MNB building phosphate (fertiliser) mine as prices at record levels

Disclosure: The authors of this article and owners of Next Investors, S3 Consortium Pty Ltd (The Company) and Associated Entities own 8,645,000 MNB shares and 1,562,500 MNB options at the time of publication. The Company has been engaged by MNB to share our commentary on the progress of our Investment in MNB over time.

Two key players in global food supply chains — Russia and Ukraine — are currently at war.

This is not unlike the 70s, where geopolitical instability combined with an energy price shock led to a food crisis.

Production of most fertilisers requires energy, usually using natural gas.

So with high gas input costs and key supply disrupted, fertiliser prices are trading at record prices in 2022.

Even before any of these recent developments, Minbos Resources (ASX:MNB) had long been one of our favourite Investments.

We like MNB because its phosphate fertiliser project in Angola looked like it could be constructed quickly and brought into production at a modest cost.

Now, against a backdrop of record fertiliser prices, MNB today released its long awaited Definitive Feasibility Study (DFS). The DFS showed us some firm numbers to build the mine, along with calculations around the project’s value, with first production now scheduled for late 2023.

The DFS is an important (and long) document that has a lot of detail about whether a project stacks up from a technical, economic point of view. It is produced to a relatively high degree of accuracy, and can be used as a basis for securing finance from serious investors to fund the project.

Our quick first takeaways from the DFS:

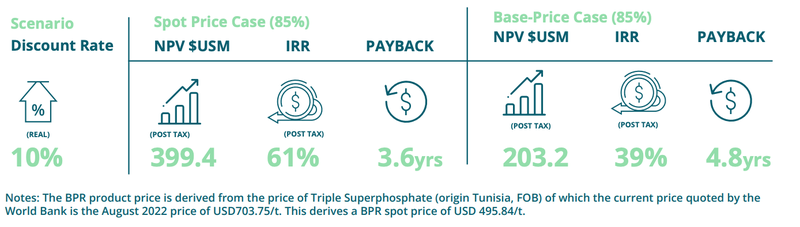

- NPV of US$203.4M (base case) - US$399.4M (using current fertiliser prices - almost double the base case)

- Remaining capital expenditures (CAPEX) of US$40M

- Relatively short timeline to first production - in late 2023

- Post-tax internal rate of return (IRR) of 61%

- Payback period of 3.6 years

- Project economics improve significantly as fertiliser prices rise.

Mine construction has already commenced. The remaining cost to complete the mine is US$48.5M, with MNB only requiring further funding of US$40M.

MNB has ~$28M in the bank from a capital raise they did back in July at 11c (there has been plenty of time to digest the 11c stock). It also has an existing non-binding commitment for a US$25M debt facility.

Now armed with its DFS (and since fertiliser prices are at record highs), we don’t think MNB will have much trouble securing the final financing to finish the mine construction.

So, as we flagged above, a DFS is the key study required to bring on serious investors.

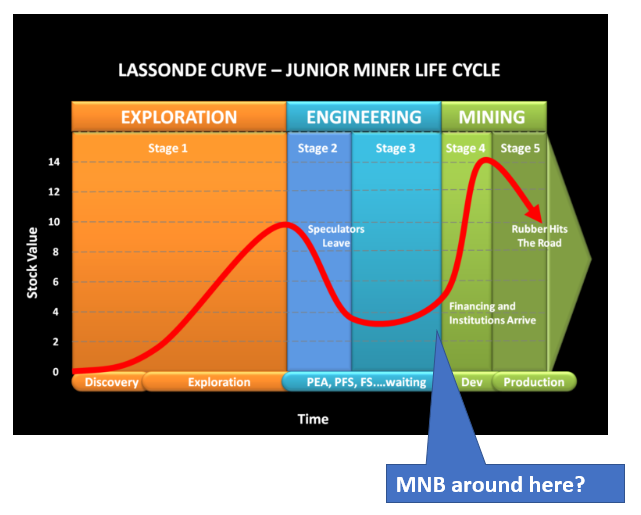

While it’s rare to see an exploration stock move to actually building a mine, most small cap stocks that do successfully move from exploration to a mine follow a similar share price pattern — shown in the Lassonde curve:

Source: KJ Kutling

The red line shows an approximation of a resource stock’s value. It tends to see a broad dip during the “boring “ bit - after the excitement of the mineral discovery has faded, when the company is completing complex feasibility studies that it can present to financiers... and current investors are waiting around for something to happen.

It looks like MNB is close to leaving the “boring” phase of waiting for studies and is hopefully moving into the more interesting phase of mine construction and then production (first production November 2023 according to the DFS).

