EIQ Secures FDA Clearance - can now market and sell in the USA.

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 3,470,000 EIQ Shares and the Company’s staff own 140,000 EIQ shares at the time of publishing this article. The Company has been engaged by EIQ to share our commentary on the progress of our Investment in EIQ over time.

EchoIQ (ASX:EIQ) just secured FDA clearance for its AI-powered algorithm that helps detect heart diseases.

FDA clearance is a BIG milestone for any early stage life sciences company.

This means that EIQ can really start marketing and selling its product in the USA - generating revenues via hospitals and partners that use its technology.

EIQ is already in ‘advanced discussions with a range of US healthcare providers’ around potential uptake of its product.

We suspect FDA clearance is likely the trigger for those discussions to convert into actual deals.

EIQ has also just signed on a highly experienced new US based CEO to drive commercialisation of its product.

The stock is coming out of a trading halt today and it will be interesting to see how the market reacts to both pieces of news.

Securing FDA clearance to market and sell a product in the USA is a big de-risking event for biotech and medtech companies.

Larger institutional funds often wait for companies to secure these types of regulatory clearances before investing.

EIQ’s tech is an AI-powered diagnostics assistance tool that detects heart diseases better than standard clinical practice (it's demonstrated this in the clinic, which helped it get FDA clearance).

EIQ is targeting the US$144BN cardiovascular market in the US.

The particular condition where EIQ secured FDA clearance (aortic stenosis) costs the US healthcare system more than US$10BN each year.

With FDA clearance significantly de-risking the technology, EIQ has now firmly entered the commercialisation stage.

As we noted above, EIQ has already made progress on this front and is in “advanced discussions” with multiple large hospital groups, pharmaceutical companies and device manufacturers.

Now that FDA clearance has been granted, we think that at any time EIQ could announce that it has signed a new license agreement or partnered with a hospital.

These are catalysts that could re-rate the company significantly - particularly if EIQ is able to land a couple of big deals in quick succession.

EIQ has a great product, has proven its effectiveness in the clinic, is armed with FDA clearance and has already established inroads into the US healthcare market.

It is now over to new CEO Dustin Haines and the EIQ team to take the product and execute on the commercialisation strategy.

With FDA clearance now secured, we are hoping that EIQ can follow in the fortunes of one of the greatest ASX tech success stories of the last 10 years...

Before we tell you the story and show a pretty epic share price chart, we need to stress that it's very early days for EIQ.

There is no guarantee that EIQ will scale to such heights as you are about to see.

But even if it's just a fraction of this success, as long term Investors we will be pretty pleased.

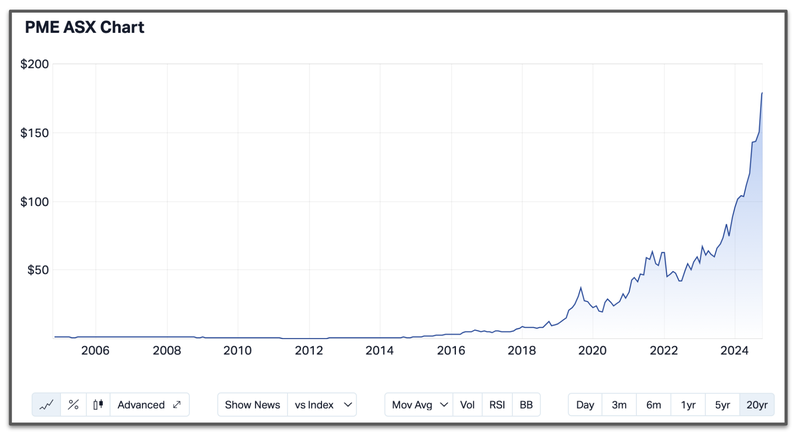

That ASX success story is the $18.7BN capped Pro Medicus - a company that delivers healthtech for the medical imaging sector.

Pro Medicus has developed a world leading diagnostics imaging technology.

The company grew by steadily grinding out recurring revenues over a 10+ year period, and catching two key macro waves at the right time - cloud-services and AI.

Demand for the cloud-based solution was instrumental in the company’s fortunes between 2019 and 2022 and since the AI run, Pro Medicus has grown to monumental heights given its leverage to the sector.

