Australian Government funding USA mining projects? All hands on deck for this urgent national security issue.

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 1,815,118 BKB Shares and the company’s staff own 30,000 BKB Shares at the time of publishing this article. The Company has been engaged by BKB to share our commentary on the progress of our Investment in BKB over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs. Any forward-looking statements are uncertain and not a guaranteed outcome.

Our current favourite investment themes are the global AI, robotics and military buildouts.

...and the critical minerals needed to build them.

Especially in the USA, which over 40 years outsourced nearly all of its mining and manufacturing to China.

Now the USA is scrambling to build it all back as fast as possible.

Confirming this urgency (yet again) - this week, the US President signed an Executive Order called: “Approving Critical Position Pay Authority for National Security Investment Workforce” (source)

Quite the mouthful.

Quick summary is that this Executive Order unlocks funds to rapidly hire mining and advanced materials experts as quickly as possible into key US government roles.

It literally refers to critical minerals and domestic mining as an urgent national security issue.

Also this week, came an even FASTER way to secure critical minerals supply:

The US, Japan, Australia, and India (the "Quad") just teamed up to announce a $20 billion plan to jointly fund critical minerals mining, processing, and recycling. (source)

The goal is to build a reliable supply chain for these materials and reduce dependence on China, which currently processes about 90% of the world's rare earths.

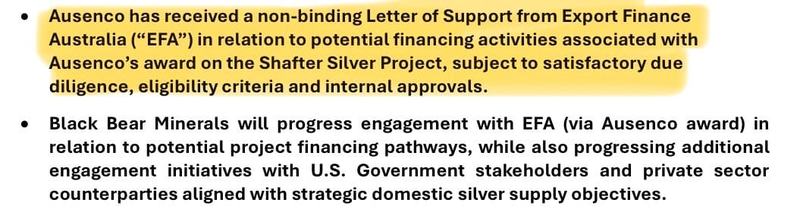

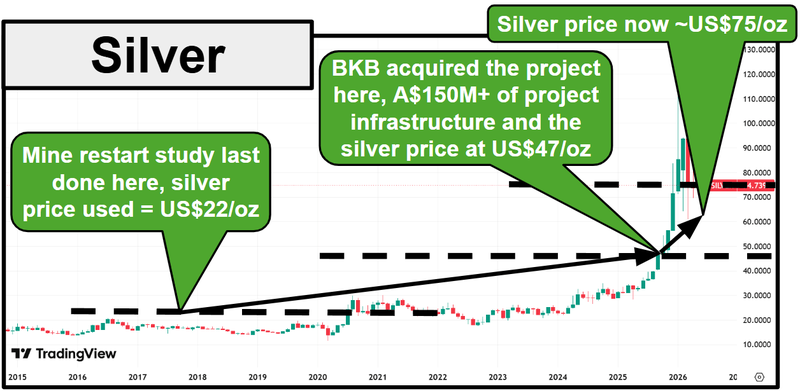

Today our USA Investment Black Bear Minerals (ASX:BKB) announced a non-binding letter of support from the Australian government to help fund the “rapid restart” of its silver mine...

that is located in the USA (a Quad member).

Silver is critical in AI, robotics and military - which is probably why the US government has silver on its Critical Minerals list.

Global silver demand reached 1.1 billion ounces in 2024, with industrial demand hitting a record 680.5 million ounces.

The silver market has been in deficit for 5 years straight...

