$83M KAU to become a 30,000 oz per year gold producer. Gold at all time highs…

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 4,665,000 KAU shares and the Company’s staff own 35,000 KAU shares at the time of publishing this article. The Company has been engaged by KAU to share our commentary on the progress of our Investment in KAU over time. Additional placement shares will be included in disclosure post transaction approval vote at upcoming EGM.

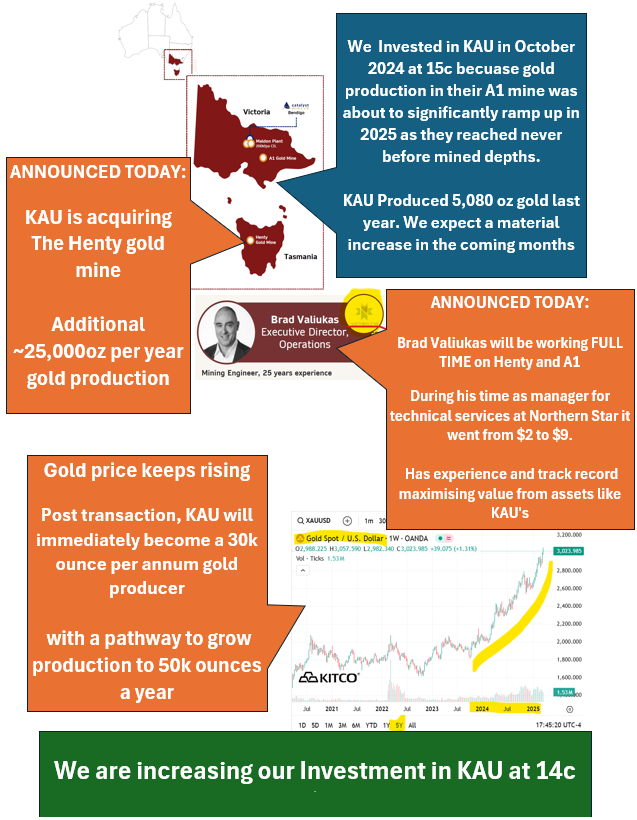

Our gold producing Investment Kaiser Reef (ASX:KAU) just announced an acquisition that will see it immediately become a 30,000 ounce per annum gold producer.

That’s A$144M in revenues per year, if the gold price stays at A$4,800 per ounce.

(KAU will be capped at A$83M post transaction, with $27M cash)

The new gold mine KAU is buying from $1BN Catalyst Metals has more than 8x KAU’s current gold production based on its last quarterly...

KAU reckons it can pay back the upfront purchase price with gold production cashflow inside 12 months.

Combined with its expected ramp up in gold production at its existing Victorian assets, KAU is on a pathway to grow production to 50,000 ounces a year.

Just as gold keeps hitting records highs.

KAU is acquiring the Henty gold mine in Tasmania - a profitable, high grade underground Tasmanian gold mine with over $100M of project infrastructure in place.

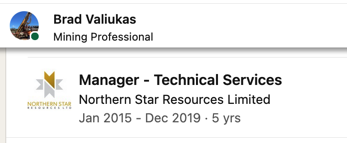

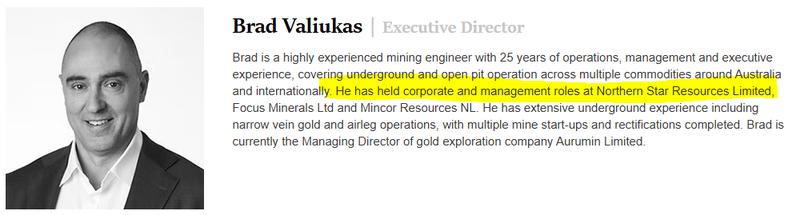

And with the Henty acquisition, KAU director Brad Valiukas is moving into the role of full time ‘Director of Operations’.