Over a nine year period between 2015 and today, Pro Medicus’ share price more than 100-bagged:

Past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

We are hoping that over the next three to five years EIQ can do something similar.

And FDA clearance is the key first step.

Like Pro Medicus, we want to see EIQ grow its revenues, sign more deals, increase market penetration for its technology and eventually build itself into a cash generating monster.

But again - market success is no guarantee for EIQ, and those epic results that Pro Medicus delivered for investors are rare events. Never risk more than you can afford to lose on the stock market.

While Pro Medicus is software for the medical imaging sector, EIQ is software specifically for cardiology (heart disease).

Although they are two distinct markets, what they have in common is that they are important tech solutions that plug into existing diagnostic workflows.

If EIQ is able to execute on its commercialisation strategy, we are hopeful that it could start to follow in the footsteps of Pro Medicus (even just a little bit would be a great result).

Or EIQ gets taken over for multiples of its current valuation...

While EIQ advances its commercial activities and we wait for the deals to start coming in, there is still another major catalyst on the horizon that we are looking forward to...

FDA clearance for heart failure.

Heart failure affects 65 million people worldwide and costs the US healthcare system US$70BN every year.

There is particularly strong demand for early stage diagnosis of heart failure because it is the number one cause of re-hospitalisation in the world.

This means it is more costly to the healthcare system if a person has to continually go back to hospital due to heart failure.

EIQ has published very promising clinical data around its heart failure AI algorithm.

EIQ has already started the process with the FDA to allow its solution to be marketed to and used by healthcare professionals in the USA as a decision support aid in the detection of heart failure.

Based on company timelines we would expect FDA clearance for market use on heart failure in less than 12 months.

So, while EIQ builds out its revenue from aortic stenosis, we can look forward to the next major catalyst of a second FDA clearance.

Two horses running at the same time.

Exactly the type of newsflow to keep investor attention, just in case the sales don’t come in quick enough.

And we all know from investing in small caps, that deals and also regulators can sometimes take just a little longer than we expect.

New CEO onboard to take EIQ to this next growth stage

EIQ has not wasted any time in securing a CEO to lead the commercialisation phase of the business.

Enter, new EIQ CEO Dustin Haines.

Haines is well integrated into the US healthcare system with over 25 years of experience.

He is the former VP & General Manager of $105BN capped Gilead Sciences and has had senior roles at GSK and ViiV Healthcare Haines.

Haines has a track record of driving revenue growth - in particular through product reimbursement.

(More on why this is important in a bit).

With FDA clearance secured, it is now over to Dustin Haines to take the EIQ product and execute on the commercialisation strategy.

This brings us to our Big Bet:

Our EIQ ‘Big Bet’:

“EIQ re-rates to a >$1BN market cap on successful commercialisation of its heart disease detection technology and/or an acquisition at a multiple of our Initial Entry price.

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of wFhich we list in our EIQ Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

FDA clearance unlocks commercialisation, what does this actually mean?

We have spoken about how FDA approval unlocks commercialisation for EIQ, particularly in our last note on EIQ which you can read here.

... but what does this actually mean?

Before we get there, a quick reminder on what EIQ’s product is:

