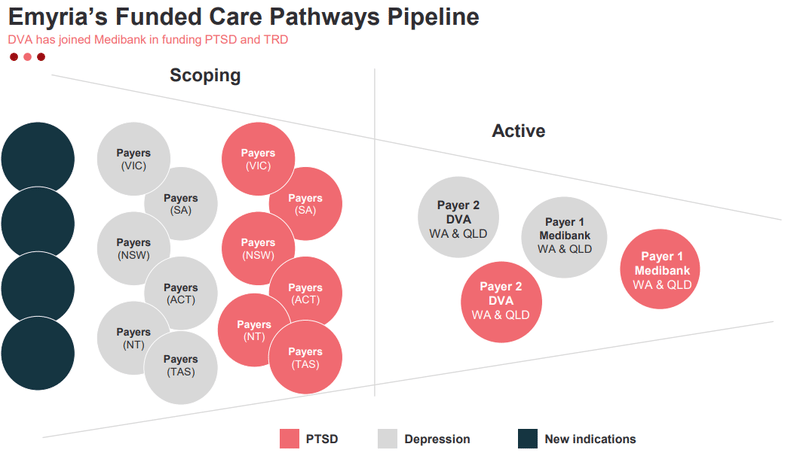

- How many "payers" emerge for EMD's service - there is already Medibank & the Department of Veterans’ Affairs (a payer is the group funding patient treatments on their behalf)

- Which indications (specific mental health issues) get legalised for psychedelic treatments - at the moment, EMD can legally treat PTSD and Treatment-Resistant Depression.

And it's finally looking like there is a lot of movement at the station on both fronts:

On the payer's side:

- potential US payers (government groups, large health insurers, pharmacy benefits managers and self-insured employers,).

The US Executive Order brings in - every existing payer agreement more profitable to deliver. AND the TGA changes could make

We listened to the following webinar from three weeks ago where Executive Chair Greg Hutchinson talked about how ~A$2.2BN NASDAQ listed Compass Pathways was finding it difficult to deliver their drug.

The AFR article Greg references mentions its hard to take because of the professionals needed to administer it (which is exactly what EMD specialises in).

Greg hammered that point home saying how EMD is “uniquely positioned to be able to assist” with the delivery of psychedelics to patients.

(skip to 4:30 - also, here is the AFR article he references)

On the indications side:

That article in The Australian said “considering whether to expand access to psilocybin-led therapy to people in end-of-life distress".

(source)

Palliative care alone in Australia means hundreds of thousands of patients per year.

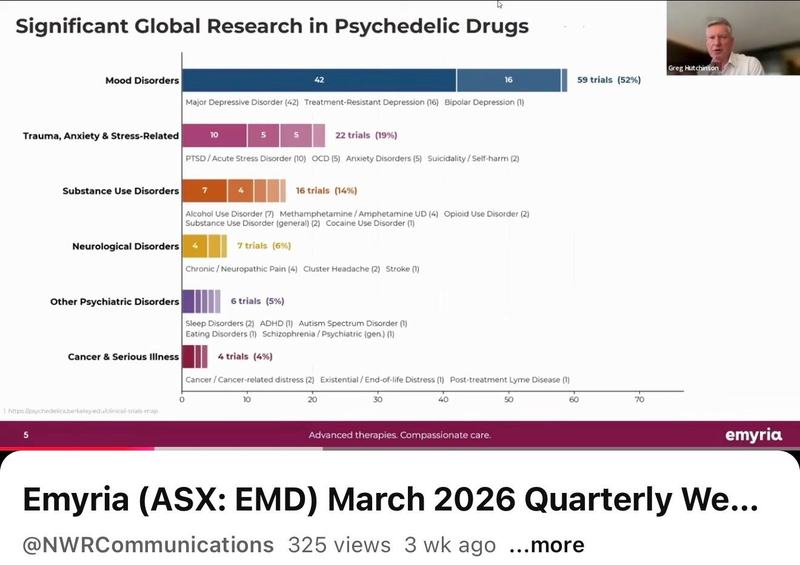

EMD’s Chief Operating Officer also had a great slide in that recent webinar on other potential indications too:

(source)

Ultimately, what we want to see is progress on the image below (more of the circles move from scoping into active status):

(source)

So what did the TGA announce?

Anyone who wants to can check out the full press release here: Targeted consultation - AP scheme for psychedelics.

Here were our four key takeaways relevant to EMD:

1. Psychiatrist hours per treatment could decrease

Authorised Prescriber (AP) psychiatrists are the single most expensive input in a psychedelic clinic.

