What is going on in the lithium market right now?

Published 16-MAY-2023 15:19 P.M.

|

6 min read

One of the hottest sectors across markets for the past five or so years has been battery materials.

The hottest of them all - lithium.

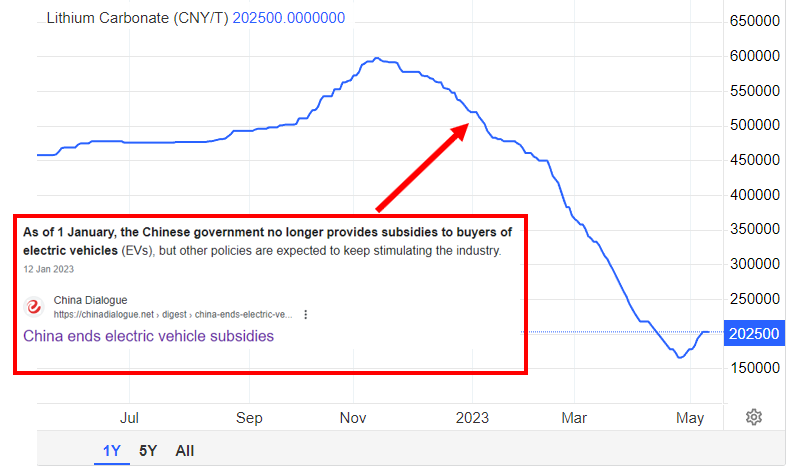

Up until the end of 2022 lithium prices were trading near record highs but in the first half of this year, spot prices have come down almost ~67%.

Today we look at what is going on in the lithium space and try to answer whether or not the price falls are structural or just short-term volatility.

Why has the lithium spot price come down?

In January China announced it would start reducing electric vehicle subsidies, understandably, demand for lithium took a short term hit.

The news also came at a time when the Chinese macro outlook is challenged with a slowing manufacturing sector and sluggish economic growth.

China is currently responsible for ~60% of all lithium processing, so any slowdown in China has a flow on effect on the demand for lithium.

The lithium market is not as mature as say the copper or iron ore markets - this lack of maturity means small changes in demand can impact SPOT prices significantly.

As a result, a large part of the transactional volume in the market is done via contracts and less so through the spot market.

Small changes in demand mean prices overshoot to the upside and downside - almost always the lithium trade continues at prices somewhere in between these fluctuations.

Eventually, pricing boils down to long term structural demand/supply - which we will touch on next.

Just a side note on prices*

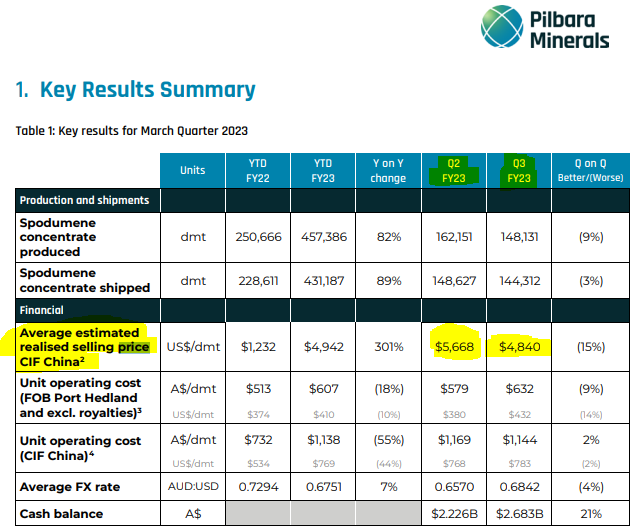

A good way to gauge the ACTUAL market price for lithium is to look at what the producers are selling their products for.

For context, in the March quarter (2023) Pilbara Minerals only saw a ~15% fall in prices for its lithium.

So while spot prices are down, the majors are still seeing demand for spodumene concentrates (which is eventually turned into carbonates/hydroxides).

We think this likely means demand for lithium is a lot stronger than the spot price may be suggesting.

The medium-long term demand/supply outlook:

Typically, when spot prices get hit as hard as lithium has been recently, it could be signaling structural change in the supply/demand for that specific material.

Lithium is a little bit different.

While in the short term, demand from China for batteries/electric vehicles and in turn lithium has come off, the medium to long term outlook is unchanged.

In 2022 for example, global electric vehicle sales were up 55% and are expected to grow another 35% this year.

In China sales were up 90% in 2022 and are already in the first quarter of 2023 electric vehicle production is up ~27.7% versus the same period last year.

American, European and Asian carmakers have all made commitments to completely electrify their vehicle fleets by the years 2030, 2040, or 2050.

Couple this with the demand coming from the battery energy storage industry which is expected to grow ~15x by 2030 and the supply/demand imbalance outlooks starts to look a lot worse.

We think that short term fluctuations in the lithium price will ultimately just be “noise” and we expect there to be demand in excess of supply through to the end of the decade.

