EIQ: Announces its AI tech can detect Heart Failure too - with 99.5% sensitivity and 91.0% specificity

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 1,990,332 EIQ Shares at the time of publishing this article. The Company has been engaged by EIQ to share our commentary on the progress of our Investment in EIQ over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs.

EchoIQ (ASX:EIQ) has developed (and is already in the market with) an AI-powered algorithm that helps cardiologists detect heart diseases.

EIQ makes money when hospitals that use its AI technology claim a $ fee from insurance companies using an approved “reimbursement code”.

EIQ’s tech is already USA FDA approved AND being used by a growing number of hospitals in the USA to detect one heart disease called Aortic Stenosis.

They are just waiting for a specific reimbursement code for Aortic Stenosis to be approved to convert this growing usage into revenue (expected in 2026).

Today EIQ announced results of a clinical validation study on a different heart disease (this one you have probably already heard of):

Heart Failure.

Heart Failure is one of the big heart diseases - US$60BN is spent on it, 1 in 4 Americans will get it, and it's the leading cause of rehospitalisation.

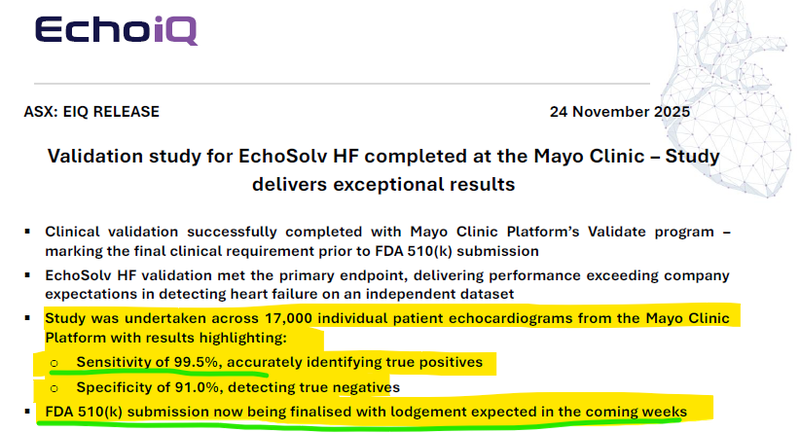

EIQ’s clinical validation study was run by the prestigious Mayo Clinic, and it delivered exceptional results on detecting heart failure with 99.5% sensitivity and 91.0% specificity (source).

Much better than the only other AI heart failure detection software used in the market today which delivers - sensitivity of 87.8% and specificity of 81.9% (source).

(Both technologies are a step change from current practices where only 50% of Heart Failure cases are accurately diagnosed.)

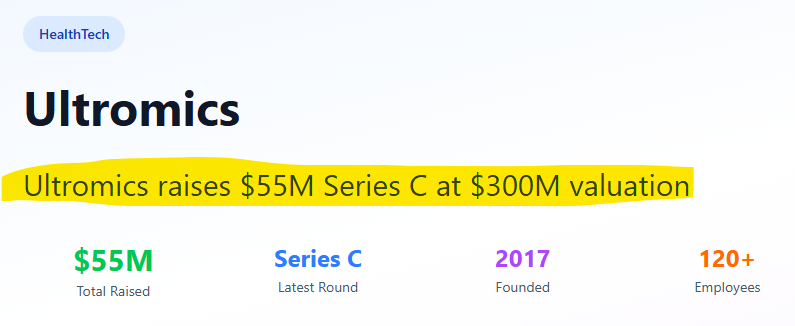

But the most important thing here is, a reimbursement code for AI detection of heart failure ALREADY EXISTS (thanks, Ultromics).

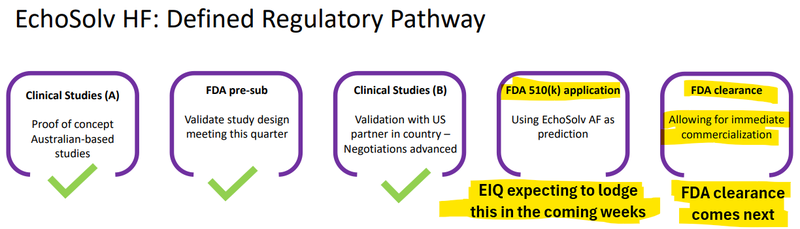

So what happens next?

IF EIQ can get FDA approval for its Heart Failure AI model, there already exists a reimbursement code the company can use to commercialise its AI tech.

The reimbursement code exists thanks to Ultromics (who raised US$55M in a series C funding round valuing them at US$300M / A$464M back in July).

BUT, today EIQ delivered results that look stronger than Ultromics - and from a dataset of patients ~13x bigger (Source).

So IF EIQ’s AI detection tech gets the all clear from the FDA for heart failure...