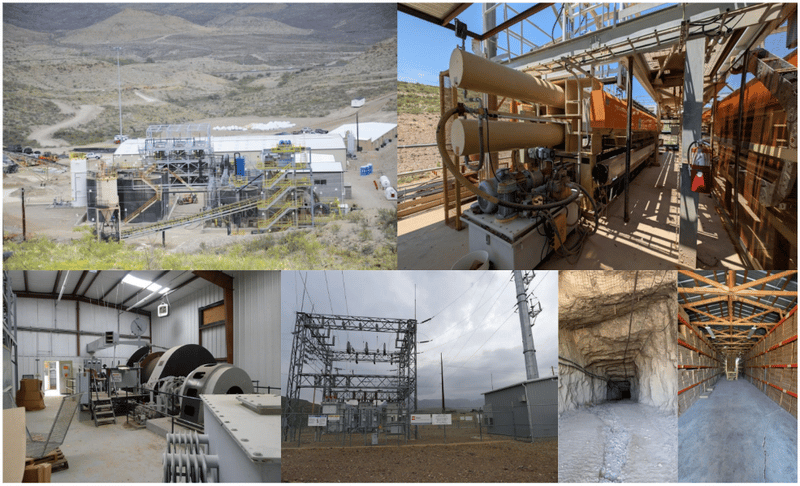

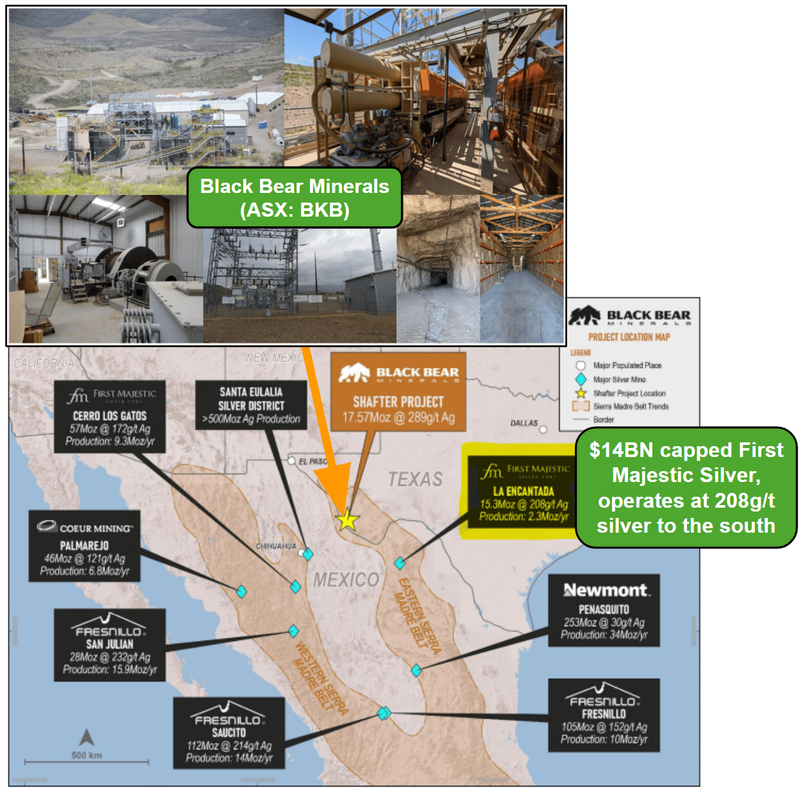

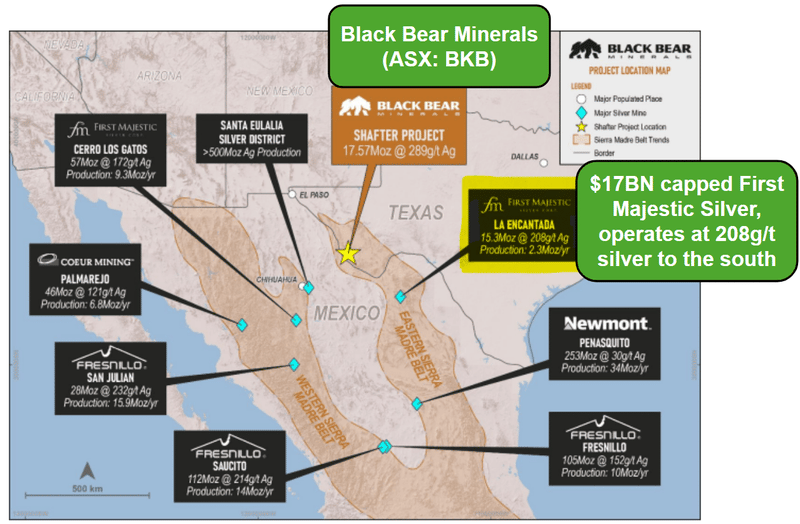

BKB owns a silver project in Texas, USA with:

- a 17.6Moz silver foreign resource (average grade of 289g/t),

- already has ~A$150M of existing on-site infrastructure

- and produced silver as recently as 2012-2013.