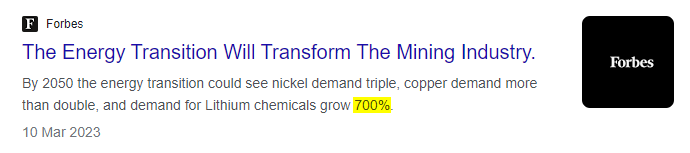

By 2050 demand for lithium is expected to increase by ~700%.

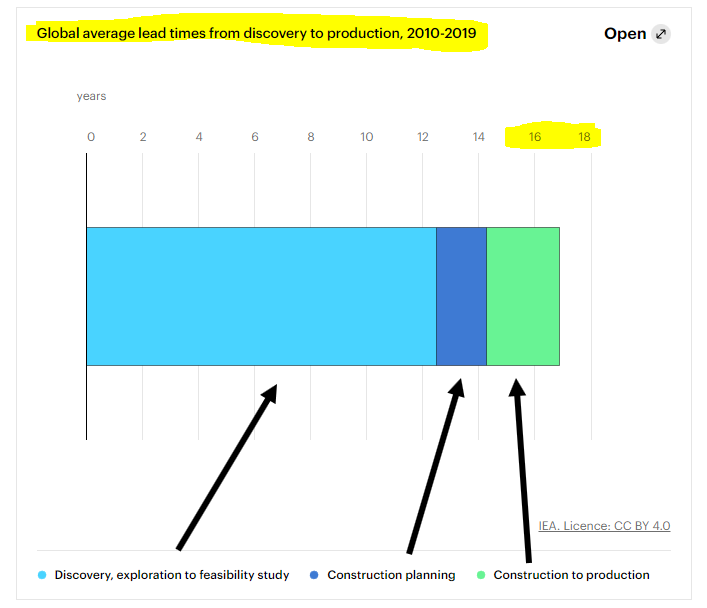

On top of all this, it takes only ~2-3 years to build downstream processing/battery manufacturing facilities BUT it can take ~17 years to take a critical minerals project from discovery into production.

If we take 2016 as the starting point for the rush to secure lithium supplies it could mean the shortages persist through to ~2033.

A spanner in the works was the recent introduction to the US Inflation Reduction Act (IRA) in which tax credits for EVs were excluded for companies that don’t use raw materials from “friendly sources”.

The new IRA rules dictate that electric vehicles can only qualify for subsidies if more than 40% of the critical raw materials in the battery come from the US or a country it has a free trade agreement with the US.

Cars with batteries that are built with raw materials sourced from “unfriendly” countries would not be eligible for subsidies which would make them less competitive in the marketplace.

Our view:

We see the lithium market being structurally short of supply over the next 5-10 years.

Supply - even in the most aggressive case where a company is going flat out - can take a minimum of 7 and up to 17 years to come online (from discovery to production).

So while we expect to see short term fluctuations in spot prices, we think that in the long run, demand will exceed supply and prices will stay above the marginal cost of production.

What are the major lithium producers doing right now?

The majors who already have projects in production have been printing cash for the past 12-24 months.

Pilbara Minerals is a great example - the company posted a net profit of $1.24Bn for the first half of FY23.

That's $1.24Bn in 6 months.

Back in 2015, Pilbara’s share price was ~3c per share, for the first half of FY23 the company paid a dividend of 11c per share.

Pilbara ended the March quarter with $2.6Bn in cash in the bank.

So the question is how are the majors capitalising on the fall in prices?

The short answer - with M&A.

Here are some of the deals we have seen get done:

1. $34Bn Albermarle looking to takeover $6.5Bn Liontown Resources & rumours of a mystery third bidder looking to outbid Albermarle.

2. $9.6Bn Allkem looking to merge with $7Bn Livient.

3. $11.2Bn Independence Group and $25Bn Tianqi lithium’s $136M rejected offer for Essential Metals. Just a few weeks ago Mineral Resources announced a 19.55% stake in Essential.

We Invest in the smaller end of the market and are pretty comfortable holding onto our lithium portfolio companies.

In fact, we are backing them to accelerate the exploration/development of their projects so that they can position themselves as better M&A targets for the majors who are deal-hungry.

What we are doing right now:

We have seen this setup several times in the past.

Majors are minting cash from projects already in production.

Smaller companies that are in the exploration & development stages are being sold down because they are capital hungry & are seen as too far away from any revenues.

Share prices amongst the juniors are trading lower and lower, those in the larger end are holding up relatively well.

In markets like this we like to re-assess the prospects of the companies we hold, and if the opportunity presents itself, add to our existing shareholdings.

Times like this also bring valuations for early-stage companies back to reality and while we may have passed on some of these (purely based on valuation), we think companies become Investment worthy as valuations are reset.

In short - we are looking to add to our existing positions and are doing more due diligence on new opportunities in the lithium space.

See which lithium companies we are invested in right now here: Our Lithium Investments.