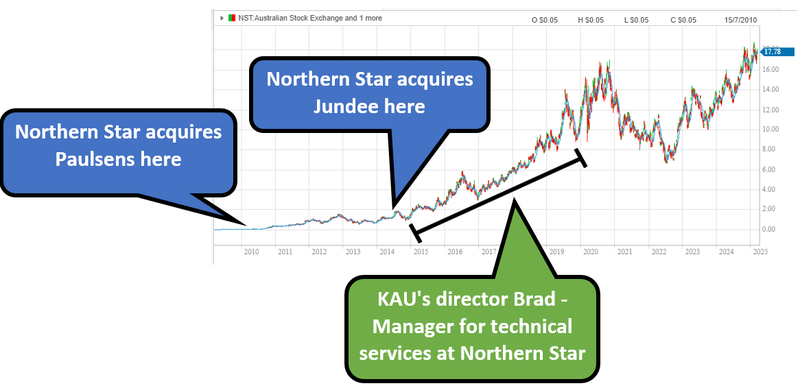

Brad was Manager for Technical Services at Northern Star Resources during its formative 2015-2019 growth period - in charge of optimising and growing its assets - during which period Northern Star’s share price went from ~$2 to $9 per share. (Northern Star is now capped at $20BN).

Brad will now be full-time at KAU, focused on optimising mine production and reducing costs at KAU’s A1 and Henty Mines.

We are putting more cash into the $30M KAU placement at 14c that is partially going towards funding the $15M upfront cash component of the acquisition.

Post transaction and capital raise, KAU will be capped at ~$83M and have ~$27M in cash (which includes a $10M loan facility).

As part of this deal, KAU has also secured a JV partner on its Victorian processing plant and new 19.9% shareholder:

$1BN capped gold producer Catalyst Metals.

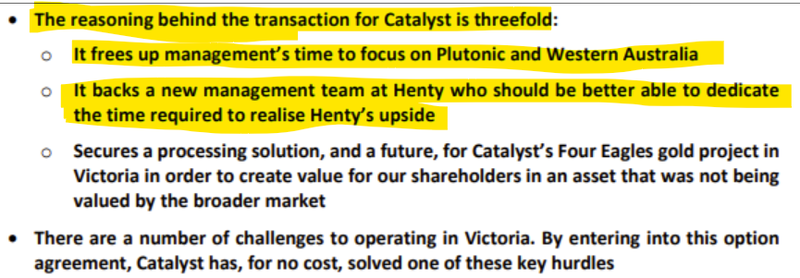

The key reasons behind this tie up come down to Catalyst and our Investment KAU being able to work together in the future in a big win-win for both companies.

And Catalyst was too distracted with its bigger gold assets to maximise the value at Henty.

Here is the reasoning from Catalyst Metals:

(Source)

To get a sense of the company transforming scale of KAU’s binding acquisition:

We originally invested in KAU at 15c in October at a ~$39M market cap because its A1 mine in Victoria was on the cusp of ramping up production during 2025.

And we thought the gold price would go up - which it did... and keeps doing.

Last quarter KAU’s current A1 gold mine produced 841 ounces...

KAU’s new Henty gold mine produced 6,594 ounces, and is profitable.

And after years of investment in improving access to the A1 gold mine, KAU is just getting to the fresh virgin zone to mine, which means production is only going to grow from here.

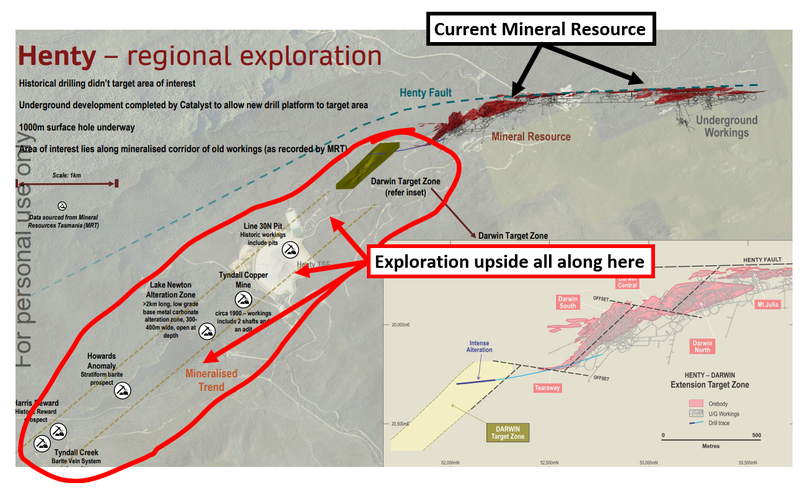

Meanwhile at Henty there are a number of exploration targets to go after and push the current mine life of ~5 years out further.

KAU is becoming a multi-asset gold producer just as gold prices hit all time highs.