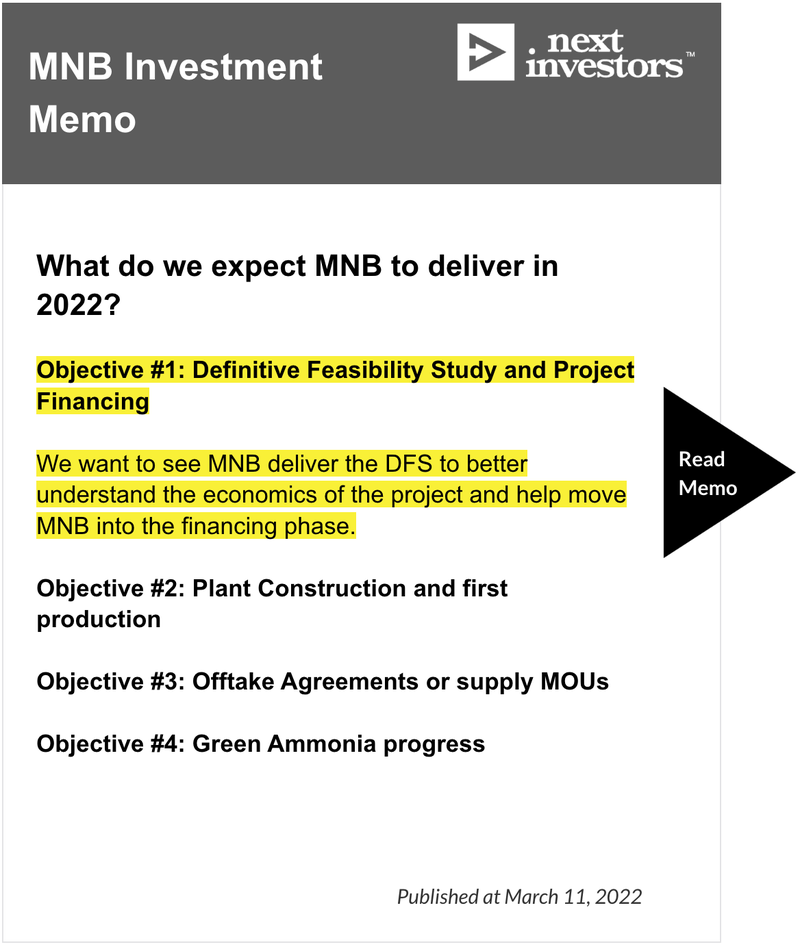

Completion of the DFS sees MNB meet our first objective that we had for the company in 2022, as outlined in our MNB Investment Memo:

Click here to read our full MNB Investment Memo, which also includes the risks and our Investment plan.

We are still watching for offtake agreements, supply MoUs and also any progress on the very interesting Green Ammonia project, which is separate to the phosphate mine and provides additional potential to add further shareholder value over time.

Which brings us to our ultimate “Big Bet” for our Investment in MNB:

Our “Big Bet”

“MNB delivers a 10x return by building a profitable phosphate mine AND progressing its green ammonia project.”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our MNB Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

To see all that MNB has done since we first Invested, we’ve compiled a brand new “Progress Tracker”:

Click here to see our Progress Tracker

Five key take-aways from MNB’s Definitive Feasibility Study (DFS):

- The project has a post tax NPV of US$400M (at current fertiliser prices & MNB’s 85% ownership) - This compares to MNB’s market cap of just $75.7M and excludes any of the value from MNB’s green hydrogen/ammonia business.

- High rate of return and very short payback period - At the current fertiliser spot price, the project would generate a 61% internal rate of return. It would pay back all of the upfront capital invested in the project within 3.6 years, extremely quick considering the potential 20+ year mine life.

- Low CAPEX relative to MNB’s current balance sheet capacity and project NPV - MNB only needs to find US$40M in funding to finish the project’s development. MNB should have around $28M in cash, and it has a non-binding commitment for a US$25M debt facility. We don’t think MNB will find it difficult to raise the remainder, either through debt or equity, given how small it is relative to the project's large NPV.

- Low strip ratio which we hope translates to a low operating cost - MNB showed a relatively low 3.2 strip ratio which means that its project can be mined with minimal waste material being produced. We hope this translates to a low cost of production for MNB in the long run.

- MNB’s project is highly sensitive to changes in fertiliser prices - A ~20% increase in fertiliser prices increases the project’s NPV by $60M. With the fertiliser spot price currently 127% higher than last year and the supply/demand situation potentially getting worse over the coming year, we expect the price of fertilisers could increase and, in turn, the value of MNB’s project.

Let's now dive in a little deeper on MNB’s project.

Why is the price of gas important to MNB?

