EMD secures first east coast site in Queensland to service Medibank members for psychedelic treatments

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 16,979,999 EMD Shares and 5,822,221 EMD Options and Company’s staff own 770,000 shares and 138,889 Options at the time of publishing this article. The Company has been engaged by EMD to share our commentary on the progress of our Investment in EMD over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs.

The scale up is happening...

Yesterday, our small cap Investment Emyria (ASX:EMD) signed an agreement to set up its first clinic to deliver psychedelic therapies for mental health conditions in Queensland.

The deal is with Avive Health at the 63 bed private hospital Avive runs in Brisbane.

This deal follows EMD’s landmark agreement last month with Australia’s largest health insurance company - Medibank.

Medibank will cover the cost of EMD's psychiatrist-led PTSD therapies for any of its eligible ~4 million members...

EMD charges between A$20,000 to A$30,000 to the insurance company to run these treatments for its members.

(with 800,000 people that have PTSD in Australia we’ll let you do the maths on what the Total Addressable Market could be)

EMD is the first (and only) company in Australia to have the regulatory approval AND the backing of a major health insurer to deliver psychedelic assisted therapies.

And this new clinic will be EMD’s first entry into the Queensland market.

EMD has first right of refusal for additional clinics in Victoria and South Australia too.

Health insurance companies have a big problem...

According to the Productivity Commission, poor mental health is costing the Australian economy more than $200BN annually, with PTSD, anxiety and depression driving significant and growing disability and insurance claims.

Payouts for mental health in Australia in 2019 were $1.2 billion and have ballooned $2.2 billion in just 5 years.

Insurers are warning of a ‘crisis of sustainability’ - with premium hikes and benefit restrictions likely unless new, more effective interventions emerge...

So insurers are turning to psychedelic therapies... because frankly, nothing else is really working.

Last month Medibank announced that it would fully fund its members' psychedelic therapies for mental health.

Delivering those therapies? Our small cap investment EMD.

Right now EMD only delivers therapies out of two clinics in Perth.

Now with Medibank’s backing, the focus for EMD is to rollout clinics across the east coast of Australia - the deal with Avive is EMD’s first entry into Queensland.

EMD expects to have the clinic up and running by Q4 of this year.

(Source)

This deal with Avive gives EMD exclusive access to deliver therapies within its site in Brisbane...

And potential to expand into Victoria and South Australia as well.

This new site will directly service Medibank clients as part of the “national rollout” plan.

More on why Australia’s largest health insurer Medibank backing EMD

Because mental health is costing them a lot...

The AFR recently reported that mental health claims to insurance companies grew from $1.2 billion in 2019 to $2.2 billion in 2024.

(Source, AFR)

Also, of all $5 billion in life insurance payouts last year, 44 per cent were linked to mental ill health rather than a physical condition or injury (compared with 25 per cent in 2019).

It is a big problem that EMD is looking to solve.

Because EMD is in the fortunate position of securing a “payer” for its services, its main focus is on scaling up its operations.

Here is how we see EMD’s “franchise” model playing out:

We have Invested in EMD to see it not only become the market leader in the Australian psychedelics care, but build a monopoly on delivering these services.

At the same time, we recognise that there is no guarantee of success here, this is small cap investing and there are risks involved.

We think EMD has a very defensible market position because it has:

- Authorisation from the TGA to deliver MDMA-assisted care to patients (this is not easy to get)

- A Payer Agreement with Medibank to cover the cost of these therapies to its members (years in the making).

- Data that shows it works and continues to work months after the patient is treated.

- A means to deliver therapies through physical clinics that it owns and operates (EMD is now looking to expand its footprint by licensing hospital space).

- Scale potential with an approved protocol from the TGA that it can “franchise” out to other clinics looking to deliver assisted therapies.

As at the end of last quarter EMD had a cash balance of ~$3.5M, with a further $1.1M due to come in following completion of Tranche 2 of the recent placement.

EMD is currently capped at ~$25M.

Our Big Bet for EMD is that it can roll out its services to as many clinics as possible, reaching more and more potential patients to treat with mental health...

This first deal with Avive Health delivers on that rollout promise.

Our Big Bet for EMD

“EMD re-rates to a +$300M market cap by making a breakthrough with one or more of its clinical trial programs (MDMA, psilocybin, ketamine, CBD) while rapidly growing the footprint of its mental health treatment clinics.”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including execution risk, regulatory risk and funding risk - just some of which we list in our EMD Investment Memo.

In the rest of today’s note we will cover:

- EMD’s team to scale a clinic business, with Chairman Greg Hutchinson

- How does EMD go about “scaling up” its business model?

- EMD share register getting cleaning up, with big trading volumes in the last few weeks

- What’s next for EMD?

- What are the risks?

Emyria

ASX:EMD

EMD’s Chairman Greg Hutchinson knows how to scale a business from his time at Sonic Health

Leading the charge for EMD is its Chairman Greg Hutchinson.

If anyone knows how to rollout clinics fast, it’s Greg.

He led the scale up of Sonic HealthPlus to over 7,000 active clients across 40 different clinic locations.

