Food security now a key global concern as fertiliser prices just keep rising

The fallout from the Russia/Ukraine conflict and the impact on commodity prices has made headline after headline in recent weeks.

The latest of these concerns is around supply chain shocks affecting fertiliser prices and a potential global food crisis. If there is one thing that the world can't live without its food.

Almost overnight, countries all around the world have entered “food security” mode. With Russia and Ukraine together accounting for a major portion of the world’s agricultural supplies, the wheat price is has surged 50% in just two weeks while corn is at decade highs.

Russia is also a key fertiliser supplier, so the recommendation last week by Russia’s “Trade and Industry Ministry” that the country’s fertiliser producers temporarily halt exports, presents a significant disruption to the global supply chain.

But nowhere in the world is food security more important than in Africa, where there have long been issues related to fertiliser access and the costs of domestic supply.

Our long term investment Minbos Resources (ASX:MNB) is developing a phosphate (a key ingredient in producing the fertilisers) project in Angola — a project that has been recognised by the Angolan government as a ‘Project of National Importance to Angola’.

Long before the current global food security concerns, African nations have faced challenges in the agricultural sector, with crop yields consistently lower than those of more developed countries. This largely comes down to the consumption of fertiliser — Africa has historically consumed ~19.9kg of fertiliser per hectare of farmland versus countries like the US that plough in ~128.7kg/ha on average.

Africa’s lower phosphate (fertiliser) consumption ultimately comes down to a lack of access to cheap domestic supplies.

The good news is that if Africa can source cheap local supplies, the whole continent could catch up to more developed countries’ food production, removing its reliance on food imports.

This is why we are invested in MNB.

MNB’s phosphate (fertiliser) project sits in Angola (West Africa) and has a high grade resource of 8.4Mt @ 29.7% phosphate.

A 2020 Scoping Study calculated a project value (post-tax NPV) of US$191-308M (A$260-420M) with low upfront costs (CAPEX) of US$22-28M (A$30-38M) over a 21 year mine life.

Importantly, the Scoping Study was done using a fertiliser price of just US$357-482/tonne.

The current fertiliser price sits at US$700/tonne, so using some simplified calculations we could expect this to lift the projected project value into the ~US$400M+ region.

Not only does MNB’s project have the potential to transform the food security of an entire continent, but the project’s economics stack up and are indicative of a potential to create significant shareholder value — both reasons for our investment in MNB.

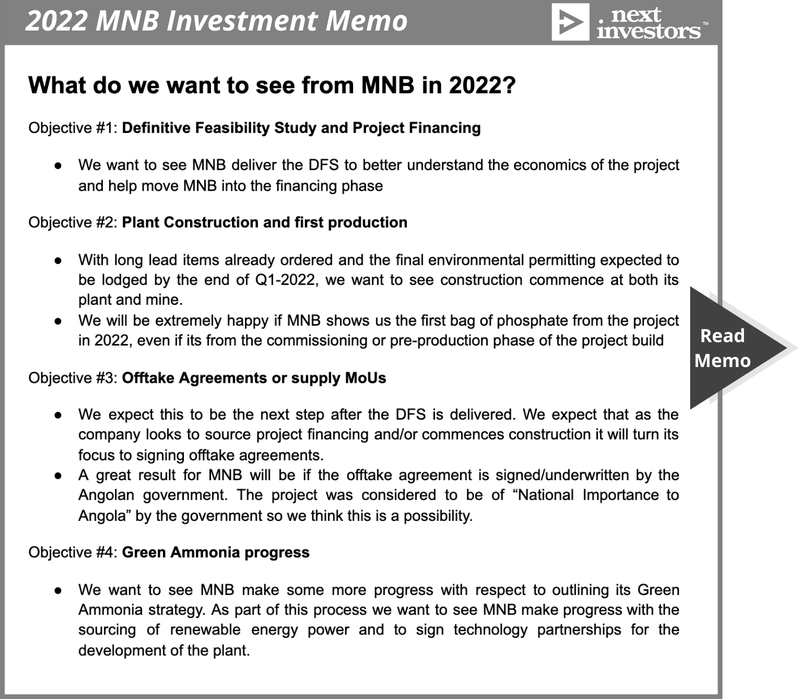

This brings us to our 2022 Investment Memo where we provide a short, high level summary of why we continue to hold MNB and what we want to see the company achieve in 2022.