Post transaction, KAU will immediately become a 30k ounce per annum producer with a pathway to grow production to 50k ounces a year.

KAU’s Managing Director, Jonathan Downes and Executive Director of Operations, Brad Valiukas will be hosting a webinar today to run through the deal at 12:00pm AEDT.

We will be listening in.

Click here to register for the webinar

In today’s note we will cover:

- The 8 key reasons why we like KAU’s new asset.

- More details on the acquisition and what KAU is paying for it.

- And why we think gold M&A can work out well if the planets align for KAU.

Once KAU completes the acquisition we will also put out an updated KAU Investment Memo where we will update our reasons for Investing in KAU, what we want to see the company achieve and the risks to our Investment Thesis.

Keep an eye out for that in the coming weeks.

Here’s what KAU will own post transaction

KAU is for the first time ever mining virgin sections of its Victorian A1 gold mine, and can now supercharge its cashflows with Henty in Tasmania.

The bet here is the gold price stays at current levels or keeps going up - and KAU becomes extremely profitable.

One year of production (30k ounces) at current gold prices (A$4,800/oz) would be $144M in revenues for KAU.

Of course gold mining can be a risky endeavour - the gold price can go down, and costs can go up unexpectedly - success is not a guarantee.

After the Henty acquisition is completed, KAU will hold:

- Gold mine in Victoria (A1 Mine, 100% owned) - The A1 gold mine is where KAU just started mining never before mined parts of the project. KAU is targeting production of ~20k ounces per annum from this mine.

- Gold mine in Tasmania (Henty, 100% being acquired) - a “plug and play” type asset, already producing ~30k ounces per annum and with over 5+ years of mine life in reserves (10+ in resources).

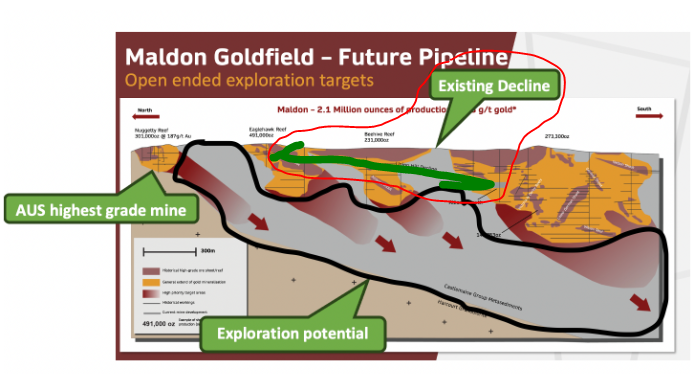

- Gold exploration in Victoria (Maldon, 100% owned) - Inferred JORC resource of 1.2Mt @ 4.4g/t gold for ~186K ounce gold resource and reserve with exploration upside.

- Gold plant in Victoria (Maldon, option to go 50-50 on this with $1BN Catalyst Metals) - Running at 20-30% capacity with the opportunity to ramp up to 350k tonnes per annum. Plants in Victoria are almost impossible to permit nowadays... anyone looking to roll up assets in Victoria could see this as a strategically important asset.

Post-deal KAU will be capped at $83M at 14c.

That brings KAU closer to the ~$100M level where the company becomes more investable for institutional funds.

Fund managers don’t (really they can’t) invest in stocks that are too small because of liquidity/size limitations from the fund.

IF KAU can deliver a few strong quarters into record gold prices, there is a chance the stock re-rates to a market cap >$100-150M which is the level where we think buying from institutional gold funds can come into play.

This is another key reason why we liked today’s deal...

Note: KAU’s acquisition is pending a shareholder vote at an EGM, the below reasons assume that the acquisition proceeds.

