It’s phosphate - and MNB has a lot of it

Disclosure: The authors of this article and owners of Next Investors, S3 Consortium Pty Ltd (The Company) and Associated Entities own 8,645,000 MNB shares and 1,562,500 MNB options at the time of publication. The Company has been engaged by MNB to share our commentary on the progress of our Investment in MNB over time.

Our Investment in Minbos Resources (ASX:MNB) is quickly becoming one of the most interesting stories in our Portfolio.

We don't think there are too many stocks on the ASX like it.

MNB has rapidly evolved over the last six months now riding not one, but THREE of our favourite long-term macro investment themes:

- MNB has used its in-country relationships to secure some of the world's cheapest hydro energy for a green hydrogen-ammonia project.

- MNB has nearly secured full finance to build its phosphate project next year - in a time of record high phosphate prices and a looming global food security crisis.

- MNB announced up to $60M in new funds ($25M placement secured at 11 cents + US$25M non-binding debt term sheet) - and $15M of the placement went to a syndicate of investors which includes the founder and chairman of the world’s largest battery anode company - AND that company could use MNB’s phosphate as a battery material.

Phosphate for batteries?

Elon Musk definitely thinks it's a viable battery chemistry alternative and some of the world’s biggest battery makers are investing heavily in it.

After much talk over the last couple years, this is now established technology, and LFP batteries are projected to carve out a growing amount of market share.

In China, LFP batteries command 44% of the EV market and nearly half of all Teslas made last quarter had phosphate in their batteries.

Other major automakers are starting to take Tesla’s lead. Ford recently moved to buy a huge volume of iron-based battery packs (LFP) for its popular Mustang Mach-E and F-150 Lightning models, in order to shift away from nickel based chemistry and cut costs.

With this placement tucked away, MNB isn’t just a fertiliser and green ammonia/hydrogen Investment anymore, it is now also a battery materials Investment for us.

We think the placement should help MNB build connections in the battery material world.

That's because the syndicate’s holdings are cornerstoned (70%) by an investment group called HongKong Jayson Holding Co.

That company has the founder and chairman of Shanghai listed “Shanghai Putailai New Energy Technology” (capped at US$18 billion) as a substantial shareholder.

Again, Shanghai Putailai New Energy Technology is the world’s largest anode materials maker for lithium batteries.

AND, HongKong Jayson Holding Co and their syndicate partners now hold ~15% of MNB.

As part of that investment, the syndicate and MNB have signed a “Strategic Cooperation Agreement” to develop a battery materials and large scale green ammonia project.

The Strategic Cooperation Agreement means MNB is committed to a long-term offtake of 100,000 tonnes per annum of high-grade phosphate rock at agreed market rates.

We expect the syndicate of investors to help make introductions and secure a binding offtake for this 100,000 tonnes/year commitment.

That volume is also slightly more than a quarter of MNB’s overall targeted annual production of 368,000 tonnes of phosphate as outlined in MNB’s Scoping Study.

Which we think means there’s plenty of room for MNB’s initial fertiliser ambitions to coexist with its new battery materials ambitions.

Sharing MNB’s phosphate around is a good problem to have, given that both battery material supply AND fertiliser supply is expected to be tight in the medium term.

In the case of the battery side of the projects - this would be for lithium ferro phosphate (LFP) batteries.

LFP batteries are starting to take up significant market share as a battery chemistry and we explore this theme further in the Strategic Cooperation Agreement section of this note.

The expansion of MNB’s potential product suite and funding comes at a time when we’ve seen so many small caps struggle to get funding in the door for their projects in difficult market conditions.

In a down market where investors and financiers are skittish about deploying capital, we’ve seen some companies forced into doing raises at 40-50% discounts to their last traded price.

Relative to those raises, MNB’s raise at a 18.5% discount to the last traded share price prior to the raise strikes us as relatively small.

MNB was one of our few Investments that held up really well during the May and June market weakness and global correction.

So we’re glad MNB was able to turn interest in its projects into all important funding - and at scale.

Interestingly, MNB is continuing to trade around the 11c capital raise price with ~ $14M of the shares are already on market, and a further ~ $10M to come onto the market in late August following shareholder approval at a General Meeting.

We think the size of the raise, the discount level of the placement and the calibre of new investors are glowing endorsements of the quality of MNB’s projects and their long term value.

Beyond this recent funding injection, the $25M placement could shortly be followed up by a further US$25M debt facility available to MNB specifically for its low cost (CAPEX - US$22-28M) phosphate project.

Those CAPEX figures come from MNB’s Scoping Study which outlines a Net Present Value (NPV) of between US$191M and US$308M - that’s for the Phosphate project alone.