5 months ago BKB announced the appointment of global engineering firm Ausenco to conduct a “rapid restart” assessment of the mine.

Today BKB announced that Ausenco have been awarded the next phase of the restart studies AND engagement from the Australian government to help fund the project.

A big part of our Investment thesis for BKB’s silver asset is to see BKB use the ~A$150M of existing on-site infrastructure and get the project back into production while silver prices are high.

Here is everything that sits on site right now: (source)

- plant + refinery (built 2011-2012) A modern

- A 24,000 sq. ft. warehouse

- An assay lab

- Existing power lines + an on-site substation

- Full water rights

- 160km of existing underground workings

- Four production shafts

- PLUS all major operating & environmental permits.

(All of that infrastructure is only ~10-15 years old, and was barely used at full capacity before being put on care and maintenance.)

(source)

BKB is currently doing “rapid restart” studies for this silver mine and processing plant.

BKB is now in the second phase of restart studies (scoping out the costs to get all that gear back into production).

And today, BKB’s development studies partner Ausenco received a non-binding Letter of Support from Export Finance Australia to potentially fund those restart costs.

(source)

We are Invested in BKB to see the company bring that mine back into production while the silver price is high.

IF/When that happens - the silver price will drive a big part of what the project can produce from an economics perspective.

(Obviously we hope it will be a lot higher than today - but it could also be down, we can’t control the silver price)

BKB is drilling this silver project right now.

(source)

Over the next few months, with everything BKB is doing, we could have:

- A completed dilapidation study - first look at costs to refurbish and restart the plant

- Drilling results and a resource upgrade

Potentially a fully costed pathway toward restarting BKB’s silver project.

Silver is used in AI, robotics, and the military - demand from these to trigger the next run?

The big question for BKB is - what will the silver price be when it's ready to make a Final Investment Decision on bringing back into production its silver project?

Our favourite momentum technical analyst Michael Oliver reckons silver is going to US$300 to US$500 per ounce - hear his reasoning here.

(Remember: he could be wrong.)

IF he is right, then BKB’s project economics will look very good - remember the mine was producing when silver prices were ~US$20 per ounce.

So what could trigger a run in the silver price to those levels?

Maybe it could come from a global, multi-decade scramble for the metals to build AI datacentres, robots and military rebuilds?

AI and AI data centres

AI chips run insanely hot when they're working, and silver is used as a thin layer underneath each chip as the “first line of thermal management defence" to suck the heat away fast enough to stop it melting.

Silver is also packed into the giant switches and breakers that handle the enormous amounts of electricity these AI data centres pull from the grid.

Robotics

Robots have dozens of moving joints, motors and electronic boards that all need to carry power reliably for years without wearing out.

Silver is used in the joint brushes, the connector pins, and the solder holding it all together because nothing else lasts as long under constant movement.

Military and weapons

Silver-zinc batteries are the only batteries that can sit dormant in a missile for years and then deliver a massive burst of power on demand.

(ever tried to turn an old car on after a few years and the battery has died?)

Silver (under radar chips) allows for signals to be blast out without overheating, and silver-coated mirrors on satellites reflect away the sun's heat so the electronics don't fry in space.

So silver plays a part in ALL THREE of our “global buildouts that will drive the all commodity boom”.

Silver has the highest electrical conductivity of any element on the periodic table, the highest thermal conductivity of any metal, and the highest reflectivity in the visible/IR spectrum.

Nothing else comes close on all three at once - which is why some silver sneaks into pretty much every high-tech build.

For context, silver demand from electronics is already up 51% since 2016, and the silver market has been in deficit for five straight years.

So any incremental increase in demand from AI, robotics or the military could push prices higher...

