VN8 following the telco playbook for growth

Aussie telco Uniti Group was one of the big ASX success stories in recent years.

The company grew from a $32M small cap at its 2019 IPO into a $3.6BN takeover in just three years.

Who knew a telco could grow so big so quickly.

Whilst not doing exactly the same thing as Uniti Group, our telco Investment Vonex (ASX:VN8) is delivering a similar strategy where it grows value via acquiring smaller players.

Just like Uniti Group, VN8’s growth path could lead it to getting taken out by a much bigger player - ideally at many, many multiples of its current $25M market cap.

Uniti IPO’d in 2019 at 25 cents per share and a market cap of $32M.

Over the next 12-18 months, Uniti acquired several smaller telcos leading to the major takeover of OptiComm for $610M in late 2020.

The strategy culminated early this year with a takeover bid for Uniti of $4.50 per share from NZ’s Morrison & Co, valuing Uniti at $3.6BN.

This isn't the first telco takeover success story in Australia.

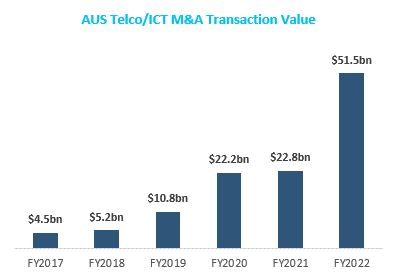

Since 2010, over 83% of ASX listed telcos with market caps of $15M to $500M have been acquired. Furthermore, over the past five years, ASX M&A (mergers and acquisitions) activity in telco-land has exploded, topping $51.5BN last year.

Source: S&P Capital IQ, disclosed deal values only

We are hoping that VN8 can follow a similar trajectory to Uniti Group which sees early shareholders rewarded.

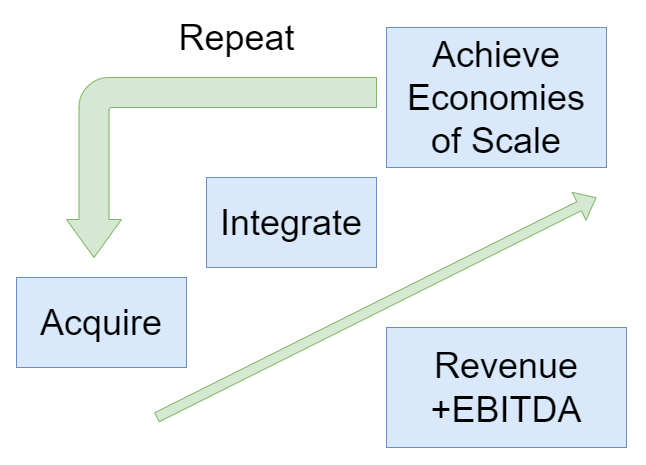

VN8 is following the well trodden telco growth pathway of Acquire → Integrate → Achieve Economies of Scale.

VN8 is trending in the right direction - last week, the telco delivered yet another strong result in its latest quarterly report.

The company posted $10.5M in revenue for the quarter, up 81% from a year earlier, marking VN8’s second consecutive quarter of record revenue as customer numbers continued to grow across all divisions.

In addition to strong revenue growth, the quarterly result included monthly debt repayments of over $800,000 related to its 2021 acquisition of MNF’s Direct Business.

Importantly, the last repayment related to the MNF acquisition was made this week - freeing up significant cashflow of around $10M annually for further acquisitions and growth opportunities.

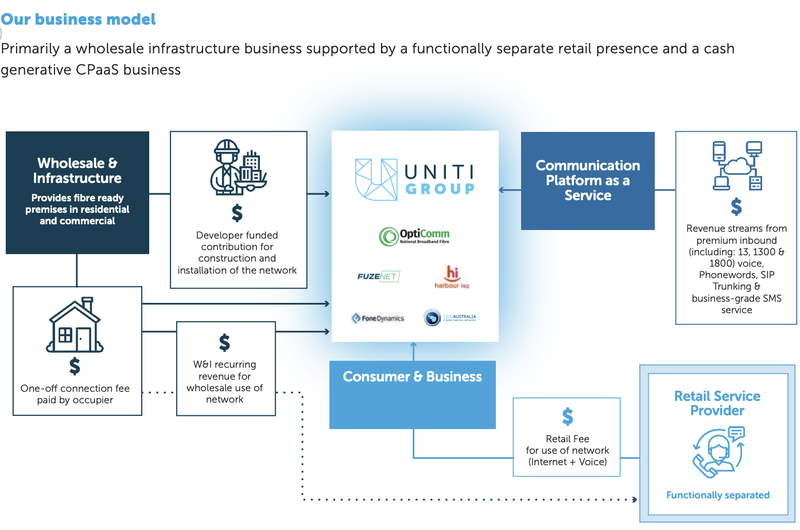

VN8 is a small cap telco that provides cloud-based, telecommunication solutions to Australian small and medium enterprises (SME).

With the pandemic changing the workplace, reliable business interconnectivity has become all the more important — benefitting the likes of VN8.

VN8’s strategy over the last 24 months has been to acquire and integrate smaller telco businesses, and use cross-selling and economies of scale to generate more revenue.

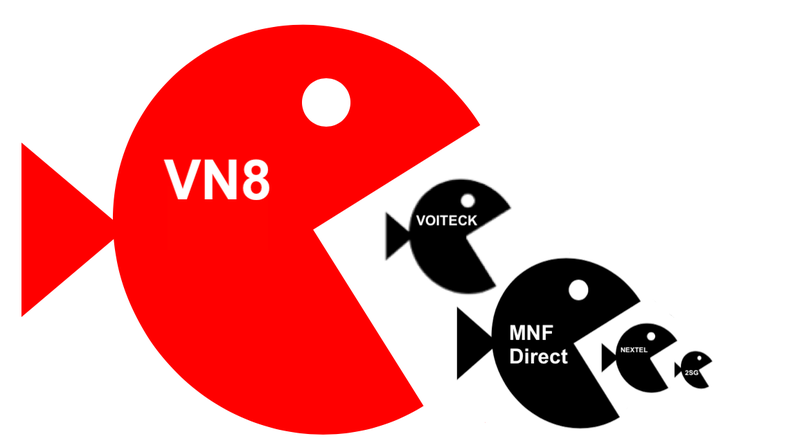

A little bit like a big fish swallowing up smaller fish, and one day VN8 might be the fish that gets eaten...

The telco industry is marked by M&A activity - consider the likes of larger cap telcos like Aussie Broadband and Uniti Group that regularly seek for smaller fish to acquire. In Uniti’s case, the company agreed to get swallowed up recently for ~$3.6B earlier this year.

VN8 is executing on this same strategy but at a smaller scale, making four key acquisitions in the last 24 months:

- Voitek: Voice and internet services, primarily in South Australia

- MNF Direct: Cloud, phone and internet services to a substantial SME and residential customer base

- Nextel: NSW telco to SMEs

- 2SG: Brisbane-based broadband wholesale provider

With each new acquisition, VN8’s annual recurring revenues (ARR) grow by the baseline amount of revenue from the acquired company. However, further quarter on quarter growth comes organically by incorporating these new customers through lead generation, cross selling and ultimately increasing average revenue per user.

Our “big bet” for VN8 is continued growth both organically and through acquisition to a size at which it can capture the attention of a larger telco as an acquisition target.

To get there, VN8 needs to show that its growth is continuing and sustainable, and we think that its most recent quarterly results are indicative of this.

VN8 is currently capped at ~$26M and has $3.2M in the bank as at 30 June 2022.

On 2 August 2022, VN8 made its final $833,000 monthly debt repayment to Symbio (formerly MNF Group) as part of its 2021 transformative acquisition of the Direct Business. VN8 still maintains a separate $16M debt facility with Longreach, of which $14.5M has been drawn down, paying this down at the rate of $500k each quarter.

We believe VN8 is well positioned to re-rate positively if it can sustain its growth trajectory and ultimately deliver positive cashflow and earnings for successive years. This fits with our key objectives as per our Investment Memo we put together for our Investment in VN8 in February 2022:

The Uniti Group Story

As we flagged above, the Uniti Group is a great example of what VN8 is trying to achieve as a telco.

In 2019, Uniti Group listed with a market cap of ~$32M, fast forward to this year and Uniti accepted an acquisition offer for roughly $3.6B.

The telco industry can be difficult to understand at times, as the end users of the products are not always clear and the market is somewhat opaque.

But Uniti’s strategy was always to Acquire → Integrate → Achieve Economies of Scale.

And repeat.

This is the Uniti blueprint that VN8 is following:

So how did Uniti get there in just three years?

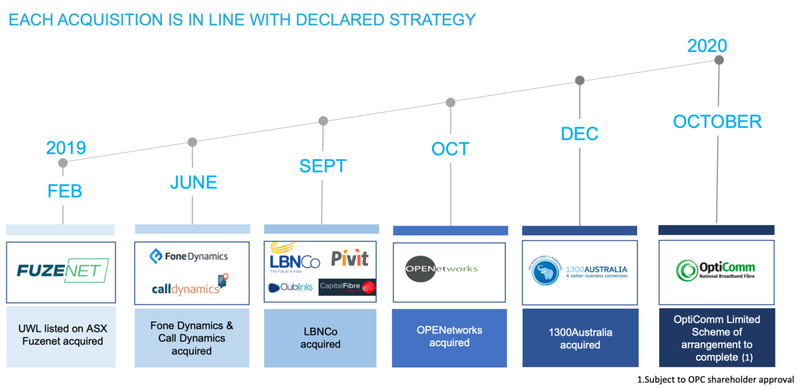

Uniti’s first move upon listing was to acquire FuzeNet for $8.1M, a retail service provider of fiber optic infrastructure.

Shortly after listing, Uniti made its second acquisition - a company called Pivit, a provider of fiber retail broadband services for a small sum of $450,000.

As Uniti started to get the ball rolling, the acquisitions quickly started to grow in scope and size.

In its first year of listing Uniti had made nine new acquisitions of smaller telco brands:

FY20 was the year the Uniti transferred from loss-making to profitable and cashflow positive.

This free cashflow allowed the company to make more acquisitions and grow at a substantial rate.

In September 2020, the company secured a $150M debt facility to continue the aggressive acquisition strategy.

The next acquisition was Uniti’s most important by far and challenging: OptiComm.

With a complex acquisition process in place, and after much back and forth between the companies, Uniti acquired OptiComm in September 2020 for $610M.

In just two and a half years, Uniti had transformed from a loss-making fixed wireless business to a highly profitable and integrated digital telecommunications infrastructure company.

Again, this accelerated growth was done through a simple growth strategy:

Acquire → Integrate → Achieve Economies of Scale.

Uniti spent the next twelve months continuing to gobble up smaller telco assets, including Telstra Velocity assets before being admitted to the ASX 200.

By the end of FY21, Uniti had grown its annual revenues to $160M and profit to $30M by taking lots of smaller companies and packaging them together into one integrated offering:

This all leads up to April 2022 where Uniti signed a $3.6BN deal to sell the company to the Morrison-Brookfield Group, the deal which, as of two weeks ago, has now been complete.

Uniti is an ideal example of business strategy executed to perfection.

VN8 is following this playbook and has already grown its revenues 81% year-on-year through its acquisition process.

As we mentioned above, our big bet for VN8 is that it grows to a size where they will draw takeover interest by a larger telco.

In the meantime, we are watching for the company to sustain its growth organically and through acquisition.

That's the broader picture, let's now take a look at how VN8 performed in the most recent quarter.

Deep dive into VN8’s quarterly

Last Friday, VN8 dropped its quarterly report (4C) with some impressive headline numbers.

Looking at the top line figures, revenues jumped 81% year-on-year (YoY), setting a new record of $10.5M for the quarter.

As a result, net quarterly operating cash inflow was $1.3M, derived from total cash receipts of $9.5M (up 110% YoY).

This marks four consecutive quarters delivering positive operating cashflow — a pleasing trend we’re keen to see continue.

There was also further growth in new business activity with SME customers driving quarterly total contract value for new sales of $2.37M, up 47% YoY.

VN8’s first acquisition, the 2SG Wholesale division, continued to deliver growth, with NBN revenue up 22% YoY, respectively.

Its flagship IP voice product continued to grow with quarterly revenues up 37% YoY, reflective of successful delivery of VN8’s cross-sell / up-sell strategy. That is, as VN8 acquires other businesses, it is able to cross sell products from other divisions to the new customer base, thereby increasing its average revenue per user.

VN8’s customer base has also rapidly grown as a result of the acquisition strategy, up over 117% YoY to in excess of 100,000 registered active private branch exchange (PBX) customers.

Going forward, cashflows are set to improve significantly following the final deferred payment on 2 August 2022 for the Direct Business acquisition (more on this later).

In terms of integrating its other acquisitions, all Voiteck customers have now been migrated to the VN8 network. However, the integration of the Direct Business has been slower than initially anticipated (it was due to be completed by now), deferring some cashflow generation to the 2H22 as a result.

Customer churn rate seems to be largely unaffected by the slower migration, meaning that VN8 isn’t losing much of the ongoing expected cashflow generation because of the delay.

When migration is completed, the company expects to save between $600-$700k annually on staffing costs, which should feed into a decent lift to VN8’s bottom line results for the year ahead.

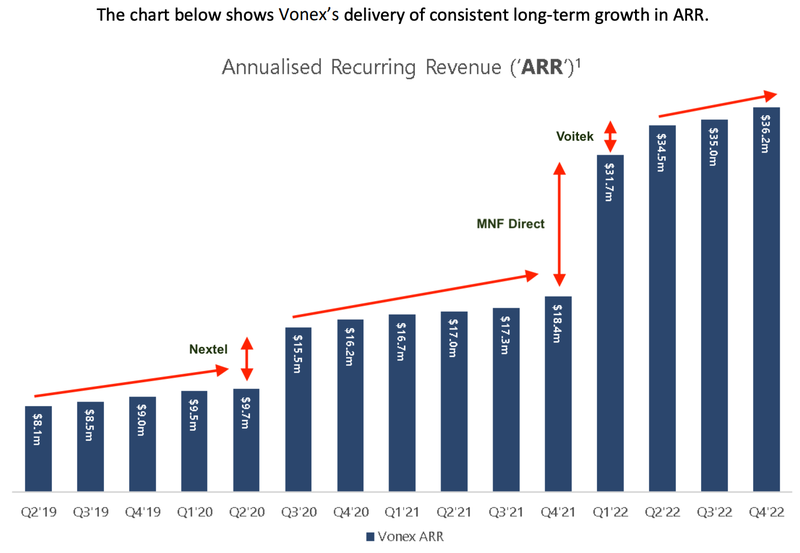

Another key metric we track is Annual Recurring Revenue (ARR), which basically indicates the amount of revenue that a company expects to repeat annually. As at 30 June 2022, VN8 has an ARR of ~$36.2M, up 97% YoY.

What we find interesting is that VN8’s ARR is above its market capitalisation - by some 70% as of Friday 29 July 2022 - and is essentially equal to its enterprise value (~$37M).

ARR is considered somewhat of an indicator of future revenues, so if VN8 can keep a handle on its costs and margins, the telco should be making significant positive cashflow going forward.

