CAY On Track to Ship First Bauxite in Early 2026

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 2,307,692 CAY shares at the time of publishing this article. The Company has been engaged by CAY to share our commentary on the progress of our Investment in CAY over time. This information is general in nature and does not constitute personal advice. It does not consider your objectives, financial situation, or needs.

Our 2025 Wise-Owl Pick of the Year Canyon Resources (ASX:CAY) is on track to build their mine and ship its first delivery of bauxite early next year.

“Production” is what every small cap mining junior sets out to achieve, but very few make it.

(it takes roughly 17 years for a company to go from exploration through to production according to S&P Global)

CAY owns one of the world’s biggest undeveloped bauxite deposits.

CAY’s project has an estimated 1 billion tonne JORC resource with an ore reserve of 109Mt in Cameroon, Africa.

(and it could get even bigger with the company scheduled to announce a JORC resource upgrade in a few weeks time)

Bauxite is the rock that is essential for the production of aluminum and is considered a “bulk commodity”.

The majority of CAY’s resource is considered “free-dig” material (the resource starts from the surface and is down to ~15m of depth)...

Meaning it is not very difficult to get the bauxite out of the ground.

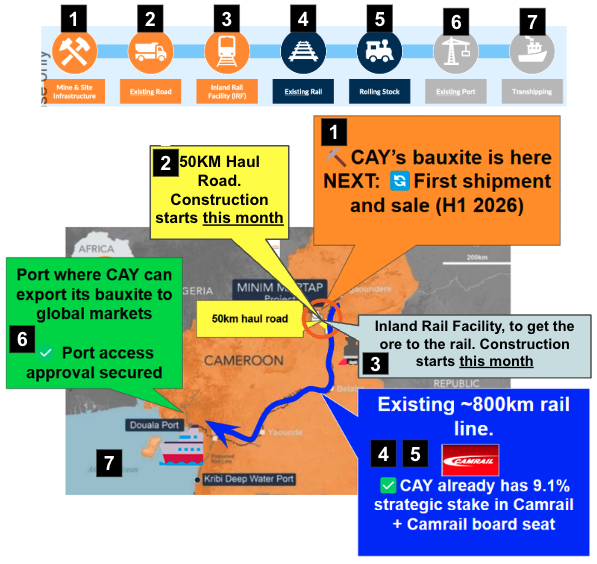

Like all bulk commodity mining projects, a big part of determining profitability is transport and logistics... i.e. getting the bauxite to the market.

In the last few weeks CAY started ordering long lead items for its project AND has:

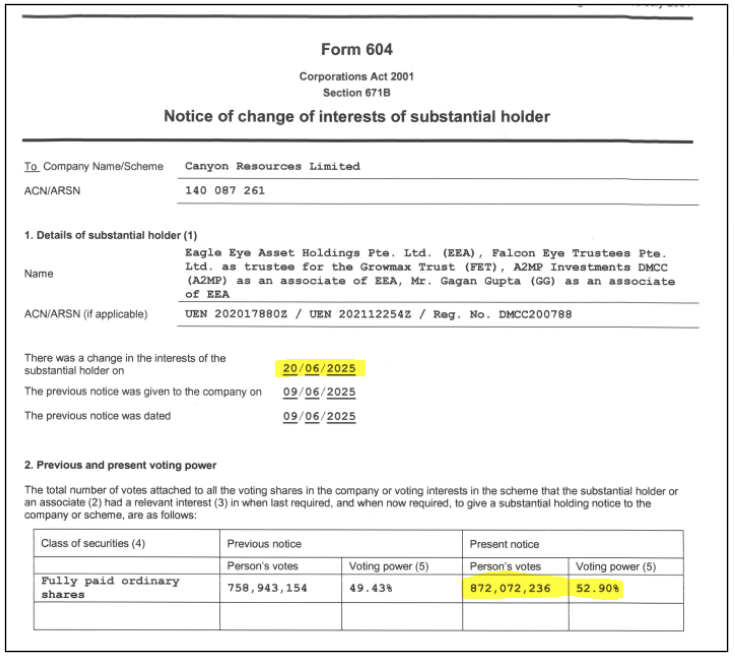

- Secured A$15.8M from the exercise of options from major shareholder Eagle Eye Asset Management (with a further A$8.7M to come) - Eagle Eye now own 52.9% of CAY (Source)