No guarantees of course, commodity price directions are very hard to forecast with any certainty.

BKB also has a gold asset in Nevada - we think both of BKB’s assets are potential company makers

So within the ~$94M capped BKB we get exposure to two potential company making assets.

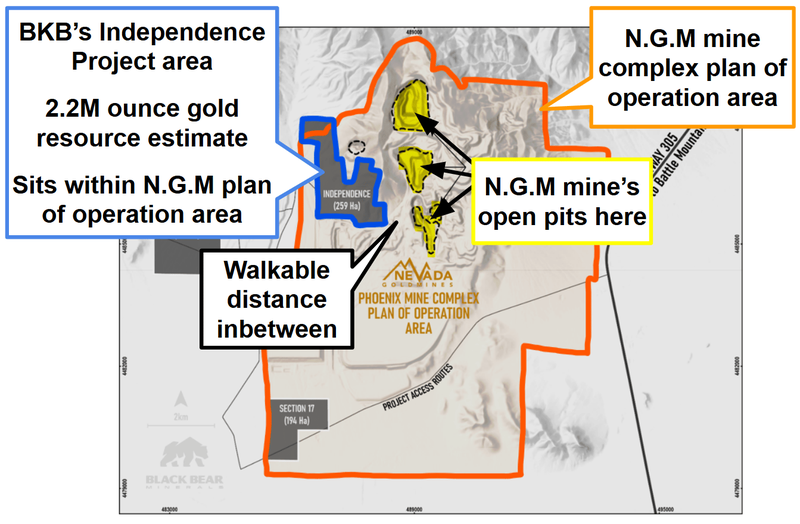

A 2.2M ounce gold equivalent JORC resource estimate - surrounded by two of the biggest gold miners in the world (Barrick and Newmont).

BKB’s project is practically surrounded on all sides but one by the giant Phoenix gold complex.

We think the gold asset alone more than justifies BKB’s current ~$94M market cap.

And that high grade silver asset with all of the processing infrastructure in place to go mining we covered above while the silver price is strong.

(source)

We think the market is only valuing one of BKB’s two assets and two scenarios:

Scenario A: Assuming the US gold project is the main story in which case BKB has:

- A 2.2Moz gold equivalent JORC Mineral Resource estimate

- Exploration upside (open along strike and at depth in every direction)

- Adjacent to the N.G.M Phoenix mine complex ($99BN Barrick and $163BN Newmont)

- Inside N.G.M's Plan of Operations Area

IF the market thinks of BKB like this then we are getting a “free option” on the silver asset (with its estimated A$150M of infrastructure and 17.6Moz of silver at 289g/t).

Scenario B: Assuming the US silver project is the main story, in which case BKB has:

- A 17.6Moz silver foreign resource estimate at 289g/t

- A$150M of existing processing infrastructure (built in 2011-2012)

- Silver on the US Critical Minerals List

- A 2018 restart study with a Net Present Value of US$42M at US$22/oz silver (way below the current ~US$87 silver price).

- A rapid restart study underway right now

- Drilling underway right now

And in this scenario, we get a “free option” on the gold asset (with its 2.2Moz gold equivalent next door to NGM).

We are bullish on BOTH gold AND silver.

So we're more than happy to hold the majority of our BKB position and let either story play out (or both).

Our BKB Big Bet:

“We want to see BKB drill, extend and grow the resources on both its gold and silver projects to the point of the projects being development ready (or to the point of a major buying out the assets). At that point, we hope to see BKB’s market cap trade at $750M+”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including development risk, market risk and commodity price risk - just some of which we list in our BKB Investment Memo.

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

In the rest of today’s note we will do a deep dive on BKB’s two projects, starting with the silver project in Texas.

Recap of BKB’s silver project in Texas

This is the asset that made BKB our 2025 Small Cap Pick of the Year back in November.