9 reasons why we like KAU’s new project

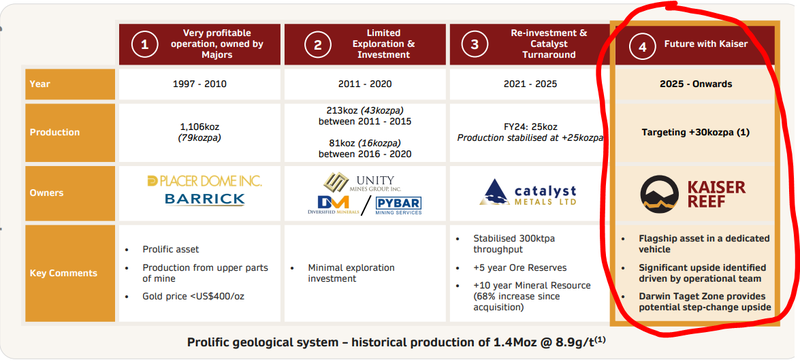

1. Producing mine with existing resources + reserves base

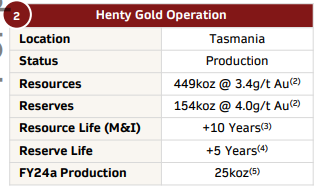

The Henty gold operation is currently producing ~5,000 to 6,000 ounces of gold per quarter. The project also has 5+ years of mine life in reserves and over 10 years of mine life in resources.

(Source)

2. The project could generate ~$120M in revenues per annum at today’s gold price

Henty produced 25k ounces in 2024 (KAU is looking to grow this number in 2025). At current gold prices, that would be ~$120M in revenues per annum. With all in costs averaging ~A$2,500/oz for Henty in 2024, KAU should be able to turn those revenues into free cashflows in the current gold environment.

(Source)

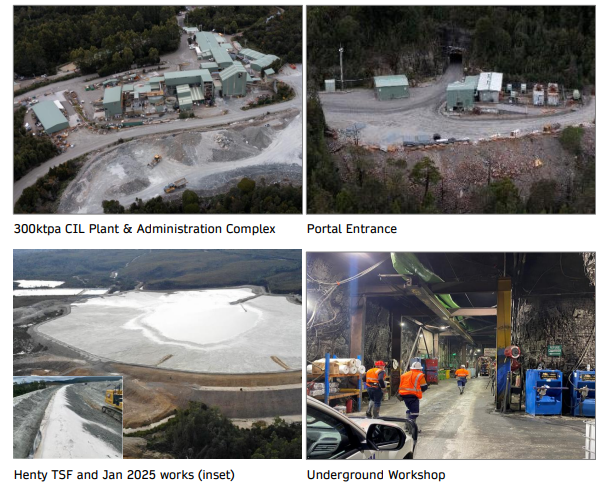

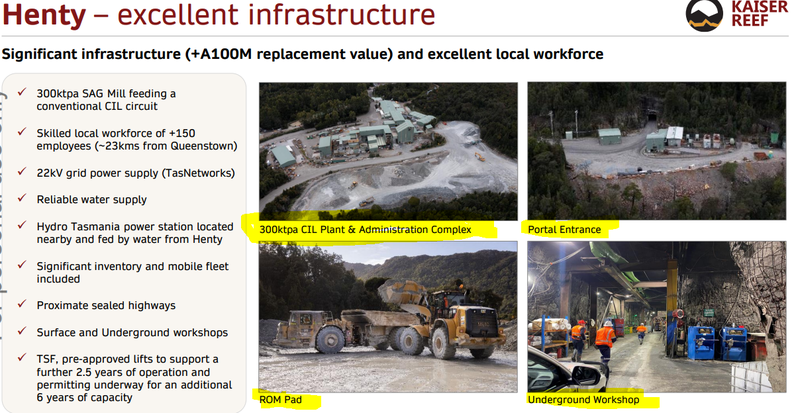

3. Henty has $100M+ of existing infrastructure

The Henty Gold Operations has an existing 300ktpa processing plant, a mining fleet/inventory and tailings storage/underground declines with replacement value greater than $100M. KAU gets to benefit from all the capital that’s gone into the asset to date.

(Source)

4. Exploration potential untapped to date

KAU is taking over the project after previous operators focused on ironing out production efficiencies. With the cashflow from operations at record gold prices, KAU can drill out the project to extend the project's mine life.

5. Acquiring a big gold asset has worked for other ASX companies

Northern Star was capped at $7M when it made its first big acquisition for $40M. 25 years later and several other acquisitions later Northern Star is capped at $20BN.

$1.7BN Bellevue Gold also started with a market cap of ~$2M before making acquisitions to become what it is today. There is a precedent for gold M&A to work in the long run.

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

6. KAU’s Exec director Brad Valiukas has experience maximising value from assets like these and is now working full time on Henty and A1

Brad was Manager for Technical Services at Northern Star during 2015-2019. His role was spread across the entire Northern Star portfolio and he helped set up the foundations for assets like Jundee to be the cornerstone of the $20BN producers project portfolio.