- Secured a US$140M credit facility from AFG Bank Cameroon (one of Cameroon’s top financial institutions). (Source)

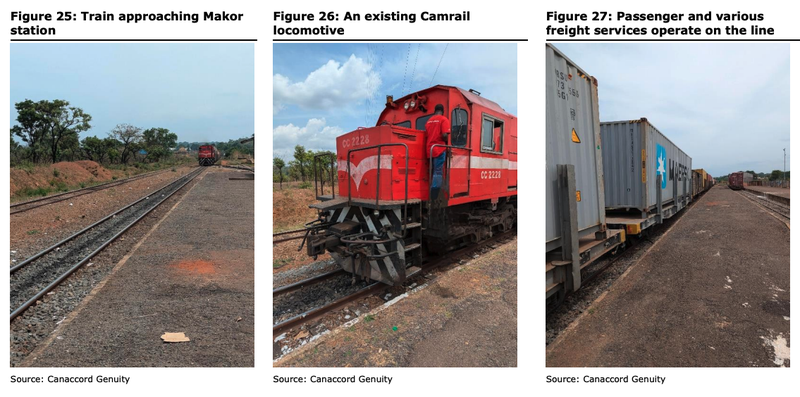

- Ordered locomotives (train carriages) - first deliveries due Q1 2026 (trains are expensive... ordering trains is a pretty strong sign that things are progressing well). (Source)

- Appointed a contractor to start construction on the Inland Rail Facility this month. (Source)

- Appointed a contractor to start road construction this month. (Source)

- Mining contractor and Ore Haulage contractor ready to mobilise by end of the year. (Source)

Today CAY announced that Peter Secker has officially commenced his position as CAY’s new CEO to oversee the construction of the mine and first bauxite production:

(Source)

Peter has been acting as a strategic advisor to CAY for the last few months and has now officially started as CEO as part of a planned succession plan.

(Big thanks to previous CEO JS for his great work in turning CAY around after a rough patch back in 2022 - JS is now moving to Chief Commercial and Corporate Development Officer)

CAY’s new CEO Peter Secker is a mining veteran with a track record of building and operating mines.

He was the CEO of Bacanora Lithium from 2015 to 2023 - during that time China’s largest lithium producer Ganfeng acquired the company for ~£260M.

We believe everything appears to be falling into place for CAY’s construction plan and first ore to be shipped by 2026.

We dug back into CAY’s Bankable Feasibility Study that the company completed in 2022.

It is remarkable to see just how ‘on track’ CAY is based on its development timeline.

(anyone who has ever renovated a house OR followed a small cap stock trying to construct a mine would know meeting projected timelines almost never happens...)

(Source - Page 10, BFS 2022)

This is how we see CAY’s project working:

There are a few more short term catalysts for CAY in the next few months while the company starts construction including:

- JORC resource upgrade (CAY’s JORC resource is made up of just 17 of 62 bauxite targets on the project area)

- Updated Definitive Feasibility Study (DFS) to reflect new outlook for bauxite and JORC resource upgrade (and any cost updates from 2022).

We will be watching closely to see how CAY’s construction is progressing, and any updates on the project economics that are in CAY’s favour.

Our CAY Big Bet:

“CAY takes its bauxite project into production is re-rated to a market cap greater than $1BN”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including development risk, country risk and commodity price risk - just some of which we list in our CAY Investment Memo. Success will require a significant amount of luck. Past performance is not an indicator of future performance.

Major Shareholder Eagle Eye is moving CAY closer to production

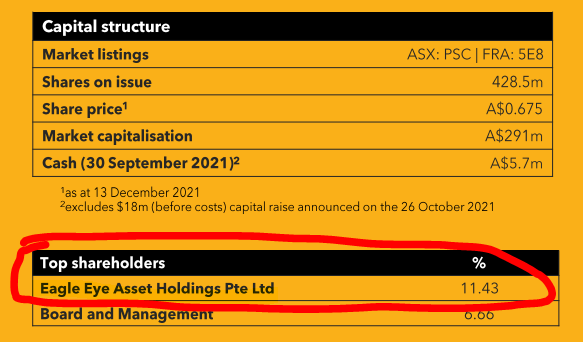

One of the key reasons we named CAY as our 2025 Wise-Owl Pick of the Year was because of its major shareholder Eagle Eye Asset Management.

