Why a Market Downturn is Healthy

Published 18-MAR-2023 16:00 P.M.

|

8 minute read

As far as the small cap market goes, the past week has been one of the worst we’ve seen in a while.

There’s a lot going on at the moment, particularly in the US banking sector.

That uncertainty inevitably finds its way to the ASX.

And it is magnified in small caps - which have been having a bit of “purge” recently.

A small cap market purge is healthy in the long run as it discovers and tests the lower bounds of company valuations.

A purge clears out traders and short term holders, and tightens shareholder registers towards long term holders.

This is compared to a bull market that tests and finds the higher bounds of company valuations - obviously way more enjoyable for traders, speculators and short term investors.

During a purge, many great companies that may have been valued “too high” for a while, will often overshoot towards being valued “too low”.

...and finally become attractive to new long term investors.

It’s the circle of life.

“Lower company valuations combined with tight share registers full of long term investors” is the formula for an increasing share price when the market turns back positive.

This is why a small cap market purge is healthy in the long run.

But obviously it’s ZERO fun while a purge is in progress.

Our strategy is to be long term investors. We try to find and Invest in quality companies with good management.

We ride the good and bad times in the hope that over 3 to 7 years the company will deliver enough objectives to sustainably re-rate the share price.

We partially de-risk along the way as companies achieve key milestones and share prices re-rate.

Hopefully a few Investments will achieve 10x plus returns.

Like we did during the COVID crash back in 2020 (and during other periods of weakness in the market), we generally hang on to all our positions and patiently wait for the market to turn.

The worst position is to be a forced seller during a market capitulation.

During rough times, we like to increase our participation in rights issues and placements for our Portfolio companies that are running low on cash.

As long term investors we have carefully selected our Portfolio companies.

During bad market conditions, capital raisings are priced at attractive discounts to already beaten up share prices, in order to attract reluctant capital.

Even though participating in capital raisings during a market purge feels counter-intuitive, most of our best returns have come from Investing during the worst market conditions.

Recently we have committed cash to rights issues or placements in LCL, TMZ, GTR, GLV, MEG, OKR and ALA.

Note: this is NOT financial advice, it has worked for us and our specific situation but it’s a risky strategy that can result in long periods of tied up capital and face palming if the market stays bad for long periods of time and share prices fall even more.

We now are also looking at new companies to add to our Portfolio.

Over the last week, we have been quiet on the email updates as our team switched focus to running the ruler over a few companies that we have been watching that are suddenly trading at much more attractive valuations.

We are also looking at capital raisings in new companies that are unfortunately (for them) low on cash during these awful market conditions.

Aside from anyone who first started investing after the COVID crash, most of us know that markets move in cycles and don’t go up forever... or stay down forever.

So hopefully this current market purge won’t last too long and we might emerge with a couple of “bottom of the cycle” pickups.

Or it might last longer than we think, so adopting a “slow and steady” approach to new Investments and participating in capital raisings is prudent.

We remain bullish on the commodities super cycle, and our view is that the companies to bounce back strongest when sentiment turns will be in battery materials and energy.

A silver lining to the current market sentiment is that gold has been on a nice little run.

So what else are we observing during this market “purge”?

Even when companies release good news we’re noticing that the good news gets sold into as short term investors use new buying pressure as an opportunity to exit positions.

Markets like this are brutal because all news no matter how good or bad is mostly met with the same reaction - more sellers than there are buyers.

Generally, in a good market everything is going up and this creates its own momentum.

Investors feel rich with paper profits (and some actual profits) so are happy to invest in capital raisings, because “everything is going up”.

Closing a capital raise in a bull market can be incredibly quick, sometimes over in minutes.

In a bad market, all of this is turned on its head - negative sentiment has its own momentum as well.

In a bad environment, capital raisings take place at larger discounts, take longer to close and sometimes need to be extended to try and fill shortfalls.

Which makes a stronger cash balance all the more important.

Meanwhile, some companies can defy gravity and move up (or at least tread water/go sideways) even as the market generally trends downwards.

As we noted last week, it can be a unique phenomenon where traders latch on to any upwards momentum in a rough market.

So in this kind of market, we look for a couple of things.

1) A stock that people want to hang on to - i.e. it’s been tracking sideways (or even up) while everything else is going down.

2) Cash in the bank - now is not the best time to raise cash, so any company with lots of cash in the bank is a big plus as it can weather the storm a bit better

Here’s our analysis of the companies in our Portfolio that fit either one of these criteria or both.