Certainly a good guy to have on the KAU team, extracting the most profits from Henty and its Victorian assets.

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

7. KAU now has two operating mines

KAU will now have a diversified production profile. Once the A1 mine production lifts to closer to Henty’s production, if one mine has a bad quarter, the other one could fill in the gaps temporarily. A smoother, more predictable production profile may attract institutional investors who want less volatile gold production exposure.

8. KAU market cap can grow to a size where institutional money can come in

The ASX gold space has had a lot of M&A deals get done over the last 12-18 months. Most of those deals are to grow in size/scale as quickly as possible so that the producers can attract investment from institutional/passive funds. KAU post-deal will have a market cap of $83M, which is approaching a level where these funds may be able to invest.

9. KAU is acquiring a non-core asset from $1BN company

Vendor of the asset Catalyst looks like it wants to focus all of its time and effort on its WA assets. KAU can now take Henty and give it the time & capital it needs to be a big part of a company’s portfolio. What might not be core for a $1BN company, can be a great foundational asset for a <$100M producer like KAU.

More on KAU’s new Director of Operations - he has done something similar before - at Northern Star

We are backing new full time executive Director of Operations Brad Valiukas to optimise operations, expand reserves and grow production just like he helped Northern Star do...

Northern Star is a $20BN mega producer that was once a tiny $7M capped explorer.

KAU’s new Director of Operations was at Northern Star as a technical services manager from 2015 to 2019, where he led multiple technical and operational improvements assisting in the turnaround of Northern Star’s foundation mines following their acquisition...

(Source)

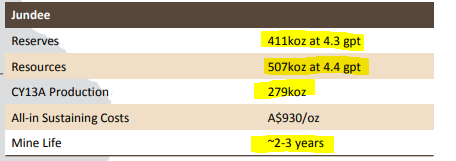

Brad was there when Northern Star picked up the Jundee asset off Barrick.

Similar to the acquisition KAU announced today, Jundee was prised out of a bigger company which couldn’t properly realise the value of the asset.

When Northern Star picked it up, it had 2-3 years of mine life left...

To this day (10 years later) that asset still produces over 250k ounces per annum for Northern Star...

Like Northern Star was when it acquired Jundee, KAU is a more nimble smaller company.

Brad is now full time and able to focus significant attention on the Henty Project.

As Manager of Technical Services at a gold mine, Brad would have been responsible for overseeing and optimizing all technical aspects of the mine, including mine engineering, geology, planning, and safety, while ensuring compliance and driving operational excellence.

Now he will be full time using these skills on A1 and Henty for KAU.

During Brad’s time at Northern Star, the company went from $2/share to $9...

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Now we're not saying Brad was solely responsible for Northern Star’s growth.

But it's definitely a good sign when one of the key operations guys was around for an incredible growth story, and is taking all of that experience and lessons learnt to the next venture - KAU.

We are hoping Brad’s operational nous can help transform KAU into a producer with much bigger scale than what it is today.

More on the Henty gold mine

KAU is acquiring a project that produced 6,594 ounces of gold in the December quarter at an All-In Sustaining Cost (AISC) of A$2,631 ounce.

That means a margin of ~$14M in just 3 months...

The project has infrastructure that would cost >$100M+ to replace.

(Source)

The project also has 5 years of mine life and ~10 years in resources... which means it will be bringing in cash to KAU from the get go.

From Henty alone, KAU is targeting 30,000 ounces of gold production per annum.

AND there is still plenty of untouched exploration upside on the project - which KAU can fund with cashflows from the gold its production...

More on Catalyst Metals - the Henty vendor and KAU’s new major shareholder

KAU is buying the Henty gold mine after years of capital spent to get the project into profitability by the vendor $1BN Catalyst Metals.

Catalyst will also emerge as a 19.9% strategic shareholder of KAU with an option to form a 50-50 Joint Venture partnership on KAU’s Maldon processing plant.

Catalyst choosing to take scrip for a large part of the deal tells us that they clearly want to retain exposure to Henty (and likely that they see value in KAU’s other assets).

Today’s deal will transform KAU into a gold producer with targeted production of 50,000+ ounces of gold per year across its Victorian and Tasmanian assets.

It also means KAU holds key processing infrastructure across two different gold hubs:

- In Victoria, where it's notoriously difficult to permit a new processing plant and where the gold industry is coming alive again... AND

- In Tasmania where the same can be said about permitting...