... it may be able to quickly start generating revenue using the existing heart failure detection reimbursement code.

Now we watch for FDA approval...

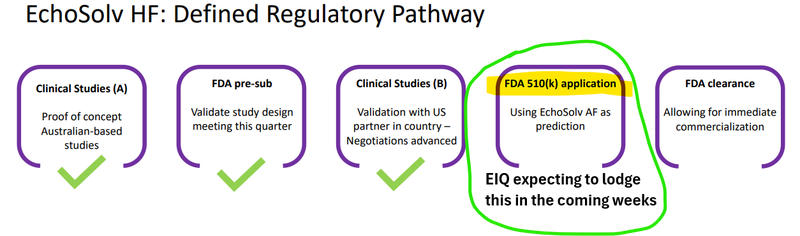

EIQ said today that they are submitting for FDA approval in two weeks time.

(Source)

Also, the hospital networks that are ALREADY using EIQ for Aortic Stenosis, can easily set up for detecting Heart Failure as well... if/once the FDA clearance comes in.

We will be tuning into the webinar EIQ has scheduled for Wednesday, 26 November at 11:00am (AEDT) - the main thing we will be listening out for is when we can expect to see FDA clearance for Heart Failure...

Click here to register for the webinar

When it comes to heart diseases, “Heart Failure” is one of the big ones.

One in four Americans will develop heart failure in their lifetime, it's the leading cause of rehospitalisation, and it accounts for 17% of US healthcare expenditure.

Heart Failure accounts for ~US$60BN in healthcare expenditure per year in the US alone.

Today EIQ released results from a clinical validation study for its Heart Failure detection algorithm.

EIQ’s study was completed on 17,000 individual patient echocardiograms and EIQ’s technology demonstrated:

- Sensitivity of 99.5% (The ability to identify 99.5% of all patients who actually had heart failure).

- Specificity of 91.0% (the ability to identify 91% of patients who don't have Heart Failure).

(Source)

Basically this means that when EIQ’s tech is plugged into cardiologists' workflows, IF the AI says you are positive... 99.5% of the time, the AI is correct...

(At the moment, only 50% of heart failure cases are accurately diagnosed).

Very high sensitivity (and good, but not perfect specificity) is what we want to see with screening/detection technologies because the overarching goal is to make sure every single case is picked up (even if it means there are a few false positives).

Higher sensitivity means very few people ‘slip through the cracks’.

As we mentioned above, the only other FDA-approved Heart Failure AI model is the one developed by US private company Ultromics - whose tech showed sensitivity of 87.8% and specificity of 81.9%.

(Source)

EIQ’s data looks stronger... Sensitivity of 99.5% and Specificity of 91.0%... and EIQ’s study was done on a dataset ~13x bigger than Ultromics.

In July, Ultromics raised US$55M in a series C funding round. According to the source below, the valuation was ~US$300M.

(Source)

Today EIQ is capped at A$150M, and held ~A$16M in cash at 30th September 2025.

Now EIQ has all the data it needs to make an application to the FDA for a clearance - which it plans to do in the “coming weeks”...

Allowing for “immediate commercialization”:

(Source)

As mentioned earlier, EIQ’s already got an AI detection algorithm cleared by the FDA before and currently in the commercialisation phase (for Aortic Stenosis).

The Aortic Stenosis AI tech had specificity of 98.1% and sensitivity of 82.2%...

The Heart Failure tech has much stronger results - which we hope translates to a higher probability of FDA approvals in the next few months.

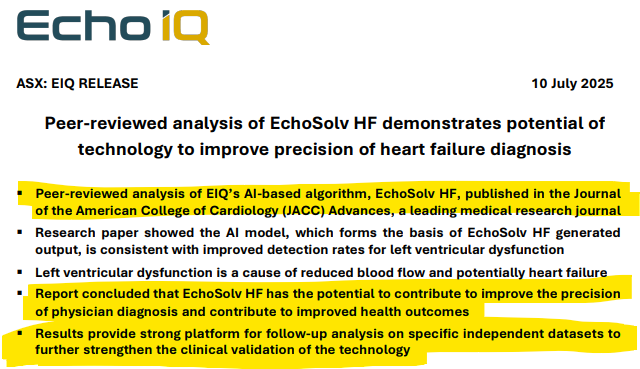

We also note that results from using EIQ’s Heart Failure tech was published in a “Journal of the American College of Cardiology” which showed:

“that EIQ’s tech could help improve precision of physician diagnosis and contribute to improved health outcomes”.

(Source)

We think this peer reviewed analysis in a leading medical research journal should strengthen the credibility of EIQ’s tech going into an FDA meeting.

We think FDA clearance for Heart Failure could be a game changer for EIQ for two reasons:

1. Because Heart Failure is a very big market (especially in the US)

Heart Failure is the leading cause of rehospitalisation and accounts for 17% of US healthcare. For context, healthcare expenditure for Heart Failure is ~US$60BN per annum.

