80% of the global niobium supply is controlled by one company CBMM. Niobium sits as the second highest risk metal on the critical materials list for both the EU and the US for supply concentration.

$0.115

Opened: 06-Aug-2024

Shares Held at Open: 24,900,000

What does SGQ do?

St George Mining (ASX: SGQ) is a Brazilian niobium & rare earths developer in the state of Minas Gerais.

What is the macro theme?

80% of the global supply for niobium is controlled by one company and one mine in Brazil.

This commodity is considered the second highest commodity for both the US and the EU in terms of supply chain risk.

Although the market for niobium is still relatively niche, it may grow as metal of the future in things like ultrafast charging batteries.

Rare earths are also considered critical minerals with production and processing capacity concentrated in China.

Our Big Bet for SGQ

“SGQ defines a niobium/rare earths deposit large enough to take into development or attract corporate interest via a takeover at a market cap of >$500M”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our SGQ Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true

Why did we invest in SGQ?

Niobium is a critical mineral. Governments want it, SGQ has it.

80% of the global niobium supply is controlled by one company CBMM. Niobium sits as the second highest risk metal on the critical materials list for both the EU and the US for supply concentration.

SGQ is capped at $55M post acquisition, much smaller than listed peers.

Post acquisition SGQ will be capped at A$55M (at 2.5c/share). Peers that have made niobium discoveries include WA1 Resources ($842M) and Encounter Resources ($249M). SGQ can also be compared to peers that have defined Rare Earth Element projects including Brazilian Rare Earths ($550M) and Meteoric Resources ($210M).

Existing discovery with 500 intercepts above 1% niobium.

Compared to other companies that are in the exploration stage, SGQ already has a niobium discovery. This provides a strong foundation for SGQ to quickly progress towards a JORC resource through more drilling of its own.

Money flowing into companies developing niobium projects.

Because of the importance of niobium, and its concentrated supply chain, large swathes of capital is pouring into other companies that are developing niobium projects. WA1 and Encounter Resources are two of the most successful stories on the ASX, both discovering niobium in WA.

Project sits next door to the largest niobium producer in the world.

SGQ is next door to CBMM, which supplies 80% of the global niobium market. SGQ’s project sits on the same geology as CBMM.

Only 10% of the project has been drilled (exploration upside).

To date, only 10% of SGQ’s project has been drilled with most of the drilling only down to ~50m depths. The high-grade mineralisation commences at surface and is open in all directions, leaving open the possibility for this discovery to grow even bigger.

Rare earths, with high grade TREO.

SGQ’s project also contains ultra high grade rare earths with TREO grades >10% in 10-60m intercepts. SGQ’s project sits on the same type of geology (carbonatites) as Lynas’ giant Mount Weld rare earths mine.

Project located in the same state in Brazil as Latin Resources.

The project is located in the Minas Gerais state of Brazil, a state that we have visited and home to one of our best ever Investments, Latin Resources. Latin Resources grew from $0.03 to over $0.40 off the back of a giant lithium discovery. The region is very mining friendly with good access to infrastructure and power.

Project acquired from a forced seller.

The vendor of the asset (Itafos) is a TSX listed phosphate producer and is currently going through a de-leveraging process trying to reduce debt. SGQ is picking up an asset that Itafos likely sees as non-core because of the business’ phosphate focus and a lack of bandwidth to bring another mine into production.

What do we expect SGQ to deliver?

Objective #1: Acquisition completion

We want to see SGQ satisfy the conditions for the acquisition and complete the deal.

Milestones

![]() Shareholder approvals

Shareholder approvals

![]() Upfront cash payment completed

Upfront cash payment completed

![]() Deferred consideration #1 Paid

Deferred consideration #1 Paid

![]() Deferred consideration #2 Paid

Deferred consideration #2 Paid

Objective #2: Drilling to increase size of discovery

We want to see SGQ drill out its existing discovery at depth and in all directions to increase the footprint of the deposit.

Milestones

![]() Drilling permits granted

Drilling permits granted

![]() Land access agreements

Land access agreements

![]() Drilling commenced

Drilling commenced

![]() Drilling results

Drilling results

Objective #3: Maiden JORC resource estimate & met testwork

We want to see SGQ define a maiden JORC resource for its project. As part of the resource estimate we also want to see SGQ run some metallurgical testwork and confirm its project sits on similar geology to CBMM’s project next door AND that it can be processed using similar processing techniques.