MNB has a giant phosphate rock resource in Angola that it can cheaply turn into fertiliser and sell to local and regional farmers.

MNB’s beneficiated phosphate rock (BPR) product will compete in the local market directly with imported water soluble phosphate (WSP) products, which are made using expensive gas.

Gas is a key input in many competing types of fertilisers, specifically ammonia-based fertilisers including MAP and DAP as ammonia production requires gas in its production. Soaring gas prices are much of the reason behind the also soaring prices for fertilisers.

Russia's invasion of Ukraine highlighted the need for countries to secure local energy supply with Russia having been the world's biggest crude and natural gas exporter. And with almost all LNG sold under contract, which are decades in length, there is very little LNG available.

Meanwhile, Western countries have been pushing ahead with their renewable energy transition, making natural gas even more expensive as these countries look to decouple from their oil dependence.

Along with being a key exporter of fertiliser, Russia’s natural gas made up 80% of the cost of fertiliser production in Europe. But since it invaded Ukraine, a huge portion of Europe’s fertiliser plants have shut down. This will have ripple effects across the world, ultimately impacting food security in places like Sub-Saharan Africa.

Adding to the pressure, more than three quarters of global population growth over the next 80 years is expected to take place in Sub-Saharan Africa, where the population is projected to double by 2050 and almost quadruple by 2100.

This growth means that higher fertiliser prices must be accepted in order to increase food production.

Further, it is becoming increasingly important to secure local phosphate production (as is the case for many commodities), so local Sub-Saharan fertiliser production is much needed.

Of course this just touches the surface of the issues around global food security — we’ll aim to take a deeper dive into these themes in the weeks ahead.

DFS at first glance

MNB has calculated the following Net Present Values (NPVs) at its current 85% ownership of the project:

- US$203M (base case)

- US$399M (spot price case)

- US$585M (best case)

It’s our view that the base case NPV of US$202M is quite conservative, as this is based on long-term average phosphate rock pricing of US$422 per tonne — the 15-year average price for bulk TSP (trisodium phosphate).

The spot price case NPV of US$399M is a more interesting figure as it uses current fertiliser prices as key assumptions. In this study MNB is using TSP prices as the basis for BPR (Burkina Faso phosphate rock-based phosphate fertilisers).

The spot price case was calculated using a phosphate (TSP) price of US$703 - the World Bank’s published price for August. In our view, this is a more realistic reflection of where phosphate prices may be when MNB is expected to begin production next year.

The large difference between the spot price case and base cases comes down to the large discrepancy in current high market prices for fertiliser compared to the lower long-term average.

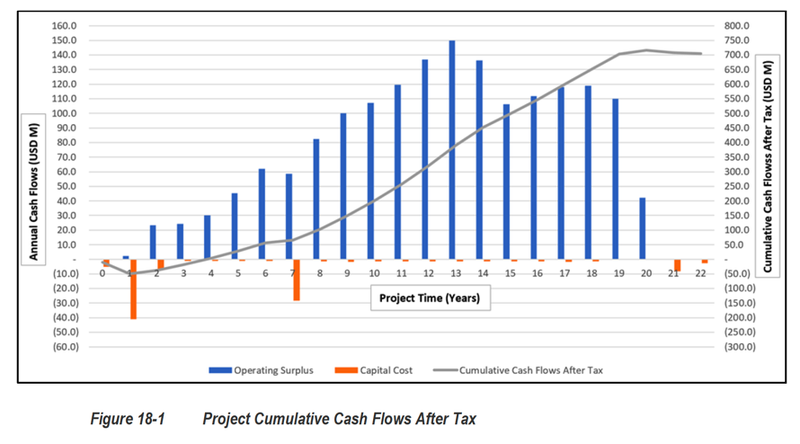

Importantly, MNB could start seeing cash flows from phosphate sales in the near future, as the project is expected to go into production in late 2023.

Here’s the annual cash flows over the estimated 20 year mine life:

All that’s really left to sort out is project financing, and now with the DFS in hand MNB can get to work on that front.

MNB has already paid for some of the project’s long lead items, but still has US$40M to be financed as part of the total upfront project capital expenditures of US$52.6M.

MNB had $3.6M in cash at 30 June 2022 and has since raised a further $25M through an equity raise, this should mean the company has somewhere around ~$28.6M in cash (before accounting for spending in the September quarter). We will get an updated cash balance for MNB by the end of October when its quarterly report is released.

MNB also has a non-binding commitment from the same cornerstone investors who participated in the equity raise for a US$25M debt facility.

The pathway to financing the project looks like it will be a mix of debt and equity. We suspect it will be more about the debt financing from here onwards given MNB’s already very healthy cash balance.

