CAY signs binding agreement for US$140M in project financing

2025 Wise-Owl Pick of the Year Canyon Resources (ASX: CAY) just locked in US$140M of project financing for its bauxite project in Cameroon.

And CAY expects to be making its “first shipment of bauxite from Minim Martap in the 1H 2026”.

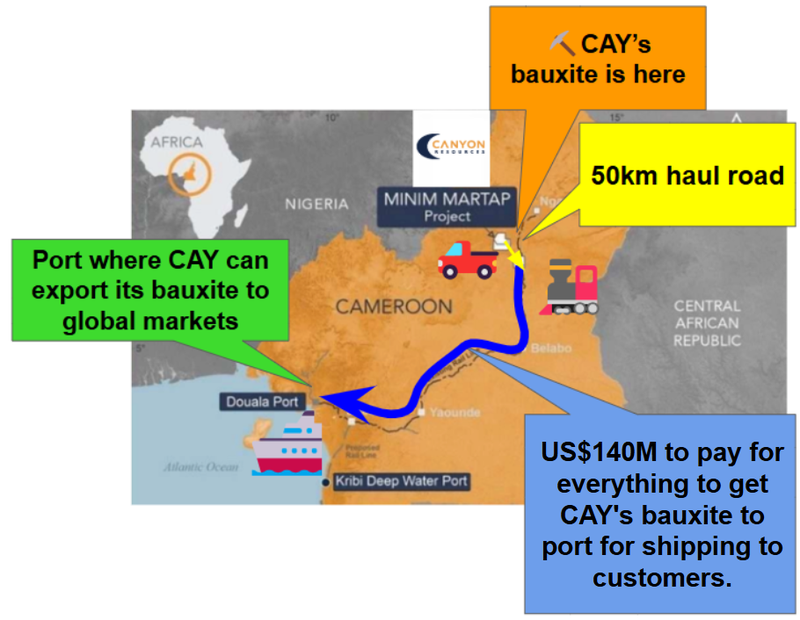

CAY owns one of the world’s biggest undeveloped bauxite deposits - one of the very few that are currently not owned by one of the mulit-billion dollar majors.

CAY’s project has a 1 billion tonne JORC resource with an ore reserve of 109Mt in Cameroon, Africa.

Enough bauxite to be mined for over 100 years…

To get its project into production, CAY’s project needs ~US$255M in CAPEX funding (source)

After today’s announcement CAY has secured US$140M in debt financing and should have >A$30M cash in the bank.

The debt financing deal is with AFG Bank Cameroon (a top three bank in Cameroon) and will primarily be used for:

- Purchasing the locomotives and wagons.

- Developing rail infrastructure

- Developing ore transport infrastructure

- Developing the port facility for shipping.

(Source)

CAY expects to be drawing down on the loan in Q3-2025.

Ahead of first production in H1-2026…

Why we think today’s news is important

The first reason is because CAY has officially signed on a debt financier for its project.

The big debt financing package is usually the hardest part of any project financing deal. They can take years and usually only come in right before construction kicks off.

CAY now has over 50% of its project financing locked in AND with a current market cap of $377M we think the company has a lot of optionality on how the rest of the CAPEX gets funded.

The second reason is because the funding is going toward logistical infrastructure.

Logistics is everything for a big bulk commodity project like CAY’s.

Bulk commodities projects are usually made or broken by the availability of infrastructure and how much work needs to go into getting the raw material to a port for export into global markets.

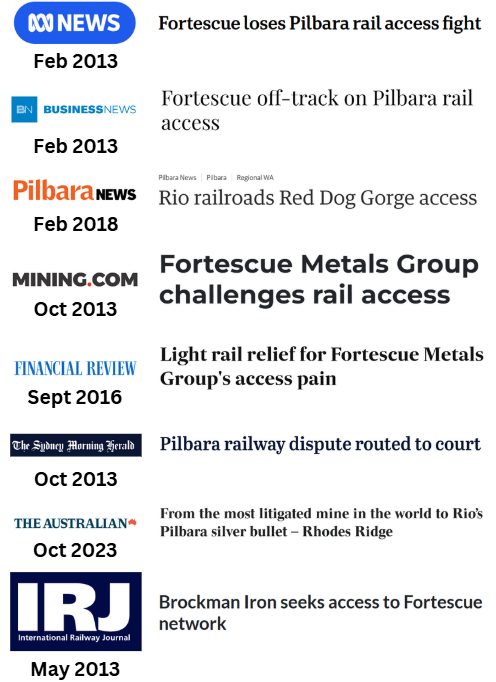

Many who followed the BHP, RIO and FMG “rail wars” in the 2010s know how important logistics can be.

