EIQ - Is FDA approval imminent? What happens after that?

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 3,470,000 EIQ Shares and the Company’s staff own 140,000 EIQ shares at the time of publishing this article. The Company has been engaged by EIQ to share our commentary on the progress of our Investment in EIQ over time.

Diseases of the heart are the leading cause of death worldwide.

But diagnosis is complex - and delayed or missed diagnosis costs lives.

Echo IQ (ASX:EIQ) is a tech company that has a remarkably accurate AI based tool to detect heart diseases early.

Based on company timelines, FDA approval for its technology could happen any day now.

This is a significant share price catalyst that we are watching out for, as it can unlock commercialisation deals for the company.

While we wait for FDA approval news from the USA, we thought now is a good time to run through how EIQ can turn its tech product into a revenue generating success story over the coming years.

EIQ has exclusive commercial access to the world’s largest echo measurement database to train its AI model.

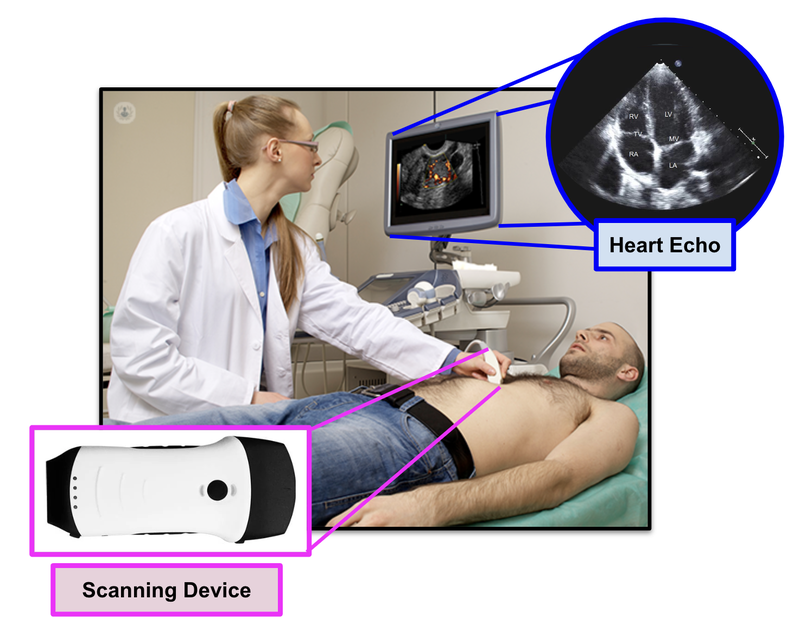

(Echocardiograms are ultrasounds that cardiologists use to get an image of your heart - an “echo” is the resulting image.)

EIQ has already demonstrated in the clinic that its technology is much more accurate than current detection methods.

EIQ has demonstrated this for two types of heart diseases - aortic stenosis and heart failure.

According to clinical trial data, EIQ’s technology has been shown to accurately identify 100% of severe aortic stenosis patients.

Also, it provides a 72% uplift in detection when the AI compares to the cardiologist “human only” method.

EIQ’s product for aortic stenosis is the one up for imminent FDA approval.

With an FDA approval, EIQ plans to sell its AI heart disease detection tool via a few well trodden paths for health technology companies:

- Reimbursement deals - hospitals or other places that deliver EIQ’s service get paid back by health insurance companies or government, or;

- Licensing deals - when for example, a Big Pharma or major medical supply company pays EIQ an (ideally) big upfront fee, then more on defined milestones.

As we noted above, EIQ is waiting on one key thing to begin commercialising its tool - FDA approval.

Based on company timelines, all signs are this news could be any day now.

This would be a major catalyst for EIQ - as FDA approval unlocks its pathways to revenues.

Today we will unpack what a successful FDA approval might look like for EIQ, and how EIQ can turn from a ‘pre revenue’ med-tech company into a ‘revenue generating’ med-tech company.

So, we are likely a few days away from a big inflection point for the company.

Below are the 5 key ways in which we think an FDA approval in the coming days could de-risk our Investment in EIQ and deliver a step change to the company’s valuation.