Importantly, the Scoping Study was done BEFORE fertiliser prices went through the roof, before the war in Ukraine, and before the now evident battery materials interest.

On the other hand, the increased sale prices for MNB’s output could be somewhat offset by the inflation in the input costs as well (things like equipment, steel and concrete etc) - so we’re eagerly awaiting the delivery of MNB’s Definitive Feasibility studies which is due in the coming two to three months (Q3).

This should give us a better look at the project economics in light of the complex array of macro factors MNB is facing, both to the upside and the downside.

That $25M debt facility is currently in the form of a non-binding term sheet, but key terms are in place.

In order for it to turn into a binding term sheet, MNB will need to deliver an “acceptable DFS” and secure offtake.

With a fertiliser crunch playing out around the world due in part to the ongoing conflict in Ukraine, we expect that DFS to be more than acceptable and offtake discussions to be straightforward.

This means MNB should have a sizeable warchest at its disposal to pursue BOTH its phosphate (fertiliser/battery materials) ambitions AND its green ammonia/hydrogen ambitions.

So there are now four products that MNB could produce:

- Fertiliser (phosphate)

- Battery materials (phosphate)

- Green ammonia

- Green hydrogen

It’s a lot to digest, and we think the first two products will be the first cabs off the rank with green ammonia and green hydrogen to follow down the track.

While the MNB share price held up really well recently, it has struggled to break out over the last six months given the looming need to raise cash to fund construction of the phosphate project.

Now that the funding is in and details of a debt facility are on the cusp of crystallising, we hope MNB will re-rate as the company edges toward first phosphate rock production in Q2 2023.

In the rest of this note we’ll provide a breakdown of the specifics of the placement and the debt funding term sheet and provide a bit more detail on the Strategic Cooperation Agreement as it pertains to LFP batteries.

MNB’s now significant funding has in essence reduced funding risk (for the foreseeable future) as we identified in our March 2022 MNB Investment Memo:

Details of the $25M MNB placement

MNB’s $25M placement was priced at 11 cents, which was a 22.1% discount to the 5-day VWAP prior to the placement.

We think that’s an acceptable discount for a placement in this market environment. It enabled MNB to secure a very large chunk of cash - this is effectively a third of its current market cap ($75M) and shares are currently trading at ~11.5 cents.

The shares are being issued in two separate tranches.

The first tranche of 131,414,473 shares settled on 19 July.

The subsequent tranche of 95,858,255 shares will need shareholder approval at a meeting scheduled for 23 August 2022, with the shares expected to be issued soon after that.

The reason for splitting the placement into two is because according to ASX Listing Rules, companies can only issue a maximum of 25% under its placement capacity. So when issuing more than 15% of the current shares on issue, the company needs its shareholders to approve the transaction for the additional 10%.

MNB has in essence completely maxed out its placement capacity here - in a tough market.

We expect to see shareholders approve the remainder of the placement (we will be voting in favour of it), especially considering how important it is to be fully funded in markets like these.

Here are the three key entities involved in the placement which now collectively own ~15% of MNB:

- HongKong Jayson Holding Co., Ltd. (HKJYS) (70% of placement funds)

- Hoston Investments (Australia) Pty Ltd. (20% of placement funds)

- Longmarch Principal Holding Limited (10% of placement Funds)

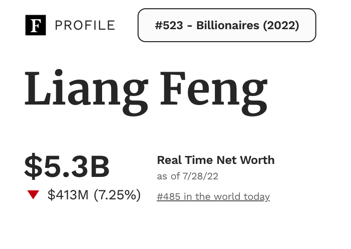

One of the key people involved in HKJYS is substantial holder, Mr Liang Feng - the founder of Shanghai listed “Shanghai Putailai New Energy Technology”.

Shanghai Putailai New Energy Technology has a market cap of US$18 billion and is the world’s largest maker of anode materials for lithium batteries.

Mr Liang Feng is worth about $5.3BN himself, and has his own Forbes billionaire profile which you can read here:

Welcome to the MNB share register, Liang Feng.

Mr Liang Feng led a syndicate of investors into the placement which included Hoston Investments and Longmarch.

Longmarch was also the company involved in the signing of the non-binding debt term sheet for the US$25M we mentioned at the start of this note.

Here are the key terms of that US$25M debt term sheet:

- High level non-binding term sheet signed with Longmarch Capital for arrangement of debt facility

- US$25 million in tranches of US$5 million, available for first drawdown on financial close

- Term – 5 years

- Interest rate – competitive market interest rates to be agreed, with potential equity participation

- Use of proceeds – CAPEX for MNB's Cabinda Phosphate Project, mining and fertiliser plant

- Conditions – completion of due diligence by financiers, execution of definitive agreements, completion of acceptable DFS by MNB, off-take and supply agreements to be in place and other customary conditions

Our view is that this debt term sheet should be enough to see MNB’s phosphate project move into construction - now due to commence in Q3 2022, so quite soon.