Solving the logistics problem is what made Fortescue the $47BN iron ore behemoth it is today - at the time a lot of the market thought they could never get it done…

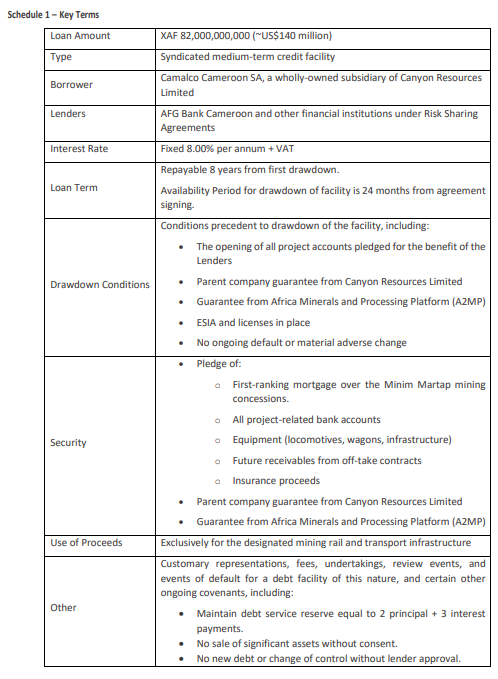

More on the debt financing:

Here are our quick fire takeaways from the financing deal:

- The loan is for US$140M at an 8% interest rate.

- CAY has 24 months to drawdown the loan and 8 years to repay it in full.

- The debt can only be used for mining, rail and transport infrastructure.

- The debt is also secured against all those purchases and subject to some pretty standard conditions.

The full document is below:

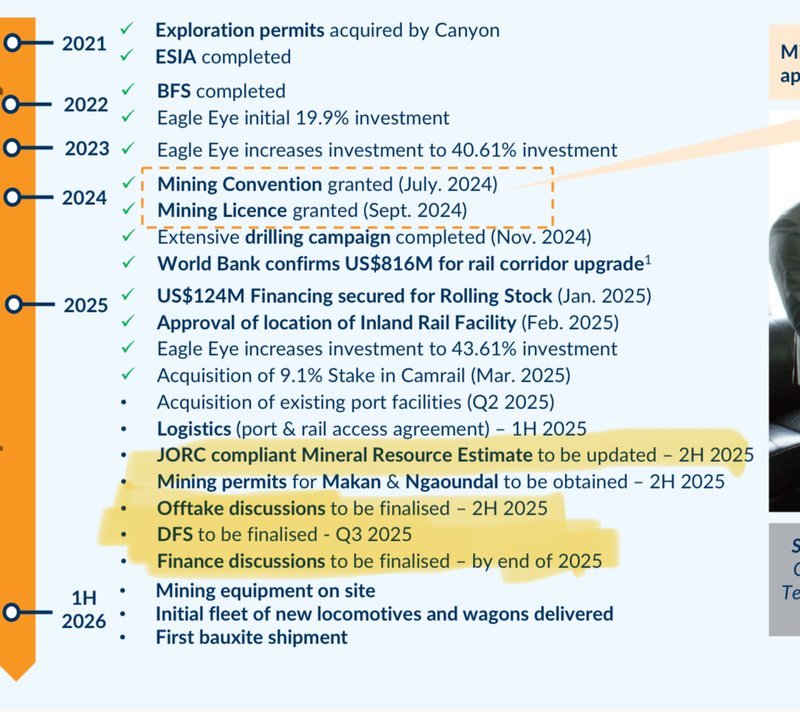

What’s next for CAY?

The slide below from CAY’s recent investor presentation gives a pretty good overview of what we can expect to see next:

(Source)

In the short term we are looking forward to an upgraded JORC resource, feasibility study results and some offtake news.

CAY’s updated Definitive Feasibility Study (DFS) is due in Q3 this year.

We think the study is an important catalyst because it will give the market a fresh perspective on the economics of CAY’s project.

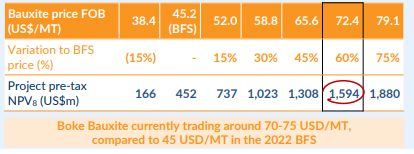

The previous study done in 2022 was done using a US$45.20/tonne bauxite price and returned a pre-tax Net Present Value (NPV) for the project of ~US$452M.

Bauxite prices are now above US$90/tonne…

A slide from CAY’s recent investor presentation gave us a pretty good idea of what to expect - with today’s spot prices more than quadrupling the project's NPV (to US$1.6BN) relative to the 2022 study:

(Source)

The NPV upgrade will ultimately dictate how the market values CAY.

Usually, as a project is getting closer to first production, its market cap will start to close the gap to its project’s NPV.

Before first production it’s not uncommon to see a stock trading at 40% to 80% of its project’s NPV.

For some context, just 40% of a US$1.6BN NPV would imply CAY should be capped at A$1BN+.

With first production now expected in H1-2026, that means we could see that convergence start to happen in the short-medium term.