Delivering on Target

Hey! Looks like you have stumbled on the section of our website where we have archived articles from our old business model.

In 2019 the original founding team returned to run Next Investors, we changed our business model to only write about stocks we carefully research and are invested in for the long term.

The below articles were written under our previous business model. We have kept these articles online here for your reference.

Our new mission is to build a high performing ASX micro cap investment portfolio and share our research, analysis and investment strategy with our readers.

Click Here to View Latest Articles

Overview: Crowd Mobile Limited ("Crowd Mobile", "the Company") is an Australian technology company focused on mobile software and mobile marketing services. Its principal asset is a Question and Answer platform (‘Q&A’) and a mobile payments network spanning 212 telco carriers, 64 countries, and 30 languages. This distribution network was built by the Company and its predecessors over 15 years. In addition, the Company launched a new division, Crowd Media, to take advantage of the $3.5bn markets for digital influencer advertising. Our last advice was a ‘spec buy’ recommendation in June 2017.

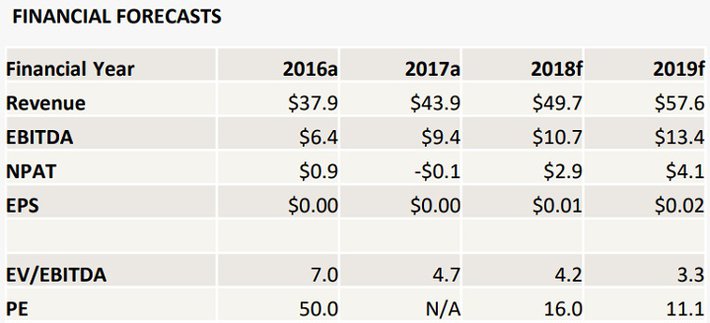

Catalysts: Supported by a new institutional investor and strengthened balance sheet, Crowd Mobile has met our FY17 forecasts (Revenue up 16%, EBITDA up 49%). With June its strongest quarter, the Company has the momentum to deliver further growth in FY18. With the cost of acquisition in its Q&A unit 20% lower YoY, early benefits of the Crowd Media initiative are beginning to show. The rhetoric surrounding the recently sluggish Subscription unit was positive, although initiatives in this unit are yet to flow through to the financials.

Hurdles: Despite the Company’s improved liquidity, its reliance on external capital may not be entirely eliminated. Whilst the performance of the Subscriptions business unit has stabilised, there is no guarantee against further erosion of its earnings base. A lack of growth within the Subscriptions division may challenge Crowd Mobile’s ability to attract an appropriate valuation for its growing Q&A division. Crowd Mobile does not own any patents to its technology and may be subject to increasing competition.

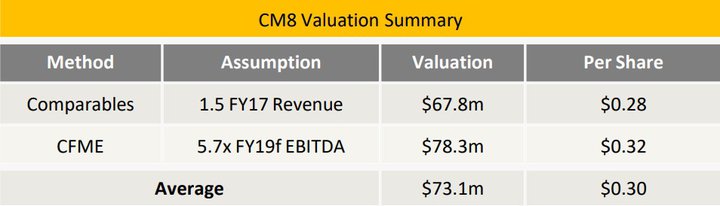

Investment View: Crowd Mobile provides profitable exposure to mobile software and services trends. After meeting our FY17 forecasts and restoring balance sheet health, the Company is in a sound position to invest in its digital influencer strategy. With recent growth fuelled by the smaller (Q&A) of its two divisions, we are carefully monitoring the performance of the sluggish Subscriptions unit and recently launched Crowd Media initiative. After updating our forecasts with the full-year result, our valuation of $0.30 per share (up 3%) represents a 66% premium to recent trade, and we maintain our ‘speculative buy’ recommendation.

THE BULLS AND THE BEARS

THE BULLS SAY

- Crowd Mobile is a cash flow positive Company with a highly diversified revenue base supported by 212 telco partners in 64 countries and 30 languages

- Crowd Mobile’s balance sheet has significantly improved following a $5.4million equity placement in April at a premium to the market, allowing surplus cashflow to be increasingly directed towards growth and capital management initiatives

- Rapid retirement of borrowings associated with the 2015 Track acquisition is providing greater certainty for Crowd Mobile’s capital structure

- The operational performance of the subscription business is stabilising and should help Crowd Mobile to further grow its Q&A division

- Our valuation represents a premium to recent trade

THE BEARS SAY

- Despite the Company’s increased scale following its acquisition of Track, high interest and amortisation charges have impacted profitability

- The poor performance of the Track business under Crowd Mobile’s stewardship may impact confidence in management’s ability to drive sustainable growth from its m-payments network

- Equity required to finance and support the Track acquisition has resulted in a diluted share count and there is no guarantee that further dilution won’t occur

- There is no guarantee against further erosion of earnings in the subscription business which may challenge Crowd Mobile’s ability to attract fair value for its Q&A division.

- Our valuation is contingent on ongoing growth

APPENDIX

Summary of revisions vs 8-Jun-2017 update

- FY18f revenue has been raised by 2% with EBITDA and NPAT unchanged to reflect increasing investment in Crowd Media

- Following the delivery of the FY17 result, the forecast period extended to FY19, and valuation multiples have been rolled forward

Notes:

EV/EBITDA and PE ratios are based on a diluted share count of 242.3million, net debt of $2.9million, and option proceeds totalling $4.4million.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.