CAY to benefit from supply shortages? - mining equipment on site…

The bauxite market just got a bit of a fright with some recent news coming out of Guinea last week.

A potential opportunity for our Investment Canyon Resources (ASX: CAY) who is expecting to have its project in production in the coming months?

Guinea accounts for over 40% of global bauxite supply and China imports 70% of its bauxite from Guinea.

So to use a variation on the popular analogy - When Guinea sneezes on bauxite, the entire aluminium industry catches a cold.

Last year, Guinea’s exports jumped 25%, which flooded the market and caused a 20% to 35% retreat in bauxite prices.

(Bauxite is the source of most of the world's aluminium, it is the source rock that is refined/smelted down to produce the metal)

We saw the following reports suggesting Guinea “is considering introducing export quotas for mining companies as early as this month, according to four sources familiar with the matter”.

(source)

One of the main reasons for our Investment in CAY was because of the real possibility supply shocks from a major producer (like Guinea) open the doors for genuine tier 1 assets in different jurisdictions to be developed.

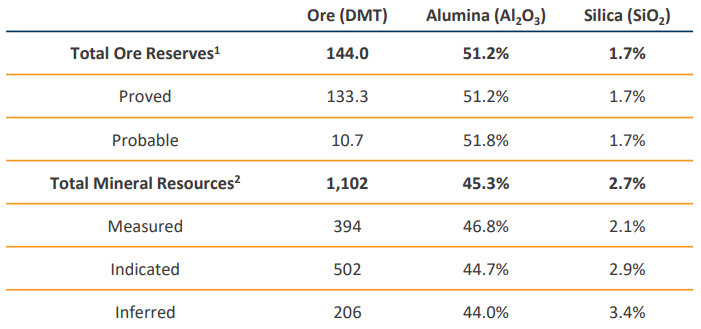

CAY’s project fits that exact bill - 1.102BN tonnes of Bauxite with plans to ramp up production across 4 main phases, starting at 1.2Mtpa in year 1, 2.1Mtpa in year 2, ramping up to 10Mtpa by 2031 (source)

Here is a look at CAY’s vast resource from the air and what the numbers of this resource equate to below:

(source)

And CAY already has:

- Surface miner on site,

- Discussions with Camrail continue looking to increase Cay’s ownership above the current 9.1%

- Offtake discussions with potential partners ongoing with the goal to secure agreements following the initial shipment of bauxite

- First locomotives delivery remain on track from the recent update with first arrival mid-late Q2, with shipments to commence in Q3

- FIRST PRODUCTION IN Q2 THIS YEAR.

Here is a quick overview of why we think the news out of Guinea could be a big positive for CAY:

- Centralised supply risk has become more real

Global refineries (especially in China, which takes 70% of Guinea’s ore) are desperate for supply diversification. So if Guinea imposes quotas, refineries will be scrambling for stable, high-quality alternatives and CAY’s Minim Martap Project in Cameroon fits the bill of a "Tier-1" alternative.

Recently CAY confirmed that it will look to sign offtakes around mid year, around the time that first shipment is to be made (perhaps even giving them a chance to use the premium ore first), so bauxite supply fears could add to demand for CAY’s premium production. (source) - Premium ore = Higher margins

Guinea’s move is a response to falling prices, however, CAY will be producing a higher grade, lower impurity bauxite product - so it could be a case of “two birds one stone” for potential buyers - supply diversification and higher grade product.

(CAY’s project has ~51.2% alumina grades, and low impurities (1.7% silica from “Proved Reserves”) versus ~2.5% for the typical projects operating in Guinea), pricing generally considers silica under 3% and carries penalties above.

This presents CAY’s product with a premium because of its high grade and low silica, so is expected to fetch around ~US$11/t premium over standard Guinean bauxite. (source) - Perfect timing: Production is months away

You’d rather be digging and shipping when a supply crunch hits, not just exploring and just last week CAY confirmed that its surface miner has been mobilised to site.

Mining operations are scheduled to commence this month, with first production targeted for early Q2 2026, ahead of first shipment in Q3 once the locomotives have arrived and been commissioned. (source)

Here is a picture of that surface miner on site:

(source)

On top of this, CAY is currently in discussions to increase its stake in the national rail company (Camrail) to 35%, securing its "mine-to-port" logistics chain.

Increasing its ownership percentage will give it a greater say on future upgrades and ensure that it is able to use the rail tracks as it requires for optimum shipping.

This news out of Guinea confirms the reality of a fragile global bauxite supply chain which may benefit other current and near term producers, such as CAY.

CAY is transitioning from a developer to a producer right as the market would like to see new supply come online from places other than Guinea.

So with mining starting this month and first shipments targeted for Q3 2026, the timing appears to be good with mining to begin imminently.

Downstream processing study

CAY also has a study looking at downstream processing options, to be able to process the bauxite to aluminium in country.

This is an extremely energy intensive process which is only more topical given the price of oil and energy has increased, especially for Europe, Asia and Africa.

Cameroon has a plentiful supply of hydroelectric power, which has become a popular choice for aluminium production. (source)

So the current macro environment could also help with a more positive result from this study and incentivise CAY to more aggressively pursue this option.

CAY has a feasibility study incoming for a value-add alumina refinery in country - with the study scheduled for Q3-2026. (source)

We think that this study has gotten a lot more interesting inside the last couple of weeks with the macro environment completely changing for a downstream alumina refinery, particularly the energy requirements.

