Big Few Weeks for NHE - Farm in bids due end of quarter

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 4,166,307 NHE shares and 2,437,037 options, and the Company’s staff own 64,339 NHE shares and 4,000 NHE options at the time of publishing this article. The Company has been engaged by NHE to share our commentary on the progress of our Investment in NHE over time.

Two high impact drilling events to come in 2023 alone - in a frontier location in Africa - targeting a large prospective gas resource.

As with most gas exploration programs of this scale, we have observed that the share price usually runs up in the lead up to drilling.

Our strategy is to Invest early, well ahead of drilling events, patiently hold in the hope that the share price will run enough into the drilling event so we can Top Slice and/or Free Carry while maintaining the majority of our position into the result.

Or in this case, the TWO drilling events...

Given the opportunity for a large discovery and outsized success - this is the kind of Investment we like - and it's what Noble Helium (ASX:NHE) shareholders have to look forward to this year.

NHE has some of the best acreage in the most prospective untested helium ground on the planet.

On one project alone, there’s potential for the world’s third largest helium reserve (behind the USA and Qatar) - and largest primary reserve.

However, NHE is going to need to drill test this potential - and that's what the two upcoming wells will be all about.

Space travel, computer chips, and other high-tech industries rely on helium.

Russia could be on course to control around a third of supply in the next 6 years.

And it’s finite.

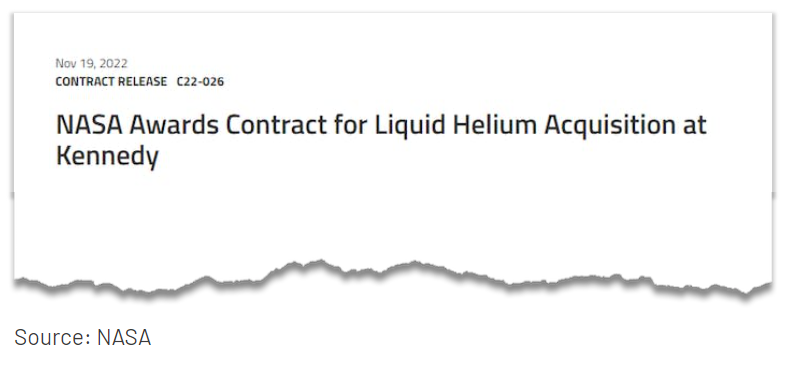

Despite being a relatively opaque market, a recent publicly available helium supply contract has shown that helium prices can go over US$1,100Mcf - that’s a thousand cubic feet (see NASA helium contract later in note for details).

NHE has a certified Mean Unrisked Prospective helium resource of 175.5Bcf (billion cubic feet).

That’s equivalent to ~30 years of the world’s current annual helium needs - on just ONE project alone.

However, while those prospective numbers look big, this is untested with the drill bit, and we would naturally expect this volume to be lower in the event of a discovery. The more defined the resource, typically the smaller it gets.

There are a myriad of variables at play here, but the annual helium market is worth ~US$5BN and that gives a bit of a sense for the scope of NHE’s projects.

NHE is currently in ‘execution’ mode as it gears up to drilling, and we are expecting newsflow to build as drilling draws near.

NHE is currently capped at $30M and had $6.2M in the bank at Dec 31st.

By the end of Q1 (only a few weeks away) we are looking out for:

- Drill targets defined

- Farm out offers in (non binding at a minimum)

- Bonus: drill rig contracted (in cooperation with AIM listed Helium One)

Each one of these events could be to share price catalysts in their own right.

NHE recently raised $6.1M at 15c, and the April 2022 IPO was priced at 20c.

NHE is currently trading around ~14c - so there’s likely a lot of investors currently underwater on this one.

It feels a bit dormant and under the radar at the moment - however we don't think it will take much for the market to catch on to NHE in the lead up to drilling, given the size of the targets and potential for a large new discovery.

We’ve been holding our NHE position patiently as drilling gets closer - and we spotted a couple of key bits of helium market news last year which confirm our hunch that “security of helium supply” is becoming critical for the high tech industries that use the gas.

For example, in August last year, a “Major Space Launch Company” signed a long-term contract with a Canadian helium company for supply starting in 2023.

Hmm, we wonder, who could that be...? There aren’t many around...

We also note that in November, US space agency NASA announced a contract that could be worth up to US$1BN over the next four years to secure forward supply of helium.