Sonic HealthPlus is now the largest provider of occupational and community medical services in Australia...

... The parent company Sonic Healthcare is now capped at ~A$12.75BN.

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

EMD is looking to replicate the same playbook.

Carve out a clinical niche, scale up operations, and build a defensible business.

In a recent letter to shareholders EMD’s chief scientist Dr. Michael Winlo wrote:

“While many international care teams have been stalled, waiting for FDA approvals or policy changes, we are privileged to be operating within Australia’s established legal pathways.”

While others debate protocol designs, we are actively evolving and measuring care models, responding to patient needs, working with payers, and generating the kind of data that clinical trials won’t capture for years.

Our program is not theoretical. It’s real, it’s working, and it’s being watched”.

This quote comes after EMD’s Michael Winlo was the marquee speaker at the largest Psychedelics Conference in the US.

(and EMD was clearly one of the most advanced companies in the space)

You can read the full letter to EMD shareholders here:

(Source)

How does EMD deliver on its “scale up” business model?

EMD’s potential to earn revenues is only limited by its ability to scale up its services because it already has a “payer” in place.

The key limiting factors are:

- Access to sites

- Access to medical grade product

- More trained physicians to deliver the treatment

- More payers

THEN, EMD can replicate this business model with a bunch of other mental health conditions.

Right now EMD is treating PTSD with MDMA, but they could also go after treatment resistant depression, panic disorder, anxiety, etc...

How does EMD get more access to sites?

Each new site for EMD is a new opportunity to deliver therapies and scale up its operations.

EMD licenses rooms from existing hospitals or clinics, which reduces the operational cost for leasing and fitting out an entire building.

The vision is that many hospitals and clinics around Australia will have a mini EMPAX Centre.

(EMPAX is the name of EMD’s therapy brand).

So far EMD has its own EMPAX Centre headquartered in Perth.

In April, the company opened a second EMPAX Centre within the Perth Clinic, scaling up its operations by 50%:

(Source)

The deal announced with Avive Health is EMD’s third EMPAX Centre.

As we mentioned earlier, EMD now has access to patients in Brisbane, and the opportunity to expand into Victoria and South Australia.

The reason this rollout is happening fast is so that EMD can service the thousands of Medibank clients potentially eligible for EMD’s therapy.

You can watch this video that gives an insight into the Avive Health clinics:

How does EMD secure more medical grade products?

Getting its hands on more products is important for EMD to deliver more therapy.

MDMA and other psychedelics are controlled substances, and securing them from overseas may take time and cost more money.

However, since Australia downscheduled psychedelics in 2023, many companies have been looking to manufacture ‘medical grade’ products here in Australia.

Last week the AFR reported that an Australian-based company called Cortex completed its first production run of 10,000 capsules of medicinal MDMA in Australia.

This is the world's largest single batch of high-quality therapeutic MDMA ever.

Until now, the majority of medicinal MDMA has been produced overseas.

And we think that these new domestic manufacturing capabilities are good news for EMD as it looks to deliver more services to more people.

How does EMD train more physicians with Authorised Prescriber Status?

Authorised Prescriber status is what is needed for any organisation or individual to administer psychedelic assisted therapy in Australia.

It is granted by the TGA and not easy to get.

Right now we know that EMD has at least one physician with AP status for MDMA therapy (this basically gives regulatory permission to deliver its therapy).

Getting AP Status requires multiple submissions to the TGA, ethics approval, a tried and tested protocol for therapy delivery and strict guidelines on how the treatment can be administered.

BUT now that EMD has AP Status, it is able to pass this on to other clinicians through a supervised therapy of its approved protocol.

This enables EMD to “franchise out” its therapy method to other clinicians around Australia.

Any clinicians that want to work in this space or get listed as AP Status may find it easier to use EMD’s licenced “blueprint” rather than run a clinical trial themselves.

It is still unclear how many physicians have been trained on EMD’s protocol, however, according to the AFR article above there are “only 20 to 30 physicians [in Australia] that can prescribe the treatment”.

We suspect quite a number of those would be trained under EMD’s protocol.

Can EMD target new conditions?

It was mentioned in yesterday’s announcement that EMD would be able to deliver care for “treatment-resistent mental conditions”.

(Source)

While the Medibank funding right now is just for PTSD, we want to see it expanded to conditions like treatment-resistant depression.

Right now EMD is just targeting a fraction of the mental health disorders that could benefit from psychedelic treatment.

EMD has all the right pieces in place to scale up its operations, now it is on the team to go and execute on this business model.

In summary, we think that EMD could be big winners in this space because:

- EMD has a commercialisation deal with Australia’s largest private health insurance company Medibank

- EMD has AP Status from the TGA (Australia’s FDA) to deliver MDMA-assisted therapies

- EMD has the means to deliver its care through its physical clinics, and is growing its footprint nationally

- EMD’s Chairman Greg Hutchinson has scaled up a clinic based business before with ~$13B capped Sonic Healthcare

- EMD has the ability to expand into different mental health conditions, and different drugs, and is looking into this right now.