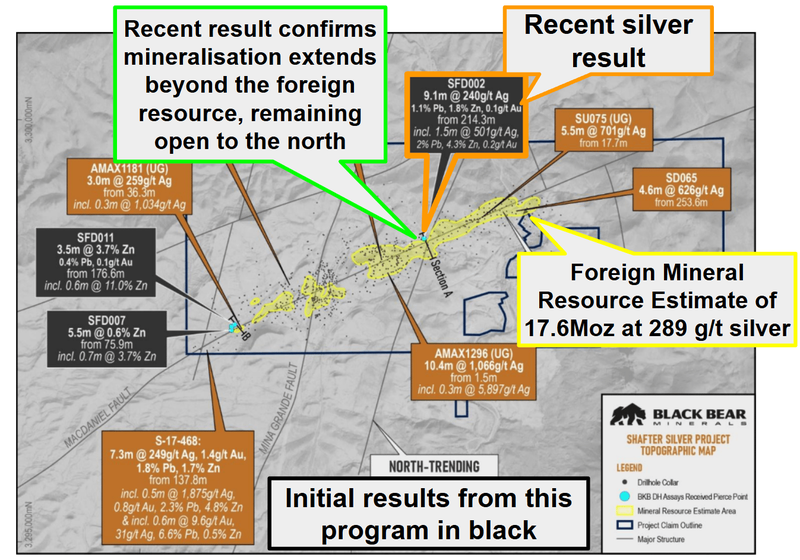

BKB owns 100% of a 17.6Moz silver foreign resource at 289g/t silver.

Those are seriously high grades especially when compared to other primary silver mines operating globally.

For example ~$17BN First Majestic Silver’s assets ~300km to the southeast on the same belt operates with grades below ~289g/t silver.

(Higher grade generally means stronger margins per tonne mined - which matters a lot for project economics)

(source)

The project has in the past produced ~35 million ounces of silver between 1883 and 1942 at an average grade of 521 g/t Ag.

And then more silver when it was last in production in 2012–2013 - until silver prices below US$18 per ounce forced the asset into care and maintenance.

The reason we like the project is that it already has A$150M of existing on-site infrastructure, including:

- plant + refinery (built 2011-2012) A modern

- A 24,000 sq. ft. warehouse

- An assay lab

- Existing power lines + an on-site substation

- Full water rights

- 160km of existing underground workings

- Four production shafts

(All of that infrastructure is only ~10-15 years old, and was barely used at full capacity before being put on care and maintenance.)

We think that this is the type of asset that can get back into production quickly (because of all that infrastructure on site) in a higher silver price environment.

Then, because of those grades they operate with strong margins...

(source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

BKB has engaged Ausenco (one of the world's leading mining engineering firms) to deliver a "rapid restart" study on Shafter.

By the end of that study, BKB should have:

- A dilapidation study - working out exactly what's needed to get the existing infrastructure operation-ready, and

- A restart CAPEX estimate - an order-of-magnitude capital cost estimate for equipment refurbishment and facility restart.

Together, that's enough information to commence a formal Scoping Study and move toward a Final Investment Decision (FID) on a restart.

And with all major permits already confirmed active and in good standing (BKB locked that down earlier this year), restart financing discussions should be a lot smoother.

So what could a restart actually be worth?

A 2018 restart study was completed on the project showing an NPV of US$42M at a US$22/oz silver price.

That same study noted that for every 5% increase in the silver price, the NPV increases by ~US$5.5M.

Silver today (~US$75/oz) is roughly 241% higher than the US$22 assumption used back in 2018.

Run that sensitivity forward, and you land at a potential NPV somewhere in the US$265M+ range (on top of the original US$42M).

Call it a total somewhere around ~US$265M... or ~A$370M.

That old 2018 study didn't include any by-product credits for gold, zinc or lead.

Any additional metal credits could improve the restart economics further.

BKB is currently drilling the project and assaying for other metals too

BKB is in the middle of an 11 hole diamond drilling program on the project.

One hole (hole #2) already hit 9.1m at 240g/t silver from 214.3m - including 1.5m at 501g/t silver.

OUTSIDE of the project’s existing 17.6Moz resource.

And assays from that hole have also returned lead, zinc and gold (with zinc grades as high as ~11%).