Here’s what we want to see MNB achieve in 2022:

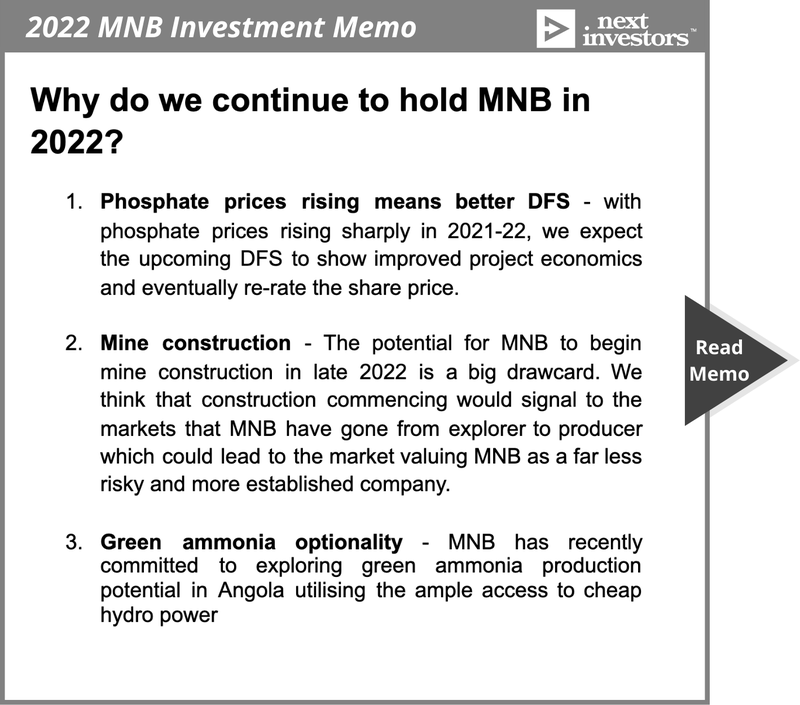

And here is why we continue to hold our investment in MNB:

To read our full MNB Investment Memo click on the button below:

So where is MNB at with its fertiliser project?

It might not be clear as to why a company looking to supply fertiliser to farmers is considered a “mining company”, but the process of producing fertiliser is no different to that of producing gold or iron ore.

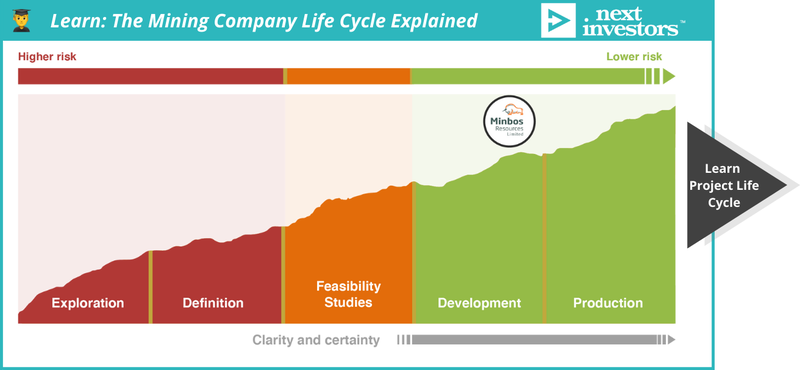

Mining companies (including phosphate) go through a process of exploration, resource definition, feasibility studies and eventually into development.

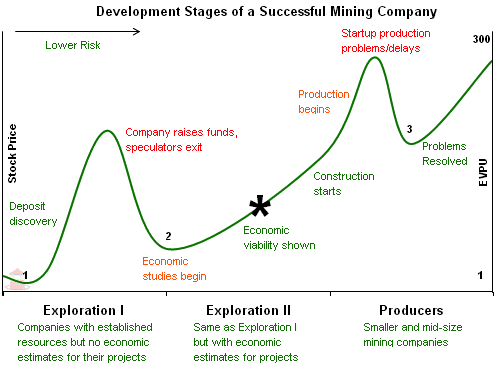

The image below shows exactly where MNB is in that development process. MNB has moved though “exploration I”, MNB is right along the end of the “exploration II” stage.

The above image shows that there are two times in a mining company's lifecycle where the its share price is likely to significantly re-rate.

The first is when the discovery is made and resource definition programs commence. The second is when the company moves from feasibility studies into construction and eventually first production.

