EIQ signs partnership for commercialisation in US healthcare market

Today, our AI heart disease detection Investment EchoIQ (ASX: EIQ) has announced significant Partnership and Integration Agreements with ScImage and MedAxiom.

EchoSolv AS (a software for the detection of a heart valve condition called aortic stenosis) will be initially deployed across 36 MedAxiom/ScImage-affiliated hospitals and cardiology practices.

ScImage has 1,200 hospitals in its network - so we think there is significant upside for EIQ to realise through this partnership.

MedAxiom is an American College of Cardiology company and the cardiovascular community’s premier source for organisational performance solutions - effectively we think the main “source of truth” for new cardiology products.

These types of major organisational buy-ins are rare for medtech companies like EIQ - so this is a key win for the company.

Here our three main reasons that this is a great step for EIQ:

- It further establishes another clear pathway to commercialisation in the USA, the largest healthcare market globally.

- It can further help demonstrate to clinicians the efficiency of EchoSolv AS through integration with ScImage's platform.

- The agreement can help act as a platform for Echo IQ's SaaS revenue model and potential for rapid growth.

EIQ - who are they working with?

Founder and CEO of ScImage, Inc., Dr Sai Raya PhD, referred to EIQ’s technology as “groundbreaking” in today’s announcement too.

That’s a ringing endorsement, and we agree - particularly considering EIQ’s Aortic Stenosis product has been shown to accurately identify 100% of severe aortic stenosis patients.

That’s the kind of proven accuracy that should form the basis of what is now EIQ’s primary focus - further commercialisation in the world’s largest healthcare market (the US).

How does this impact our EIQ Investment Memo?

Today’s news about a partnership with ScImage builds stronger bonds with an existing “soft launch” partner, which we highlighted as part of EIQ’s emerging high growth SaaS revenue model in our EIQ Investment Memo:

SaaS revenue model, potential to rapidly grow revenue and/or secure large licensing deals.

EIQ is a cloud based platform that will likely operate on a Software as a Service (SaaS) model when initially commercialised.

SaaS tech companies with demonstrated recurring revenue growth over time attract large valuation multiples.

EIQ’s tech platform is already built, meaning software development costs should be low, leading to higher margins on sales.

An ongoing “soft launch” has the product in the hands of an end user via a strategic partnership with a leading US medical Enterprise Cardiovascular Information Systems (CVIS) provider, Scimage, which has over 2000 sites in the US.

We expect this to provide an early opportunity for revenue growth under US reimbursement codes if EIQ secures FDA approval.

Source: 6 September 2024 EIQ Investment Memo

Note EIQ’s product has already achieved FDA clearance.

What’s next for EIQ?

🔄 Further strategic partnership updates - we want to see EIQ advance discussions in this area to help rapidly roll out the company’s tech, grow EIQ’s revenue and build market share.

🔄 Australia and NZ pilot program - this program is with a ”leading global structural heart innovation company” - this will advance EIQ’s licensing revenue pathway and be a “proof of concept” study that EIQ can take into the US. We haven’t talked about this sales strategy much today, but you can read about it here Is FDA approval imminent for EIQ? What happens after that?

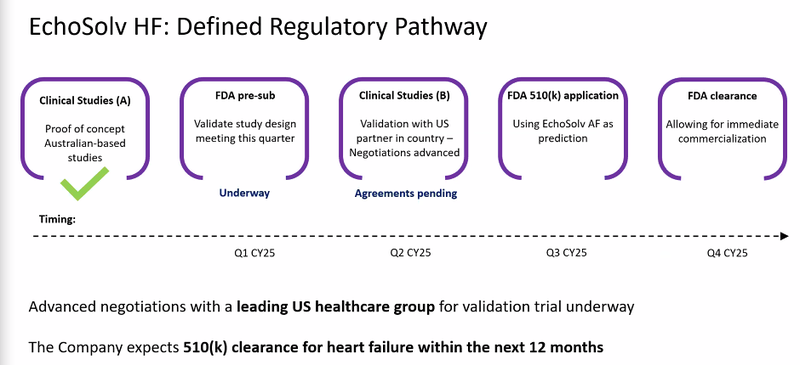

🔄 Heart Failure validation study with US based Group - the indication from EIQ’s most recent webinar is that the US based group is the prestigious Mayo Clinic, we think that the outcome of this study could be a big coup for EIQ.

🔲 Partnership with European re-seller to broaden market exposure - we want to see EIQ expand into new markets like Europe, in a previous webinar EIQ said the company was pursuing this opportunity.

🔲 CE Mark and TGA applications - this is so that EIQ can sell into Europe and Australia.