CAY confirms 26.9% ownership of national rail company and 42.8% ownership of Port operator in Cameroon

Our bauxite Investment Canyon Resources (ASX: CAY) has just finalised some strategic moves on the logistics chains for its Minim Martap Bauxite Project in Cameroon.

CAY is developing the Minim Martap Bauxite Project which is one of the world's highest grade bulk bauxite deposits - the project has an 1.102BN tonnes JORC resource.

And an Ore Reserve of 144Mt at 51.2% alumina and just 1.7% silica - enough for ~20 years of mining (even at CAY’s phased ramp up to a 10mtpa production target).

Today’s CAY announcement provided the key logistics stakeholding Investments being finalised which is good to see come through.

These had been flagged as near term for a while now so these items can now be ticked off the list of items that further derisks the project.

Specifically these involved:

- Camrail stake increased from 9.1% to 26.9% - CAY's in-country subsidiary Camalco has paid ~A$23.8M (XAF 9.852BN) to increase its equity in Cameroon's national rail operator

- 42.8% strategic investment in Terminal Bois du Port de Douala (TBPD) - CAY now has a major equity stake in the operator of the Port of Douala (~A$0.8M / CFA 347.447M)

CAY has gone from a minority influence to major shareholder positions in both the rail operator AND the port operator that will be moving its bauxite product to market.

So this move effectively locks in a significant "controlling slice of the mine-to-port chain" and has come ahead of the first shipment.

What this means for CAY as a near term producer

A few reasons today's news is meaningful for CAY:

1. CAY now has a much bigger seat at the Camrail table.

Camrail is Cameroon's primary rail transportation company, i.e. the company that provides the infrastructure that will move CAY's bauxite from the Inland Rail Facility (IRF) to the Port of Douala.

Going from 9.1% to 26.9% means CAY:

- Has materially stronger oversight and influence on Camrail's operational decisions

- Is actively engaged on the PQ2 rail upgrade (the rail upgrade that supports CAY's volumes)

- Can secure timely bauxite transportation slots with the operator

- Significantly de-risks the mine-to-port logistics chain

For a bulk commodity producer in Africa, the rail logistics piece is a significant "outside of CAY's control" risk that with this move is significantly mitigated.

Today's news materially reduces that risk, basically because CAY is becoming a 26.9% owner of the rail network, it should be able to get what the business needs to operate in terms of rail logistics.

This is expected to complete during Q2 following in-country admin to ratify the change in shares in CAMRAIL to CAY.

2. CAY has a 42.8% stake in the operator of the Port of Douala.

This complements CAY's existing Port Access Agreement (which already gave CAY the right to export bauxite/alumina and import raw materials).

But equity ownership of the operator is a different level of control.

CAY now has a direct say in how the port is operated, evaluated and optimised which it can do so around its specific shipping requirements.

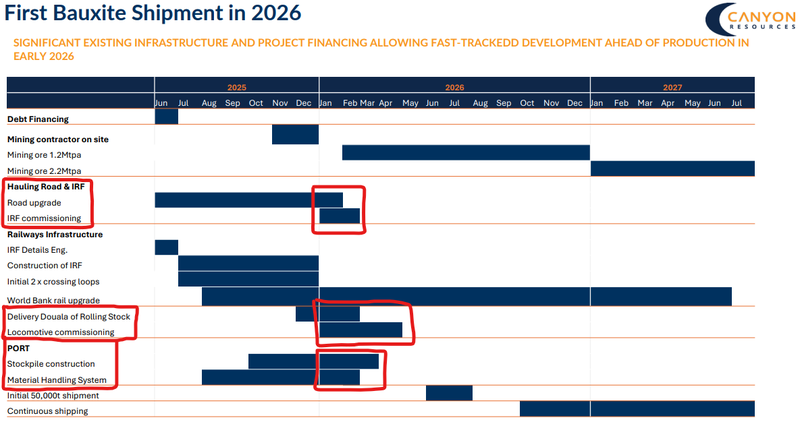

3. Both moves de-risk the Project ahead of imminent first shipment.

Today's update also confirmed that:

- The surface miner is on site at the Daniel Plateau

- Trial mining to start mid Q2 (so possibly days away) - this will begin to build stockpiles at the mine, then IRF (Inland Rail Facility) and then port ahead of first shipment

- Tracklaying at the IRF and bulk earthworks at the Port of Douala have commenced in preparation for rail operations

- First seven locomotives expected at Port of Douala in late Q2

- Rail wagons to follow in July

- First bauxite ore shipment scheduled for late September 2026

- Continued engagement with potential offtake partners (aiming to complete these after first shipment to show off its premium product)

- The Feasibility Study on an alumina refinery is on track for Q3 (more on this below)

CAY included a picture of the port where earthworks are now underway ahead of first shipment in Q3:

(source)

And also site works at the Inland rail facility:

(source)

So today's moves on Camrail and TBPD are timed to lock in the logistics chain control for the rail and port in time for CAY ahead of the start to move the bauxite product.

For those who want a refresher on where CAY is at

We covered in a QuickTake around 4 weeks ago the prior project update which was more focused on the production side of things, you can see that here.

Here are some key stats on the project:

- Ore Reserve: 144Mt at 51.2% aluminium oxide and 1.7% silica oxide, i.e. high grade, low key impurity

- JORC Mineral Resource: 1,102Mt at 45.3% aluminium oxide which provides multi-decade mine life potential

- Production target: 10Mtpa phased ramp-up

- First production imminent (mining to begin this quarter), first shipment expected late Q3

- Feasibility Study for value-adding alumina refinery scheduled for Q3

That last point in particular we are pretty keen to see the results of, especially with the current bauxite/aluminium macro, CAY reaffirmed this is on track for Q3..

The main source of bauxite (the source rock used to create aluminium) comes from Guinea, which partly due to massive increases in exports has seen the bauxite price retreat.

As a result there have been reports of Guinea considering quotas on exports to protect profit margins and country tax/revenues.

On top of this, Aluminium production from the bauxite is incredibly energy intensive and Cameroon has vast quantities of hydroelectricity.

So we see a big potential opportunity for CAY to be able to leverage this and to become a producer of aluminium itself.

CAY’s resource has low impurities, being particularly low in silica so is already expected to fetch US$11/tonne extra for it compared to the Guinea Price Index. (source)

So this would likely make the self refining less complex and increase potential margins as it would be able to get more aluminium produced for less input, with a lower input energy cost and stable energy supply.

We covered this in a macro themed quicktake a few weeks ago now here: CAY to benefit from supply shortages? - mining equipment on site…

What’s next for CAY?

The key catalysts we will be looking out for over the coming months are:

- 🔲 An offtake deal that locks in a sale price for CAY’s product (keeping in mind that CAY’s bauxite is a premium product expected to fetch US$11 higher than market bauxite prices)

- 🔄 Trial mining to commence mid this quarter (the surface miners already on site and commissioned). Commencement expected mid this quarter

- 🔲 Locomotives arriving in country (first 7 shipped from China in late March, expected to arrive from mid-late Q2 and into Q3) The first 7 locomotives are expected late Q2 and wagons to follow in Q3

- 🔄 Road/rail infrastructure completion (expected to be ready during Q2 for ore haulage to the rail facility). Tracklaying has commenced and earthworks at the port have begun.

- 🔲 Alumina refinery Feasibility Study Q3 2026

We want to see CAY execute its development plan as they have outlined below:

(source)