FDA approval for EIQ:

- allows it to start discussions with Reimbursement Authorities,

- increases the level of interest with the various licensing partners that the company has been engaging with,

- increases the likelihood of hospital uptake,

- supports future regulatory applications with other jurisdictions (like TGA in Australia or EMA in Europe), and;

- makes EIQ a far more attractive takeover target.

We will go through each of these in detail today, give you a taste of two cardiologist conferences we attended as part of our due diligence on EIQ before we Invested, and also address the ‘what happens if they don't get FDA approval’ risk for Investors such as ourselves.

Get comfy, as this is a longer note.

With a major catalyst on the horizon, we think it is a big year ahead for our latest Investment.

EIQ recently raised $7.1M at 15c per share, with a significant portion of funds going towards its commercialisation efforts.

(We Invested in this placement)

That raise amount should give EIQ an excellent runway to start making money if FDA approval is secured.

And that news could drop any day, so here’s a primer on what we’re looking out for and why.

FDA decision on aortic stenosis - due any day now

The type of heart disease that EIQ is awaiting FDA approval on imminently is aortic stenosis.

Aortic stenosis is a condition where the valve that controls blood flow from the heart to the body becomes too narrow, making it harder for the heart to pump blood.

There is a 50% mortality rate within 2 years if left untreated - so an early detection tool like EIQ’s, can be extremely valuable.

There are around 1.5 million people in the US that suffer from aortic stenosis.

The direct costs to the US healthcare system are currently US$10 billion per year.

Previously, EIQ has indicated that “a number of large US healthcare groups have indicated that FDA clearance would mark an important step in their consideration for deployment of the technology”. (Source)

We think this is in large part due to the US’s healthcare systems penchant for liability claims and lawsuits.

FDA approval effectively reduces this risk for major healthcare groups and gives EIQ the go-ahead to sell to these healthcare systems.

After aortic stenosis, next in EIQ’s ‘FDA approval pipeline’ will come heart failure - that's expected in about 12 months time - another future catalyst to look forward to for this stock, and it's an even bigger market.

EIQ’s two commercialisation strategies

FDA approval will unlock two different commercialisation strategies that the company is currently targeting to generate revenues from its product.

First, reimbursement.

In the US, whenever a hospital or other healthcare provider uses EIQ’s AI technology, the patient does not pay the full cost of the service.

The healthcare provider will charge a fee to either public health programs or private insurance companies through a reimbursement scheme.

EIQ intends to take a % of this fee.

Second, licensing.

EIQ may look to secure licensing deals with companies that have an interest in identifying more patients with heart issues.

Given the size of the market, we think there would be quite a few.

(We’ve seen it first hand, cardiology events are huge, we went to conferences in Perth and London)

Generally, these are organisations that provide treatments like medical device manufacturers and big pharma companies.

For these companies, more diagnosis = more sales.

Ultimately, FDA approval will be the key hurdle for EIQ to unlock these particular commercialisation opportunities, and we are expecting it any day now.

The 5 ways an FDA approval will help EIQ

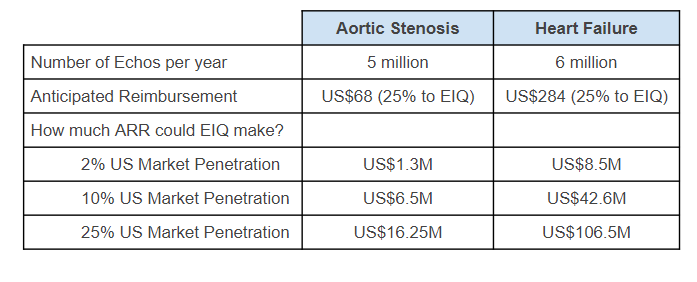

1. EIQ can advance discussions with Reimbursement Authorities

EIQ will be seeking to commercialise its aortic stenosis product through the US reimbursement pathway.

Essentially, healthcare providers that use AI algorithms like EIQ’s are able to secure reimbursement from insurance companies.

To receive this reimbursement, EIQ will need what's called a CMS code - which is administered by the Centers for Medicare & Medicaid Services (CMS) and allows this reimbursement to take place. (Source)

EIQ can establish this by ‘piggybacking’ off an existing reimbursement scheme and get a miscellaneous code.