The current resource sits across ~4km of strike that is largely untested, with known mineralisation - with this current round of drilling, we are hoping to see that resource grow.

BKB is targeting a maiden JORC resource on the silver project in 2026.

(source)

BKB also owns 100% of a 2.2M oz gold project in Nevada

As mentioned earlier, we think the market is currently pricing BKB based on one of its two assets.

BKB’s gold project in Nevada has a JORC 2.2M ounce gold resource AND it sits inside the mine plan of N.G.M’s Phoenix operation.

Yes... N.G.M as in the $99BN Barrick and $163BN Newmont JV.

(source)

Being next door to that N.G.M asset is especially important right now.

Because $99BN Barrick is officially spinning out its US assets into a separately listed entity.

(source)

The new entity, which is expected to complete an IPO in late 2026 at a ~US$42BN valuation would hold:

- 61.5% stake in Nevada Gold Mines (the JV with Newmont - includes Phoenix, Cortez, Carlin, Goldstrike, Turquoise Ridge)

- 100% Fourmile (Barrick's wholly-owned Nevada discovery), AND

- Barrick’s 60% stake in Pueblo Viejo (Dominican Republic)

For the first time in decades, Nevada will be home to a pure-play, listed US gold producer whose management can focus 100% of its time and capital on the US.

No more competing inside Barrick for capital that gets allocated to copper projects in Pakistan, gold in Mali, or African expansion.

Which we think means more capital flowing into its US based assets for growth.

IF only there was an asset with a 2.2M ounce gold equivalent resource...

...sitting right next door to one of NewCo's assets...

...and actually sitting inside one of NewCo's existing mine plans.

BKB’s resource is getting big enough to be interesting to a major too

We think now, with a 2.2M ounce gold equivalent resource estimate, BKB has demonstrated that its project is big enough to warrant attention from the operators of a massive mine next door.

Especially given BKB’s project still has plenty of exploration upside too.