Eagle Eye first invested in CAY back in December 2022 at 6 cents per share (source).

Since then, Eagle Eye has been buying on and off-market very aggressively, moving up to ~52.9% ownership of CAY.

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Over the last ~30 days Eagle Eye exercised $15.8M in 7 cent options ($8M on the 18th of June and $8M on the 5th of June).

AND CAY expects them to exercise another $8M of options soon. (Source)

Eagle Eye’s ownership of CAY now stands at ~52.9% of CAY.

(Source - Change in Substantial Holder Notice)

We are backing Eagle Eye’s expertise to repeat the type of success they have had on other projects in Africa.

One recent example on the ASX is the sale by Prospect Resources.

Eagle Eye became major shareholders in Prospect October 2020.

The company then led the development and funding of its Zimbabwean based lithium asset through to an eventual sale in July 2022...

For US$343M (~A$530M).

The company went on to return most of that money to shareholders in a dividend, at ~8x share price return from when Eagle Eye originally entered the picture:

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. These products, like all other financial products, are subject to market forces and unpredictable events that may adversely affect future performance. Eagle Eye’s past successes may not be repeated.

Eagle Eye were the single biggest shareholders in Prospect before that deal was done:

(Source)

A nice win for shareholders given Prospect’s share price was less than 20 cents only 12 months before the sale and the eventual ~96c cash return.

Eagle Eye has already demonstrated with CAY its ability to get things moving within Cameroon, playing a key role in securing the mining licence for the project.

Eagle Eye has continued to show support as a major shareholder, and appears to be willing this project through to production.

We are backing Eagle Eye expertise to get the most out of CAY’s assets (either through an eventual sale, or through to production and eventual dividends...).

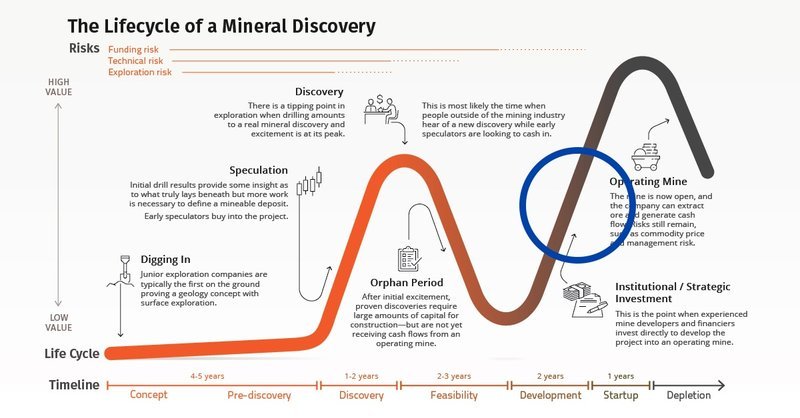

CAY moving into the “production” phase of the mining lifecycle

It takes on average 17 years for a mine to move from exploration to production, and many, many mines don’t make it that far. (Source)

FID or Final Investment Decision, is the last hurdle before a mine moves from the development stage to the construction stage...

And then eventually production.

After all of the exploration work, millions of dollars spent on drilling, time to lobby the government into securing permits and everything in between, the production phase is where the mines ACTUALLY return money to shareholders.

(As long as the price for the commodity is strong and the mine operates efficiently).

Thousands of assets go through the exploration stage, but only a handful make it to production.

And in the first half of 2026, our 2025 Wise-Owl Pick of the Year CAY might just get there.