They are highly specialised which means they are expensive.

Before the TGA’s recommended changes, the rules required APs to stay on-site for the entire dosing session - up to 8 hours per patient, per dose.

Now they only need to be present at administration - not for the full dosing day.

After dosing, the trained therapy team takes over (provided the patient remains within 15 minutes of an emergency department).

THE BENEFIT FOR EMD:

A single psychiatrist can lead more treatments at the same time and have a team of staff helping manage patients which ultimately means lower costs.

2. The therapy team now includes other professions

Before the TGA’s recommended changes, the team running treatments required a psychologist plus a counsellor.

Now the team can include:

- nurses with mental health experience

- occupational therapists

- social workers

THE BENEFIT FOR EMD:

The treatment team can now be built up of a much bigger labour force - which will allow EMD to scale easier and with more staff availability.

3. Therapies don't have to take place in a hospital anymore

Treatment sites no longer need full hospital accreditation under the National Safety and Quality Health Service Standards (NSQHS).

Instead they can be lower criteria clinics that are WITHIN 15 minutes of an accredited hospital Emergency Department.

THE BENEFIT FOR EMD:

The clinics EMD sets up will cost less and can be put in parts of Australia that wouldn't have been possible otherwise (like regional towns, where hospital space is limited).

4. EMD's existing Authorised Prescribers can train new ones

Under the new rules, a psychiatrist can qualify as an Authorised Prescriber via supervised practice under an existing AP.

THE BENEFIT FOR EMD:

EMD already has a team of Authorised Prescribers - so it can train more in-house on its own treatment program. That gives EMD even more of a moat in terms of specialisation.

Summary of the impact on EMD:

We think the changes could turbocharge EMD’s scale up.

It should make the costs of delivering psychedelic therapies significantly cheaper, which ultimately means the therapies become more accessible, meaning more demand for EMD’s services.

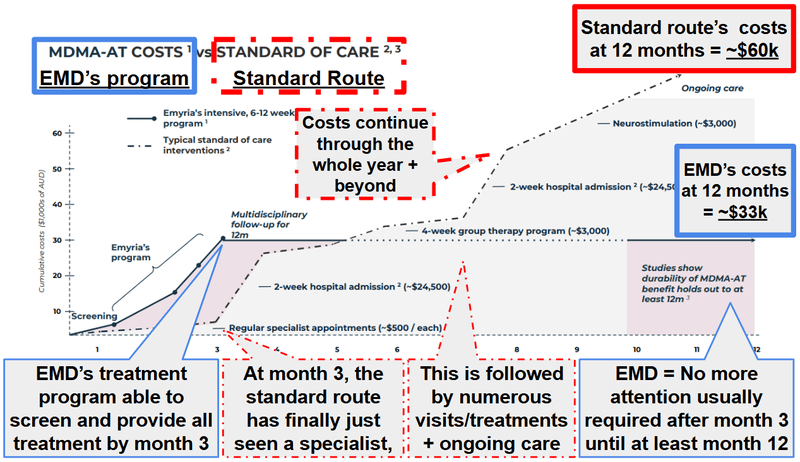

EMD's current treatment cycle costs ~$20,000–$30,000 per patient (covered in part or in full by Medibank and the DVA).

Even though the current standard of care for patients can be upwards of $60k in the first 12 months of treatment (and even more in the longer run).

(source)

You can also read more about the treatment, the benefits and the costs, in this ABC report here.

IF the treatment costs can come down, then the value proposition for a potential payer becomes even more attractive.

We already know EMD's therapy works - and better than expected

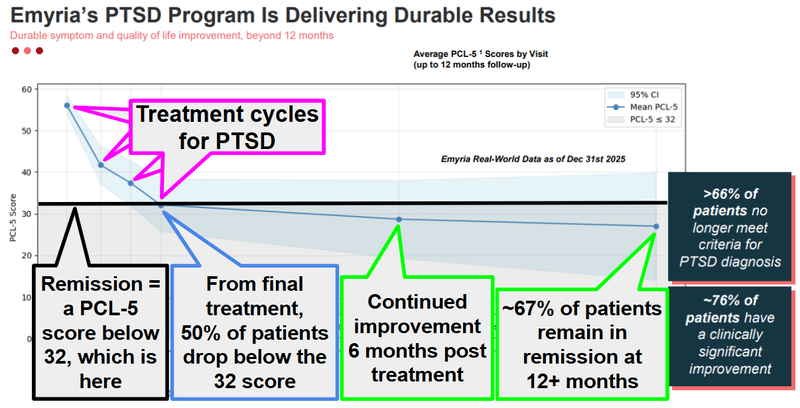

Back in February, EMD published real-world data showing that its PTSD treatment program produces durable, lasting recovery.