Milestones

![]() Metwork updates

Metwork updates

![]() Maiden JORC resource estimate

Maiden JORC resource estimate

Objective #4: Enter feasibility studies

We want to see SGQ take its project into economic studies either via a scoping study, Preliminary Economic Assessment (PEA) or a Pre Feasibility Study (PFS).

Milestones

![]() Scoping study/preliminary economic assessment commenced

Scoping study/preliminary economic assessment commenced

![]() Scoping study/preliminary economic assessment completed

Scoping study/preliminary economic assessment completed

What could go wrong?

Exploration risk

A big part of our Investment is in seeing SGQ extend mineralisation at its project at depth and along strike.

There is no guarantee that drilling will return anything of significant commercial value for SGQ (either through weak grades or thin intercepts).

There is also some risk associated with metwork for later stage projects like SGQ’s - SGQ will be focusing on understanding the metwork over the coming months in parallel to drilling.

Commodity price risk

The niobium market is very small, which means that there can be big swings in commodity prices based on supply out of CBMM (who controls 80% of the market).

There are also a number of substitute commodities to niobium such as tantalum and vanadium.

If the price of niobium accelerates, then buyers may look for substitutes, pushing the price of the commodity down.

Deal Risk

The acquisition by SGQ is still subject to a certain number of conditions being met.

SGQ will need to get shareholder approvals for the deal - and there is a chance the vendor will need to get approvals for the transaction also.

SGQ expects the conditions of the deal to be satisfied by late September/early October 2024 but there is always a risk that these do not happen. If the deal falls through then our Investment Thesis wouldnt be applicable anymore.

Deferred payments risk

To pay for the acquisition SGQ will need to make three separate payments totaling US$21M. The first US$10M instalment is due on closing of the deal with the remainder due over the next 18 months.

IF SGQ is unable to raise funds to pay for the deferred milestone payments then it risks losing the asset. It is possible that SGQ fails to make these payments in which case we would expect the company’s share price to be re-rated significantly lower.

Market risk

Broader market sentiment could deteriorate, and shares as an investment class trade lower, taking SGQ’s share price with it. Alternatively, there could be further sector specific pain ahead where junior explorers suffer a lot more than the broader market.

Development/delay risk

Should any or all of the above risks materialise, SGQ could wind up stuck in “development purgatory” where newsflow dries up and the project remains stagnant for a prolonged period of time, hurting the share price. Additionally, if delays occur in terms of material newsflow, the market could turn on SGQ.

What is our investment plan?

We are Invested in SGQ to see it progress its project into development.

Our plan is to hold the majority of our position in SGQ for 3 to 5 years which we hope is enough time to see SGQ to move towards development (see “our long term bet” above).

After 12 months we will apply our standard de-risking strategy.

We may also look to sell up to 20% of our holding if the company delivers on one or more of our Investment Memo objectives and/or the share price materially re-rates.

Any sell downs will be in accordance with our trading and hold policy disclosure.

Disclosure: Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 24,900,000 SGQ shares at the time of publishing this Investment Memo. The Company has been engaged by SGQ to share our commentary on the progress of our Investment in SGQ over time. Some shares are subject to shareholder approval.

SGQ: New upgraded resource: 75% bigger at 70.91Mt @ 4.06% TREO (and 0.62% niobium) - with drilling ongoing…

Mar 3, 2026

Mar 3, 2026 |

11 min

The largest and highest-grade carbonatite-hosted rare earths deposit in South America. The highest grade undeveloped rare earths asset in the Western world. And it just got 75% bigger… Today our Investment St George Mining (ASX: SGQ) significantly increased the size of its rare earths-niobium project in Brazil.

SGQ: Giant rare earths deposit in the USA’s “neighborhood” - how about these drill results…

Jan 19, 2026

Jan 19, 2026 |

11 min

This morning our Brazil rare earths & niobium Investment St George Mining (ASX: SGQ) hit more high grade rare earths mineralisation. Up to 99.1m at 5.62% rare earth grades, all from surface

SGQ: 87.7m high grade rare earths drill hit - 150m step out from existing JORC resource. Gina Rinehart invests $22.5M.