If NHE's helium drilling is successful, then we think that its project will be of global significance due to the scale of its resource, and the security of supply it provides vendors.

Helium is a resource that is very much defined by geopolitical factors given the industries it is critical to.

Which makes the selection of a farm out partner all the more important...

According to NHE’s latest announcement, farm out discussions are being advanced via discussions with “multiple parties”, with non-binding bids due by the end of Q1.

Here are some current major helium suppliers as we identified in our recent note:

- Air Products and Chemicals

- Exxon Mobil

- Air Liquide

- Qatargas

- Linde Plc

We wonder if they might be interested in securing exposure to an early stage, significant undrilled prospective resource via a farm in...

We think a farm out will not only give the market a grip on how to value NHE’s ground, it would also validate the prospectivity of NHE’s projects as it goes after a potentially company-making helium discovery in Tanzania.

A farm out has the dual benefit of limited or no dilution and (if it's a good one) enough cash to cover the costs of the two wells.

A lot of work has gone into getting NHE to this point.

NHE Managing Director and CEO Justyn Wood built this company from the ground up over many years and we’re quickly approaching NHE’s first pass at what we hope is another East African Rift System “String of Pearls”.

Meaning a successful drill program at this Basin Margin Fault Closure play, effectively opens up the basin for high probability drilling success at a number of other sites in the basin.

Get at least one well right, then other subsequent drilling programs should be successful as well - at least that's the theory.

Needless to say, our anticipation is building ahead of NHE’s Q3 drilling events.

Here’s a quick summary of why:

- Experienced CEO - NHE CEO Justyn Wood brings significant East African Rift System experience. He played a key role in opening up the region’s geology with breakthrough exploration success in 2006 with Hardman Resources (~2c to $2.50).

- Successful drill team - Dermot O’Keeffe joined as drilling exploration manager in November. O’Keeffe and Wood have a long history together that dates back to the early 2000s. The pair helped to open the Albertine Rift Basin in western Uganda, making two oil discoveries for Hardman Resources. These were Basin Margin Fault Closure plays which had a 100% success rate.

- Massive undrilled prospective resource - NHE has an independently certified Mean Unrisked Prospective helium resource of 175.5Bcf in the Rukwa Basin — just one of its four project areas in Tanzania. By itself, NHE’s Rukwa Basin has the potential to be the world’s third largest helium reserve behind the USA and Qatar. It has the potential to provide the equivalent of approximately 30 years’ of (current) annual helium supply.

- Highly prospective geology - In Uganda and Kenya, the East African Rift System has a 80% success rate from over 30 exploration wells, including a 100% success rate for oil and gas wells (14 from 14) since first oil in 2006. Tanzania’s East African Rift basins possess the same reservoir-seal-trap as these oil and gas wells, but are charged with another type of gas – helium, which is seeping to the surface at up to 10%. With similar geological fundamentals at work, this bodes well for NHE’s exploration work in Tanzania where the same exploration techniques are being used.

- Multiple leads, with big rewards on offer - NHE is working with 9 leads (prospective targets) for drilling and is in the process of narrowing these down to the best two candidates. For example, the Chilli Chilli structure has a mean Prospective Helium Resource of 10.5 Bcf (billion cubic feet) and NHE says this by itself could be an economically viable helium target assuming a price of ~US$450/Mscf (thousand cubic feet) for long-term liquid helium contracts. There are at least two other leads of a similar scope.

- Opportunity for “String of Pearls” - if NHE is successful with its first two drill targets it could result in multiple successful drilling events down the track. If NHE drills the first “pearl” and it turns out successful, it implies all the other leads (pearls) could be successful too - effectively opening the basin up as one of the world’s largest helium reserves. This is down to the geology that NHE is working with.

Our ‘Big Bet’

“NHE discovers the world’s largest helium reserve held by a single company and is strategically acquired by a major company OR a state owned enterprise to secure supply (USA, China, Qatar).”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done and many risks involved - some of which we list in our NHE Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

To monitor NHE’s progress since we first Invested and to track how the company is doing relative to our “Big Bet”, we maintain the following NHE “Progress Tracker”:

Click to see our NHE Progress Tracker here:

Space industry snapping up future helium supply

NHE’s big drilling event in Q3 takes place within the context of rapidly accelerating trends in technology.

The commercialisation of space travel is happening right now before our very eyes - SpaceX made 28 orbital launches in 2021, and 61 in 2022.

