PKP raises A$2.4M to fund Q4 production ramp up

Our “picks and shovels in a gold rush” Investment for the THC drinks sector, Peak Processing (ASX: PKP), has just announced a A$2.4M Loan Note raise (before costs) to fund its contracted Q4 FY26 production ramp.

Three things stood out to us about today’s announcement:

- PKP just delivered its first month of positive EBITDA under the new operating model.

In its Q3 quarterly out a couple of days ago, PKP confirmed March 2026 was the first month of positive EBITDA under the new management team with ~A$159K EBITDA on ~A$1.2M revenue.

While not a huge dollar number on its own, it’s a meaningful signal that the cost-out and operational reset that new management has been executing is flowing into the actual P&L numbers.

So with production forecasted to continue growing, we could see positive EBITA’s start to escalate alongside.

1. The raise is going into funding inventory for confirmed purchase orders.

So there should be a fairly locked in pay-back on the funds being raised.

Here is the detailed use of funds from today’s announcement:

The proposed use of funds:

- ~A$1.5M: inventory build for the ~1.5M units of confirmed Q4 FY26 production

- ~A$445K: accretive capex at the Windsor, Ontario facility, here the anticipated payback is under 12 months

- ~A$455K: general working capital, customer program support, CRA monthly installment, US working capital, and costs of the offer

2. PKP expects to be in a positive working capital position for the first time in recent reporting periods.

Combined with the cost-out and operational reset:

- A$2.25M in annualised cost savings already flowing through the P&L,

- The CRA payable reduced from a peak of ~A$1.8M down to ~A$200K under an agreed monthly repayment plan

PKP says today’s raise effectively completes the financial reset undertaken in FY26 under new leadership.

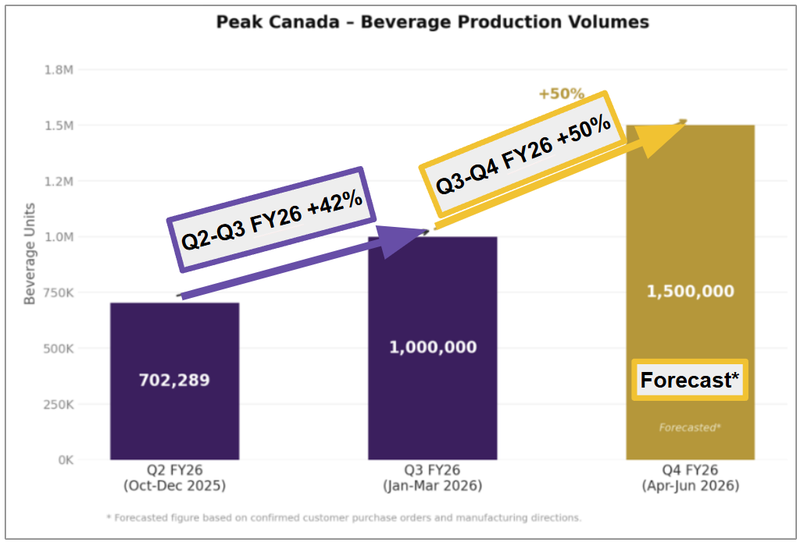

Another thing we noticed is that last quarter's production has been revised up from 900k to 1M units, with an additional 100k units forecast for the current quarter.

So it is good to see that the future appears to be continually growing:

(17th march operation update, mid quarter)

(source)

Today:

(source)

Quick recap on the operational momentum

Here is a quick overview on all of the growth PKP has announced over the past few months:

- Q3 FY26 produced ~1M beverage units (exceeding prior guidance of ~900K)

- 99.95% On-Time In-Full (OTIF) delivery sustained across the quarter - vs ~54% back in mid-2025

- Q4 FY26 production forecast upgraded to ~1.5M units (+50% QoQ) based on confirmed customer purchase orders

- Customer wins backing the ramp:

- Electric Brands extension (Sweet Justice ~1.4M units annually)

- St. Peter’s Beverages 250% expansion (Cookies and Green Monké portfolios)

- 30 new OCS listings (Ontario Cannabis Store)

- New brand launches with Reggae Royalty and Juana Sip

Key terms of the raise

- Total raise: A$2.4M (before costs) via an unsecured convertible note.

- Conversion price: A$0.015 per share

- Maturity: 12 months from issue (cash redemption if not converted)

- Establishment fee: 3% of face value, payable in shares (4.8M shares at the conversion price)

- Lead Manager: Powerhouse Ventures - through Powerhouse Advisory Australia. PVL’s Funds Management division was a cornerstone investor on the same terms.

(nice to see the lead manager also getting its own fund invested on the same terms).

What we want to see next from PKP:

There are three major catalysts we're watching over the next 6–12 months:

Continued production ramp toward 12M unit Canada capacity

Each quarterly update will show whether the ~47% utilisation is improving further. Ideally, throughout the quarter we will see PKP sign more partnerships in Canada.

Here are the milestones we are tracking:

- 🔄 Q4 FY26 production: ~1,500,000 units (confirmed purchase orders in hand)

- 🔲 Continue filling Canada capacity toward ~75%+ utilisation

- 🔲 Additional new brand partnerships announced

- 🔲 Further OCS listing acceleration in next call

US operations update

This is the one we are most looking forward to.

Here are the milestones we are tracking:

- ✅ Florida facility opened

- ✅ Envision Emulsions lab commissioned at Florida facility

- ✅ First US sales: 680,000+ cans in H1 FY26

- ✅ Funky Buddha deal signed

- 🔲 More manufacturing deals signed.

US regulatory resolution

There is a November 2026 deadline for federal hemp law resolution.

We think that, depending on what regulation is put in place it could be transformative for PKP’s US business.

See more on this risk in our last PKP note here: PKP: Business turnaround is kicking in? 1.4M units produced this quarter, up 56%.