Of course there is a long way to go and it is all in the execution. There’s plenty of risks involved which we go into detail below.

EMD share register appears to be getting cleaned up, big trading volumes in the last few weeks

For any small cap stock looking to re-rate its share price, trading volumes are very important.

High volumes indicate that new shareholders are coming into the story and allows old shareholders to sell out their positions without damaging the share price.

Since the Medibank deal, EMD has turned over ~150M shares which is around 25% of the share register and more volume than the entire previous 12 months.

EMD also announced that it would clear around 12M shares of “unmarketable parcels” for small shareholders with holdings less than $500.

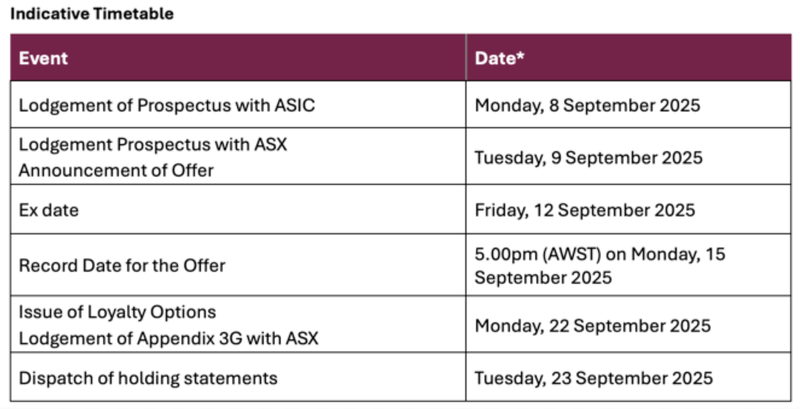

This is important because it just announced a “free” bonus option for shareholders that hold shares in EMD on the 15th of September.

This bonus loyalty option is exercisable at $0.05 and provided on a 1 for 4 basis.

Here is the timeframe:

(Source)

The extended timeframe on record date for the offer means that there are plenty of opportunities for shareholders to buy into the story before then.

What’s next for EMD?

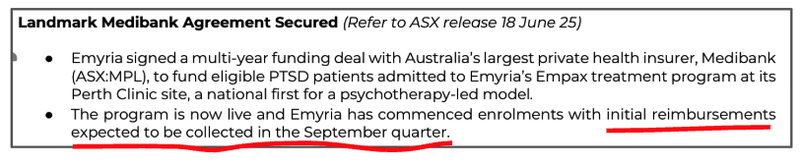

First revenues from Medibank deal

According to EMD’s quarterly report, the company has said that first revenues from the Medibank deal will be booked in the following quarter.

(Source)

Our expectations are relatively low here because EMD is yet to scale up its operations, and it is revenues from just two sites...

But it is a big milestone all the same.

More new sites opened

Now that EMD has signed on with Avive Health we want to see other potential sites that it can scale up its clinics to.

Expand care offering to new indications and/or new drug therapies

We want to see EMD expand its assisted therapy programs to psilocybin and ketamine, also for different mental health conditions like anxiety, treatment resistant depression etc...

More payers

We want to see if EMD is able to secure another payer alongside Meidbank.

What are the risks?

Regulatory Risk

EMD is working in a heavily regulated space.

The regulatory changes that allow EMD to operate in the field of psychedelic therapies are new and could be reversed. A regulator could step in and intervene either across the industry or specifically in relation to EMD.

Scale Up Risks

Even though EMD can secure funding for Medibank, there is a lot that needs to go right in terms of scale.

This includes securing more sites to operate its services as well as securing more MDMA supply to meet the expected demand.

Scaling costs money, and EMD needs to reach a level of profitability before it can scale without continuing to tap the market for resources.

Other Risks

The company’s expansion is also limited by the small number of doctors with Authorised Prescriber (AP) status for MDMA-assisted therapy. Training and credentialing additional clinicians is essential but not guaranteed to scale quickly.

Financially, EMD remains early-stage with ~$4.6M cash balance and a market cap of just $25M.

Although Medibank is covering treatment costs for its members, EMD is heavily reliant on this single payer. Any change to the Medibank agreement, or a slower-than-expected patient ramp-up at new sites like Avive Health Brisbane, could strain cash flow and potentially require further capital raises, leading to dilution of existing shareholders.

Operationally, the company has yet to prove it can deliver therapies at scale.

Treatment throughput per clinic remains unclear, and access to medical-grade MDMA and other psychedelics is still subject to supply chain risks, despite domestic manufacturing starting to come online.

EMD’s growth plan also depends on rolling out its EMPAX clinic model nationally, which requires securing additional sites, training staff, and maintaining quality and compliance at every location.

In short, while EMD is well-positioned with a first-mover advantage, its success hinges on execution.

Our EMD Investment Memo

You can read our RML Investment Memo in the link below.

We use this memo to track the progress of all our Investments over time.

Our EMD Investment Memo covers:

- What does EMD do?

- The macro theme for EMD

- Our EMD Big Bet

- What we want to see EMD achieve

- Why we are Invested in EMD

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.