EMD showed that two thirds of patients were in “remission” - not just at the end of treatment, but over 12 months after treatment ended.

(Remission means a significant decrease in, or disappearance of the signs and symptoms of a disease by a particular treatment).

And that patients were continuing to improve even after EMD’s therapy was complete.

Improvement post therapy is a strong signal because it tells us that EMD’s treatments aren’t just suppressing symptoms temporarily - it's leading to genuine, lasting recovery.

In a cohort of patients with severe, treatment-resistant PTSD who had tried everything else and failed, ~67% no longer met the criteria for a PTSD diagnosis more than a year after EMD's psychedelic-assisted therapy.

~76% showed clinically significant improvement.

(source)

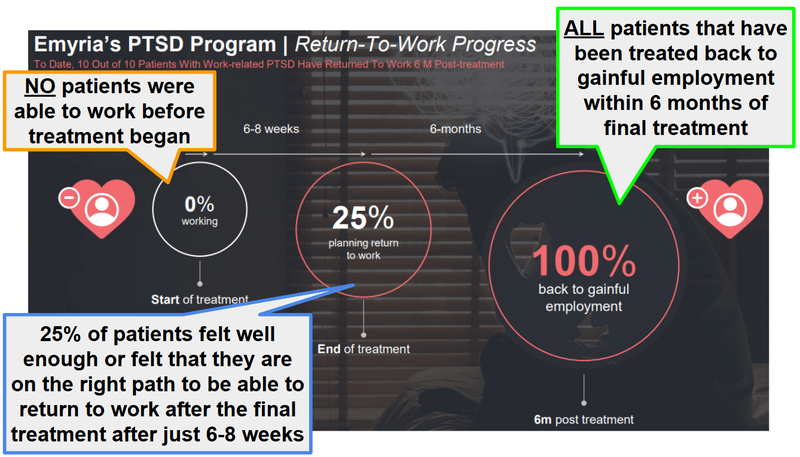

The one case study we found super interesting was of “Kate” - a first responder with cumulative workplace trauma. She was on permanent disability for nearly 5 years, tried every therapy under the sun, and was completely stuck.

Six months after EMD's MDMA-assisted therapy, she returned to work.

More than 12 months after treatment, she remains in remission.

(EMD reported 10/10 patients with work-related PTSD returned to work within 6 months of finishing treatment)

(source)

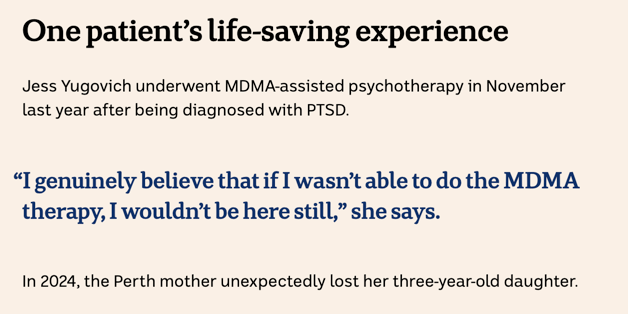

The ABC report also covers the story of Jess Yugovich who tragically lost her three-year-old daughter. Jess underwent MDMA-assisted psychotherapy at EMD’s Empax clinic, and the results were life saving for her:

(Source)

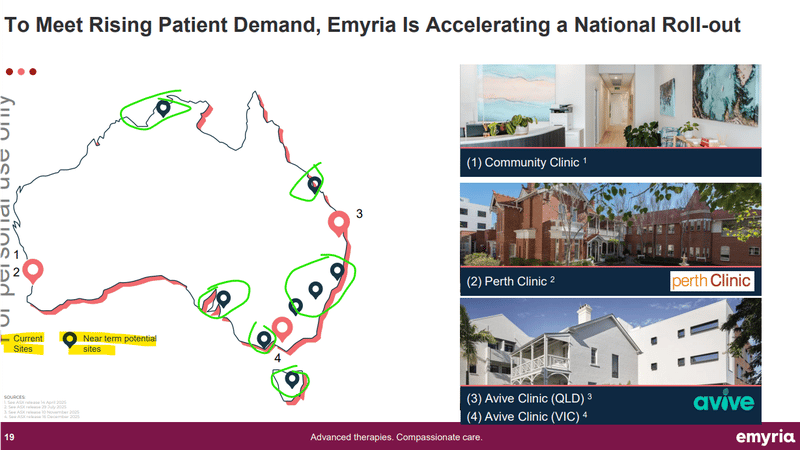

EMD is currently in scale-up mode

EMD is currently opening up new clinics all around Australia to meet increasing demand.