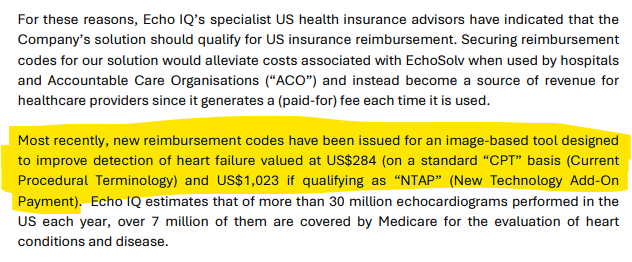

2. Because the Heart Failure tech already has an established reimbursement code pathway in place so EIQ can switch on revenues a lot quicker...

In the US, there are ~7M patients covered by Medicare for the evaluation of heart conditions and diseases...

For heart failure, there are existing reimbursement rates of ~US$284 for “an image-based tool designed to improve detection of heart failure tech” and US$1,023 if qualifying as (New Technology Add-on Payment).

(EIQ could look to use these existing codes to commercialise its heart failure tech)

(Source)

The big win then for EIQ will be that the Heart Failure tech will benefit from all the rollout work EIQ is doing on Aortic Stenosis.

Because EIQ’s is a software product, it is very much “plug and play”.

Any hospital networks that are already using EIQ for Aortic Stenosis, can easily set up for Heart Failure as well... if/once the FDA clearance comes in.

(Instead of doing the cold intro, bringing a hospital/imaging network up to speed on who EIQ is and what the company can do for them, it's more a case of informing them that they can now use the same tech to also detect Heart Failure.)

So far, EIQ, as part of its Aortic Stenosis commercialisation push, EIQ has already pulled in:

- A reseller agreement with SARC MedIQ - a leading provider of imaging workflow solutions in the US...SARC MedIQ services over 300 US healthcare facilities and clinics catering to more than 1,500 physicians.

- An integrations agreement with Beth Israel Deaconess Medical Center (BIDMC) - Harvard Medical School's flagship teaching hospital which ranks in top 1% of US hospitals for cardiology and conducts ~30,000 echocardiograms annually.

- Strategic partnership and integration agreement with ScImage - An enterprise imaging platform with ~1,200 active users across the US.

- Commercial partnership with MedAxiom (in conjunction with ScImage) - Works in conjunction with ScImage partnership for deployment across 36 affiliated hospitals and practices

- Sales deal with Cassling Diagnostic Imaging - an established healthcare provider since 1984, who provide imaging and therapeutic technology services across the Midwest and portions of South and West US

- Licensing agreement with Respiri - Integration of EchoSolv into Respiri's US Remote Patient Monitoring offering; focus on Accountable Care Organization (ACO) sector treating Medicare patients; monthly license fee per patient meeting AHA guidelines for severe AS

So EIQ has already laid the foundations for integrating its tech into hospitals and imaging networks in the US.

And we expect that network to get even bigger by the time EIQ’s Heart Failure detection tech is FDA cleared and ready to be commercialised...

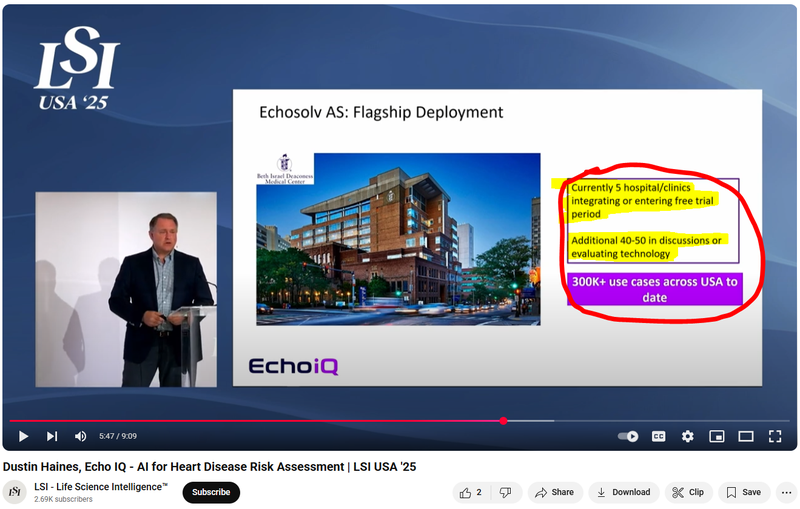

Here is EIQ’s CEO (Dustin Haines) take on EIQ’s integration pipeline from a presentation in March - note he mentions additional 40-50 hospitals/clinics are in discussions or are evaluating EIQ’s tech:

(Watch the full presentation here)