Once EIQ is able to show adoption of its technology under the miscellaneous code it can seek a national reimbursement code.

Securing national reimbursement for EIQ’s technology would be a very big catalyst... but it needs to show that it is being utilised first.

It’s a little bit complicated but you can listen to Chief Commercial Officer Deon here in more detail in this video at 38:40. (We recommend watching this to get your head around it).

If FDA approval is granted, EIQ will be able to commence discussions with the Reimbursement Authorities, which is necessary for EIQ to pursue the reimbursement revenue pathway.

Here is what annual reimbursement revenues could look like for EIQ - for market penetrations less than 25%:

2. Increases the level of interest with the various partners that EIQ have engaged with.

EIQ’s second commercialisation strategy is to secure licensing partnerships with various organisations that provide services to patients with heart issues.

Organisations like medical device manufacturers and big pharma companies make sales by selling products to patients with heart issues.

Sales are driven by identifying people with heart issues.

More people identified = more sales for the company.

If EIQ is able to show that its AI algorithm is better at identifying patients with heart issues than these companies, it could potentially support an uplift in sales for the bigger company.

We think that EIQ will likely take a royalty on this uplift.

What sort of uplift could we see?

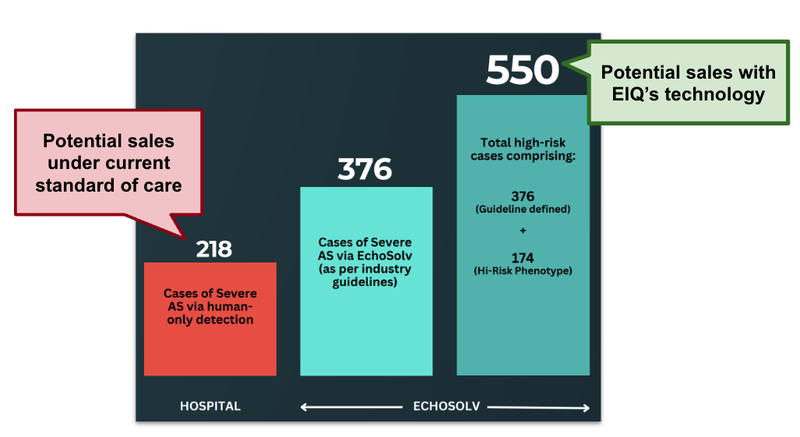

The data from EIQ aortic stenosis clinical trial with St. Vincent's Hospital showed a 72% increase in disease detection from over ~ 9,000 echos measured.

For companies that provide care to patients with heart issues, this is an extra 232 potential sales that they could make.

(Source)

In addition, we hope that EIQ is able to secure up-front payments for any licensing deals (as we’ve seen with other biotech companies in the past).

EIQ has already begun a “soft launch” of its product, putting it in the hands of potential licensing partners.

Although FDA approval is not entirely necessary to secure these deals, we think it will be a very big help and strong external validation for potential licensing partners to show interest in the product.

3. Increases likelihood of hospital uptake

The more hospitals that use EIQ’s product, the more reimbursement revenue it will get.

Think of this like market penetration.

If the FDA approves EIQ’s AI algorithm it will provide external validation for the product as safe and effective to use.

For hospitals and cardiologists that work there, they don’t have the time to independently evaluate every new technology that comes onto the market.

They rely on independent organisations like the FDA to verify the products that are safe and effective to use.

Which means that some (or many) may be waiting for the FDA approval before using EIQ’s product.

Hospitals are notoriously slow movers (and generally conservative by nature).

But, if EIQ can grow its network of hospital clients, we see this as a big positive, as revenue tends to be reliable and compounding given the “sticky” nature of the clients.

4. Supports future regulatory applications such as TGA

The FDA is like the “big boss battle” of medtech applications - other jurisdictions usually fall in line once it is granted.

If it’s good enough for the US, we’re hoping that additional jurisdictions and regulators also quickly embrace EIQ’s tech, leading to an even larger total addressable market (TAM).

When it comes to approvals for AI algorithms, the FDA is by far the most cooperative.

That’s why, the TGA in Australia and the EMA in Europe will generally follow suit but never lead the way.

