A Rough Week That Ended Well

Published 13-JUN-2026 12:49 P.M.

|

14 minute read

Disclosure: S3 Consortium Pty Ltd and its associated entities may hold direct or indirect interests in securities referred to in this publication and may receive fees or other forms of consideration from entities mentioned. These interests and arrangements may create a potential conflict of interest in the preparation of this material.

The information contained in this communication is provided for general information purposes only and may relate to speculative investments. It does not constitute financial product advice, and has been prepared without taking into account your personal objectives, financial situation or needs. You should consider obtaining independent financial advice before making any investment decision.

Any forward-looking statements are uncertain and not a guaranteed outcome.

Thank god that week is over.

Well the first 4 days of it at least - things appear to be turning positive again in the last day and half.

On Thursday night, new talk of an Iran peace deal made the Aussie markets pop on Friday.

Then last night SpaceX started trading on the NASDAQ and... went up - lifting many moods AND the US markets, which means the ASX small end should be good on Monday.

(SpaceX’s IPO performance is an important barometer for sentiment in the broader global markets, with a lot of people watching - more on this in a second.)

But the days BEFORE, things had been looking rough...

Much like the back end of last week, there was no point even looking at the market for the first half of this week.

Nearly everything we watch or care about continued getting beaten down.

May as well come back to the screen once the current vomit has run its course.

(which is now looking good, earlier than we expected - thanks Donald and Elon).

To spare ourselves force-drinking from the firehouse of red hued horrors emanating from our screens earlier this week, we took a rare few days off from writing daily emails too.

(Mental health day? Our work environment of watching small ASX stocks definitely did NOT feel like an emotional “safe space”...)

Last Saturday we blamed the prior week's “sea of red” on tax loss selling in June... (read it here)

(with a silver lining... it meant that for the first time in 3 years, people out there had been making enough capital gains that needed offsetting with June selling, which is an acceptable consolation prize I guess).

Why did things get worse in the first half of this week?

Commencing what already promised to be another grim “June tax loss selling” week on the small end of the markets...

With the ASX feeling sick in bed, dizzy and fighting not to barf even more...

The US markets decided to (proverbially) drunkenly come home at 3am and jump into the bed with poo stained trousers... and get grabby.

Making matters worse down here.

Before Trump’s peace deal and the day one SpaceX success, the DOW and NASDAQ continued their drops over the first 3 days of the week, again infecting sentiment and affecting selldowns on the ASX.

Gold and silver both copped it too.

(Fun fact - every multi year gold and silver mega-bull run in the last 60 years had a major pull back before the huge, main run - more on this in a second too)

At least on Monday the ASX was closed for a public holiday...

We all had one day of respite prior to the forced insertion into our collective bottoms by the sideways pineapple of another brutal small cap sell off.

BUT it ended on a positive note:

There was a big rebound yesterday with the ASX up almost 2% closing up overall for the week, and positive sentiment trickling down to our small caps.

The night before, Donald Trump gave a boost to the US market by calling off planned strikes on Iran at the last minute.

ANOTHER imminent peace deal?

Seems like when the US markets drop too much, Trump declares a ceasefire or imminent peace deal to end the conflict.

And the market goes right back up again.

This has happened quite a few times now:

(source)

(Source)

It's widely reported that a buoyant US market is a key pillar in Trump's strategy for the mid-term elections in November this year.

(which bodes well for our stocks in the second half of 2026)

The wording of this most recent “last minute cancellation of planned attack and imminent peace deal” was one of the strongest yet.

And the market liked it.

Ok, get your tin foil hats ready...

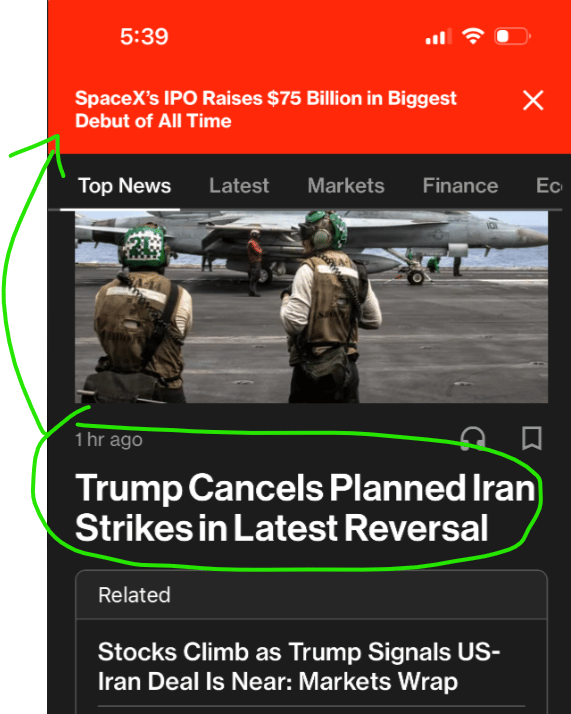

Given how important the SpaceX IPO is to the US markets, is it just a co-incidence that Trump pressed the “make markets good now” button less than 24 hours before SpaceX commenced trading?