MNB is towards the lower risk end of this process and we think that with a construction decision likely this year, the company is heading to the point where the market may re-rate MNB from explorer to producer.

Learn: The Mining Company Life Cycle Explained

As mentioned, MNB completed a scoping study (the orange feasibility studies stage on the image above) in 2020, returning the following results:

- Post-tax NPV of US$191-308M (A$260-420M).

- Low upfront CAPEX of US$22-28M (A$30-38M).

- 21 year mine life.

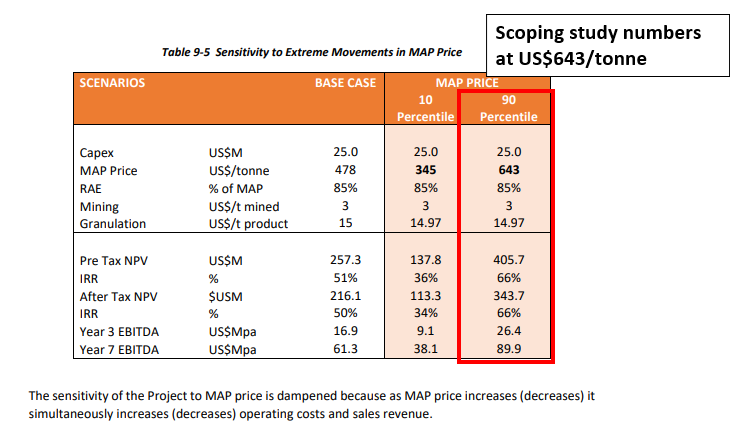

This was calculated using a US$357-482 per tonne phosphate price (MAP Price). MNB also released a best-case scenario with phosphate prices at US$643/tonne where the after-tax NPV was US$343M.

But now, with the phosphate price at ~US$700/tonne, we think the post tax NPV should be at, or above, US$400M (A$546M).

The caveat here is that over the last two years the input prices of almost everything in the construction industry have risen, so we would expect to see costs increase too.

The positive is that MNB has heaps of headspace with the scoping study showing a 14X return on the estimated US$22-28M upfront CAPEX requirement. We are hoping the increases in costs to be offset by the increase in fertiliser prices.

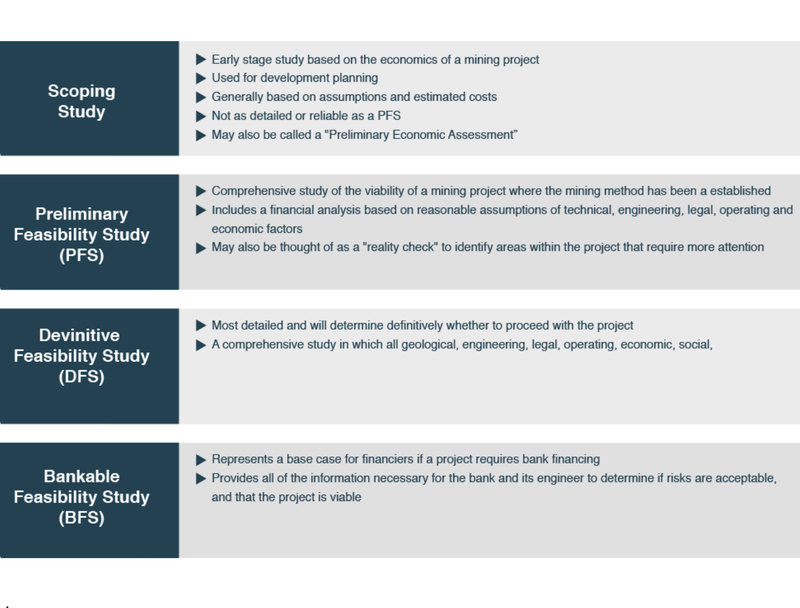

The next stage before getting the project development ready is usually completing a Pre-Feasibility Study (PFS), but MNB has confidently skipped this, having moved straight to a Definitive Feasibility Study (DFS).

For a project to reach the development stage, a completed DFS is generally a minimum requirement. If there is a need for significant debt financing, an explorer is more likely to also complete a Bankable Feasibility Study (BFS).

In the case of MNB, we don’t think that the company would have trouble raising the required CAPEX, especially considering where phosphate prices are.