5. EIQ becomes a far more attractive takeover target

We had a look for companies that work specifically in the cardiovascular/imaging/AI field and some of the valuations that are attached to these companies.

Clearly, some big money is heading towards this space:

Viz.ai - FDA-cleared algorithms to analyse medical imaging data, including CT scans, EKGs, echocardiograms etc., not yet listed - April 2022 valuation of US$1.2BN. (Source)

Arterys (acquired by Tempus) - medical imaging AI platform for radiology, post-money valuation of US$100-500M. (Source)

Caption Health (acquired by GE HealthCare) - cardiology ultrasound AI guidance tool, undisclosed value, potential valuation of US$127M. (Source)

What these examples point out to us, is that there is intense industry interest in AI into cardiology applications and disease detection that currently relies on human interpretation of 2D images.

And that’s the space that EIQ operates in.

What’s more, large healthcare companies are currently very acquisitive in this space and are willing to shell out large sums to secure the latest technology.

We think FDA approval will play a large role in any future appeal EIQ might have as a takeover target to much larger companies.

We got to see first hand how big the cardiology industry is, and get a sense for the amount of money involved, first hand when we attended two major cardiology conferences.

Here’s more on those experiences...

What we learned from attending two prominent cardiology conferences...

First in London

A few weeks ago, we attended the European Society of Cardiology Congress in London.

(We went to a major Perth cardiology conference prior to that - more on that below)

So this was our team's second trip to a cardiology conference to learn more about EIQ and its place in the wider industry.

More importantly, where it could go.

The ESC Cardiology Conference in London was massive, with over 24,000 industry stakeholders and all the big players in town.

It is the world’s preeminent forum for advancing cardiovascular research and treatment.

EIQ was specifically invited to participate in two ‘late-breaking science presentations, following peer review of its results for AI detection of heart failure.

Here’s EIQ’s Chief Research & Strategy Officer, Professor Geoff Strange, presenting the results:

After sitting in the sessions, one of the first things we noticed about this conference was its sheer scale.

All the heavy hitters were there from Big Pharma:

EIQ presented twice.

First, Professor Geoff Strange provided an overview of the technology and a high level overview of the results achieved so far.

After the presentation Geoff pointed out that listening to the presentation were senior members of the heart foundation and some known high-level executives at big pharma companies.

The room was packed, but more importantly, it was packed with the right audience.

Then, EIQ presented again later in the day in a more technical overview of the results.

This was the “late-breaking science” session we mentioned above - a special type of session reserved for the most well regarded and recent scientific breakthroughs in cardiology.

After the presentations we walked through the “digital health” wing of the conference.

There was an entire quarter of the conference dedicated to all of the digital advancements in cardiology, in particular AI diagnostics (where EIQ sits).

Larger players like Philips and GE HealthCare were presenting new hardware technology like portable, handheld echo machines.

These machines are getting smarter, cheaper and better... and eventually the vision is to have GPs use this technology to better identify heart conditions.

There are various companies like Butterfly or Clarious that are working on small portable echo machines that can be plugged into your phone:

Generally these devices use an AI to support the usability.

Whether it is used by a specialist or someone that is not trained.

Seeing all of the device manufacturers out there, we think that EIQ’s product goes very much hand in hand with these products, potentially as an acquisition target later down the line by a big pharma company in the space.

Also in Perth

We also attended the CSANZ cardiology conference in Perth in August:

There, we got some good insights into Australian cardiology research, and had a chance to spend more time with EIQ’s Professor Geoff Strange.

This is Professor Geoff Strange EIQ’s Chief Research & Strategy Officer presenting data from EIQ’s research program in Perth:

EIQ’s model is trained on an Australian echo database.

One consideration with EIQ is that perhaps different countries' populations could have different hearts or types of hearts, based on any number of factors.

However one of the big takeaways from that presentation was that EIQ’s Australian echo data does indeed match up well with American echo data.

Which is in our eyes, a good sign ahead of potential FDA approval.

Furthermore, what was clear from both of these conferences was that EIQ is at the forefront of innovation in the cardiology space - the calibre of people involved on the scientific advisory board speaks to this.

And these researchers and scientists will hopefully act as great ambassadors for EIQ’s products.