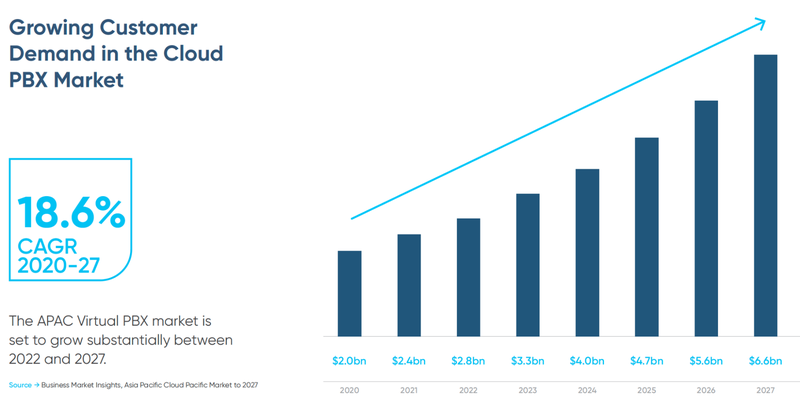

The market outlook for VN8’s lead products and services also are expected to remain buoyant, auguring well for future revenues to continue its uptrend.

According to Business Markets Insights, the Australian-Pacific market for cloud PBX services is expected to grow strongly over the next 5 years, by some 18.6% CAGR (compound annual growth rate).

Looking under the debt hood

As part of its acquisition of MNF’s Direct Business in July 2021, VN8 entered into a debt arrangement with MNF, agreeing to monthly repayments of $833,000.

This last repayment was made on 2 August 2022 - Tuesday this week.

This means that going forward, VN8 will unlock significant cashflow, to the tune of about $10M per annum.

VN8 has also drawn down $14.5M of $16M available from a debt facility with Longreach Credit Investors (at Longreach’s lowest rate, as part of the Direct Business acquisition last year). The company pays this off at about $500k per quarter, so could accelerate repayments here to get this off the books earlier.

What will be interesting is how the bottom line figures over the next year look, as cashflow is freed up now that the Direct Group debt repayments have ended.

What else has happened lately?

During the quarter VN8 announced a partnership with Commonwealth Bank (CBA)-backed telco provider ‘More’, perhaps best known for its Tangerine broadband services.

Both parties have entered binding heads of agreement which will see VN8 become More’s exclusive provider of Hosted PBX services to new and existing CBA customers.

VN8 will also deliver a new hosted PBX and IP telephony enablement platform for More's new and existing small to medium enterprise (SME) customers.

Upon full release of the Platform and migration of existing Hosted PBX business services, VN8 expects a significant increase to annual recurring revenue from the partnership, predominantly from license fees, hardware and call carriage.

Vonex will also charge a one-off fee for initial software development and an ongoing monthly platform management fee. These should provide a further boost to ARR.

What is up next for VN8?

Whilst the share price hasn't reacted yet, VN8 has been executing its growth strategy, leading to substantial growth of its customer base, and flowing onto stronger cashflow generation going forward.

We’d like to see the company continue on its aggressive growth path through further acquisitions and integrations.

On this, we envision the telco delivering the following through to the end of the year. We will keep track of VN8’s progress, and provide updates accordingly.

🔲 Completion of integration of Direct Business (2H22)

🔲 Further potential acquisitions (2H22-23)

🔲 Sustain cashflow positive quarters going forward (2H22)

🔲 EBITDA positive (2H22)

🔲 125k PBX users (4Q22 - 1H23)

Our VN8 Investment Memo

Back in February of 2022 we put together our VN8 Investment Memo - in that you’ll find:

- Key objectives for VN8 in 2022

- Why we continue to hold VN8

- What the key risks to our investment thesis are

- Our investment plan

The ultimate purpose of the memo is to track the progress of our portfolio companies using our Investment Memo as a benchmark, throughout 2022.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.