EMD: Medibank agrees to fund EMD’s MDMA-assisted therapies

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 15,888,332 EMD Shares and 5,822,221 EMD Options and Company’s staff own 561,667 and 138,889 Options at the time of publishing this article. The Company has been engaged by EMD to share our commentary on the progress of our Investment in EMD over time. (6,250,000 shares and 2,083,333 options are subject to shareholder approval)

Emyria (ASX:EMD) has just announced a world first...

An agreement with a major insurance company to fully fund its members to use EMD’s “psychedelics for mental health” treatment.

The largest private health insurance company in Australia, Medibank.

Medibank will cover all the costs of EMD’s psychiatrist-led PTSD therapies for any of its eligible ~4M members...

This is around $30,000 per patient for EMD’s treatment.

...and is uncapped for the number of medibanks members to use it.

Mental health is the new global crisis, and existing treatments are not working - but there is very promising data from psychedelic assisted therapy.

And (surprisingly) Australia is leading the charge in this space.

In 2023 Australia was the first country in the world to legalise the use of psychedelics to treat mental health.

In 2024 EMD was the first company in the world to use psychedelics (MDMA) to treat a patient in a commercial clinic setting under these regulations.

Today, Medibank is the first insurance company in the world to offer fully funded psychedelics for mental health treatments to its members, through its deal with our Investment EMD:

(Read today’s EMD announcement here)

A major insurance company funding EMD’s treatment for its 4.2 million members is a major milestone.

It essentially opens up EMD’s pathway to revenue and expansion.

And interest from other major insurance companies...

And most importantly EMD’s model to be expanded globally as other countries start to legalise psychedelics for treating mental health.

(especially into the USA which is warming up to the idea)

To execute expansion plans, in January this year EMD appointed Greg Hutchinson as Executive Chairman.

Greg led the scale up of Sonic HealthPlus to over 7,000 active clients across 40 different clinic locations.

Last year Greg put $1M into EMD’s capital raise at 3.5c per share (we participated too, just not for as much as Greg did).

EMD is capped at just $16M post raise with ~$5.7M in the bank.

We have not sold a single share since we first initiated coverage on EMD in 2023

(our Initial Entry Price was 7.5c - currently trading at around 3c)

And we have just increased our position.

We now want to see EMD announce the first customers paid for by Medibank.

We also want to see new clinics get opened and secure the drug supply EMD needs to deliver its therapies.

(maybe even another insurance company will sign on now that Medibank has led the charge?)

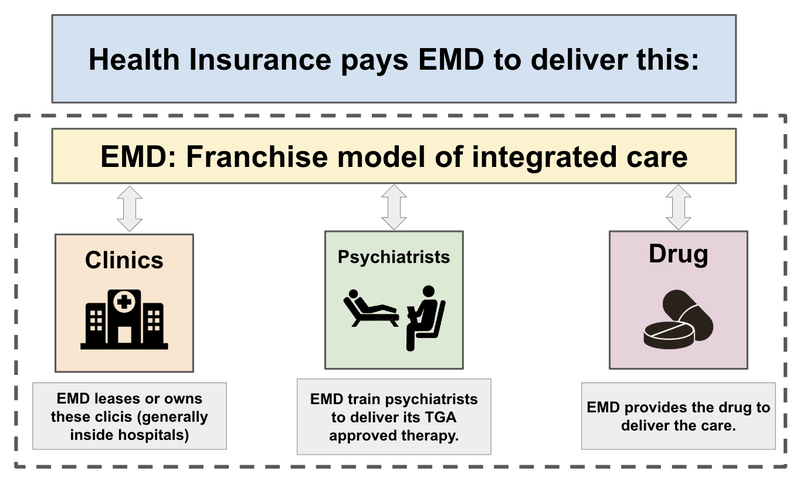

EMD offers psychedelic therapy for those with mental health conditions, in commercial clinics.

Like you would go to a physio, dentist, optometrist etc

EMD has developed an integrated care model, which means that it owns the clinics, contracts the physicians, provides the MDMA and has the (hard to get) licence to do all of this.