- It’s no secret that Trump wants buoyant and all time high markets leading into mid term elections in November

- SpaceX’s IPO performance is going to determine the market mood for years to come...

- SpaceX’s IPO performance will set the scene and tone for two follow up blockbuster US IPOs in AI: Anthropic and OpenAI - also key drivers in the flywheel of the market mood leading to November mid term elections.

A lot hinges on these three blockbuster US IPOs delivering the goods, and injecting positive moods into the US markets (which trickles down to the ASX)

And the first test is SpaceX.

We managed to take the below screenshot on our phone that planted the seed of this wacky conspiracy theory.

“1 hour ago Trump canceled planned attacks... Then breaking news in red: SpaceX raises US $75BN... and will commence trading in less than 24 hours:

Stranger things have happened... right?

In the early hours of this morning Australia time, Elon Musk rang the opening bell for SpaceX on the NASDAQ.

And this morning we woke up to the news that it closed up 19% from IPO price.

Job done, everyone happy, paper and real profits all around, “how good is the stock market”, “I’m so good at investing”, “ I wonder what else I should invest in?”...

It’s only the first day for SpaceX, but after the sentiment rollercoaster over the last few weeks we’ll take the win.

(and as always, as our compliance manager reminds us - the past performance of SpaceX is not a reliable indicator of future performance)

Market ups and downs aside, we have a plan and we are sticking to it.

So while the little old ASX small cap market is effectively an “Australian kite caught in a USA hurricane”...

At least markets have been up more than they’ve been down over the last 12 months.

We have chosen our macro themes, we are playing the long game.

And after a few days off from writing emails about our Portfolio stocks and staring at the screen, we are hoping Trump’s “rev the markets into the November” plan will provide the next phase of buoyant conditions for our small ASX stocks.

While helplessly staring at the temporary sell down in our (and most other) stocks wasn't helpful, what WAS helpful was putting some time into our key macro investment themes.

Here is this week's edition of “coping with our stock prices getting hit by re-enforcing our belief in our chosen long term macro investment themes”:

Cope 1: Gold and silver multi year bull runs always have major pullback before the big price rise

We went back in time a bit this week and checked out previous gold and silver multi-year mega bull runs.

Turns out there is always a big, mid-bull run pull back.

First, here’s what AI had to say about it, presented in a nice table:

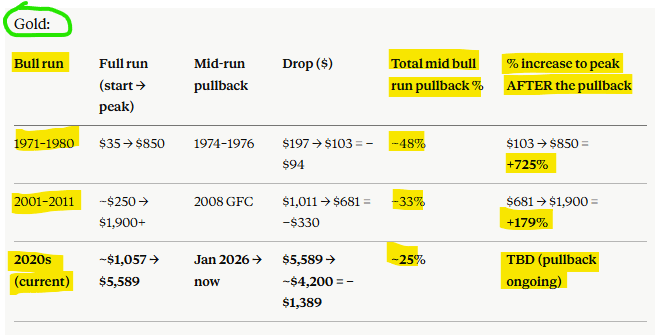

Gold:

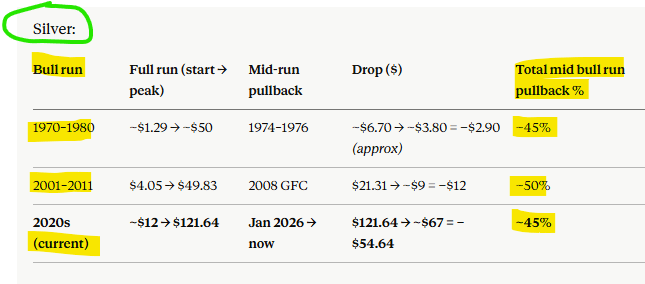

Silver:

Now here’s my meat brain cutting and pasting some charts for more context.

I’m trying to imagine the current gold and silver pull back as the mid bull run pullback in historical runs (highlighted in yellow) BEFORE this bigger price run happened:

Gold & silver in the 70’s:

Gold fell from US$200 to US$103 in the mid 70s - from that low it ran to US$850 by January 1980.