Helium is used to keep hot gases and extremely cold liquid fuel separated during lift-off of rockets - it is a crucial part of launch safety.

The space industry looms as a major driver of helium demand growth - and we think this industry can give us clues as to where companies that use helium think the price could be in a few years time.

So with the space industry projected to have a compound annual growth rate of 10% in helium demand and given the July 2022 helium shortage crisis - it makes sense that space exploration organisations started to move quickly to secure supply last year.

For instance, in August of last year a Canadian helium company signed a deal with a mysterious “Major Space Launch Company” - with no specific dollar values assigned and initial deliveries slated to begin this year.

Then in November we got a good look at what a potential price for helium could be well into the future when the US government space organisation, NASA, released details of a contract that it had signed US based Air Products and Chemicals (capped at US$63BN).

That contract was to supply 33 million litres of liquid helium to NASA's Kennedy Space Center for an initial 23 month period, and potentially through to 2027.

The contract could be worth up to US$1.07BN.

Another helium company placed the implied price per Mcf at over US$1,100:

Following the loss of the BLM source of helium, NASA has done a potential deal with Air Products to supply helium for over $1,100/mcf. #BNL will be providing high-grade helium into the US market from its Voyager and Galactica/Pegasus discoveries. For more: https://t.co/vWnJNaBwCc

— Blue Star Helium Limited (@HeliumBlue) November 23, 2022

And just to check, we ran some rough numbers on what the implied upper bounds of a price per Mcf would be in this NASA contract and came to the conclusion that it could be ~US$1,224 an Mcf:

- One litre of liquid helium expands to 750 litres of helium gas

- 750 litres = 26.486 cubic feet

- Multiply by 33 million litres

- That = 874,038,000 cubic feet

- US$1.07BN divided by 874,038,000

- Or ~US$1.224 a cubic foot x 1,000

- Gets us ~US$1224 an Mcf

We calculate a helium price of ~US$1,224 an Mcf based on NASA’s November contract.

Ultimately given that figure we calculated is roughly 4x the price of US helium in 2019 - we think this premium pricing gives strong incentives for helium exploration.

Like the exploration that NHE is doing right now.

Note that these calculations are our own internal workings and interpretations of one helium contract - we made some assumptions based on limited information - which could be incorrect.

Demand for helium, like all products, is susceptible to change, and there is no guarantee that the price of helium will continue on this trajectory, especially as more helium supply comes online.

It’s also important to note that the value of helium in the ground is less than the value of helium that is ready for delivery, given the capital, development and transport costs required to move into production.

NHE’s current resource is an unrisked prospective resource, the lowest level of confidence, so the chances that the entire resource will move to the higher ‘reserve’ level of confidence is extremely slim.

You can read more about understanding oil and gas resources here: 🎓 How to Read Oil & Gas Resources

With that said, this price point of ~$US1224Mcf for helium gives us an idealistic value of the potential value of NHE’s project, especially ahead of drilling.

We expect that NHE is in the process of sharing more data with potential farm out partners right now - and that this farm out will form part of the basis of how the market values NHE’s potential helium resource.

What’s NHE done since our last note?

Cooperation agreement with Helium One to secure drill rig ✅

The cooperation agreement between NHE and the company’s Tanzanian helium neighbour, London listed Helium One, is designed to ensure that both companies work together to source the right rig for their respective drill programs.

This means NHE should derive some cost savings from the arrangement.

As we’ve said before in previous notes - we think the two companies can win together in Tanzania.

Should Helium One make a discovery - it would further validate the overall prospectivity of Tanzania to NHE’s benefit i.e there could be an ensuing wave of market sentiment for NHE on the back of Helium One’s success.

Conversely, should Helium One fail to make a discovery, this would have little specific geological bearing on the likelihood of success for NHE’s drilling of the company’s two wells. Helium One is targeting a different play type

Completion of 3D seismic ✅

This was a core component of NHE’s exploration program and is a key part of NHE’s mapping of potential traps in the Basin Margin Fault Closures that the company is targeting. The final stage of the Phase 1 3D seismic was completed - read this Quick Take to learn more about the leads NHE is working with.

And with drilling getting ever closer, NHE has the following milestones ahead of it.

What’s next for NHE?

We are expecting a lot of activity for NHE in the lead up to the Q3 drilling event. As each of these milestones are accomplished we expect more and more interest to grow in the story.

