DXB raises $8.7M to progress Phase 3 clinical trial

Our Phase 3 biotech Investment, Dimerix (ASX:DXB) has completed a capital raise that will see it sufficiently funded through to important Phase 3 interim analysis results and beyond.

DXB raised ~$8.7M, $5.2M from the rights issue and $1.6 M of the initial tranche of $3.5M from the convertible note with $1.9M expected subject to shareholder approval.

We participated in the DXB rights issue.

We’re comfortable increasing our exposure to DXB at this critical stage in DXB’s trajectory.

The funds will be used to take DXB past just the interim analysis results and into manufacturing and partnering activities.

We think this added balance sheet strength will ultimately provide DXB with good leverage in any licensing/partnerships negotiations that may be underway or on the cards.

Across our Portfolio, we’ve often seen larger companies use balance sheet weakness opportunistically to get equity stakes in smaller companies or otherwise secure favourable terms.

So we see this DXB raise as a good strategic move as it alleviates any potential pressure on licensing/partnership negotiations.

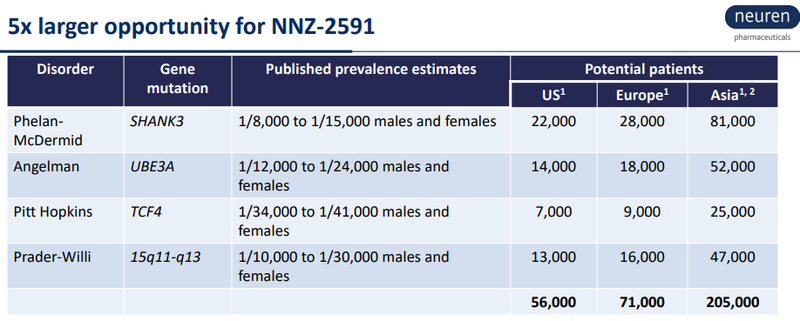

We take particular note of the experience of Neuren Pharmaceuticals, which also had an orphan drug designation and quickly became an ASX biotech darling after a long dormant period.

Indeed, we attended a recent Investor Presentation which paired Neuren and Dimerix which underlined some powerful parallels between the two companies.

Neuren spent a long period trading in the ~$1 range before positive Phase 3 results were announced, subsequently Neuren reached as high as $15 as the story built momentum.

For reference, Neuren was working off a smaller population for Rett Syndrome:

And Neuren’s upside is partly derived from the following numbers:

Neuren in its presentation quotes an average US Orphan Drug price of US~$187K per patient per year for 2017.

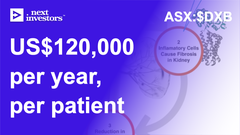

While it remains to be seen what kind of pricing DXB will be able to secure - recent pricing guidance released by a complementary treatment (sparsentan) placed the number at US$120,000 a year.

Subsequently, sparsentan failed to demonstrate in Phase 3 study that it improved kidney function for FSGS - the disease DXB is targeting.

With a well established safety profile, this leaves an even more pressing need for DXB’s treatment.

To read more about why we like orphan drug companies read: 🎓 Orphan Drugs Explained.

All up, we see this capital raise by DXB as a great foundation with which the company can build from.

Neuren was largely ignored by the market for a long time, until its commercialisation of an orphan drug established significant forward cash flows with successful Phase 3 results that the market couldn’t ignore Neuren any longer.

We’re Invested in DXB to ideally achieve a similar result - something which forms the basis of our DXB Big Bet:

“DXB re-rates 10x by successfully commercialising its drug through Phase-III clinical trials”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our DXB Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

What’s next for DXB?

We’re eager for the interim analysis from the Phase 3 trial, which is due in the first quarter of 2024.