~48% pullback before the main run show in yellow:

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Silver did something very similar just before that parabolic run to U$50 between 1978-1980.

(zoomed in on the 43% pull back before the main run because the subsequent run up makes it look like barely a blip)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

In 2008 during the GFC:

Gold dropped from US$1,030 to ~US$680.

By April 2011 and gold was US$1,920

~33% pull back before the main run shown:

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Silver dropped from US$21 to ~US$9.

Silver then ran to US$49.

~58% pullback before the main run shown:

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

What are we seeing now?

Gold pullback at ~25% from peak:

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Silver pullback at ~45% from peak:

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

So are these the pull backs before the main run?

We’ll see.

Pretty inline with the past pullbacks so far.

I’m not sure if we’ve mentioned this, but past performance is not an indicator of future performance.

This would all be great if past performance WAS an indicator of future performance, which unfortunately it isn't.

Obviously we are hoping for a major run after a not too long sideways period for both gold and silver.

So what happens next?

Who knows, but we hope it's a similar flush out, pre-rally, like it has happened in the past.

We are positioned on our thesis that gold and silver will deliver a major, even bigger run once the current pullback / sideways phase is complete.

(The past not being an indicator of the future of course.)

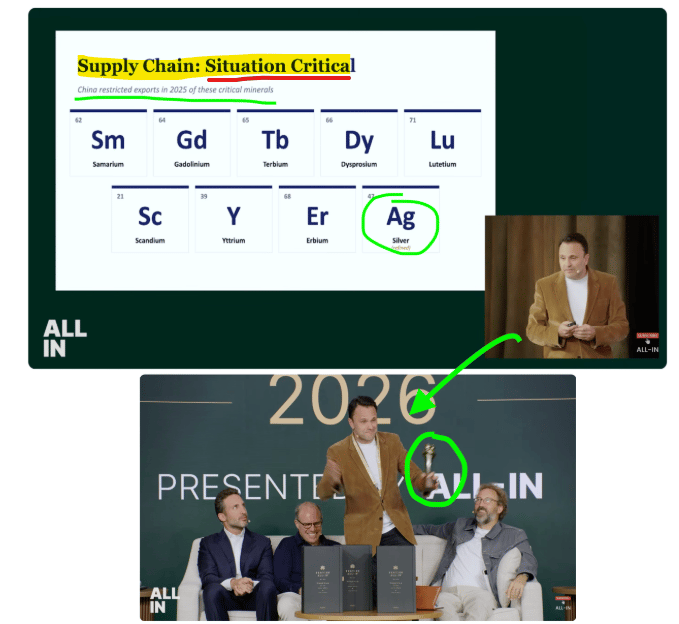

Cope 2: Critical Minerals guy wins a pitch battle at US Venture capitalist conference

We have been banging on for a while now about how we think the US critical minerals push is going to be a 5-10+ year macro thematic.

This week a US commodities specialist fund manager (yes, they exist) - Dan Dreyfus - presented to a majority tech crowd at the All-In Liquidity Summit (and the All-In Podcast Series).

In fact, the same guy also won “best pitch” award for his long energy and hard asset thesis from the investors sitting in the crowd:

(Side note: does anyone remember the name of that Perth Drum and Bass MC from the mid 2000s that used to say “situation critical” a lot? Please reply if you do)

Yet again, another signal that there is appetite (and capital) for critical minerals yet to come out of the US.