Oct 23, 2025

Oct 23, 2025 |

12 min

St George Mining (ASX: SGQ) already has the largest and highest-grade carbonatite-hosted rare earths resource in South America - in Brazil. It’s the second-highest grade rare earths resource in the Western world. (it also has a big niobium resource, which we think the market is not pricing in while rare earths take all the attention)

SGQ signs strategic rare earths alliance with US defence industry magnet maker

Sep 10, 2025

Sep 10, 2025 |

12 min

It’s happening. The USA is banning its domestic defence contractors from using Chinese-sourced rare earth magnets and metals in any weapons system. The US has set a date for when rare earth import bans come into effect - 31 December 2026

SGQ: USA signals interest in Brazil rare earths and niobium in potential new trade deal

Jul 28, 2025

Jul 28, 2025 |

9 min

The US has made it clear that the first critical mineral market it wants to beef up is rare earths. 48 hours ago we saw this article saying that the “United States has begun signalling interest in a trade agreement with Brazil focused on access to critical and strategic minerals, including niobium and rare earth elements”. (Source) We think our Investment St George Mining (ASX: SGQ) could be one of the few winners with an asset outside of the US from the big flow of US capital into the critical minerals sector.

SGQ signs downstream deal to upgrade magnet rare earths

Mar 12, 2026

Mar 12, 2026 |

4 min

Our rare earths and niobium Investment St George Mining (ASX: SGQ) just signed a strategic alliance with Brazilian nano materials company Nanum Nanotecnologia.

SGQ keeps hitting 100m+ rare earth intercepts from surface

Mar 11, 2026

Mar 11, 2026 |

4 min

Our rare earths and niobium Investment St George Mining (ASX: SGQ) just released more 100m+ fully mineralised intercepts from its rare earth project in Brazil.

SGQ hits largest rare earth intercept from South America’s largest hard rock rare earths project

Feb 18, 2026

Feb 18, 2026 |

3 min

Our rare earths and niobium Investment St George Mining (ASX: SGQ) just drilled its largest intercept at its rare earth project in Brazil.

SGQ acquires land for processing infrastructure at its rare earths/niobium project

Feb 16, 2026

Feb 16, 2026 |

3 min

Our rare earths and niobium Investment St George Mining (ASX: SGQ) just acquired land suitable for processing infrastructure next to its project in Brazil.

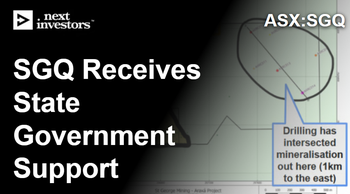

SGQ receives state government support for Brazilian rare earths project

Feb 13, 2026

Feb 13, 2026 |

4 min

Our rare earths and niobium Investment St George Mining (ASX: SGQ) has just received further state government support for its rare earths and niobium from its project in Brazil.

Broken or Sprained? What the Market's Telling Us Right Now

Mar 28, 2026

Mar 28, 2026 |

20 min

Is the market broken again? What could be different this time? Maybe this Iran conflict market freak out of the last few weeks is just a “tweaked hammy” or “dead leg” and recovery will only take a couple of weeks…

Sunday Edition: 22nd March

Mar 22, 2026

Mar 22, 2026 |

22 min

Here you can find links to everything we wrote last week, plus some interesting stuff we came across on our travels.

Sunday Edition: 15th March

Mar 15, 2026

Mar 15, 2026 |

21 min

Yesterday we wrote about the “SaaSpocalypse” being overdone. We think there are currently some great ASX listed SaaS businesses out there with share prices that have taken a big haircut in recent weeks, and valuations are very attractive during peak SaaSpocalypse fear. We also provided an update on each of our favourite themes for 2026. (silver, gold, military metals, AI metals, robot metals, energy and oil & gas) Silver is still one of our favourite themes for the next 12 months. (waiting for that next leg up in the silver price that should lift all silver stocks)

We Survived the SaaSpocalypse (Here is Our Next Move)

Mar 14, 2026

Mar 14, 2026 |

20 min

Ever had a breathless stockbroker call you and generate huge amounts of FOMO about a company to get you to put money into a capital raise? (it works) Then a week later when the stock is trading at 20% below the placement price you wonder why you got so hot and bothered on the phone call? All these “AI is going to disrupt everything” announcements are sort of like that… except at a global scale. Has your company ditched its software systems for AI vibe coded replacements yet? Probably not.

Sunday Edition: 8th March

Mar 8, 2026

Mar 8, 2026 |

21 min

Here you can find everything we wrote about last week, plus some interesting stuff we came across on our travels. On Friday afternoon after market, the S&P Dow Jones Indices announced changes to the ASX indices, which will be effective from Monday March 23rd. A few of our Portfolio Stocks are climbing into the All Ordinaries Index...