More and more companies are adopting AI tools to support detection of heart disease and technology is getting better and better.

It is an interesting time for the company as it secures the final regulatory approvals to take its product to market.

And the cardiology industry is a BIG market.

Just the type of market that we like to see targeted by our early stage tech companies.

What are EIQ’s chances of success with the FDA?

FDA approval is an extremely valuable breakthrough for early stage biotechs, medical tech and diagnostic tools.

So what are the chances that the FDA will actually approve EIQ’s tech into the giant US market?

To gauge that, we did some digging...

Although FDA approval is considered a binary outcome with investors, the first thing to understand is that EIQ’s product is not a drug which means:

- There is no nasty side effect profile to consider

- Nothing is physically entering a human body

Which we think makes it a “lower risk” approval for the FDA.

Secondly, recent approvals show that the FDA is very open to approving AI solutions, particularly when the results of EIQ’s study show that its algorithm significantly improves the accuracy of results.

In our view EIQ’s tech only helps, and “does no harm” - the classic Hippocratic oath that doctors historically swore to uphold when they entered medical practice. (Source)

Putting it all together, we think that EIQ is in with a strong chance of securing FDA approval because of:

- Recent trends in FDA approvals for AI algorithms.

- FDA likes AI in medical fields where where image interpretation is involved.

- EIQ has published very strong data.

If FDA approval is not granted it will likely be a setback for the company and more data will likely be needed for collection.

However, we think this is unlikely given the list of reasons above...

Let’s break it down.

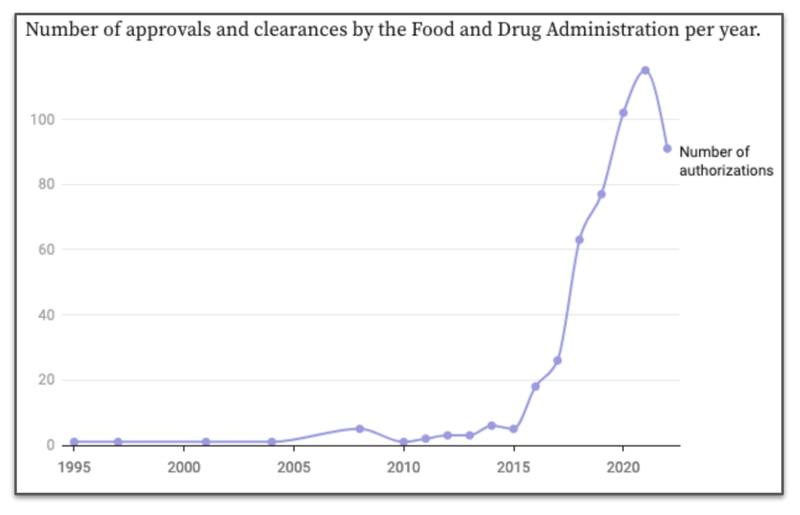

1. Recent trends in FDA approvals for AI algorithms

There have been some recent major changes to the FDA’s attitude towards approval for algorithm based tools that we think bode for EIQ and the industry it is working in.

Since 2015, approvals for AI algorithms have grown dramatically:

(Source)

We’re not too worried about that recent reduction - we attribute this more to a backlog in AI algorithm approvals that needed to be cleared by the regulator between 2015 and 2022.

We think many products would have been knocked back for a period of time, before the regulator changed its stance and became more comfortable with AI algorithms as they improved.

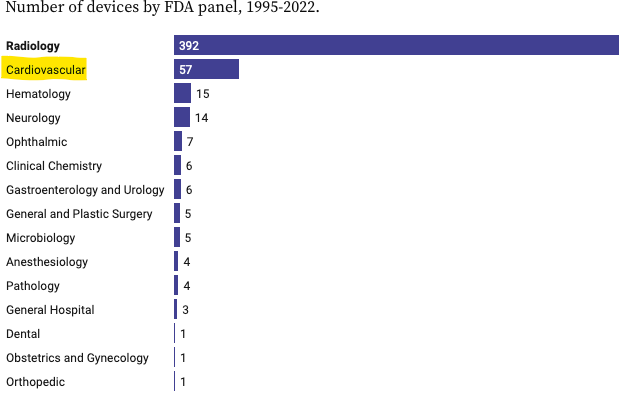

2. FDA likes AI in medical fields where where image interpretation is involved

The two key areas that the FDA is approving AI algorithms are in the radiology and cardiovascular industry.