Best two drill targets selected 🔄

We suspect that NHE is quickly narrowing down 9 current leads towards having two ideal candidates for drilling. This gives NHE two shots at a discovery, ideally with both drill targets delivering a discovery.

Farm out partner secured 🔄

The selection of the two best drill targets would enable NHE to shop out its project to potential farm out partners to de-risk the project further.

NHE would be showing these potential partners the data that it has collected, and the projected payback on a discovery.

With LAB Energy Advisors Ltd appointed to manage the farm out process - we’ll be looking for an announcement around this towards the end of Q1 (i.e around March, or earlier).

Rig contract executed 🔄

With the cooperation agreement with Helium One, we’re hoping NHE will announce a rig contract towards the end of this quarter (ending 31 March) or early in Q2. Both companies will be keen to have this locked away.

Rigs are not always easy to come by in this part of the world, but with an experienced drill manager appointed in Dermot O’Keeffe we’re hoping the NHE team can secure the right rig at the right time and for the right price. Any delay here could impact the company’s timeline (see risks section).

The big one: Drilling 🔄

A serious drilling event that could have historical significance looking back in a few years time.

We don’t say that lightly.

Scheduled for Q3 of this year, NHE is going after a Mean Unrisked Prospective helium resource of 175.5Bcf that could secure a part of the world’s supply of this finite gas well into the future.

NHE has previously referred to a benchmark of 6Bcf recoverable helium as a “company maker”.

Closer to the drilling event, we intend to outline our bull/bear/base cases for NHE.

All going well we’d be looking for a proven helium structure, commercial helium grades and a commercially viable flow rate.

Pre-drill run? Our NHE Investment Plan

As with our other previous exploration stage oil & gas investments we Invest early, well before the main drilling event and will aim to be free carried and have taken profit before the drill results are announced in 2023.

We look to hold at least 50% of our initial position into the first drill result and this is usually a ~3 year strategy.

Part of our Investment Plan is based around our experience with other major gas drilling events.

We’ve found over our many years of Investing that as speculative fervour around a big drilling event builds, there is a good opportunity to Top Slice and/or Free Carry, provided we’ve Invested well ahead of the drilling event.

This doesn’t always play out of course - and it may not play out with NHE.

We’ve seen it with a previous Investment in Africa Oil and more recently with Invictus Energy which we remain Invested in:

As we wrote about above, NHE isn’t alone in helium exploration in Tanzania. A comparison can be drawn with NHE’s London listed neighbour Helium One, which saw a similar IVZ-style pre-drill run play out, albeit over a shorter period due to the proximity of its drilling after listing in London.

Helium One, which is also working in the Rukwa Basin (and now with NHE to secure a rig) re-rated ~300% in the lead up to its maiden drill program in Tanzania:

And obviously as the chart shows - the Helium One share price suffered after the company wasn’t able to deliver a flow test.

But Helium One is gearing up to drill again, and we’ll be watching the company closely to see if the pre-drill re-rate pattern repeats itself again.

While there’s no guarantee that NHE’s share price will move like Helium One’s did (or IVZ for that matter), our experience with other big frontier gas drill events tells us pre-drill price run could be on the cards.

We must note that past performance is never an indicator of future performance, and drilling frontier locations is very risky.

What could go wrong?

These are the three risks we are most focussed on as NHE approaches drilling in Q3, exploration risk, operational risk and funding risk.

Exploration risk is a primary risk for NHE.

Just because the initial signs from the exploration program are positive, there is no guarantee that NHE will make a discovery when it drills.

As the experience of Helium One shows, the sell-off ensuing from a failed drilling event can be harsh.

In terms of operational risk, there is a chance that NHE is unable to secure a rig in time to drill prior to the wet season in Tanzania.

This wet season can start in October and stretch through to December. Without drilling during this period, there is a possibility that the share price could soften with no tangible newsflow in that time.

Finally, as our first NHE memo reflected its IPO funds - we’d also note that funding risk could now materialise if a farm out partner is not secured. We will know more on this in the coming months.

Our NHE Investment Memo

Click here for our Investment Memo for NHE, where you can find a short, high level summary of our reasons for Investing.

The ultimate purpose of the memo is to record our current thinking as a benchmark to assess the company's performance against our expectations following the launch of the memo.

In our NHE Investment Memo, you’ll find:

- Key objectives for NHE

- Why we are Invested in NHE

- What the key risks to our investment thesis are

- Our investment plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.