What is next for the Market?

Published 03-AUG-2024 12:42 P.M.

|

14 minute read

- Commentary: TechKnow conference, Filo Mining deal, uranium

- Quick Takes: TG1, GTR, NTI, EXR

- This week in our Portfolios: IVZ, TRI, IIQ, MAN, SS1

Well, that was a rough week in the markets.

Particularly the last two days of trading.

Small cap markets are often at the mercy of big geopolitical shifts and central bank policy - fears that the US may be headed towards a recession caused the sharpest sell off on the ASX 200 in a year.

Recession fears increase chatter about rate cuts, and sometimes “bad news is good news”.

But if the news is really bad... anyway, that’s how the top end of the market is thinking for at least this brief moment.

There are silver linings though, and central bankers have plenty of rate cut ammo to use if needed.

We’re still of the view that a small cap market is experiencing some teething issues ahead of a long awaited bull run.

Valuations have been so depressed for so long (micro cap resources stocks down ~75% in two years etc.) that there isn’t much left to sell off.

And there are still great projects out there that can perform in a range of different market environments...

We remain on the hunt for new Investments, while also monitoring existing Investments.

One of the best ways to gauge specific positions is to venture into the outside world and pop into a few conferences.

It’s not who you know, its TechKnow

Attending conferences gives you a good sense for the market sentiment, as well as giving you a chance to “pulse check” how CEOs and MDs are tracking.

This week we attended the TechKnow Invest Roadshow in Melbourne where a number of small cap companies were presenting.

Running through the conference list of companies presenting, it looked very heavily skewed toward biotechs and medtech companies compared to previous years - which makes sense given the attention biotechs are getting from investors.

We have been Invested in a number of biotechs in recent years that have done well, and we took the chance to catch up with TRI and ALA while at the conference.

First up was our recent AI mental health Investment, Trivarx (ASX:TRI).

Although TRI is running clinical trials, it's really more of a ‘medtech’ stock than a biotech.

TRI has developed a screening tool that analyses a patient’s sleep data and screens for mental health conditions like depression.

TRI has the world’s largest database of sleep study data labelled with a patient’s mental health status to train its AI algorithm on and screen patient data.

TRI has been using AI for years (not just this year when it was in vogue with investors) for its algorithm development, and has been successful so far in Phase II clinical trials, demonstrating its much more effective than traditional screening tools.

We saw TRI Chief Operating Officer, Kai Sun present on what the company is doing to improve screening for depression using data collected while patients sleep - click on the link below the image to watch Kai’s 15 minute presentation.

Watch TRI’s full TechKnow presentation

TRI’s Kai spoke fluidly about the recent strong Phase 2 trial results - even mentioning that at a recent major sleep conference in Texas that he was approached by a US military commander who said he was really amazed at what TRI has been able to achieve.

Clearly, the prospect of bringing to market the first FDA approved AI screening tool for depression is starting to get the attention of a wider audience.

We hope that continues, and the company is able to expand into screening for different mental health disorders, as well as one day making it into wearable devices such as Apple Watches, Fitbits etc.

We see the expansion into mass market consumer wearable devices like Apple Watches and Fitbits as the ultimate blue sky outcome for TRI’s technology - and a key part of our long term investment thesis for the stock.

The idea behind the technology is that “sleep is a window into a person’s mental health”.

If TRI can prove this with bankable clinical data, it could become a very important technology in the future.

Another ResApp founder joins TRI

Also during the conference, we also got a chance to spend some time chatting with TRI’s new non-executive director Dr Tony Keating.

Tony was one of the co-founders of ResApp, and was CEO and Managing Director of the company up until its $180M acquisition by Pfizer in 2022.

Roughly 10 years ago ResApp developed a diagnostic tool that could detect and identify various respiratory conditions based on the sound of a cough made into a smartphone.

ResApp began at a University of Queensland start up and did a backdoor listing in 2015 at a market cap of just ~$11M and at ~2c.

In 2022, seven years after listing, Pfizer acquired ResApp for ~$180M at a share price of 20.8c:

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

The FDA approval process for ResApp was long and had a few false dawns over the years, but was ultimately successful.

We think that Dr. Keating’s FDA experience from ResAp will be extremely valuable for TRI as it goes through its own process with the FDA.

Following the ResApp acquisition by Pfizer, Tony spent almost a year as a Managing Director at Pfizer, reporting directly to the New York based executive leadership team of the $178BN pharma giant.