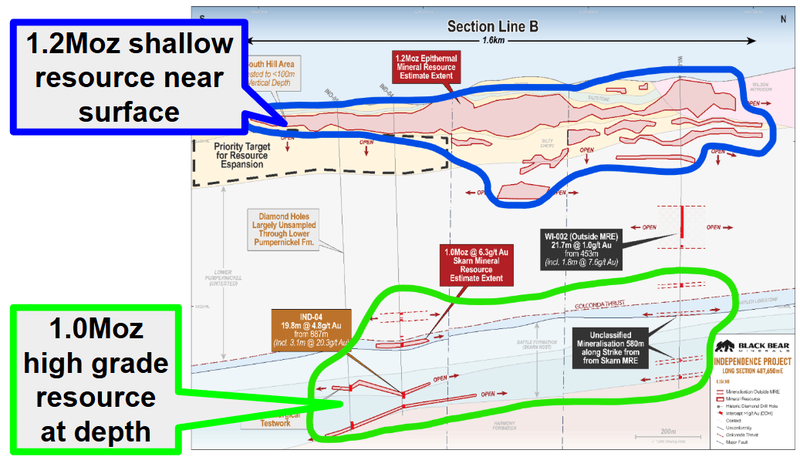

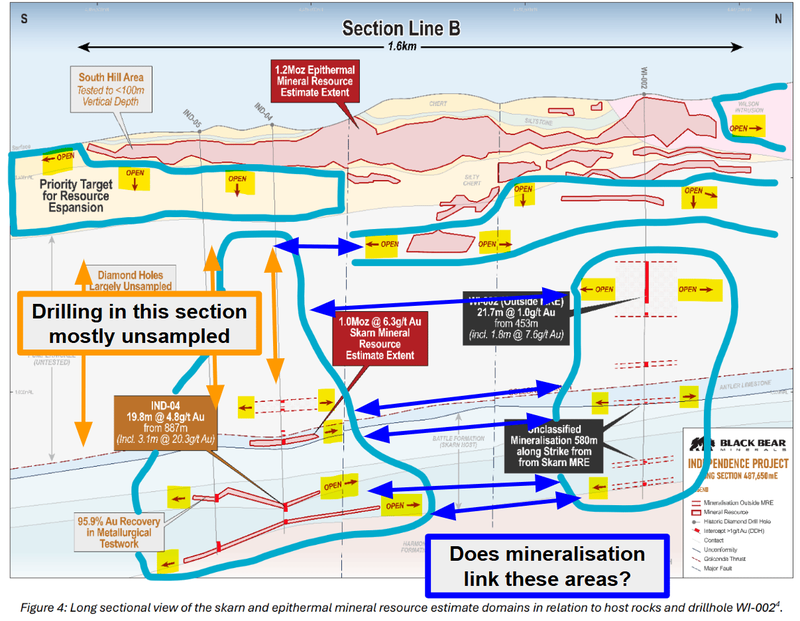

Here is where the current JORC resource estimate sits:

- 1.2M ounces near-surface across ~1.5km of strike, and

- 1.0M ounces at depth with an average grade of 6.29g/t gold

(source)

And here is all that exploration upside (something that a major looking at the asset would care a lot about):

Open along strike, down dip, north, south.

(source)

We already know BKB's project sits inside N.G.M's "Plan of Operations Area" - the formal administrative boundary N.G.M has filed for its operating envelope.

That means it sits inside the permitting framework N.G.M already has in place. And it could mean faster integration of the project into whatever N.G.M wants to do next.

We also know that BKB’s deeper resource is the same type of material that was mined at N.G.M’s Phoenix operation at the Fortitude pit between 1984-1993.

That pit produced ~2.1Moz of gold at ~6.68g/t Au at over 90% recoveries.

Almost identical grades to BKB’s current resource (BKB's deeper resource is 1Moz at 6.29g/t Au) and Interestingly the metallurgy looks similar...

BKB has shown that it could have 95.9% gold recovery (per BKB metallurgical testwork).

So BKB’s deeper resource is something N.G.M understands very well and has mined/processed before...

As for the shallow part of BKB’s resource...

We already know that the at surface mineralisation is similar to the stuff that N.G.M’s been mining at its Phoenix pit for years - and the right type of ore to go straight into their processing plants.

Here is what we said in our BKB site visit note from last year:

(source - our site visit article)

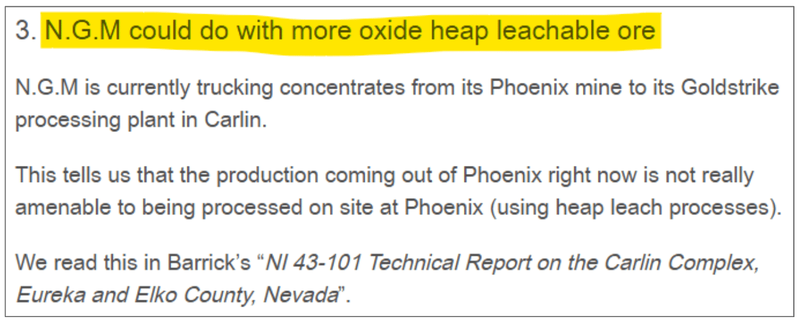

And here is that reference to the Carlin plants processing “third-party ores” from Phoenix.

Yes, N.G.M has to truck the concentrates from the Phoenix mine all the way to their other plants in Nevada because the ore coming out of the current project isn’t ideal for on-site heap leaching.

(meaning N.G.M could do with more near-surface, oxide, heap-leachable ore - like BKB’s 0.42g/t gold for 1.2Moz shallow resource).

(source)

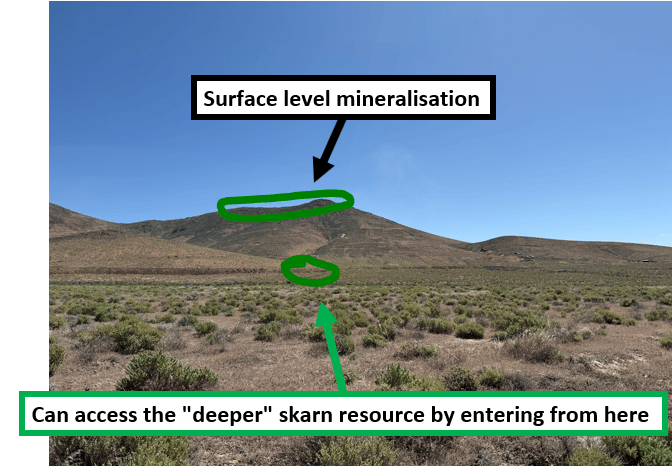

We have been to site in Nevada too

We have actually been on site and hiked up to the border of BKB’s ground and the giant pit N.G.M is operating.

When you stand on top of that hill and look in one direction, you see BKB's project and on the other side, the massive pit being mined by N.G.M:

Check out our site visit note here: JBY is surrounded by the one of the world’s biggest gold mines - here’s what we saw on site

We are not mining engineers - but it feels like BKB’s near surface resource could be mined using conventional heap leach processing and an open-pit, then once that’s exhausted an underground decline to access that deeper resource:

Black Bear Minerals

What's next for BKB?

🔄 Silver project in Texas, USA

Over the next 6 months the main things we want to see are the following:

- 🔄 Rapid restart study (CAPEX estimate)

- 🔄 Drill program - 11 diamond holes

- 🔄 Multi-element gold/zinc/lead assays

- Maiden JORC resource 🔲

- 🔲 Scoping Study starts

- 🔲 Restart Final Investment Decision (FID)

🔄 Gold project in Nevada

BKB just finished drilling this project and upgraded its JORC resource.

Over the next 6-9 months we want to see:

- 🔄 Mining studies

- Follow-up drilling on deeper targets 🔄

- 🔲 Metallurgical testwork across shallow resource

- 🔲 Scoping study (project economics)

What could go wrong?

The single biggest risk for BKB right now is "Exploration risk".

BKB is drilling its silver resource — which currently sits as a foreign resource estimate.

IF the drilling and JORC modelling fail to confirm that resource, BKB could deliver results below market expectations and the share price could re-rate down.

The second risk is "Commodity price risk".

BKB's share price moves in line with gold and silver prices.

Both are at or near all-time highs. A meaningful pullback in either would hurt BKB regardless of operational progress.

Commodity price risk

The performance of commodity stocks are often closely linked to the value of the underlying commodities they are seeking to extract. Should gold or silver prices fall, this could hurt BKB’s share price. We have already seen this happen with the lithium price and what it meant for BKB’s Canadian lithium assets in the past.

Source: “What could go wrong” - BKB Investment Memo 02 October 2025

Other risks

Like any small-cap resource exploration and development company, BKB carries significant risk, here we aim to identify a few more risks.

While the Texas silver project features substantial existing infrastructure, the upcoming dilapidation study could reveal that refurbishment costs are much higher than anticipated.

Getting a mine out of care and maintenance after a decade often uncovers hidden mechanical or structural issues that can blow out timelines and costs.

Funding these restart costs and running simultaneous programs across two states will require fresh capital. Even with non-binding government support on the table, BKB may need to execute further capital raises that could dilute current shareholders.

The Texas silver asset also currently relies on a foreign resource estimate rather than a modern, JORC-compliant resource.

There is always a statistical risk that the upcoming 2026 maiden JORC resource modeling fails to verify the historical data, resulting in a lower-than-expected grade or volume.

Furthermore, the bullish thesis for the Nevada gold asset relies heavily on its proximity to Nevada Gold Mines and their potential appetite for an acquisition.

There is no guarantee that the upcoming Barrick spin-off will ever make an official corporate play for BKB’s asset, which could leave the company holding a project it must develop on its own.

Investors should consider these risks carefully and seek professional advice tailored to their personal circumstances before investing.

Our BKB Investment Memo

Our Investment Memo provides a short, high-level summary of our reasons for Investing. We use this memo to track the progress of all our Investments over time.

In our BKB Investment Memo, you can find the following:

- What does BKB do?

- The macro theme for BKB

- Our BKB Big Bet

- What we want to see BKB achieve

- Why we are Invested in BKB

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.