JBY - Nevada gold peer gets taken over for ~A$170M.

A major gold producer buying out a junior in the Nevada gold sector…

This morning $36BN AngloGold Ashanti announced the ~A$170M acquisition Augusta Gold Corp - consolidating ground around its existing projects in Nevada’s Beatty district

We think the news will bring more of the juniors operating in Nevada onto the radar of corporates and the broader market.

Which is good for our Investment James Bay Minerals (ASX: JBY).

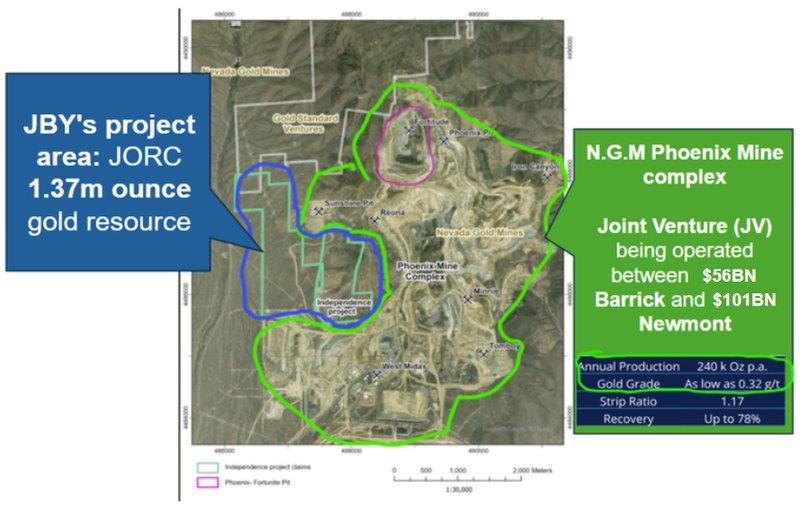

JBY’s project is also in Nevada and it sits right in and amongst ground held by majors Newmont and Barrick’s NGM Joint Venture (Nevada Gold Mines).

JBY’s project has an existing 1.37m ounce gold JORC resource estimate split:

- Shallow oxide resource - ~384k ounces of gold at 0.32-0.4g/t gold. This is the type of ore that can be mined using similar methods from N.G.M’s Phoenix operation. Its also a style of mineralisation that is common in mines all across Nevada where these sorts of grades are still feasible to mine.

- Deeper skarn resource - 984k ounces of gold at 6.64g/t.

Here is a GIF of us standing on top of JBY’s project, looking into N.G.M’s (Barricks and Newmont) Phoenix mine:

We were recently on site at JBY’s project - see our site visit note here: JBY is surrounded by the one of the world’s biggest gold mines - here’s what we saw on site

What the Augusta deal means for JBY -

For some context, Augusta’s two main assets have a combined resource of ~1.7m ounces of gold, and Anglo was happy to pay ~A$170M for the company.

Augusta's assets are not directly comparable to JBY’s because a portion of JBY’s resource is deep, whereas Augusta’s resources are more similar to the shallower part of JBY’s project.

For us, the bigger takeaway here is that the majors in Nevada have an eye on the juniors in the region and, if a deal makes sense, are willing to deal on their assets…

A big part of our JBY Big Bet is related to the potential for M&A of its assets, as follows:

Our JBY Big Bet:

“JBY re-rates to a +$300M market cap by expanding its large US gold resource and moving into development studies and/or attracting a takeover bid at multiples of our Initial Entry Price”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including development risk, country risk and commodity price risk - just some of which we list in our JBY Investment Memo.

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

What’s next for JBY?

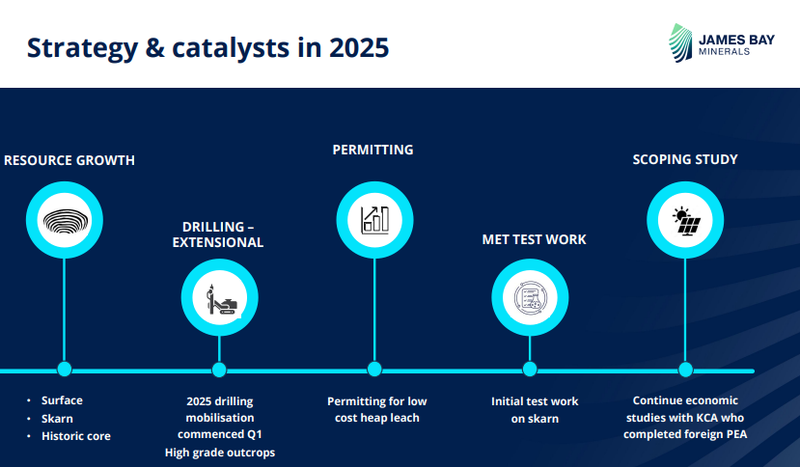

The following slide from JBY’s most recent investor presentation gave a good overview of what to expect next from JBY:

More drilling across JBY’s shallow resource 🔄

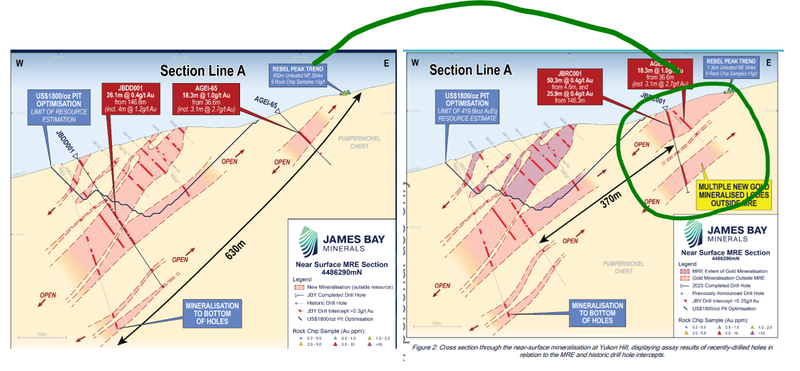

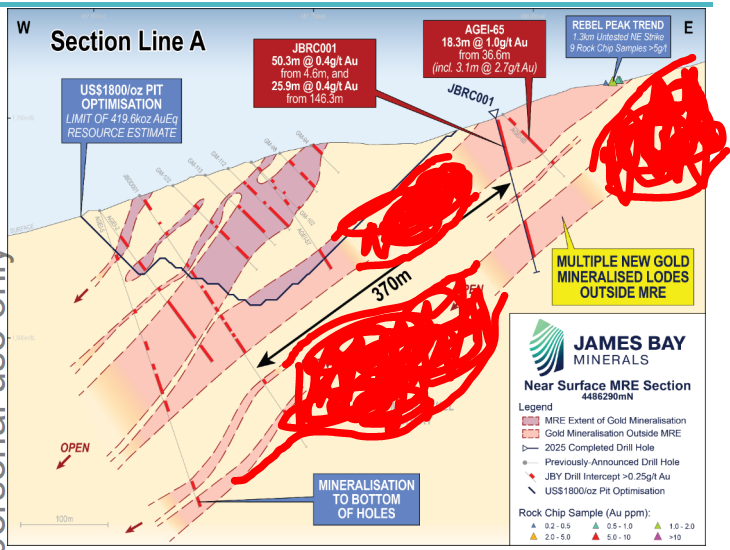

We have already seen JBY prove mineralisation outside of its current resource (FROM SURFACE) with its most recent set of assay results.

Here are the extension to the north (in red) - the image on the left is before the drill results, the image on the right is AFTER the drill results and the black outline is where the current resource sits:

With the next round of drilling we are hoping to see the following:

Ultimately, we are hoping that translates into a bigger shallow resource that JBY can add to its scoping study

Metwork testing on the deeper Skarn resource 🔄

JBY has also flagged it would look to do some metwork testing on it’s deeper skarn resource.

From that program we are hoping to see recoveries that somewhat resemble the ones from N.G.M’s Fortitude pit which has mined ~2.3M ounces of gold from similar geology.

If the metwork is similar, the look through for us will be that JBY’s resource might also be feasible to mine.

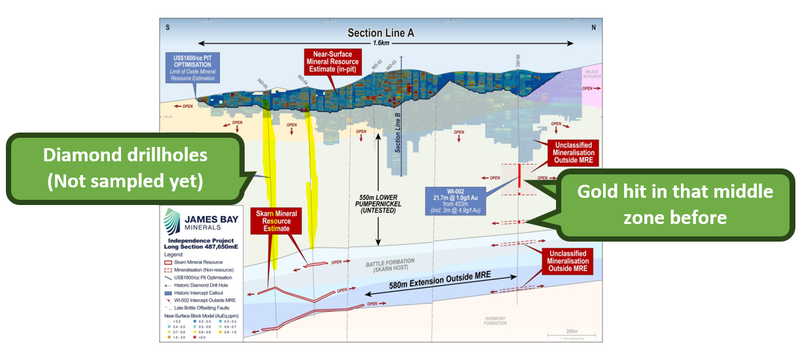

Re-assaying old cores 🔄

JBY has flagged potential assay results from old deep diamond drillcores that were never tested for gold.

These should give us some more information on whether or not there is gold in between JBY’s shallow and deep resources: