PUR raises $1.1M to advance Argentinian lithium project

Our Argentine lithium Investment Pursuit Minerals (ASX: PUR) just completed a cap raise raising $1.1M at 6c per share in a “significantly oversubscribed” placement.

The placement also comes with 1:2 free options exercisable at 9c with a two year expiry.

We noticed PUR’s director also came into the raise for $70K.

We have also added to our position in the placement to try and maintain as much of our position in PUR as possible.

For us adding in this raise is a way of holding onto as much of our position in PUR as possible while the macro environment for lithium is negative.

Hopefully in the long run, when the macro turns for the better, the Investments we make at current valuations mean our average entry price is low enough for PUR to deliver us a nice return.

What is PUR using the cash for?

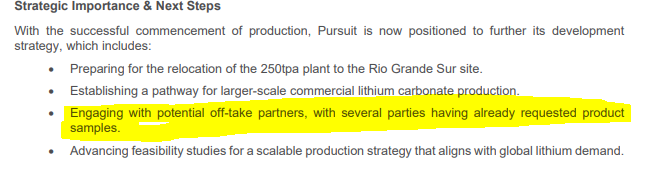

PUR confirmed in today’s announcement that the cash would be used to “advance Rio Grande Sur’s 250tpa Pilot Plant towards lithium carbonate production”.

PUR recently announced the plant was up and running processing synthetic brines, after today’s raise PUR should have the cash runway to transition the plant to slowly start producing battery grade carbonates.

Battery grade product will unlock potential offtake partners which PUR has said have “already requested product samples”:

(Source)

We covered all this in a recent Quick Take here: PUR’s lithium pilot plan now up and running

We also noticed in today’s announcement that PUR would use some of the cash to “evaluate further strategic acquisitions”.

Given PUR’s current market is ~$6M (at the 6c offer price) we don't mind seeing PUR look at acquisition opportunities, though our main reason for Investing in PUR is its lithium asset.

The latest from PUR’s project:

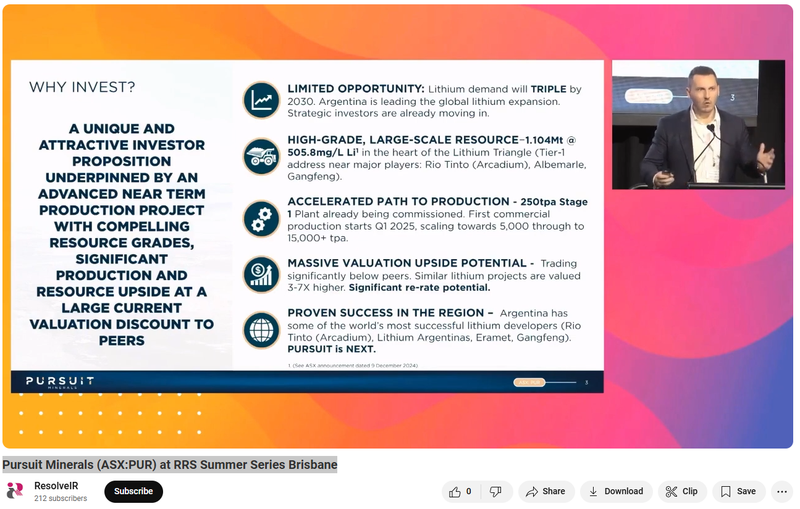

PUR’s Managing Director Aaron Revelle gave a pretty good overview of where PUR is at with it’s project in a presentation recently at the Resources Rising Star conference in Brisbane.

See that presentation here: Pursuit Minerals (ASX: PUR) at RRS Summer Series Brisbane

Aaron will also be presenting at the Ingite Investment Summit in Hong Kong on the 26th and 27th of March.

Anyone who is interested in scheduling a 30-minute meeting with Aaron can do so using the following link: https://weareignite.com/contact/#investor

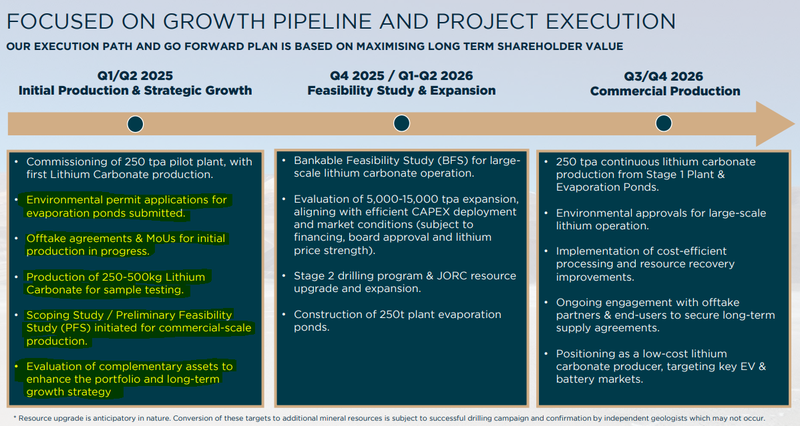

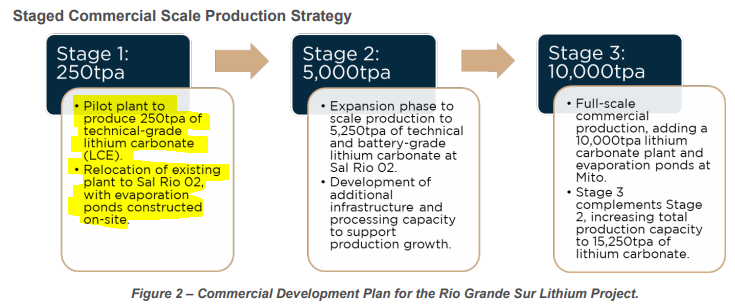

At a very high level, PUR’s plan is to develop its project in three stages.

First a 250tpa operation using PUR’s pilot plant on site, and then scale up in two stages, first to 5,000tpa then 10,000tpa.

The CAPEX estimate to get to stage 1 was estimated at US$9.751M, that would include:

- The costs to relocate the pilot plant

- Building out the evaporation ponds

- Building out all other associated project infrastructure.

So for ~US$10M, PUR would be able to produce ~250 tonnes per annum of lithium carbonate.

At today’s (depressed) prices, that would be ~A$4M in lithium carbonate production per annum.

To get an idea of what that would have been worth at the height of lithium prices - lithium carbonate prices were almost 10x higher in 2021-22. The same production from PUR’s planned stage 1 development would have been worth ~A$30M per annum in revenues.

Beyond stage 1 - PUR’s plan is to first build a 5,000tpa lithium carbonate plant, and then expand the project even further by building a second 10,000tpa facility.

What’s next for PUR?

The following slide from PUR’s presentation at the Resources Rising Stars conference in Brisbane gave us a pretty good idea of what to expect next from PUR.