With both the placement funds and the non-binding debt term sheet, we expect MNB to make quick progress on the phosphate project while at the same time moving on its green ammonia/hydrogen project.

Phosphate for batteries? MNB’s Strategic Cooperation Agreement

As part of the Strategic Cooperation Agreement with the syndicate of investors, MNB will work with the parties to the agreement on feasibility, partnerships, offtake agreements.

As we noted at the start, MNB has committed to a long-term offtake of 100,000 tonnes per annum of high-grade phosphate rock at agreed market rates, or slightly more than one quarter of annual production.

We expect the syndicate of investors to help make introductions and secure a binding offtake for this 100,000 tonne commitment.

The type of batteries that interest the syndicate of investors backing MNB in this placement, are lithium ferro phosphate batteries (LFP batteries).

China is the world’s largest EV market, 44% of Chinese EVs are LFP and we suspect that major holder Mr Liang is well aware of the big trends in battery chemistry, given he’s a co-founder and Chairman of the world's biggest battery anode company.

LFP batteries are quickly growing market share. In 2021, EVs equipped with LFP batteries made up 14.3% of the global market, an increase of 5.2% compared with 2020.

Indeed, between December and March of this year, Tesla confirmed that nearly half of all the vehicles it produced are already using LFP batteries. Ford is also increasingly adopting this technology for its EVs.

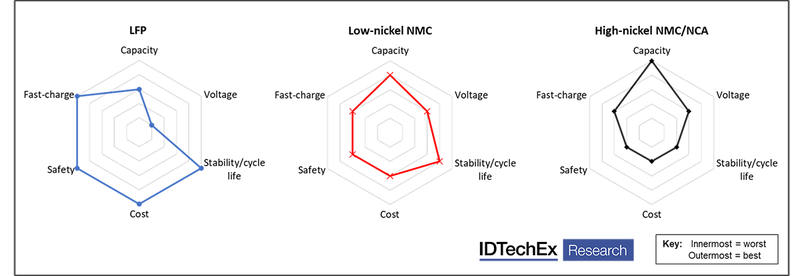

LFP batteries don’t use nickel or cobalt and are generally cheaper and safer, but because they offer less energy density they as a result are currently better suited to lower performance and shorter range EVs:

The way we understand it - LFP is the kind of battery chemistry that could help facilitate EV uptake at magnitudes of scale.

The appeal of this battery chemistry is that iron is plentiful and phosphate costs significantly less than say nickel or cobalt.

However, like most commodities, phosphate prices have risen dramatically since the onset of major global inflation and the war in Ukraine.

So you can see why the syndicate of investors were keen to help advance MNB’s phosphate project.

What’s next for MNB?

As MNB Investors, we think MNB has a large volume of newsflow in the pipeline over the next three to four months ahead of production which is scheduled to commence in Q2 2023.

For instance by late September alone, we think the following should happen for MNB’s phosphate project:

- DFS delivered

- Final Investment Decision (via non-binding term sheet being converted into a binding term-sheet)

- Commence construction (long-lead items begin to arrive)

- Site for granulation plant granted - this is where the phosphate will be processed

As for after that, MNB provided the following timetable:

So from Q2 2023 onwards, the goal is to be selling phosphate to the market.

Meanwhile, it's also full steam ahead on the green ammonia/hydrogen project. A Scoping Study is to be carried out with Stamicarbon, aiming for output of 300kmtpa of green ammonium nitrate products.

That would be a globally significant project - about a third of the size of the largest ammonia plant in construction right now, the Perdaman plant in WA.

It would also be the only large scale green ammonia plant in Africa (to our knowledge), backed by MNB’s already secured access to super cheap, zero-carbon hydropower.

As a result, we think after the latest MNB capital raise it will be phosphate first.

Meanwhile with the green ammonia/hydrogen bubbling along - from Q2 2023 onwards, MNB can reinvest subsequent revenues from the low capex phosphate project back into the green ammonia/hydrogen project.

In short, we think this was a good raise done on the back of compelling project economics that should see MNB into production.

Our MNB Investment Memo:

Our “Investment Memo” is a short, high-level summary of why we continue to hold a position in MNB and what we expect the company to deliver in 2022.

We’ll be using these Investment Memos as a way to assess the company’s progress over 2022 and also examine how our investment thesis plays out throughout the year.

In our MNB Investment Memo you’ll find:

- Key objectives for MNB in 2022

- Why do we continue to hold MNB

- The key risks our investment thesis

- Our investment plan.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.