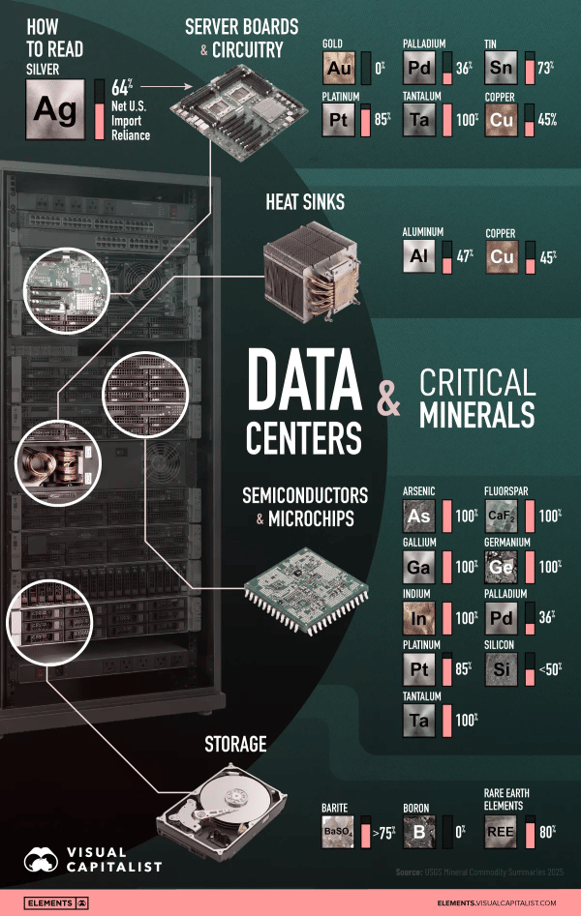

Dan’s whole pitch is around a 15-year commodity supercycle driven by simultaneous demand shocks (AI data centres, grid rebuild, reshoring, defence, aerospace)...

... colliding with a domestic supply base nobody has invested in for 20 years, plus fiat debasement as the kicker.

Exactly what we have been writing about almost weekly for the past few years.

Check that our most recent article dedicated to this here: Triple-Crown Supercycle: The 3 Incoming Global Buildouts

Dan’s comments on the US government’s willingness to support the sector were our favourite bits - he mentions support across three paths (equity, permitting and take-or-pay offtakes with floor prices).

All of the demand side signals mines need to get off the ground.

Interestingly he also talked about silver saying the world was short ~200M ounces per year and that the 600M ounce above ground inventory would run out in three years.

On silver, he also said:

1. The China export cutoff list:

"Samarium, gadolinium, terbium, dysprosium, lutetium, scandium, yttrium, erbium, silver, just cut it off ."

2. The main silver block (one continuous passage, late in the talk):

"We're going to be short silver, for example, to build these solar panels, especially if we start launching data centers in space, right? These are going to consume incredible amounts of silver. But right now the silver supply demand dynamic is we consume 1.2 billion ounces a year. We supply a billion ounces a year. So there's a 200 million ounce deficit per year and we only have 600 million of above ground inventory left. So the clock's ticking. We got three years left guys before we just stock out. And then the solar story is where do you get the silver for the photovoltaic cells?"

3. His closing allocation comment:

"So for our kids and for the country generation tool belt for us allocating, get some exposure to copper, silver, minerals and then there's a bunch of service providers in and around that area that we should be investigating over the next year."

Check out Dan’s full pitch here: Dan Dreyfus: America’s Critical Minerals Crisis is Here

Cope 3: AI spend - Zork game analogy for how much is still to come in the AI buildout

The calls of “AI is a bubble” have been coming almost since AI first caught investor attention a few years ago.

(1999 dot-com crash PTSD maybe?)

Will the AI and datacentre buildout not be big enough to drive all the new critical minerals supply we are predicting?

Bill Maris (founding CEO of Google Ventures, early backer of CrowdStrike, Coinbase and Cohere) made an analogy last week that stuck with us.

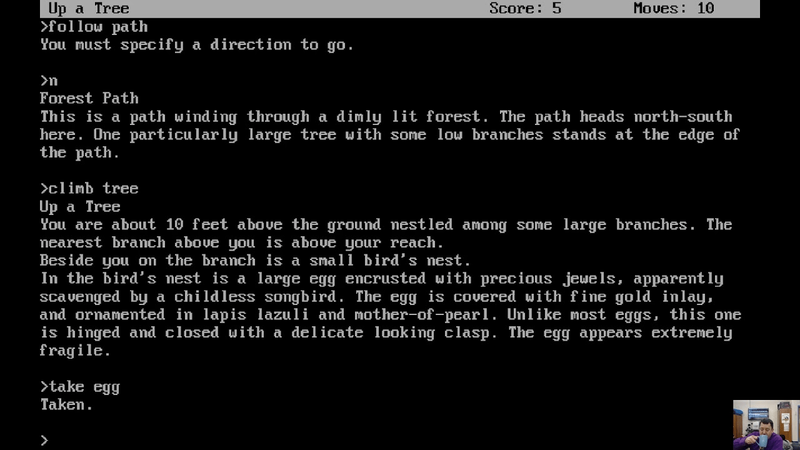

Back in the 1980s, the most sophisticated game you could play was Zork.

It was a text adventure. You typed "grab the lamp" and the computer spat back an error because you should have typed "lantern".

(still, these games were mind blowing at the time, a lot of fun)

(yes this was a “game” in the 80s...)