In summary:

- EMD has a commercialisation deal with Australia’s largest private health insurance company Medibank

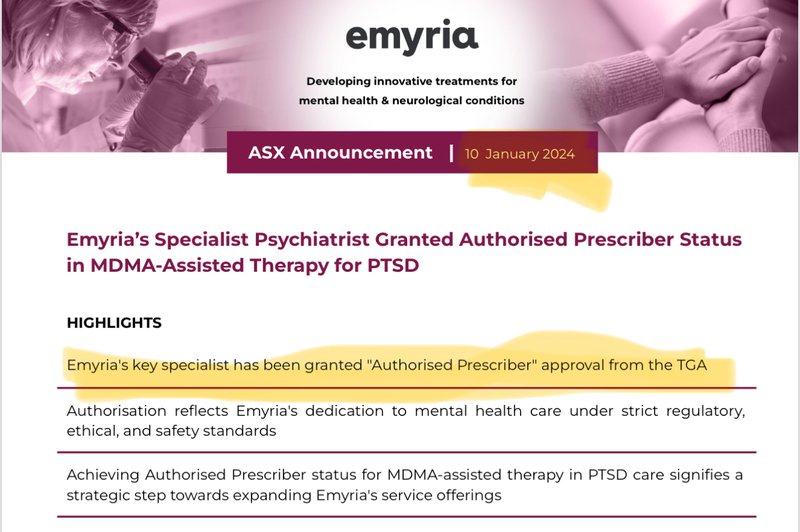

- EMD has Authorised Prescriber Status from the TGA (Australia’s FDA) to deliver MDMA-assisted therapies

- Australia is leading the charge globally in new age treatments for mental health

- EMD has published clinical data that shows its treatment works

- EMD has the means to deliver its care through its physical clinics

- EMD’s Chairman Greg Hutchinson has scaled up a clinic based business before with ~$13B capped Sonic Healthcare

- EMD has the opportunity to expand into the US

- EMD has the ability to expand into different mental health conditions, and different drugs

Today, EMD signed a major commercial payer deal with Medibank...

The largest private health insurance company in Australia.

A payer deal means Medibank will cover all the costs of EMD’s psychiatrist-led PTSD therapies for any of its eligible ~4M members...

In April the Herald Sun published an article that announced that Medibank’s move into the Mental Health space:

The deal with EMD would see Medibank cover ~$20,000 to $30,000 per patient per year.

Within Australia there are over 800,000 adults eligible for MDMA assisted therapy due to chronic or severe PTSD.

The size of the mental health care market in Australia is around ~A$36B according to EMD, and this deal is just the beginning.

In the US this issue is even bigger.

And recent commentary from the US FDA indicates that the country is ready to support psychedelics for mental health.

But Australia is leading the way here, and that is where EMD is validating its business model.

In 2023 Australia’s drug regulator, the TGA, legalised the use of MDMA, ketamine and psilocybin for medical use in therapy.

At the time these laws were “revolutionary” and made Australia a pioneer in this space.

This meant that any person or organisation with “authorised prescriber status” could administer therapies with psychedelic treatment.

EMD has this status (and it wasn’t easy to get).

Now that the company has a “payer” - someone to fund these treatments - it can focus all of its attention on scaling up its operations to deliver the service.

Here is how we see EMD’s franchise model playing out:

We are backing EMD to become the market leader in the Australian psychedelics care market because it has:

- Authorisation from the TGA to deliver MDMA-assisted care to patients (this is not easy to get)

- A Payer Agreement with Medibank to cover the cost of these therapies to its members (years in the making).

- Data that shows it works and continues to work months after the patient is treated.

- A means to deliver therapies through physical clinics that it owns and operates (EMD is now looking to expand its footprint by licensing hospital space).

- Scale potential with an approved protocol from the TGA that it can “franchise” out to other clinics looking to deliver assisted therapies.

The Big Bet for EMD is now all about rolling out as many clinics as possible, reaching more and more potential PTSD patients...

This is where EMD’s Chairman Greg Hutchinson comes into play.

If anyone knows how to rollout clinics fast, it’s Greg.

He led the scale up of Sonic HealthPlus to over 7,000 active clients across 40 different clinic locations.

Since them, Sonic HealthPlus is now the largest provider of occupational and community medical services in Australia...

