US oil giant Chevron is entering offshore Peru - just south of CND

The world’s third largest oil producer is preparing to enter offshore Peru - immediately to the south of our micro cap Investment Condor Energy (ASX: CND).

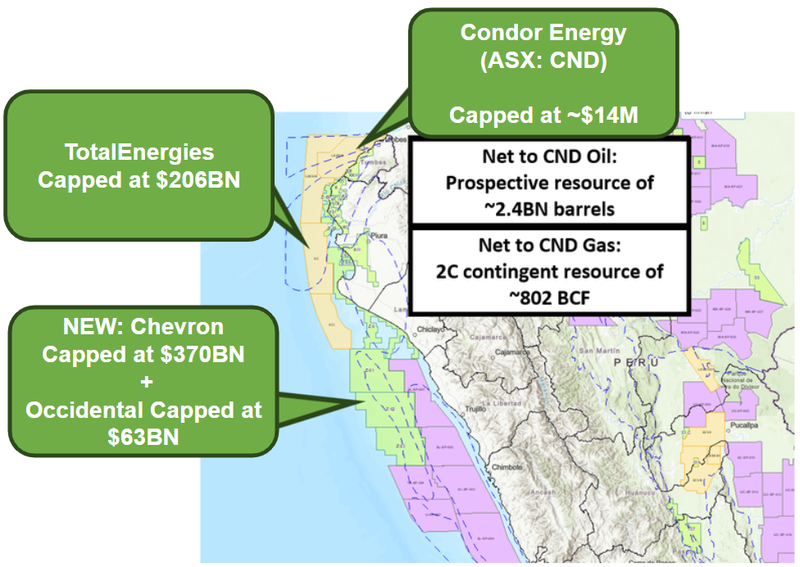

Scroll down for a map of exactly where each company’s acreage is…

We came across the below recent article from El Gas Noticias, which said Chevron was about to enter offshore Peru on oil exploration blocks partnering with the $63BN capped Occidental Petroleum:

(the original article is in Spanish so you’ll need to hit translate on the page if you want to read it in full in English)

(Source)

The article says that the structure for a deal on the three blocks offshore was submitted to Peruvian regulators a few weeks ago.

Once formalised, the three blocks would be owned:

- 35% by Chevron (world’s third largest oil company, capped at $370BN).

- 35% by Occidental Petroleum (capped at $63BN, with Warren Buffet as a major share holder).

- 30% by Westlawn (a US based private oil & gas investment company).

Occidental and Chevron are the second and third major oil companies to enter the region - with this deal coming after TotalEnergies started picking ground up surrounding our Investment CND.

CND was first to its assets - Total came after and now we have Chevron and Occidental in the region too…

Here is where everyone's blocks sit relative to the ~$14M capped CND:

Total, Chevron, Oxy now in Peru - FOMO to kick in?

The entry of another oil major into offshore Peru will start to create competitive tension for exploration blocks in this part of the world.

When CND first entered offshore Peru, there was barely any recent activity offshore.

Total and Occidental then came in and picked up big acreage positions.

Now with Chevron coming in, we think CND’s block becomes a lot more attractive for a major that is looking to get exposure to offshore Peru.

With the majors taking up their positions, ‘FOMO’ from those who haven't moved yet might start to kick in…

In April CND said that a farm out process had commenced and it had “multiple parties” in its data room.

AND it is now at the stage where it is ready to do a deal on its projects…

We think Chevron’s entry into the neighbourhood is good timing for CND.

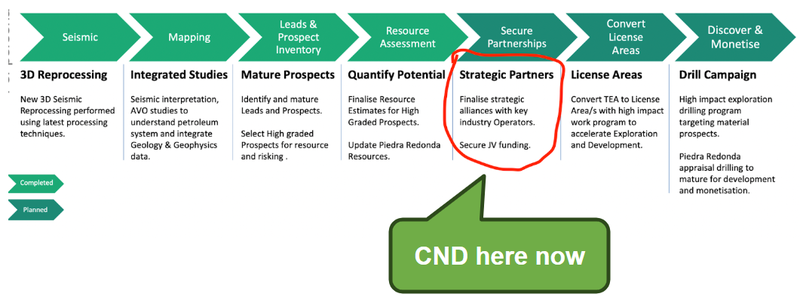

In a recent Investor Presentation, CND next goal is to Secure Partnerships - finalise strategic alliances with key industry operators, and ‘secure JV funding’:

(Source)

CND is “deal ready” with world class assets

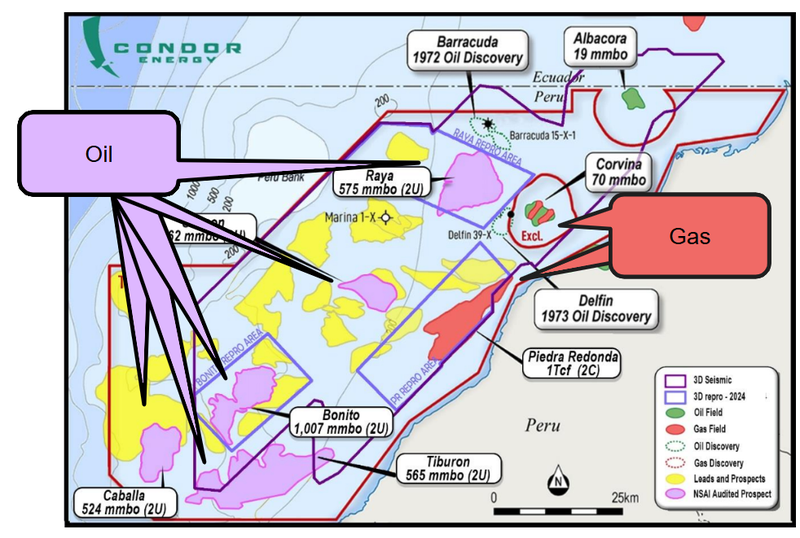

In April CND confirmed it holds a multi billion barrel prospective resource across five prospects, following an Independent Estimate.

The Total Best Estimate (2U) stands at 3 billion barrels of oil prospective resources (100% gross unrisked) across the five prospects.

This adds to CND’s substantial discovered gas field at Piedra Redonda of 1 tcf (2C).

We think a farmout deal will be a big catalyst for CND because it should provide significant funding for what we really want to see - either the gas project gets developed or a big exploration well gets drilled.

Farm out deals are typically share price catalysts.

A recent farm-out deal was what led to the rally of another ASX listed oil and gas explorer, Pancontinental which is exploring offshore in Namibia.

Pancontinental signed a deal with Woodside back in 2023 and rallied to a market cap of ~$230M.

CND is currently capped at ~$14M - which is why we think the farmout could trigger a rally in the company’s share price (assuming it is a good deal for CND).

The main reason we think CND is in a strong position now is because there are two potential deal avenues.

CND has an existing gas discovery at its Piedra Redonda asset AND big exploration prospects (totalling billions of barrels of prospective resources) scattered across its project area that could be farmed out as a collective (or individually).

The best way to think about the farm-out process is that, CND, by having both oil and gas assets, has a much larger target audience at the top of a ‘sales funnel’.

This includes both companies that are interested in high risk/high reward exploration AND companies that are looking for nearer term, lower risk development assets.

AND of course companies that are interested in oil and others that might be more interested in gas.

It’s hard to predict with so many different possibilities, but we think any of the following could be a big catalyst for CND’s share price:

- CND deals out its gas asset - maybe some of the proceeds that come from this can go toward drilling an oil exploration well? Maybe CND gets a free carried interest in an asset that could generate revenues in a reasonable timeframe?

- CND deals out oil exploration assets - CND gets a free carried interest in a well that would be fully funded by a farm-in partner. This means less dilution going into a big drilling event for existing shareholders…

- Maybe a combination of the two? - CND could bring someone in that is interested in both…

In any event, we think that a farm in deal could trigger a positive re-rate in CND’s share price.

There is also a precedent set for big deals to happen in Peru.

Back in 2009, KNOC (South Korean National Oil Corporation) and Ecopetrol (Colombian National Oil Company) signed a deal worth US$900M for projects to the south of CND’s block.

(Source)

And now we know Chevron is willing to come into offshore Peru (to the south of CND) and Total is happy to take all of the ground surrounding CND…

With the current market cap hovering around ~$14M, it could be an interesting upcoming period for CND.