Given the state of the global fertiliser market at present and the project economics, we think MNB has a good chance of securing financing on favourable terms.

Another way MNB could fund the project is via an offtake partner making pre-payments to MNB for future products. On that front, this sentence in the DFS caught our eye:

MNB has previously said it has engaged with some of Angola’s largest commercial farms to secure binding sales and offtake agreements, including field trials to evaluate the relative economic effectiveness of its phosphate fertiliser in target customer crops and soils.

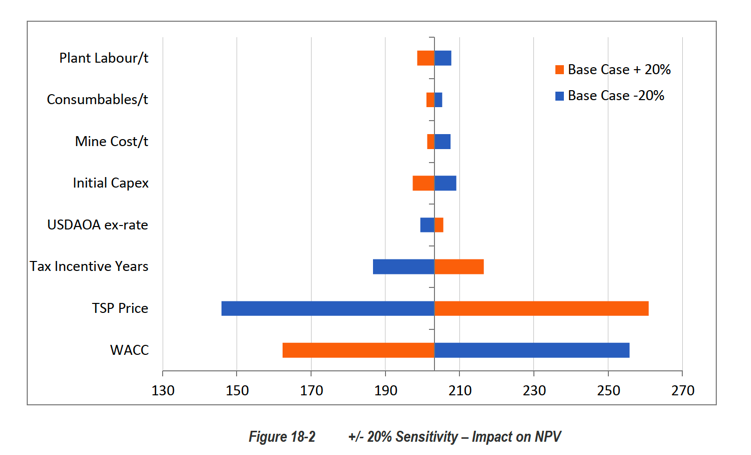

Project value sensitive to fertiliser price and financing costs

The following chart from MNB’s DFS announcement was also interesting.

The chart shows the sensitivity of inputs into the financial model and the impact they have on the project’s overall net present value (NPV) figures.

The first major impact comes from the fertiliser (triple super phosphate or TSP) price where a 20% increase in TSP price lifts MNB’s base case NPV by ~US$60M.

The second is the weighted average cost of capital (WACC) which is basically a reference to the price MNB has to pay to finance its project.

MNB used a 10% WACC in the DFS. For every 20% decrease in the cost of capital, MNB’s NPV increases by ~US$50M.

We will be watching to see the terms of any debt/equity financing the company completes given it will have such a large impact on the overall project economics.

We will be monitoring both of the relevant inputs to both of these metrics over the coming months to watch out for any major changes.

What’s next for MNB?

As we outlined in our March 2022 Investment Memo, completion of the DFS was part of our first objective set for MNB to achieve in the 12 months from March 2022:

Objective #1: Definitive Feasibility Study and Project Financing

Now that the DFS is in, we can look to the financing phase.

We want to see MNB secure the remaining financing required to fund its plant construction.

Objective #2: Plant Construction and first production

With long lead items already ordered and the final environmental permitting expected to be lodged by the end of Q1-2022, we want to see construction commence at both its plant and mine.

Now with the DFS in hand and with a better grasp on MNB timeline, it looks like we may see that photo of the first bag of phosphate from the project in late 2023. However like all construction projects, we are also mindful this timeline may slip and it might not be until early 2024.

Objective #3: Offtake Agreements or supply MoUs

We expect that signing offtake agreements, along with progress on the financing front that we mentioned above, will now be MNB’s immediate focus.

A great result for MNB will be if the offtake agreement is signed/underwritten by the Angolan government. The project was considered to be of “National Importance to Angola” by the government so we think this is a possibility.

Objective #4: Green Ammonia progress

We want to see MNB make some more progress with respect to outlining its Green Ammonia strategy. As part of this process we want to see MNB source renewable energy power and sign technology partnerships for the development of the plant.

So far, MNB has signed a strategic cooperation agreement for its green ammonia project with a Hong Kong based syndicate led by Mr Liang Feng.

Key risks

Click on the image below to see the key risks to MNB in detail.

Our 2022 MNB Investment Memo

Below is our August 2022 Investment Memo for MNB, where you can find a short, high level summary of our reasons for Investing.

The ultimate purpose of the memo is to record our current thinking as a benchmark to assess the company's performance against our expectations for the following 12 months.

In our MNB Investment Memo, you’ll find:

- Key objectives for MNB for the coming year (starting from March 2022)

- Why we are Invested in MNB

- The key risks to our Investment thesis

- Our Investment plan

Disclosure: The authors of this article and owners of Next Investors, S3 Consortium Pty Ltd (The Company) and Associated Entities own 8,645,000 MNB shares and 1,562,500 MNB options at the time of publication. The Company has been engaged by MNB to share our commentary on the progress of our Investment in MNB over time.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.