... The parent company Sonic Healthcare is now capped at ~A$12.75BN.

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

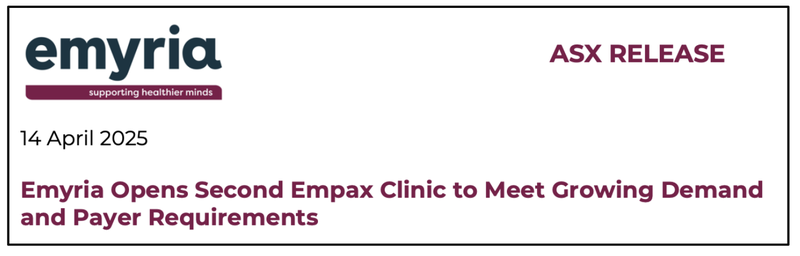

Since Greg came on board EMD has already increased its clinical capacity by over 50%.

EMD did this by leasing space in the Perth Clinic hospital - allowing the company to open more sites without a big capital outlay.

EMD mentioned in the announcement that it is close to securing “multiple East Coast sites”, we see this as a big part of the company’s scale up efforts:

(Source)

There are very few ASX-listed companies leveraged to the psychedelic space, and we think that EMD is primed to take advantage.

In today’s note we will cover:

- The 8 reasons why we Increased our Investment in EMD

- How EMD became one of the only companies to get permission to deliver MDMA-assisted therapy in Australia

- EMD’s data, which shows 50% improvement in quality of life for people with PTSD

- What success would look like for EMD

We will also release our new EMD Investment Memo which covers:

- What does EMD do?

- The macro theme for EMD?

- Our EMD Big Bet

- What we want to see EMD achieve

- Why we are Invested in EMD

- The key risks to our Investment Thesis

- Our Investment Plan

The 8 Reasons We Increased Our Investment in EMD

1. EMD now has a commercialisation deal with Australia’s largest private health insurance company Medibank

EMD signed a 2-year deal with Medibank, Australia’s largest private health insurance company.

This deal means that Medibank will fund the full costs of any eligible members who utilise EMD’s PTSD care programs.

The deal will see EMD cover around $30,000 per patient, per year, and underpins EMD’s ambition to scale up its mental health platform nationally.

(Source)

2. EMD has Authorised Prescriber Status (approvals) from the TGA to deliver MDMA-assisted therapies

Authorised Prescriber status is what is needed for any organisation or individual to administer psychedelic assisted therapy.

It is not easy to get and requires multiple submissions to the TGA, ethics approval, a tried and tested protocol for therapy delivery and strict guidelines on how the treatment can be administered.

This status provides a significant regulatory advantage to EMD compared to anyone else trying to enter the space.

(Source)

3. Australia is leading the charge globally in new age treatments for mental health

In 2023 Australia’s drug regulator, the TGA, announced the legalisation of various controlled substances for medical use in therapy.

This was a world first.

This provides the perfect regulatory environment for a company like EMD to develop and validate its business model.

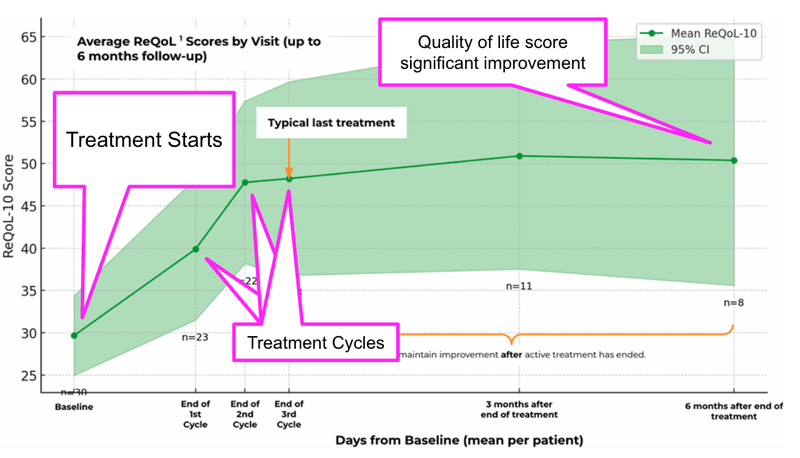

4. EMD has published clinical data that shows its treatment works

In 2023 EMD launched a clinical trial for MDMA-assisted therapy.

