CND completes 2D seismic reprocessing

Our oil and gas Investment Condor Energy (ASX: CND) just put out results from reprocessed 2D seismic data on its project, offshore in Peru.

Yesterday’s news follows almost ~24 months of reprocessing old seismic data which has seen CND define:

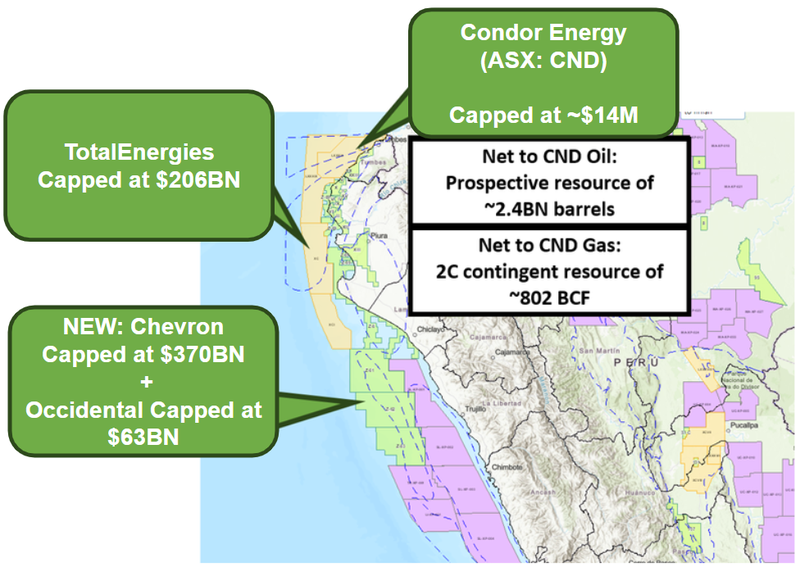

- Piedra Redonda gas project - 2C contingent resource net to CND of ~802Bcf of gas.

- Oil exploration targets - unrisked ~2.4BN barrel prospective resource net to CND across five targets (the single biggest being a ~800M barrel prospect).

CND’s project is located in a part of Peru that has already attracted TotalEnergies, Occidental Petroleum, and most recently Chevron.

AND CND recently said that a “Farmout process had commenced with multiple parties in the data room”.

CND was a first mover into the region, picking up its blocks before all of those majors and so we think there is a good chance they (at the very least) have been following CND’s work…

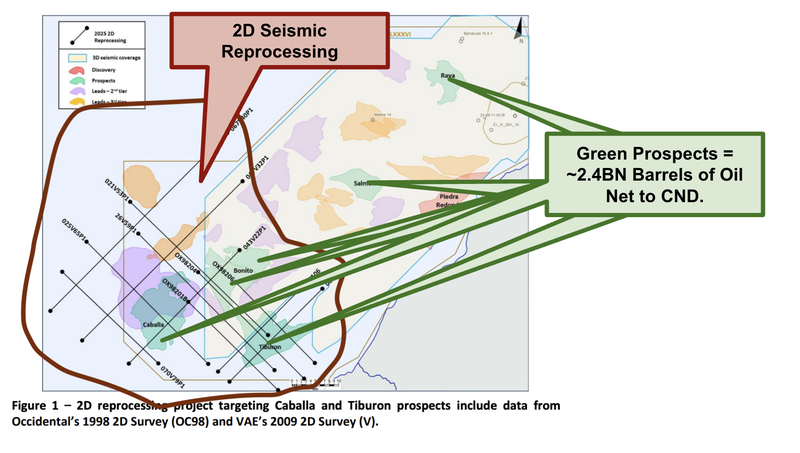

Yesterday, CND put out the results from reprocessed 2D seismic data in the far eastern portion of its project - where most of the prospects sit outside of CND’s current prospective/contingent resources.

Here are our key takeaways from yesterday’s announcement:

Cabala Prospect

The 2D reprocessing increases the clarity of the image which allows CND to define the structure a lot better.

You can see from the image below that the amplitude responses (yellow and red in the image below) are sharper in the reprocessed image.

Stronger amplitudes are often a good sign that the oil & gas explorer is looking in the right place:

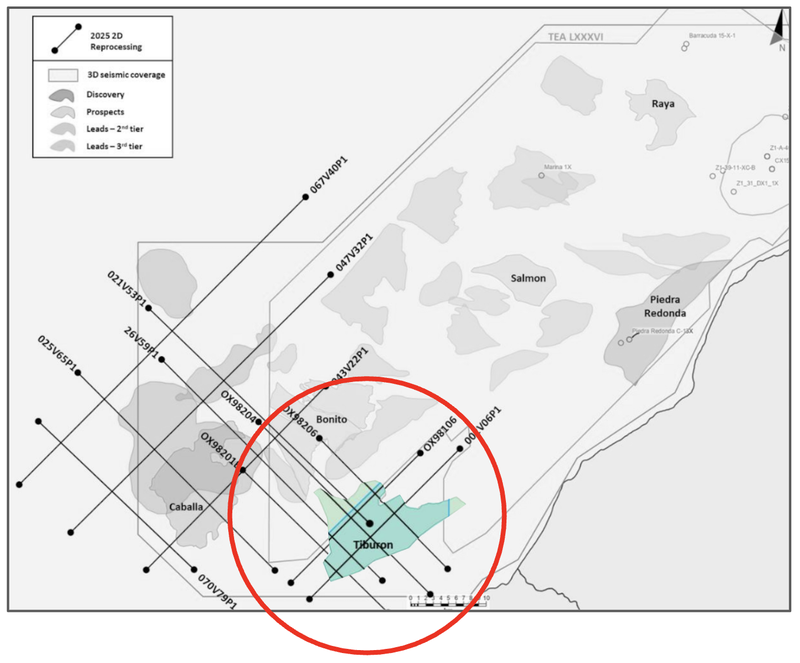

Tiburon prospect

The reprocessed seismic shows improved fault delineation and more coherent reflectors.

There is also possible gas accumulation in the top right corner of the image that wasn’t evident before:

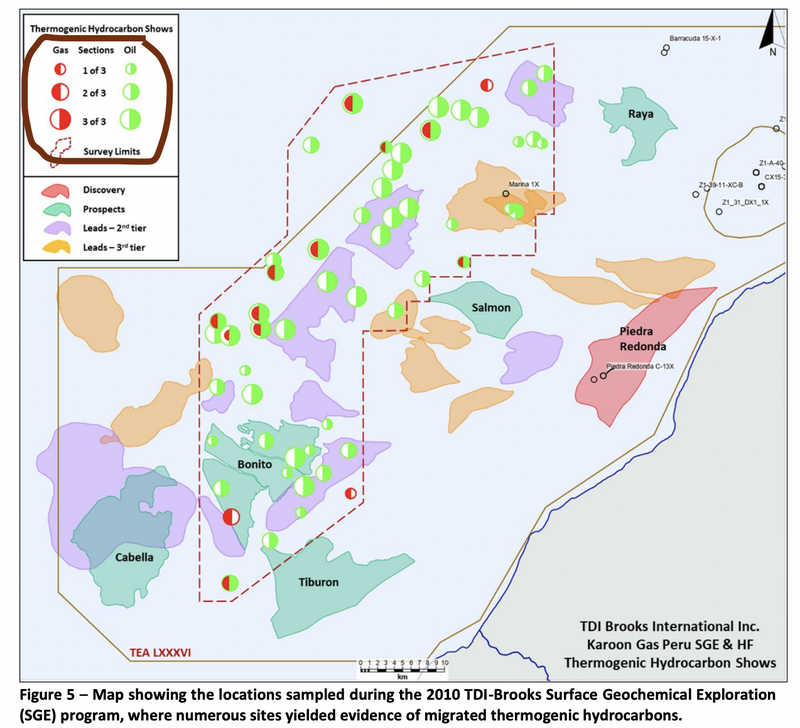

More information about where the oil & gas could be

CND also reviewed old geochemical data to define all the spots where it thinks oil and gas could be across its project.

The MAIN thing to point out here is how prospective a large part of CND’s block is for oil…

Yesterday’s news enhances data sets for potential partners

CND has explicitly said that it is running a farm-out process.

We think yesterday’s news puts CND in a far stronger position when it comes to engaging with potential farm-in partners.

CND will show all of this data to interested parties and give them a clear line of sight to additional exploration upside for the project.

We think a farmout deal will be a big catalyst for CND because it could provide the funding needed for what all early stage oil and gas projects want - a big exploration drill.

(In CND’s case, it could also be that its gas prospect gets developed, the company has both options over its block)

Farm out deals are typically share price catalysts.

A recent farm-out deal was what led to the rally of another ASX listed oil and gas explorer, Pancontinental which is exploring offshore in Namibia.

Pancontinental signed a deal with Woodside back in 2023 and rallied to a market cap of ~$230M.

CND is currently capped at ~$19M - which is why we think the farmout could trigger a rally in the company’s share price (assuming it is a good deal for CND).

CND is also going into farm-out discussions with both an existing gas discovery at Piedra Redonda AND big oil exploration prospects…

We think that will mean CND’s assets attract a much larger audience of potential partners.

Companies that are interested in high risk/high reward exploration AND companies that are looking for nearer term, lower risk development assets.

AND of course companies that are interested in oil and others that might be more interested in gas.

It’s hard to predict with so many different possibilities, but we think any of the following could be a big catalyst for CND’s share price:

- CND deals out its gas asset - maybe some of the proceeds that come from this can go toward drilling an oil exploration well? Maybe CND gets a free carried interest in an asset that could generate revenues in a reasonable timeframe? CND has options.

- CND deals out oil exploration assets - CND gets a free carried interest in a well that would be fully funded by a farm-in partner. This means less dilution going into a big drilling event for existing shareholders…

- Maybe a combination of the two? - CND could bring someone in that is interested in both…

We already know that Chevron, Occidental and Total are in the region… CND’s block could make for a good bolt on project for one of these guys OR a good entry asset for another major looking for exposure to the region.

With the current market cap hovering around ~$19M, it could be an interesting upcoming period for CND.