MNB Green Ammonia Progress

Today, our fertiliser Investment, Minbos Resources Limited (ASX:MNB) announced that it has signed a non-binding collaboration agreement with Talus Renewables Inc., a major player in modular and zero-carbon green ammonia technology.

This is what the modular set up looks like in Kenya:

We see this as a good move for MNB, with significant cost reductions on the previous Stamicarbon system which had been proposed.

MNB has access to ultra cheap green hydro power already at a cost of USD1.1c/kWhr already, so this collaboration agreement is the natural extension of that - which should help MNB move quicker on the green ammonia project as we await first production from the phosphate fertiliser project in Angola.

To get that producing we estimate that MNB need an additional ~$10M.

The remaining ~$10M could come from different Angolan government initiatives - especially considering the amount of emphasis being put on the domestic Agricultural industry.

Our latest MNB note covers what we are looking for next at the phosphate fertilser project:

$61M capped MNB Secures Funds to Build $70M EBITDA per year phosphate mine within 12 months?

How does today’s MNB announcement impact our Investment Memo?

Why did we invest in MNB?

Capanda green ammonia project

MNB is exploring green hydrogen / green ammonia production potential in Angola. It is leveraging its support from the Angolan government to ensure access to the country’s local hydro-electric power at what may be the world’s cheapest energy rates.

We see this as positive news for one of the key reasons we Invested in, and continue to hold MNB.

What do we expect MNB to deliver?

Objective #3: Green Ammonia Project progress

- Sign technical, offtake, and investment partners for the development of the proposed Green Hydrogen/Ammonia Project.

Today’s announcement we see as a precursor to a binding agreement, firming up today’s collaboration agreement.

Click here to read our MNB Investment Memo in full

What’s next for MNB?

We’re primarily focussed on MNB’s phosphate fertiliser project at the moment.

🔄 Funding for the remainder of CAPEX on the project

We estimate that MNB requires a further $10M to fund the CAPEX of the fertiliser project.

In October last year, MNB secured an indicative term sheet on a loan facility of US$14M from the Industrial Development Corporation (IDC).

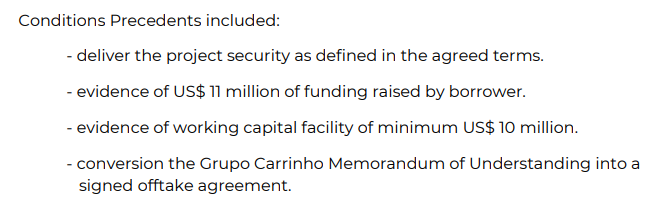

That has now been approved, contingent on the following pre-conditions being met:

(Source)

(pre-conditions are standard in these type of deals)

The facility allows MNB to draw down on cash when they need it. The interest rate on the loan is the Secured Overnight Financing Rate + 6.77% payable quarterly in arrears.

The IDC is a South African development finance institution established in 1940 to promote economic growth and industrial development. MNB’s engagement with this corporation provides other commercial opportunities for offtake of Stage 2 production for South African customers.

With this loan facility in place, it means that MNB will still need to find the remaining $10M to fund the rest of the project construction.

At the end of the December Quarter, MNB had ~$4.6M in the bank.

🔄 First production from phosphate fertiliser project

MNB is targeting first production in Q2 2025 in order to ensure the major phosphate customer has the majority of its fertiliser requirements for the 2025/26 growing season.

🔄 Converting offtake MOU into a binding offtake agreement

We want to see MNB convert its offtake MOU with Grupo Carrinho (Angola’s largest agro-industrial group) into a binding offtake agreement.

Offtakes are almost always looked upon favourably by debt financiers and so MNB will likely need to lock this in before it gets the remaining funding for its project locked in.

We also note that the US$14M debt deal announced today is contingent on the offtake MOU being converted into a binding deal.