From that study EMD was able to show that its treatment reduces PTSD symptoms by more than 50%.

And patients continued to improve six months after the assisted therapy was complete.

(Source)

5. EMD has the means to deliver its care through its physical clinics

As part of EMD’s integrated care model, EMD needs to provide access to physical sites for its physicians to undertake EMD’s approved therapy.

Right now EMD owns and operates the Empax Centre in Perth.

But EMD has also been able to open up satellite centres within hospitals expanding its capacity into the Perth Clinic.

EMD is in discussion to launch these satellite sites on the East Coast, which will provide the means for EMD to expand nationally.

While EMD will set up some core sites that it owns, it can also lease these sites from different hospitals.

6. EMD’s Chairman Greg Hutchinson has scaled up clinics before with ~$13B-capped Sonic Healthcare

EMD’s Chairman Greg Hutchinson led the scale up of Sonic HealthPlus to over 7,000 active clients across 40 different clinic locations.

Sonic HealthPlus is now the largest provider of occupational and community medical services in Australia...

If there is anyone that is able to deliver the “scale up” business model for EMD, it's the Chairman, Greg Hutchinson.

(At EMD’s 3.5 cent placement in November last year Greg put in $1M, at the most recent placement at 2.5 cents, Greg put in $197k).

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

7. EMD has the opportunity to move into the US

As EMD is able to scale up its business and secure more payer agreements, we think this will create a significant moat around the business.

We think that if it is able to validate its business here in Australia, it could potentially take that business model and replicate it in the US.

~24M people suffer from PTSD in the US.

The cost of PTSD-related anxiety disorders is more than US$42.3 billion annually in the US.

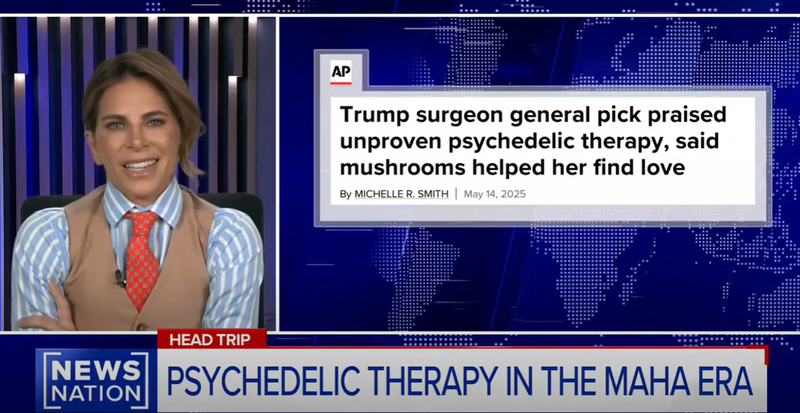

And the FDA commissioner recently said on News Nation that research on psychedelic treatment is a “Top Priority” for the organisation.

This actually provides an advantage for EMD, as it is able to accelerate its business here in Australia, while potential competitors in the US are in limbo waiting on the regulatory environment to change.

By that time we hope that EMD is seen as a powerhouse in the industry and can transfer all of its learnings overseas.

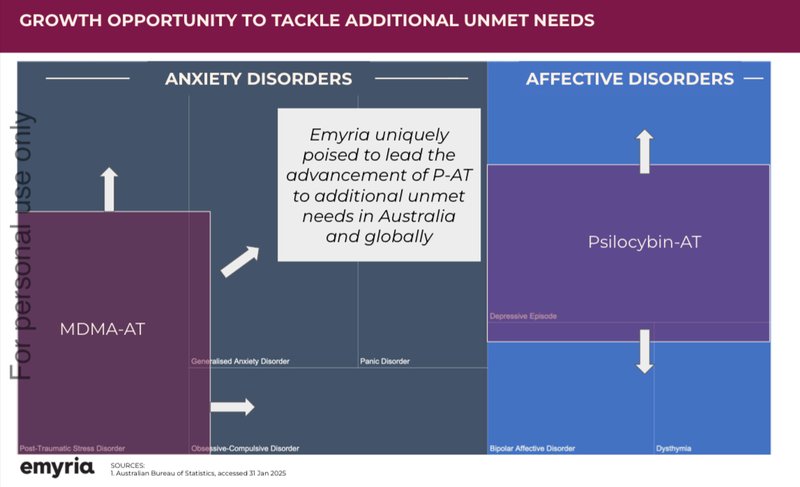

8. EMD has the ability to expand into different mental health conditions, and different drugs

While EMD is currently focused on MDMA assisted therapy for PTSD the company also has the opportunity to target different drugs (like psilocybin and ketamine).

AND eventually start treating different disorders like treatment resistant depression, parkinson's disease and Bipolar disorder.

As more therapies are developed in the pipeline, EMD will be able to offer patients are broader range of care and target different markets.

(Source)

A History: How EMD became one of the only companies to get permission to deliver MDMA-assisted therapy in the world

In 2023 Australia’s drug regulator, the TGA, announced the down-scheduling of controlled substances for medical use in therapy.

At the time these laws were “revolutionary” and Australia is seen as a pioneer in this space.

Practically, this meant that any physicians with “authorised prescriber status” (AP Status) would be able to deliver assisted therapies using illicit substances... and make money doing so.

AP Status was reserved for clinicians that were experts at delivering psychedelic-assisted treatments, and very hard to achieve.

The catch?

There weren’t any ‘experts’ in the field because up until now the provision of this kind of therapy was illegal.

So, clinicians needed to run a clinical trial in order to build up the skills and treatment protocol to secure AP Status from the TGA.

In 2023 EMD launched a 72-patient open label clinical trial.

During this trial EMD was able to secure AP Status for its head clinician.

Now that EMD has AP Status, it is able to pass this on to other clinicians through a supervised therapy of its approved protocol.

This enables EMD to “franchise out” its therapy method to other clinicians around Australia.

Getting to Authorised Prescriber Status is no easy task...

It requires multiple submissions to the TGA, ethics approval, a tried and tested protocol for therapy delivery and strict guidelines on how the treatment can be administered.

Any clinicians that want to work in this space or get listed as AP Status may find it easier to use EMD’s licenced “blueprint” rather than run a clinical trial themselves.

EMD now has the licence, but who is going to fund all of that treatment?

EMD has published data showing that its treatment is incredibly effective

In 2023 EMD launched a clinical trial for MDMA-assisted therapy.

The goal of the trial was:

- To show that EMD’s therapy works

- To secure authorised prescriber status for its clinicians

- To secure a payer agreement

With the news today, EMD has achieved all three objectives from its clinical trial.

Earlier this year EMD published data that showed its treatment reduces PTSD symptoms by more than 50%.

And patients continued to improve six months after the assisted therapy was complete.

63% of patients no longer met the PTSD criteria, with symptoms dropping 55.5% on average:

Here is the data that also shows quality of life improvements by more than twice, again, improving six months after the treatment is complete:

EMD will continue to collect data in its open label clinical trial, however the trial has effectively “done its job” to secure AP Status and secure a payer agreement.

We expect EMD to shift away from the trial to focus on scaling up the commercial delivery of its services to Medibank members.

What does success look like for EMD?

If EMD is able to scale up its business and secure more payer agreements, we think this will create a significant moat around the business.

An economic moat is a competitive advantage that a company possesses which is very difficult to copy or replicate.

The moat that EMD possesses is its access to clinics, payer agreement with Medibank, the data from its therapy and its Authorised Prescriber status in Australia.

(the more stakeholders in the business model, the stronger the moat is for the company that can actually pull it all together).

Now that EMD has the first mover advantage, it can scale up and secure the lion's share of the market for this emerging industry in Australia.

Remember, the TGA only downscheduled the controlled substances in 2023...

No one is doing treatments at a big scale... except EMD.

If EMD proves its business model here in Australia, we think that it could even take this to the US.

Recently, the FDA commissioner said on News Nation that research on psychedelic treatment is a “Top Priority” for the organisation:

It’s a big shift for the FDA that less than a year ago rejected Lykos Therapeutics' application for approval of its MDMA-assisted therapy.

This could pave the way for EMD to enter the US from a position of incredible strength, if it is able to prove out its business model in the smaller market here in Australia.

EMD Investment Memo 2

Date Published: 18th-June-2025

Shares Held: 15,888,332

Options Held: 5,822,221

What does EMD do?

Emyria (ASX:EMD) is an integrated clinical drug development and care delivery company.

The primary area of focus is on psychedelic assisted therapies on PTSD using MDMA.

What is the macro theme behind EMD?

We think psychedelic assisted therapy and psychedelic clinical trials have the potential to reshape care and treatments for difficult to treat neuropsychiatric disorders such as complex trauma, depression, anxiety, chronic pain and Parkinson’s disease.

As more patients become aware of their options, and the regulatory environment eases, we think companies that can deliver these types of treatments, services and clinical trials will attract capital.

8 reasons why we are Invested in EMD

- EMD has a commercialisation deal with Australia’s largest private health insurance company Medibank

- EMD has Authorised Prescriber Status from the TGA to deliver MDMA-assisted therapies

- Australia is leading the charge globally in new age treatments for mental health

- EMD has published clinical data that shows its treatment works

- EMD has the means to deliver its care through its physical clinics

- EMD’s Chairman Greg Hutchinson has scaled up clinics before with ~$13B-capped Sonic Healthcare

- EMD has the opportunity to move into the US

- EMD has the ability to expand into different mental health conditions, and different drugs

Our Big Bet for EMD

“EMD re-rates to a +$300M market cap by making a breakthrough with one or more of its clinical trial programs (MDMA, psilocybin, ketamine, CBD) while rapidly growing the footprint of its mental health treatment clinics.”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our EMD Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

What do we want to see EMD achieve in the next 2 years

Objective #1: Scale up services to more sites

We want to see EMD partner with more hospitals and care centres to deliver its care offering.

Milestones

🔲 New site opened

🔲 New site opened

🔲 New site opened

Objective #2: Secure more payer agreements

Now that the company has secured a 2-year deal with Medibank, Australia’s largest private health insurance company, we want to see EMD secure more payer agreements.

Milestones

✅ Payer Agreement 1 - Medibank

🔲 Payer Agreement 2

🔲 Payer Agreement 3

Objective #3: Secure more MDMA

One of the big bottlenecks for EMD to deliver its care is the supply of medical grade MDMA. We want to see the company identify both short term and long term supply opportunities.

Milestones

🔲 Supply Agreement 1

🔲 Supply Agreement 2

🔲 Develop own MDMA-analogues for use in its own clinics

Objective #4: Expand care offering to new indications and/or new drug therapies

We want to see EMD expand its assisted therapy programs to psilocybin and ketamine, also for different mental health conditions like anxiety, treatment resistant depression etc...

Milestones

🔲 Commence clinical trial on ONE new indication or drug.

Key Risks for EMD

Regulatory Risk

EMD is working in a heavily regulated space.

The regulatory changes that allow EMD to operate in the field of psychedelic therapies are new and could be reversed. A regulator could step in and intervene either across the industry or specifically in relation to EMD.

Scale Up Risks

Even though EMD can secure funding for Medibank, there is a lot that needs to go right in terms of scale.

This includes securing more sites to operate its services as well as securing more MDMA supply to meet the expected demand.

Scaling costs money, and EMD needs to reach a level of profitability before it can scale without continuing to tap the market for resources.

Funding risk

Small caps often need to raise cash to fund their growth.

Whilst EMD is generating revenue now, it is still making a loss (it spends more cash than it brings in).

If EMD is unable to develop a self-sustaining business model with positive operating cash flow, this could force EMD to raise capital in the future, likely at a discount to market prices to secure funds.

Market risk

There is always the possibility that broader market sentiment gets worse and shares as a whole trade lower, taking EMD’s share price with it. Alternatively, there could be further sector specific pain ahead. For example, the biotech sector sells down.

What is our investment plan?

We have not sold a single share in EMD since we initiated coverage in 2023.

Our Investment Plan for EMD is to hold on to a majority of our position to see the company execute on its business strategy over the next two to three years.

If the company’s share price materially re-rates in the medium term due to the scale up efforts we may look to sell up to ~20% of our holding. See our general hold policy for more details.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.