The bauxite smelting required to create aluminium is an incredibly energy intensive process (temperature up to 1,100deg celsius, source), which has become a concern during the Iran conflict.

The price of energy has gone up significantly for oil and gas, so If this conflict and supply issues were to drag on for months, this may be positive for CAY as some refineries use coal and gas for heat.

CAY is looking into building a downstream business to process its bauxite in Cameroon which has vast quantities of hydroelectric power.

So the results of the study CAY is doing could come back positive in a world with high energy costs and reduced ore supply.

This could result in CAY getting the study out, just as the market is starting to show a heightened interest in something like this, aluminium refining with energy coming from stable sources and stable supply.

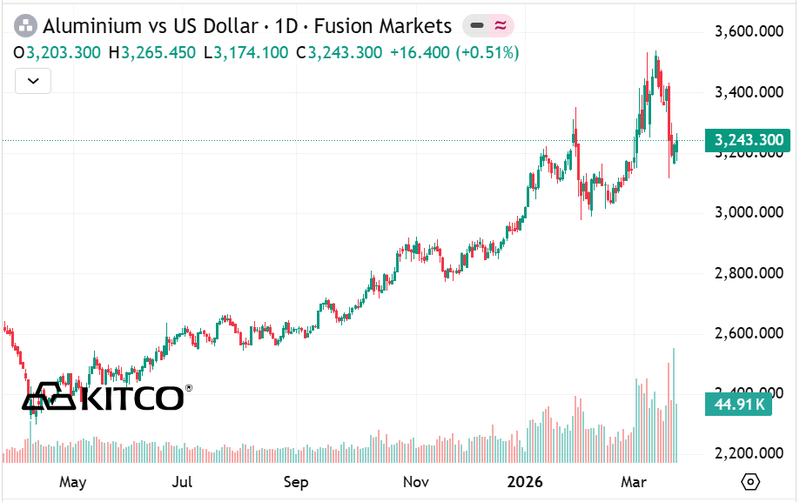

This is a 1 year chart for the price of aluminium, so while the bauxite price has come off quite a bit, aluminium has held up much better which would be encouraging for a company looking into a downstream operation:

(source)

Recently we listened to a Money of Mine podcast which was with Alan Clark from CM Group, who is dubbed “Aluminium Alan”.

Here were some of our key takeaways from the following interview with a bauxite/aluminium expert and how we think it relates to CAY:

- Guinea concentration risk is THE structural story in bauxite - Guinea supplies 70-75% of China's bauxite imports. The 2024 disruption at GAC sent alumina and bauxite prices to all-time records. Alan called it the industry's "no shit moment." (basically confirmation that the industry is now very aware of a requirement to bring new supply online)

- Downstream refining is credible at CAY's scale - Guinea miners are being forced by government to build refineries - Cameroon could lead by choice. Energy is the key question (Alan flagged this for Guinea too) - Cameroon's hydro capacity could be an advantage.

- The market is temporarily weak but structurally solid - Alan talked about how ~40% of global alumina refining capacity is currently operating at a loss. Bauxite prices are at or near the cost curve. It's a buyer's market right now - but the Guinea supply risk hasn't gone away, it's just been underpriced again.

A key quote during the podcast for us was this:

"The demand for aluminium… It's just always going up and you know the world needs… at least one new smelter prime aluminium every year..." (09:45)

So there appears to be a long term market that CAY could become a part of in both the bauxite supply and refining/smelting in the not so distant future if the economics from this study stack up.

It's a great watch for anyone who wants a deep dive into the bauxite markets:

Why Aluminium Just Went Vertical - Money of Mine

What’s next for CAY?

The key catalysts we will be looking out for over the coming months are:

- 🔲 An offtake deal that locks in a sale price for CAY’s product (keeping in mind that CAY’s bauxite is a premium product expected to fetch US$11 higher than market bauxite prices)

- ✅ Mining fleet mobilising to site - 2 weeks ago - with surface miner commissioning expected this Month.

- 🔲 Locomotives arriving in country (expected to arrive from mid-late Q2 and into Q3), with first shipment expected in Q3

- 🔄 Road/rail infrastructure completion (expected to be ready during Q2 for ore haulage to the rail facility).

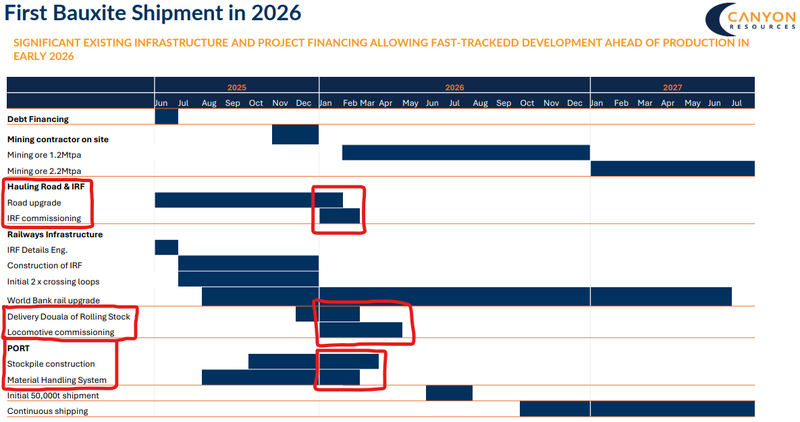

We want to see CAY execute its development plan as they have outlined below, noting that today’s update has some of these timelines sliding relating to train commissioning and first shipment:

(source)