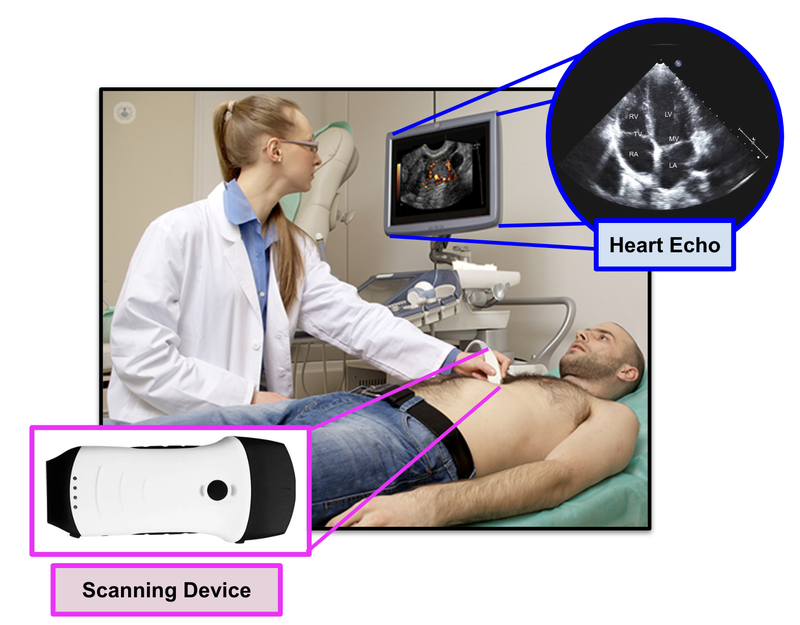

EIQ’s product EchoSolvTM is a machine learning AI-based decision support software that, when used together with a cardiologist, is able to detect heart diseases at a much better rate.

Cardiologists are specially trained doctors that are able to interpret heart conditions from 2D images that are presented from an ultrasound (known as an echo):

EIQ’s EchoSolv product can provide an actual 3D interpreted image of the heart, and provides assistance to the cardiologist in detecting heart related issues.

You can check out a short video overview of how the technology works here:

https://www.youtube.com/watch?v=N7s3I1-fJQY

So how does EIQ make money?

The economics and value transfer is a little bit different when it comes to healthcare...so bear with us.

But as a tech product, it is important to understand that EIQ effectively has a 100% gross margin on any “sales” made.

“Sales” are not made in the traditional sense, but rather sales are done through customers using the product (either hospitals or licensing partners).

Let us explain the two key commercialisation strategies EIQ is pursuing.

First, reimbursement

Private insurance companies or public health programs will reimburse healthcare providers (like hospitals) that use EIQ’s product.

This is done through a reimbursement scheme, and EIQ will get a %.

Whenever EIQ’s product is used by a hospital the cost is not paid by the patient, but rather the health insurance pays the hospital and EIQ splits the revenue.

Think of this like a “sale”.

In order for EIQ to be eligible for payment it needed to secure FDA clearance ( ) and a reimbursement code ( ).

And to make more “sales” EIQ needs more uptake of its product.

These are the two key things we are looking for:

- Reimbursement code for EIQ

- More hospital uptake of the AI Algorithm

Hospitals are notoriously slow movers when it comes to changing behaviour.

However, EIQ is already in “advanced discussions” with several US hospitals.

We are hoping that current EIQ Chief Commercialisation Officer Deon Styrdom and eventually new CEO Dustin Haines (when he starts) will be able to deliver some key partnerships to prove uptake of that product.

Currently, EIQ is using a ‘try before you buy’ model.

This means offering the EchoSolv product for free, so that cardiologists can grow accustomed to using it...

And then once the reimbursement code kicks in, EIQ will be able to make money from insurance companies using it.

Deon covers this in more detail in this video at 38:40.

The key takeaway is more hospitals = more sales.

EIQ is effectively looking to partner with more and more hospitals.

More hospitals (that use the product) = more sales.

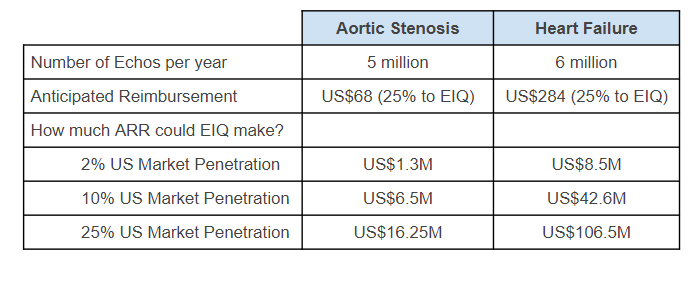

If EIQ is able to capture just 25% of the US healthcare market it could be worth up to US$16.25M per year.

The numbers look even better when you look at heart failure, but EIQ will need to secure FDA clearance for that disease first.

Second, licensing.

EIQ’s second commercialisation strategy is to secure licensing partnerships with various organisations that provide services to patients with heart issues.

Organisations like medical device manufacturers and big pharma companies make sales by selling products to patients with heart issues.

Sales are driven by identifying people with heart issues.

More people identified = more sales for the company.

If EIQ is able to show that its AI algorithm is better at identifying patients with heart issues than these companies, it could potentially support an uplift in sales for the bigger company.

We think that EIQ will likely take a royalty on this uplift.

Again, new CEO Dustin Haines, ably supported by current Chief Commercialisation Officer Deon Styrdom, will lead the charge in terms of securing licensing deals.

EIQ says it is at advanced stages with pharma companies and device manufacturers.

These deals could be announced at any time, but with FDA clearance in hand we think that conversations will be accelerated.

What might happen to the share price?

Apart from the obvious benefits for EIQ’s commercialisation strategy, FDA clearance is also big on the corporate front.

FDA clearance is a big de-risking milestone for EIQ.

Without it, the company would have to go back and get more data before it can commercialise its product.

This risk for the aortic stenosis product is now gone.

This may be a “buy the rumour, sell the fact” scenario for EIQ, and there may be some selling - especially from speculative investors that may have been waiting a long time for this news...

But on the other hand...

Binary risks like FDA clearance typically sideline investors with much deeper pockets - like big institutional funds and family offices that are mandated to only invest in biotech/healthtech with no regulatory risk.

After yesterday’s news, we think EIQ is open to capital from that world of investors.

(it's a little different to the micro and small cap world we normally Invest in, with different drivers and capital allocation ideas)

From a share price perspective that could mean that there is a lot more buying in EIQ over the coming months as those new investors look to build a meaningful position in the company.

IF EIQ can deliver some quick wins (from a commercialisation perspective) it might even lead to some FOMO buying from those investors.

We have seen that sort of share price action immediately after FDA news before:

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Managers of big capital dont like binary risks BUT they are willing to miss out on the spike after a binary outcome comes in for a company and pay up after an announcement like EIQ’s today.

These funds are generally set up first to “not lose money” and then second to make returns.

Usually this risk management is part of their mandates.

(This quote is from the website of a private equity fund that targets EIQ type companies - we are not saying this fund does or will invest in EIQ, its merely an example of what certain funds can and can't invest in)

The risk-reward equation fits much better now for bigger funds as the risk moves from “Regulatory Risk” to “Commercialisation Risk”.

Bigger guys, with much more patient capital, prefer the commercialisation risks (which can take time) rather than the binary risks posed by FDA clearance.

What comes next?

Objective #2: Commercialise aortic stenosis product

We want to see EIQ make sales and grow its revenue for this product.

Milestones

Reimbursement approvals

First sales from aortic stenosis product

Deal with healthcare provider (Pharma company)

Licensing deal (medical device manufacturer/imaging company)

Source: “What do we expect EIQ to deliver” - EIQ Investment Memo 6 Sept 2024

EIQ mentioned in yesterday’s announcement that it was “advancing discussions with a number of parties including large hospital groups, device manufacturers and pharmaceutical companies” for its EchoSolv tech.

With FDA clearance secured, we are hoping EIQ can convert these negotiations into revenue generating agreements.

EIQ will also scale up work alongside its US consultancy to obtain reimbursement codes for users of EchoSolv under insurance.

This will create financial incentives for more widespread use of EchoSolv AS in US hospital settings on a fee-per-use basis.

At the same time we want to see EIQ make progress on the reimbursement code front.

A reimbursement code will be a game changer for EIQ because it will create “financial incentives for more widespread use of” EIQ’s tech in the US hospital setting.

What could go wrong?

For EIQ today marks a shift in the risk from “regulatory risk” to “commercialisation risk”.

Sales, particularly in the healthcare industry, take time.

If EIQ is not able to execute on its strategy, or sales are delayed and take longer than the market expects, then “commercialisation risk” could materialise for the company.

Sales/Commercialisation risk

EIQ is reliant on its partners, both under the licensing and reimbursement strategy, to use EIQ’s product. If EIQ’s product is not used (because it doesn’t add value back to the provider), then it won’t be able to generate revenue. There is no guarantee that EIQ’s product will be used by its partners and, therefore, no guarantee of revenue.

Source: “What could go wrong” - EIQ Investment Memo 6 Sept 2024

Our EIQ Investment Memo

In our EIQ Investment Memo, you can find the following:

- What does EIQ do?

- The macro theme for EIQ

- Our EIQ Big Bet

- What we want to see EIQ achieve

- Why we are Invested in EIQ

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.