As a result, we think a DFS should be more than enough for MNB to take its phosphate project into the development/construction stage.

This is exactly where MNB is — currently completing its DFS and the long-lead items for the development of the project being ordered.

As part of the DFS process MNB has completed the following:

Mining licence granted ✅

Early last year MNB was granted a mining licence over its phosphate project.

Having been granted well in advance of the DFS and any construction decision means that when MNB is ready and all of the environmental permitting is completed, it can simply start mining.

Phosphate plant design ✅

MNB recently signed an agreement with a Brazilian EPCM contractor (EPC Engenharia) as part of the processing plant design and delivery.

Just yesterday, MNB announced that the DFS ready plant design had been completed, modelled on a 150,000tpa facility with the potential to expand throughput to 450,000tpa.

This forms a part of the DFS’s cost estimation process, giving MNB a more detailed design of its plant and a highly accurate estimate of how much it will cost to construct.

Resource upgrade ✅

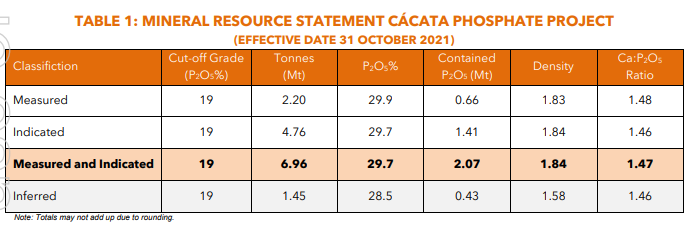

MNB has completed a resource update for a total measured, indicated and inferred mineral resource of 8.5mt @29.6% phosphate. The updated resource is important because it forms the basis for the mine plan that goes into the DFS.

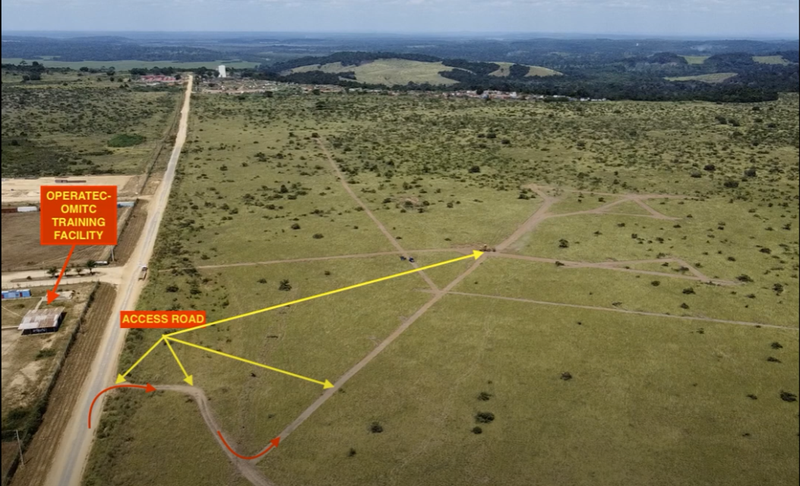

Site secured to construct granulation plant and long lead items ordered ✅

Last August, MNB secured the site where it plans to build the phosphate granulation plant — this sets the base for the design of all the processing infrastructure costs in the DFS.

The video below, showcasing the site, was rather interesting to us:

MNB has also approved the purchase of key long lead items, well in advance of development of its phosphate plant development. This will allow for the project schedule to be fast tracked when the time comes to start plant construction.

$6M raised to deliver DFS + environmental approvals ✅

Late last year, MNB raised A$6M in a Placement @10c per share (directors and management took $595k in the raise). As of 31 December 2021, the company had $6M in cash in the bank.

With the balance sheet recapitalised, MNB should have enough cash to complete all of the DFS work and move its phosphate project towards being construction ready.

What’s next for MNB’s fertiliser project?

Definitive Feasibility Study (DFS) 🔄

The last 12 or so months have been all about getting the background work done on the DFS, which we expect to be delivered by the end of Q2-2022.

We will be looking to see firmed up costs for all of the upfront CAPEX that MNB needs to commit, and a detailed mine plan showing targeted throughputs and production numbers.

The completion of the DFS would mean MNB has ticked off one of the key objectives we set in the “what we want to see MNB achieve in 2022” section in our Investment Memo.

Environmental permitting 🔄

In the latest quarterly report, MNB confirmed that the EIS and EISA reports for both its mine and granulation plant were nearing completion, with submissions expected by the end of the quarter.

This is the last step before MNB can commence construction works across both its processing plant and its phosphate project. We don’t know when these will be reviewed and approved by the regulators, but we hope it will be by the year’s end.

Maiden ore reserve estimate 🔄

The final stage of the resource definition for a mining company is to produce an ore reserve.

In its recent quarterly report, MNB forecast the announcement of a maiden ore reserve before the end of this quarter.

We expect this to be some of the last news delivered before the DFS is completed.

What about MNB’s “zero carbon” green ammonia ambitions?

We mentioned in a previous note that MNB had started desktop studies on a potential zero carbon ammonia project.

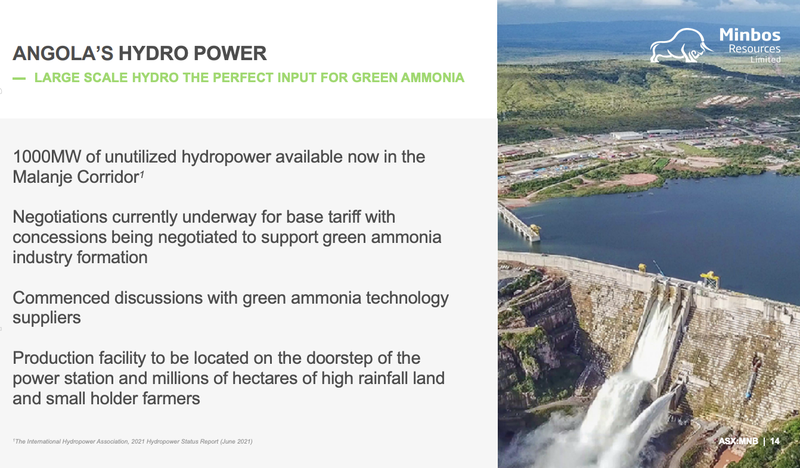

Since then, MNB has received support from the Angolan Ministry of Agriculture to progress the development of the project on a site nearby the Capanda hydroelectric dam, which the government says could provide 100MW of hydro-power to MNB’s project.

In the letter of intent MNB lodged with the ministry for agriculture, the company laid out its plan to develop a nitrogen fertiliser facility using green ammonia produced from hydroelectric power from the Capanda Hydroelectric Dam.

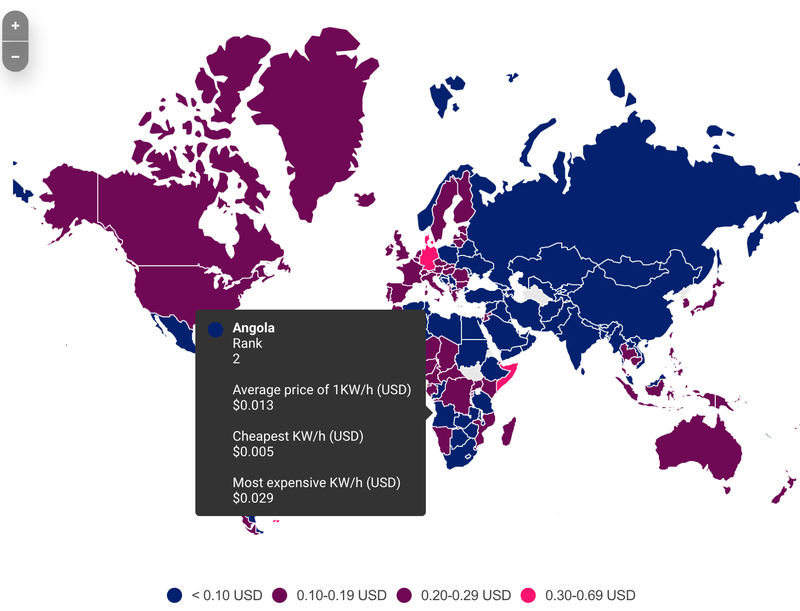

To produce green ammonia competitively the plant needs to be built in a region with an abundance of cheap renewable energy power — exactly what Angola has.

As you can see in the image below, Angola ranks second for the cheapest source of electricity on the planet, so Angola ticks the box for “cheap source of power”.

Angola also ticks the box for an abundance of renewable energy power with over 1,000MW of hydropower available throughout the Malanje province alone.