Now look at gaming today - photorealistic, real-time, entire worlds you can inhabit:

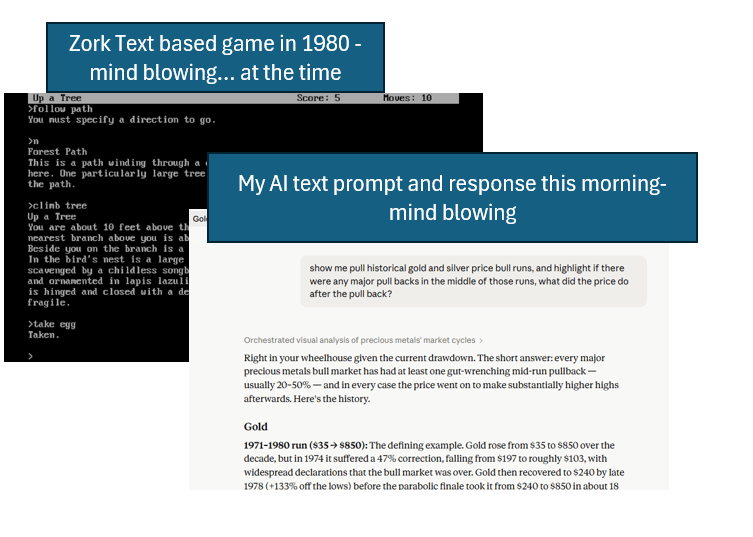

Maris's point is that today's text based AI chatbots are like the original text based Zork.

You type a prompt. You wait. It forgets your last session. It misunderstands you in ways that feel a lot like "I didn't recognise the word lamp".

Yet it's the most incredible thing you have ever seen...

In his words, we're at the "Atari command line stage" of AI - and he reckons the gaming industry's 40-year journey is going to be compressed into about five years for AI.

(both look pretty similar, right? Imagine what we will think looking back at AI text chat interfaces in 10 years time)

But here's the part we think matters most for investors.

What took gaming from Zork to PlayStation wasn't better stories.

It was controllers, physics engines and GPUs - the underlying machinery.

Maris says the same will be true of AI.

The value won't just accrue to bigger models, it will accrue to everything that needs to be built to make ambient, always-on AI a reality.

That's compute, data centres, power and the raw materials that go into all of it.

(source)

By the way, how good was the first time that the Zork text games added a graphical interface with “Return to Zork” in the 90s - I spent many weeks on that game:

Also honorable mention goes to Granny’s Garden, mine and many 80’s kids first exposure to computer games:

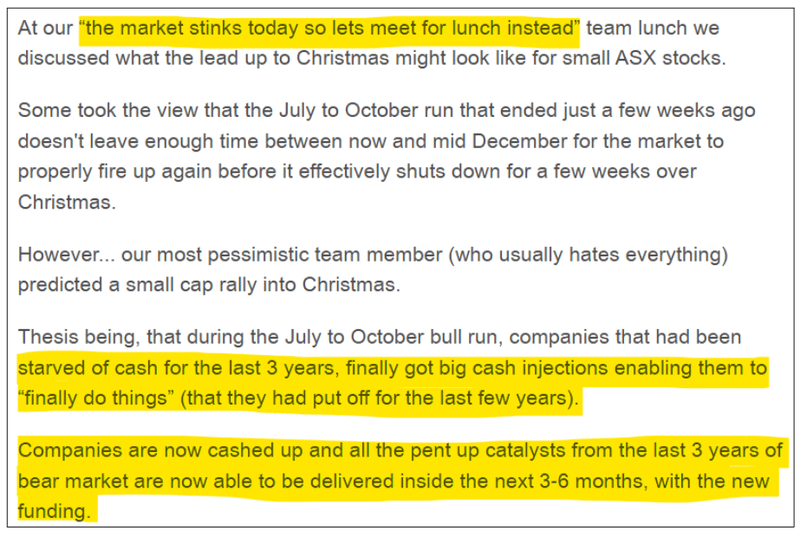

Cope 4: At least most of our companies raised money during last year’s run

Back in November last year, we called a Santa rally - mainly centered around the idea that companies had finally raised cash and could put that cash to work delivering big catalysts.

(The market must have sucked that week, like it did this week - enough to spend the whole day away from our screens at lunch).

Sure enough, the Santa rally came...

(source - our Nov 22nd, 2025 note )

We think the setup this time around is even better.

Most got through that Christmas period - then we came into Jan/Feb where the market was even stronger.

Market sentiment felt like it peaked in February (literally on the last day) when the US-Iran war started.

Some companies used that period of enthusiasm to get some more cash in the door.

Luckily most our Portfolio companies have come out of that period with some pretty strong balance sheets.

(phew - having to raise in this market would be tough)

We are now looking forward to Monday and getting back into it, with what should be a further bounceback in sentiment.

Have a great weekend.

Next Investors

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.