When all is said and done, Catalyst will hold 19.99% of KAU... a good signal they want to retain exposure to Henty, and maybe they see value in KAU’s other assets too?

... In fact we think Catalyst taking a big equity component in KAU has a lot to do with KAU’s Victorian assets.

KAU is about to start producing gold from never before mined parts of its A1 Mine, AND it owns a 350ktpa processing facility in Victoria...

That plant is an important base for anyone looking to roll up a portfolio of gold assets in Victoria... (Maybe that’s the long term play for $1BN Catalyst who already own projects in Victoria)

(Catalyst’s 163kt gold resource in Bendigo is just 45km away from the 350ktpa gold processing facility)

For us, Catalyst taking a cornerstone position in KAU is a big part of today’s deal...

Whatever happens, we think KAU’s position as “gatekeeper” to Victorian gold (with its operating 350ktpa processing plant) puts it in a strong position.

And the gold industry in Victoria looks like it is coming alive again...

It’s easy to forget, but Victoria is actually home to the Fosterville mine... an anchor asset in the world’s biggest gold producer ($84BN Agnico Eagle).

Over the last ~2 years Victorian gold exploration has picked up in a big way, so we think there is a lot of strategic value in KAU’s processing plant going forward.

Now that $1BN capped Catalyst Metals has taken a strategic ~19.99% stake in KAU, and an option on 50% of the production plant, we think that KAU is set to play a major role in the Victorian gold region going forward.

Exploration is still a big part of the story with producing ounces

One thing successful ASX gold producers have in common is that they used existing cashflows to fund exploration.

Dig up the gold, sell the gold, find more gold... rinse and repeat.

Exploration success has kept many gold mines producing well beyond the initial mine life identified by the discovered resource or reserve.

Hundreds of millions of dollars in capital is spent on project infrastructure, and so operators are incentivised to do as much drilling in and around the project to try and make new discoveries.

New discoveries that can feed straight into the existing infrastructure.

As mentioned earlier, at Northern Star’s Jundee mine, a 2-3 year mine life has become over 10 years of production with exploration success.

14 years after Northern Star acquired the project, they produced ~270k ounces in one year - at today’s gold prices that's over A$1.2BN in gold...

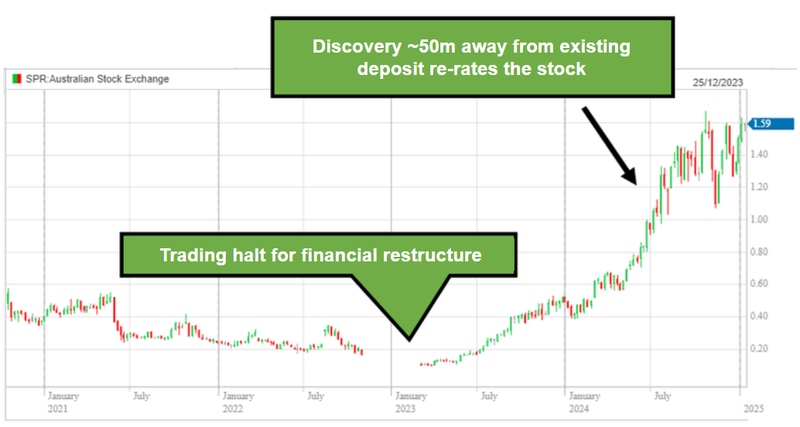

A more recent success story on the ASX has been Spartan Resources (the old Gascoyne Resources).

Spartan went from 10c to ~$1.80 per share.

Spartan is now an M&A target of Ramelius Resources in a deal worth up to $4.2BN.

Spartan (Gascoyne) had been restructured multiple times before in 2022 it drilled a hole ~50m away from its existing JORC resource (which had been producing gold for years) changed the company’s fortunes.

Previous drilling had missed a giant discovery, literally a stone's throw away from its old open pit...

Spartan’s new discovery and all the drilling after it took the company to a market cap close to $2BN.

Past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Exploration upside is still a big part of the KAU’s story on the asset being acquired today and its Victorian assets.

Here are the parts of KAU’s Tasmanian project that are open for exploring:

And here is a visual of KAU’s Maldon assets in Victoria next door to its processing plant that haven't had any widescale exploration done on them:

We are hoping the cashflow from both its Henty and A1 mines can be used to run bigger exploration programs across its projects and (fingers crossed) make new discoveries.