Add in the fact that Angola has no established fertiliser industry and MNB has the perfect recipe to be a first mover in an industry that we think will become of strategic importance to the country in the future.

But what is green ammonia and what is it used for?

Before we get into what MNB plans to do with its green ammonia plant, to learn more about how ammonia is produced and to get an idea of what a production plant would look like, read our previous note where we did a short explainer here.

According to Forbes green ammonia is “A Key To The ‘Hydrogen Economy’ (source)

But today we will focus on ammonia’s applications in fertiliser.

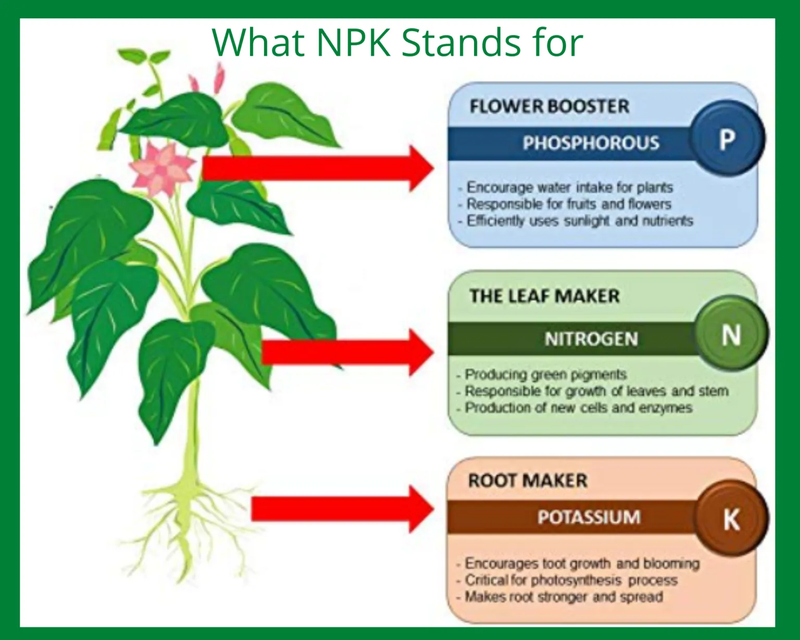

Ammonia is the key ingredient to producing “nitrogen fertiliser”, which is simply a mix of phosphate and nitrogen.

These nitrogen fertilisers are becoming increasingly popular because of the impact they have on improving crop yields. The key differentiator from standard fertilisers is that nitrogen is released over time, which is an essential nutrient for growing plants.

The resulting fertiliser is referred to as “NPK” fertiliser.

At the moment ~80% of global ammonia production goes into fertiliser and almost all of it is produced using fossil fuels.

The key advantage for MNB in producing fertiliser is that it has access to cheap and renewable energy sources. This means it can produce zero carbon “green ammonia” — ESG proofing its end product.

With MNB so close to developing its phosphate project, the move to also produce zero carbon ammonia could see it also become a supplier of nitrogen fertiliser in Africa.

With Angola (and most of Africa) dependent on ammonia and/or fertiliser imports, local supply will be a game changer as transportation/internal handling costs currently comprise ~45% of the cost of landed fertiliser products.

What's next for the zero carbon green ammonia project?

Progress securing renewable energy power 🔄

MNB is currently engaged with Angola’s Ministry of Energy and Water to try to secure ~200MW of hydropower from the nearby Capanda Hydroelectric Dam.

MNB already has confirmation that ~100MW of power can be supplied to its zero carbon green ammonia project, but it has requested up to 200MW through a staged tariff structure to offset high fixed costs during the initial development phase.