During his time at Pfizer, Tony provided strategic input on digital health technology to Pfizer leadership.

After no doubt doing his own due diligence on TRI, we think it's a great sign that Tony has joined the company and hitched his reputation to its success.

We see Resapp as the blueprint for TRI’s future success and think Tony is definitely the right person to have on the TRI board, with his experience driving one of the biggest medtech success stories on the ASX in the last few years.

Understanding how a big machine like Pfizer operates, and having those networks and relationships could prove handy for TRI.

ALA’s cancer killing technology on track for Phase 1 trials

At the conference we also had a chat with the ever-ebullient Dr. Michael Baker, CEO and MD of Arovella Therapeutics (ASX:ALA) and Chief Operating Officer Dr Nicole van der Weerden.

Dr van der Weerden is heading up ALA’s clinical pipeline and clearly has a deep knowledge of the biotech space after chatting to her.

Dr. Michael Baker even pointed out that the recent ALA share price run correlates with Dr van der Weerden’s appointment.

It reinforces to us that behind every great CEO or Managing Director is a great hard working team that doesn’t necessarily get all the limelight, but is equally important to the success of the company.

ALA has been one of our best performing stocks in recent years, and there is no doubt that Baker presents well as the company CEO and has captured investors attention.

This quarter Baker hit the conference circuit hard, presenting at Bio2024 in SanDiego, then again in Singapore, Hong Kong, non-deal roadshows around Australia and finally at TechKnow this week.

At TechKnow, Baker went through in detail all of the benefits of ALA’s cancer killing technology which is set for phase 1 clinical trials next year.

You can watch the full ALA presentation here:

Watch ALA’s full TechKnow presentation here

ALA has been looking good on the charts, moving from 10.5c to ~17c in the last three months as the company’s Phase 1 trial for blood cancer rapidly approaches.

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

ALA had $12.7M in cash at June 30th, and is now capped at ~$173M.

After investing in ALA a few times - at 3.8c, 2c, 4.5c and 10c, ALA has been one of our best performing stocks in the Portfolio over the last couple years.

We think there could be more to come from the company especially as Phase I clinical trials approach.

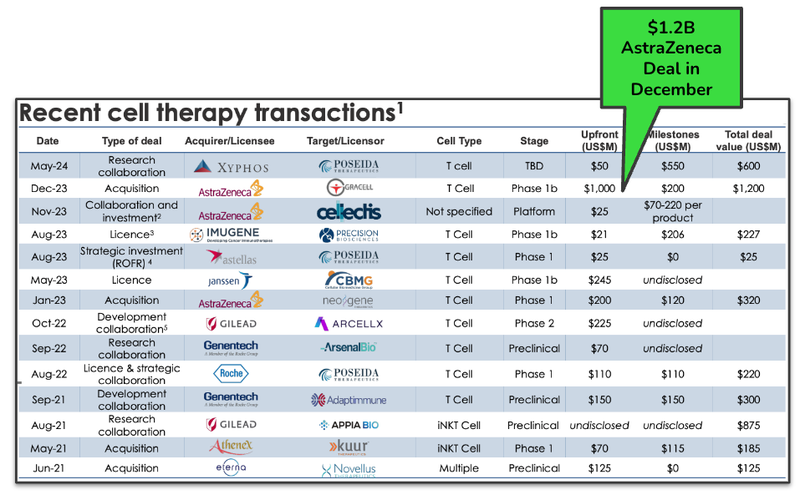

Particularly considering some of the dollar values attached to deals in the cell therapy space recently.

One of these deals was a US$1BN cash up front deal with $200M in milestone payments that was done in December last year between Astrazeneca and Greycell:

We are looking forward to ALA continuing to advance its cell therapies... if it doesn't get taken out first.

Quarterly season ended yesterday...

Normally leading up to the quarterly deadline, companies with low cash balances go into trading halts and raise capital to avoid that quarter end sell off.

This quarter we saw a lot more companies running a sub $1M cash balance - something we haven't seen for a while.

The last time companies were cutting it this close was back in ~2019 when the market was really tough especially in the small caps space.

We think it says a lot about the current state of the small cap markets and the ability for pre-revenue businesses to raise capital... especially amongst the junior explorers.

There was downwards selling pressure for companies that had a lower than expected cash balance compared to a higher market cap.

Interestingly, the companies with extremely low cash balances had relatively stable share prices...

Usually the market would punish these stocks with brutal selling in anticipation of a capital raise.

This time around it was the companies with much bigger market caps that announced lower than expected cash balances that were punished the most.

That tells us that share prices for the micro / small caps that are cutting it close could be trading near their bottoms and just like we saw in 2020 after the COVID panic - a successful capital raise might actually be a share price catalyst for the company.

Who would have thought...

Big copper M&A to flow into the junior end of the market?

This week saw BHP and Lundin mining announce the takeover of Filo Mining for US$3BN.

It's a huge deal (one of the biggest we have seen in a while) at the big end of mining...

For investors in junior mining companies, deals like this are an example of the blue sky opportunities for early stage companies.

Filo Mining came onto the Canadian markets in 2016 with a CAD$20M raise at $2 per share and a market cap of ~CAD$130M at the time.

Like most of the stocks on the ASX/TSX it was just another junior miner scratching around looking to explore, define and develop its project.

8 years on and the company is being taken over at CAD$30 per share in an all cash offer valued at ~$3BN.

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

These mega deals don't happen often but are a good reminder for us as to why we like the junior exploration space...

Because with a bit of luck, anything could happen.

Especially now, with sentiment so low for these high risk high reward companies, we think it is a good time for identifying high-value projects that just two years ago would have been much more expensive.

The second order impact of that deal is that there is now US$3BN of cash in the hands of investors who will be looking for the “next Filo Mining”...

... and the capital merry-go-round can continue.

We are hoping deals like this bring some life back into the smaller end of the market.

Background rumblings in uranium...

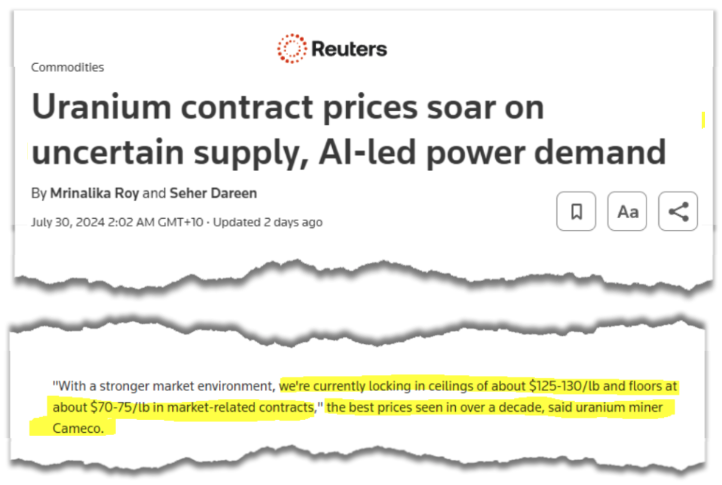

This week we came across this in an article from Reuters:

The key quote in case you can't read the screenshot above:

"With a stronger market environment, we're currently locking in ceilings of about $125-130/lb and floors at about $70-75/lb in market-related contracts," the best prices seen in over a decade, said uranium miner Cameco.

You can read the full article here.

The comments from Cameco are references to prices being achieved in the uranium contract market.

Most uranium is sold through long term supply contracts between producers and utilities.

Most of those deals have 3-15 year terms and deliveries often start multiple years after a deal is signed.

The spot price is more a reflection of where the marginal uranium lb is sold but is a good reflection of where supply and demand sits right now...

The term market is a good reflection of what utilities (big uranium buyers) are willing to pay in the long run.

So the news this week of uranium contract prices hitting 16-year highs isn't something that should go unnoticed. It means the big buyers are willing to lift bid prices on long term deals in exchange for supply certainty.

For context, the term prices this week of ~US$79/lb are the highest since 2008.