(Source)

And this makes sense.

These two industries use “specialists looking at images” to diagnose conditions.

But detecting heart disease this way is a big challenge.

The current methods rely on a trained specialist visually interpreting 2D images produced by an ultrasound on your chest (known as an “echo”).

It's a bit like trying to drive with an eye patch on - depth is hard to grasp and you can make mistakes.

Effectively, cardiologists (as good as they are) are being asked to make diagnoses by building a 3D image of the heart in their head from these 2D images.

We think this is the perfect task to be helped by AI.

EIQ’s AI can provide an actual 3D interpreted image of the heart, which is an extremely complicated organ, and provides assistance to the cardiologist in detecting heart related issues.

As EIQ’s Professor Geoff Strange explains, “it's not about replacing the cardiologist, but rather providing assistance to busy workers that may need a second and objective opinion on interpreting the echograph”.

3. EIQ will present very strong data to the FDA.

According to clinical trial data, EIQ’s technology has been shown to accurately identify 100% of severe aortic stenosis patients.

According to clinical trial data, EIQ’s technology has been shown to accurately identify 100% of severe aortic stenosis patients.

Also, it provides a 72% uplift in detection when the AI compares to a cardiologist. (Source, p. 10)

On top of that, EIQ published data that shows its AI product EchoSolve accurately identified 15% more patients with severe aortic stenosis compared to humans. (Source)

While those numbers may not sound like a major difference, the direct costs to the US healthcare system are north of $10BN and there is a 50% mortality rate within 2 years if left untreated.

With 1.5 million people suffering from aortic stenosis in the US alone, that equates to roughly 100,000 people a year that EIQ’s tech could pick up and get into better treatment quicker.

These are important numbers, and we think they further contribute to the case for EIQ’s AI algorithm getting FDA approval.

What happens if the FDA doesn’t approve?

There is always the chance, however slim we may think it is, that the FDA does not approve EIQ’s aortic stenosis product.

The heart is a sensitive topic in medicine, and the regulator has a duty to ensure that lives are not harmed or ended by approving the wrong products.

If EIQ does not receive FDA approval, this may mean that EIQ has to “go back to the drawing board” and come back with more data and make another submission.

This would require more trials, and more time.

We really hope it doesn’t come to that, but we are prepared for this outcome, should it eventuate (see Risks below).

Either way, we will know very soon.

So, now that we’ve established why we think that EIQ will secure FDA approval, let’s look at potential risks...

What could go wrong?

The most immediate risk for EIQ is regulatory risk.

We should know within the next few weeks the FDA decision on aortic stenosis.

Regulatory Risk

EIQ has applied for FDA clearance under the 510(k) pathway for aortic stenosis and will apply for FDA clearance for heart failure.

There is no guarantee that the FDA will provide clearance, and the application may be rejected.

Also, EIQ’s strategy is reliant on securing reimbursement for its product.

If EIQ is not able to secure a reimbursement deal then its commercialisation strategy may need to pivot.

What could go wrong? EIQ Investment Memo

In the medium term EIQ’s key risk will be sales/commercialisation.

Selling into hospitals and healthcare providers can take a long time. There are long sales cycles and large onboarding / integration processes.

We expect it to take at least 12 months for EIQ to ramp up sales of its products (in line with the standard sales cycle within the industry), but if it takes longer investors may get impatient.

Sales/Commercialisation Risk

EIQ is reliant on its partners, both under the licensing and reimbursement strategy, to use EIQ’s product.

If EIQ’s product is not used (because it doesn’t add value back to the provider), then it won’t be able to generate revenue.

There is no guarantee that EIQ’s product will be used by its partners and, therefore, no guarantee of revenue.

What could go wrong? EIQ Investment Memo

Our EIQ Investment Memo

In our EIQ Investment Memo, you can find the following:

- What does EIQ do?

- The macro theme for EIQ

- Our EIQ Big Bet

- What we want to see EIQ achieve

- Why we are Invested in EIQ

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.