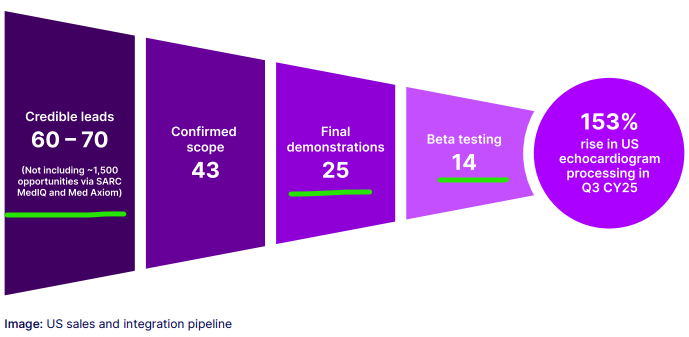

And we noticed the latest quarterly show EIQ is in the final demo stage and beta testing across a total of 39 sites spanning large hospital groups and clinics.

(Source)

The major takeaway for us here is that EIQ is managing to sign multiple deals with multiple partners which we hope means faster integration into workflows across the US.

That’s where EIQ’s Heart Failure detection tech comes into play.

All of the integration work EIQ is doing now means EIQ can instantly roll out Heart Failure (HF) detection tech to those same networks once the FDA clearance comes in...

What’s next for EIQ?

🔄 Commercialisation updates for Aortic Stenosis AI tech

The key metric we will be tracking in the short term is how many integrations EIQ can secure for its Aortic Stenosis tech.

We want to see EIQ sign more distribution deals - either through strategic partnerships or reseller deals.

🔄 Heart Failure FDA submission and approvals

We want to see EIQ make its FDA submission for its Heart Failure detection tech (and fingers crossed) receive clearance for the tech allowing it to be commercialised.

🔄 Australia and NZ pilot program

EIQ has previously mentioned that this program is being run with a ”leading global structural heart innovation company”.

We want to see some more news on this front because we think it could help advance EIQ’s licensing revenue pathway and be a “proof of concept” study that EIQ can take into the US.

What are the risks?

EIQ is now in the commercialisation stage for its Aortic Stenosis tech and there is a risk that integrations are delayed and EIQ struggles to get buy in from hospital/clinicians to adopt the tech.

Sales/Commercialisation risk

EIQ is reliant on its partners, both under the licensing and reimbursement strategy, to use EIQ’s product. If EIQ’s product is not used (because it doesn’t add value back to the provider), then it won’t be able to generate revenue. There is no guarantee that EIQ’s product will be used by its partners and, therefore, no guarantee of revenue.

Source: “What could go wrong” - EIQ Investment Memo 6 Sept 2024

There is also an element of regulatory risk.

We mentioned in our last note that there was a risk EIQ’s Category III reimbursement code for Aortic Stenosis isn’t approved.

Unfortunately, that risk ended up materialising in early October when EIQ was “was unsuccessful in its application for a Category III Current Procedural Technology (CPT)” for the second time. (source)

The major risk now is EIQ’s Heart Failure tech not being cleared by the FDA.

Again if this were to happen it could have a material negative impact on EIQ’s share price.

Regulatory Risk

There is no guarantee that the FDA will provide clearance, and applications made by EIQ may be rejected. Also, EIQ’s strategy is reliant on securing reimbursement for its product. If EIQ is not able to secure a reimbursement deal then its commercialisation strategy may need to pivot.

Source: “What could go wrong” - EIQ Investment Memo 6 Sept 2024

Other Risks

Like any stock market investment, investing in EIQ carries a multitude of risks which may affect the value of the company, some which are unable to be identified (this is the nature of risks).

Here we aim to identify a few more risks.

The company’s primary assets are pre-commercial, FDA-cleared/under-development diagnostic technologies, and it is possible that EIQ fails to achieve widespread clinical adoption or meaningful revenues.

Competition risk is also relevant, the cardiovascular AI imaging space is crowded, with well-capitalised peers like Ultromics pursuing the same market. Competitors could capture adoption, limit pricing power, or reduce EIQ’s market share.

EIQ is still considered a pre-revenue company so there is always a chance EIQ may need to return to market for funding if commercialisation timelines extend. Any such raise could dilute existing shareholders.

Finally, execution risk remains. Successful integration into hospital and clinic workflows requires significant operational capability, sales execution, and clinician acceptance. Delays or setbacks here could hinder revenue generation.

Investors should consider these risks carefully and seek professional advice tailored to their personal circumstances before investing.

Our EIQ Investment Memo

You can read our EIQ Investment Memo in the link below.

We use this memo to track the progress of all our Investments over time.

Our EIQ Investment Memo covers:

- What does EIQ do?

- The macro theme for EIQ

- Our EIQ Big Bet

- What we want to see EIQ achieve

- Why we are Invested in EIQ

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.