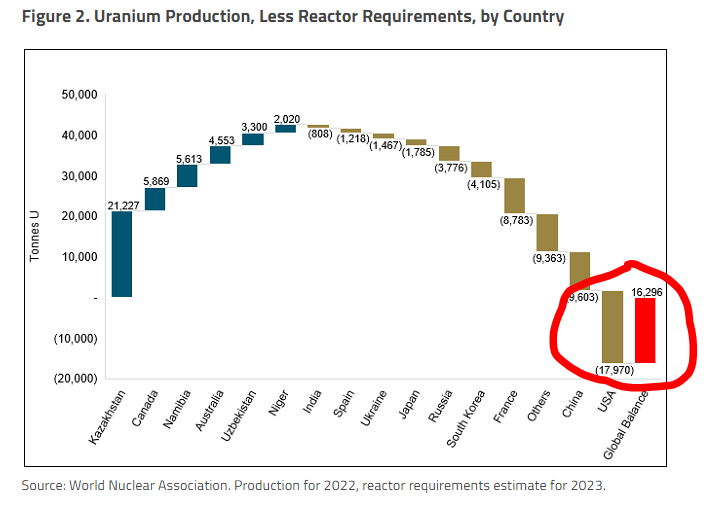

We recall a note by Sprott back in late 2023 which talked about the world going into a uranium contracting up cycle which will mean we are likely to see more of this type news out in the market over the coming years.

That article especially referenced how most of the contracting was being done outside of the US and the US would eventually need to catch up with the market given it has the world’s biggest nuclear reactor fleet.

(Source)

We think all of this will just mean uranium supply in the US becomes even more in demand as time passes.

That bodes well for our US uranium Investments, in particular GTi Energy (ASX:GTR).

GTR is in the middle of drilling at one of its projects in Wyoming.

GTR’s projects sit ~16km away from Cameco’s Smith Ranch-Highland plant (the USA’s biggest ISR uranium production facility).

The company is currently undertaking a rights issue raising up to ~$2M at $0.004, with a one for three option with an exercise price of $0.01 and four year expiry.

As long term GTR holders, we plan on participating in the offer.

There’s also an options offer for GTROA holders that looks pretty interesting that we will participate in.

The ex-date for the GTR offer is Friday 9th August, which means new buyers of the stock can participate in these offers, as long as they hold GTR before that date.

What we wrote about this week 🧬 🦉 🏹

Invictus Energy (ASX:IVZ)

IVZ announced a US$10M strategic capital raise backed by Zimbabwe’s Sovereign Wealth Fund, the Mutapa Investment Fund.

A big bonus was that the shares issued from the capital raise are all going to be traded on the Victoria Falls Stock Exchange (VFEX) in Zimbabwe.

That (hopefully) means the placement shouldnt bring any selling pressure onto the ASX.

With cash in the bank we are looking forward to IVZ getting its Petroleum Production Sharing Agreement (PPSA) and seeing what comes from the ongoing farm-out discussions with potential strategic partners.

Next though, we want to see IVZ appraise its discovery.

Read more: ⛏️ IVZ Secures Sovereign Wealth Fund backed Strategic Investment. PPSA and Farm-Out very close. Mukuyu-2 Flow Test Imminent.

Inoviq (ASX:IIQ)

This week we put out a note on IIQ just after the company released its quarterly report.

IIQ is our fifth biotech addition in three years.

IIQ is looking to apply its exosome technology to develop diagnostics and treatments for cancer and Alzheimer's.

IIQ is backed by Merchant Capital Group AND three of the company’s four directors (including IIQ chair David Williams) are from ASX biotech success story Polynovo which has a market cap in the billions.

We are hoping the team can repeat the Polynovo success with IIQ...

Read more: ⛏️ News in the queue for IIQ - upcoming share price catalysts...

Mandrake Resources (ASX:MAN)

Lithium explorer MAN put out its June quarterly report this week which showed a huge $14.9M cash balance.

Huge for a company of its size - MAN’s market cap is hovering close to its cash backing...

We are looking forward to the next 6 months of newsflow from the company, and with no need to raise capital, hopefully MAN can re-rate - a bit of luck from the lithium market would also help.

We think MAN’s upcoming JORC resource from its US lithium asset could be a big catalyst for the company.

Read more: ⛏️ Lithium turnaround opportunity? MAN close to cash backing - JORC resource due in coming weeks

Sun Silver (ASX:SS1)

SS1 hit a 296g/t silver intercept 115m away from its existing resource boundary this week.

Note this impressive step out result was from an XRF reading - we will have to wait for lab assays in a few weeks to confirm the final grade.

Its a great early sign though, and SS1 has plenty more drilling still to do.

IF SS1 can keep hitting high grade silver it could deliver a resource upgrade that surprises everyone...

Read more: ⛏️ SS1 finds silver in step out hole - bring on the assays...

Quick Takes 🗣️

TG1 finished gold drilling in WA

GTR’s first batch of uranium drill results

Good data from NTI’s Rett Trial

EXR back on site at QLD gas project

TG1 kicks off first ever geophysical survey at copper project

Have a great weekend,

Next Investors

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.