After a positive start in January, the market started feeling sick at the start of February, and really started barfing during the last couple of weeks.

Here are the stocks in our portfolio that have either gone sideways or even up since February 1st:

(note - this is just a very specific time window for illustrative purposes of todays example)

It’s also important to note that some of the above companies already experienced weakness in the lead up to February 1st, so had already consolidated at a lower point, and appear to be happy at the level at which they entered the recent rough patch.

When raising capital is hard in a bad market, investors will usually punish stocks that are very low on cash and look like they need to raise money in the near term.

Most investors will wait for the inevitable capital raise at a deep discount, rather than buying shares on market.

Some existing investors will even sell in anticipation of participating in a discounted cap raise, further pushing down the price - a vicious cycle.

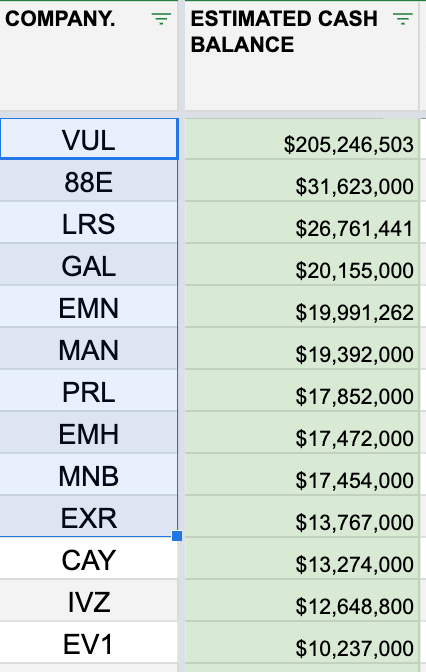

Companies that have a big cash balance during a bad market generally hold up better.

Here is a list of our portfolio companies who are (by our estimate) sitting on over $10M in the current bad market:

Obviously each company has a different market cap, spends at a different rate and some have big ticket items like drill campaigns in progress or coming up, but as a rule of thumb we think any sub $50M company with over $5M in the bank is in a good position during tough times.

(you can see the full list of cash balances at any time here)

Note that these cash balances are correct as at December 31st plus any cash from shares issued under a cap raise since that time. It doesn’t account for any expenditure of the company in that time, we will get a better idea of the Company’s FYQ3 balance at the end of next quarter.

Congratulations to MNB, LRS and CAY who have held up well in the bad market AND are sitting on a large cash balance.

This week’s Quick Takes 🗣️

ALA: Appointment of medtech veteran as Chairman

BOD: Trial milestone for over-the-counter CBD insomnia treatment

GTR: Drilling data acquired to accelerate uranium resource

KNI: massive sulphides intersected at Norwegian Nickel Project

LCL: rights issue closing shortly - drilling now at PNG project

⏲️ Upcoming potential share price catalysts

Updates this week:

- KNI: Drilling 2/3 of its Norwegian battery metals projects inside the EU.

- Massives sulphides intersected at Norwegian Nickel Project (read our full take here)

- 88E: Drilling for oil in the North Slope of Alaska next to UK listed Pantheon Resources.

- The company tweeted out some photos of the drilling program which is currently underway that you can see here.

No material news this week:

- GGE: Drilling its US helium project looking for a commercially viable flow rate.

- EV1: Updated DFS looking to improve on the already relatively strong US$323M project NPV.

- DXB:Interim Analysis of Phase III Clinical Trial on FSGS (Q3, 2023)

- IVZ:Drilling oil & gas target in Zimbabwe, Myuku-2 (Q3, 2023)

- NHE: Scheduled to drill two targets this year at its helium resource in Tanzania (Q3, 2023)

- GAL: Is undertaking a second round of drilling at its Callisto PGE discovery in WA.

- TMR: Maiden JORC resource estimate for its Canadian gold project.

Have a great weekend,

Next Investors

General Information Only

S3 Consortium Pty Ltd (S3, ‘we’, ‘us’, ‘our’) (CAR No. 433913) is a corporate authorised representative of LeMessurier Securities Pty Ltd (AFSL No. 296877). The information contained in this article is general information and is for informational purposes only. Any advice is general advice only. Any advice contained in this article does not constitute personal advice and S3 has not taken into consideration your personal objectives, financial situation or needs. Please seek your own independent professional advice before making any financial investment decision. Those persons acting upon information contained in this article do so entirely at their own risk.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.