This is the exact point on the Lassonde curve that things start to ramp up, and there is more institutional interest in the project:

(Source)

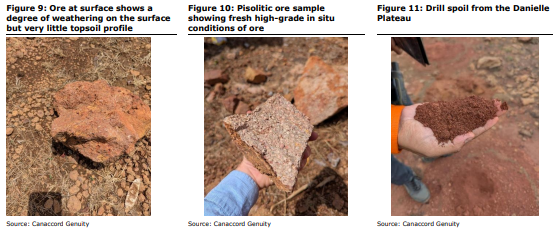

Update from an Analyst who went to site

Recently a team of analysts from Canaccord Genuity, led by the affable Timothy Hoff, visited CAY’s project:

(Source)

There’s plenty of other photos of CAY’s site plus surrounding infrastructure in the link above.

Generally, these bigger site visits happen when the company is preparing for the next phase of development.

In the analyst report, Hoff speaks about the remaining funding for the project. Here are what we think are the key lines from his report:

- “We believe the funds currently available will allow the company to set up operations to ultimately achieve the 6.4Mtpa BFS run rate”

- “We believe [the release of the DFS in the September Quarter] may allow the company to attract further partnerships by way of further funding investments and/or offtake agreements.”

- “Once in production, we believe that any progressive expansion of the operation can be funded through generated cash flow.”

Of course, like all of us, analysts can't predict the future with certainty, and those points made above are no guarantee to eventuate.

In any case it’s now full steam ahead for CAY as the company moves forward with the plans to make the first shipment of bauxite ore early next year.

What’s next for CAY?

CAY’s team has delivered their progress on schedule so far. Here are the upcoming catalysts that we want to see now:

🔲 Publish an upgraded JORC mineral resource estimate.

CAY already has the 8th largest bauxite resource in the world. CAY expects to upgrade its mineral resource estimate by the end of this month. CAY will likely also release drilling results as well.

🔲 Finalise offtake discussions

🔲 Finalise DFS

The bauxite price has significantly increased since the company completed its DFS in 2022. We are hoping to see some new project economics with an updated bauxite price and upgraded JORC resource.

🔲 Construction begins

🔲 First shipment of bauxite

CAY expects first shipment of bauxite by early 2026.

What are the risks?

Investing in pre-operational mining companies is inherently speculative and carries significant risks.

Being a later stage mining project, CAY is most exposed to fluctuations in the bauxite price.

Late last year and early into 2025, bauxite prices rallied to above US$100 per tonne. More recently, prices have come off back into the ~US$70 to US$80 per tonne range.

While the prices are still almost double where they were when CAY did its last study in 2022, if the bauxite prices continue to fall then it could hurt CAY’s share price.

Commodity price risk

CAY’s project is at the BFS stage, meaning it is highly sensitive to changes in underlying commodity prices. If the bauxite price were to fall it would hurt overall project economics and make it harder for CAY to lock in project financing for the development of the project.

Source: What could go wrong? - 20 January 2025 CAY Investment Memo

There is also sovereign risk associated with operating in Cameroon, where legal enforcement and regulatory conditions may differ materially from Australia.

Cameroon has an election expected to occur around October 2025.

As CAY’s project needs the support of the country, changes to its political make-up may alter its progress to production.

Geopolitical risk

While we believe Cameroon’s current political climate is stable, there have been four coups in the last 4 years in the West Africa region. CAY’s project is subject to the volatility of doing business in this part of the world. Geopolitical risks form a significant part of CAY’s overall risk profile.

Source: What could go wrong? - 20 January 2025 CAY Investment Memo

Now that the company is in the construction phase, execution risk and delay risk may manifest for the company.

The project is located in a remote part of Cameroon, and unforeseen issues may emerge in the project construction.

In addition to commodity price, geopolitical, and execution risks, investors should be aware of regulatory, funding, and permitting uncertainties; foreign exchange volatility; and the possibility of operational, environmental, or community-related disruptions.

Delays in securing offtake agreements, infrastructure development, or achieving production milestones may adversely affect project viability.

We list more risks to our CAY Investment Thesis in our Investment Memo here.

Our CAY Investment Memo

You can read our CAY Investment Memo in the link below. We use this memo to track the progress of all our Investments over time.

Our CAY Investment Memo covers:

- What does CAY do?

- The macro theme for CAY

- Our CAY Big Bet

- What we want to see CAY achieve

- Why we are Invested in CAY

- The key risks to our Investment Thesis

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.