More on Northern Star’s acquisition model - can KAU follow a similar pathway?

Big acquisitions in the small cap gold space are pretty common AND there is a long hall of fame of successful gold M&A stories on the ASX.

Some of the biggest gold producers on the ASX were born out of transactions like KAU’s deal today.

(we are hoping that KAU can follow in their footsteps)

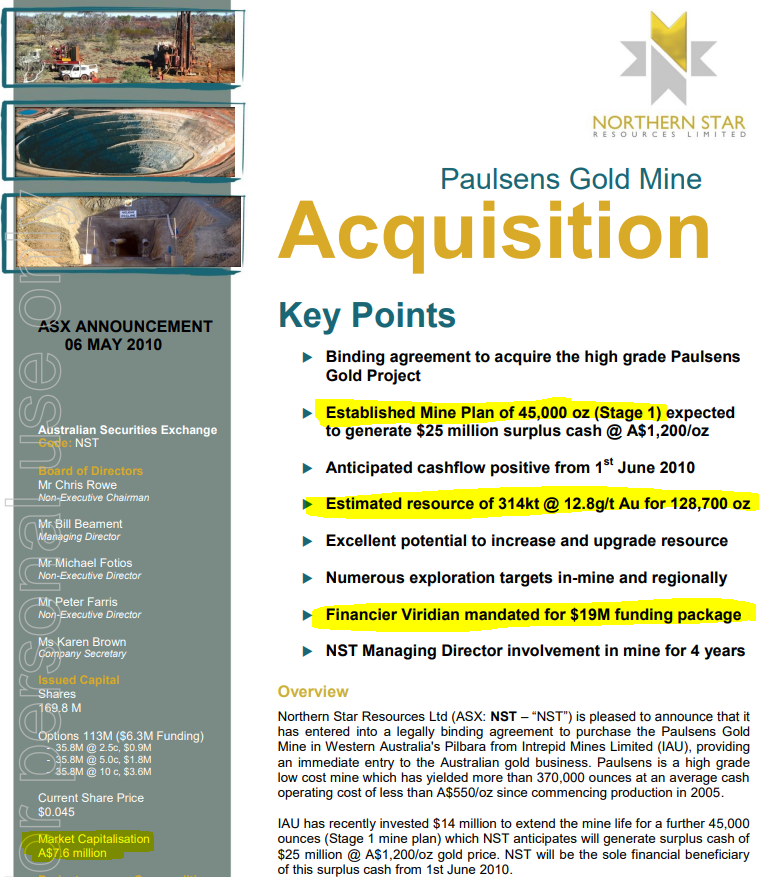

Anyone who has been around markets for 20+ years will remember the Northern Star Paulsens acquisition.

Back then Northern Star was capped at just ~$7.6M, but Northern Star paid up to ~$40M for Paulsens which was a previously producing mine with a modest resource...

Paulsens had been operated as an underground mine and was scheduled to be wound down just before Northern Star came into the project.

The Paulsens deal at the time was a big change in scale/operations by Northern Star.

The market also saw it as way too big for Northern Star to digest.

(Source)

Similar to KAU’s deal today, the project had a mill, and infrastructure (worth more than Northern Star’s market cap), and Northern Star’s management had their own ideas about how to make money from the project.

Northern Star took that project and went on to become one of the biggest gold miners in the world today (only 15 years after that deal...)

Interestingly, there is a connection between KAU, the foundations of the Northern Star story and Barrick...

As we pointed out earlier, Brad Vallukas, KAU’s new full time Executive Director of Operations, was Northern Star’s Technical Services Manager between 2015 and 2019.

In that role he was working across all of Northern Star’s assets - here is a list of the things Brad would have likely been in charge of while at Northern Star:

(Source - Google)

Sounds like the perfect skillset to optimise and grow production at A1 and Henty...

Jundee was acquired by Northern Star from Barrick for $82.5M, at the time the project had only 2-3 years of mine life left (similar to KAU’s Henty deal).

(Source - Presentation 13 May 2014)

Brad was a part of the Northern Star team that took Jundee and set it up to become what it is today...

10+ years later Jundee is STILL producing at ~250k+ ounces of gold per annum and has almost 6M ounces of gold in resources today...

So Northern Star was able to turn that 2-3 year mine life into a project that has printed billions of dollars in cash for the company for 20+ years...