EMD already has:

- A clinic in Perth at full capacity (and currently being expanded) - now with 5 approved psychiatrists (up from 2), 39 trained therapists, and a 4th treatment room about to come online

- A clinic operating in Brisbane - with first insurer-funded patients treated.

- A clinic operating in Victoria in the Mornington Peninsula, AND

- More near-term potential sites in the pipeline.

Here is a slide from EMD’s most recent presentation showing the “near term potential sites”:

(source)

As mentioned earlier, EMD’s treatment costs ~$20,000-$30,000 (including three days of dosing, all pre dosing and follow-up therapy sessions).

The growth model is pretty simple to follow - the more clinics EMD opens (or expands existing clinics), the more dosing that can happen, which ultimately means more revenues.

Now layer in what the TGA has recommended and the margins delivering those same therapies could be about to improve.

Over the next 3-6 months we think the expansion into VIC and NSW could be the main story in terms of national rollout for EMD.

Ultimately the growth of its mental health treatment clinics forms the basis for our Big Bet which is as follows:

Our EMD Big Bet:

"EMD re-rates to a +$300M market cap by making a breakthrough with one or more of its clinical trial programs (MDMA, psilocybin, ketamine, CBD) while rapidly growing the footprint of its mental health treatment clinics."

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our EMD Investment Memo.

Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

What we want to see next:

Here are some of the big things we are looking out for over the next few months from EMD:

- VIC clinic treatments start (now operating).

- NSW clinic treatments commence (post the current therapist recruitment drive, 7 psychiatrists confirmed for NSW training ahead of commencing).

- More payers - EMD has already launched a NSW workforce campaign (including the Australian Federal Police's cohort, one of the highest PTSD-burden groups in the country). (source)

A third major payer after Medibank + the Department Of Veterans’ Affairs could also be a meaningful re-rate catalyst.

- The BIG new one after the recent US news: Any US-related deal. Given the Trump Executive Order, this is the catalyst we were previously only hoping for - now we think it's a "when" more than an "if."

What are the risks?

Clinic scale ups are not easy to execute, especially across multiple geographic locations.

EMD must replicate its Perth success in multiple states, which involves securing new physical locations, establishing more payer relationships as well as onboarding qualified physicians.

This may not run smoothly by running into unforeseen issues, so until EMD achieves self-sustaining profitability it remains reliant on external market funding to fuel this growth.

Any delays in the scale up could impact the market’s perception of EMD’s ability to execute its strategy and re-rate the company's share price lower.

Scale up risk

Even though EMD can secure funding for Medibank, there is a lot that needs to go right in terms of scale. This includes securing more sites to operate its services as well as securing more MDMA supply to meet the expected demand. Scaling costs money, and EMD needs to reach a level of profitability before it can scale without continuing to tap the market for resources.

Source: “What could go wrong” - EMD Investment Memo 18 June 2025

Other risks

Like any early-stage clinical services and drug development company, EMD carries significant risk, here we aim to identify a few more risks.

EMD is not yet cash flow positive, which means its spending more cash than its bringing in.

It’s possible that EMD will need to raise additional capital to support growth in the coming months and years.

Setting up physical clinics and hiring staff ahead of treatments creates high upfront costs and cash burn. Until EMD achieves self-sustaining profitability, it remains exposed to the risk of further capital raises that dilute existing shareholders.

The recent TGA updates are currently only recommendations and have not yet been formalised into binding regulations. If these proposed changes fail to go ahead or face implementation delays, EMD's expected cost savings from reduced psychiatrist hours and lower clinic setup criteria will not materialize.

The current business model relies heavily on a limited number of approved payers like Medibank and the DVA. If other major health insurers are slow to approve and fund these treatments, EMD's addressable market expansion might face headwinds.

Scaling up operations requires a consistent and secure supply of medical-grade psychedelics like MDMA and psilocybin. Any disruptions in global or local supply chains could prevent clinics from operating at full capacity and meeting patient demand.

Investors should consider these risks carefully and seek professional advice tailored to their personal circumstances before investing.

Our EMD Investment Memo

You can read our EMD Investment Memo in the link below.

We use this memo to track the progress of all our Investments over time.

Our EMD Investment Memo covers:

- What does EMD do?

- The macro theme for EMD

- Our EMD Big Bet

- What we want to see EMD achieve

- Why we are Invested in EMD

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.