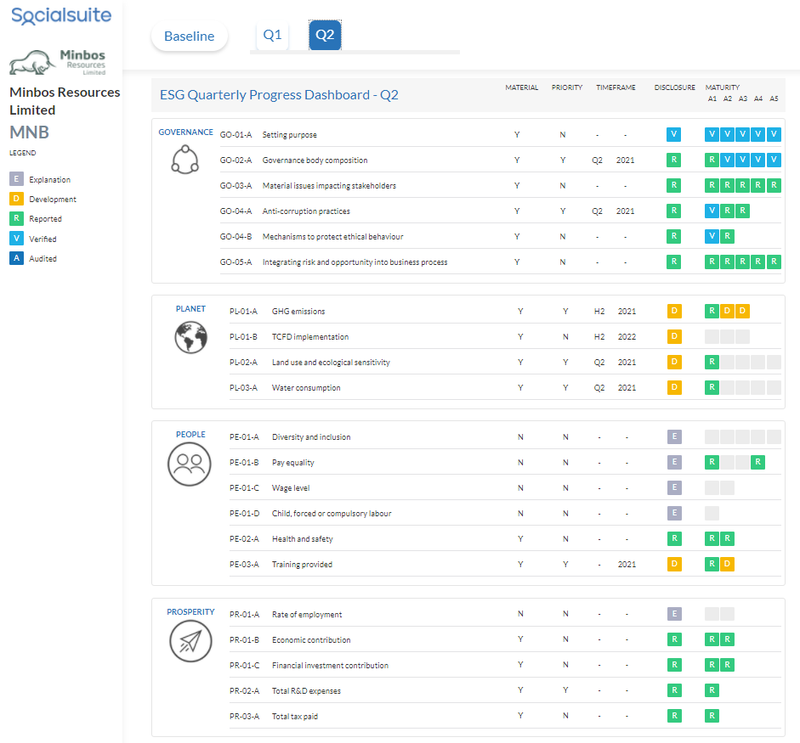

MNB discloses Environmental, Social and Governance (ESG) progress.

Global fund managers, high net worth family offices and millennials are now actively seeking to invest exclusively in ESG companies. Consumers are demanding best in class ESG products and smart people only want to work with top ESG credentialed companies.

MNB uses the world economic forum ESG framework to regularly report their ESG progress so they can best tell their story to international ESG investors.

MNB’s ESG goals are multi-faceted in sub-Saharan Africa:

- Improve food security and nutrition

- Decrease levels of poverty

- Mitigate the impacts of climate change on farmers.

MNB in the right place at the right time?

Having established what MNB is working towards, it is important to put some context behind it.

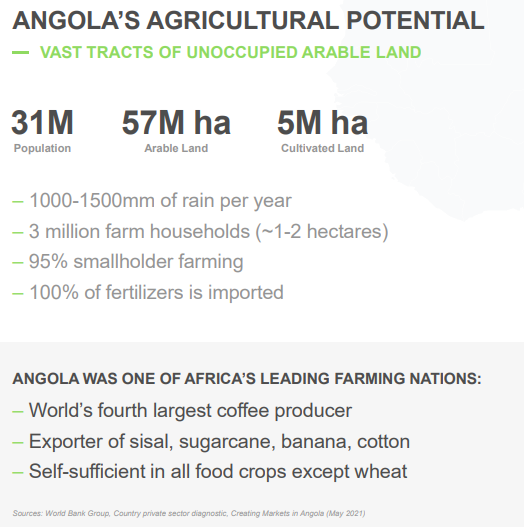

Keep in mind that MNB is developing its projects in a country with the potential to become one of Africa’s biggest agricultural hubs.

The company’s latest investor presentation summarises this perfectly – Angola has what it needs to become an agricultural powerhouse in Africa. The country has 57 million hectares of arable land available for farming yet only 5M hectares cultivated, and it has a cheap source of hydroelectric power.

And with 100% of its fertiliser imported, the key to unlocking Angola’s agricultural potential will be an affordable domestic supply of fertiliser.

The challenge for Africa’s agricultural industry has always been crop yields, largely due to lower rates of fertiliser consumption compared to more economically developed regions.

For example, according to The World Bank, the average fertiliser consumption in this part of Africa is estimated at ~20 kilograms of nutrients per hectare of farmland, versus ~128 kilograms of nutrients per hectare of farmland in developed countries such as the US.

One of the main reasons for this lack of consumption is affordability — most of the continent's farmers are small family run businesses, meaning the cost of purchasing imported fertilisers isn't feasible.

This is where the opportunity lies for MNB as a first mover in supplying fertiliser to a region that is in desperate need of it.

MNB 2022 Investment Memo

Our “Investment Memo” is a short, high-level summary of why we continue to hold a position in MNB and what we expect the company to deliver in 2022.

We’ll be using these Investment Memos as a way to assess the company’s progress over 2022 and also examine how our investment thesis plays out throughout the year.

In our MNB Investment Memo you’ll find:

- Key objectives for MNB in 2022

- Why do we continue to hold MNB

- The key risks our investment thesis

- Our investment plan.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.