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

We are hoping in 5 or 10 years' time we will look back at today’s deal by KAU the same way Northern Star holders look back at those deals from the early days of the company.

Hopefully Henty and KAU’s Victorian assets are part of the foundational assets that help transform KAU from small cap to mid-cap (and fingers crossed, one day a mega cap producer).

The bet from KAU is pretty simple.

KAU has two assets that can work very nicely in a high gold price environment.

Across the two projects, KAU could spit out up to 10,000 ounces of gold each quarter...

At a gold price of A$4,800 that could mean ~$48M a quarter in revenues for $83M KAU...

And if KAU can keep AISC down around $2,600 that could mean ~$22M profit per quarter.

IF the gold price does something silly like spend a couple of years at around A$8,000 per ounce (just speculation by us) then the profit numbers could look really big for KAU.

Disclaimer* These profit numbers are all speculation on our end, the gold price could fall from here. Production numbers could also be a lot lower than expected OR costs could be higher. A lot will need to go right for KAU to hit the numbers we are saying.

What did KAU pay for the asset?

There are a few different moving parts to the deal.

KAU is paying upfront $15M cash to Catalyst and $15M in equity which gives Catalyst a 19.99% shareholding in KAU.

KAU also has to pay a deferred component of 50 ounces of gold per month (capped at 3,000 ounces) starting 6 months after the deal closes.

On top of that KAU also has to pay a $3.9M environmental bond over a 12 month period.

In total the upfront cash cost to KAU is $15M, the remainder is a mix of equity and deferred payments split over 12+ months.

How is KAU paying for the asset?

To pay for the deal, KAU is raising $30M cash via equity and $10M via debt facility.

The capital raise is at 14c per share - we participated in this raise.

As for the loans, KAU is taking out two for a total of $10M, split as follows:

- $8M gold loan and offtake deal - KAU will be repaying the financier Auramet in gold over an 18 month period. At the end of the 18 month period, KAU will sell 100% of its gold production at market rates to Auramet as part of an offtake deal built into the loan.

- $2M prepayment facility - where KAU can tap this funding ahead of delivering gold to Auramet at a small discount to the spot price.

The final part of the deal - an option to for a joint venture for KAU’s VIC processing facility

Catalyst will have an option to acquire a 50% interest in the Maldon gold processing plant for $1.

The agreement has a lot of different clauses that look to us like it's mainly aimed at protecting both company’s access to capacity at the mill.

There are also explicit provisions in there about increasing the capacity of the mill through loans from Catalyst.

Clearly, Catalyst wants ownership in the mill and wants pre-agreed terms with KAU for expanding the mill’s capacity.

Given the processing plant is currently operating at well below its full capacity (around 20-30%), we think there is an obvious longer term aspiration here from Catalyst.

We will do a deeper dive on this agreement IF/when Catalyst chooses to exercise the option.

For now it's a bit of a wait and see on the plant JV.

What we want to see next from KAU:

In the short term we want to see two things:

1. Acquisition of the Henty Mine in Tasmania finalised

Milestones:

✅ Capital raise

🔄 Shareholder vote to approve the transaction

🔲 Transaction completed

2. Exploration drilling and increased production at the A1 Mine in Victoria

Milestones:

✅ Drilling commences

🔄 Drilling results

🔄 Decline construction progress

🔄 Mining of virgin ground commence

🔲 Increased average gold grade processed

What are the risks in the short term?

The two key risks for KAU in the short/medium term are “development/delay risk” & “deal completion risk”.

Development delays risk is relevant here because KAU has ongoing costs from operating its processing facility AND on decline development work.

IF decline development is delayed or takes a lot longer than expected it could mean KAU goes longer periods without production revenues.

We think the market could perceive this as a negative and start to price in future capital raises.

Development/delay risk

Should any or all of the above risks materialise, KAU could wind up stuck in “development purgatory” where newsflow dries up and the project remains stagnant for a prolonged period of time, hurting the share price. Additionally, if delays occur in terms of material newsflow, the market could turn on KAU.

Source: What could go wrong? - KAU Investment Memo 21 October 2024

Deal risk is a new one that sits outside of our Investment Memo.

There is always a risk that the deal does not go ahead for whatever reason. If that were to happen then we would expect the KAU share price to re-rate lower.

We list more risks to our KAU Investment Thesis in our Investment Memo here.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.