Tax loss selling is back, which is actually a good sign

Published 06-JUN-2026 10:47 A.M.

|

16 minute read

Disclosure: S3 Consortium Pty Ltd and its associated entities may hold direct or indirect interests in securities referred to in this publication and may receive fees or other forms of consideration from entities mentioned. These interests and arrangements may create a potential conflict of interest in the preparation of this material.

The information contained in this communication is provided for general information purposes only and may relate to speculative investments. It does not constitute financial product advice, and has been prepared without taking into account your personal objectives, financial situation or needs. You should consider obtaining independent financial advice before making any investment decision.

Any forward-looking statements are uncertain and not a guaranteed outcome.

Have you got any stocks that were up a lot at some point this financial year?

(Finally! A good year.)

Then they had come off a bit... ok fine, ebbs and flows, in it for the long term blah blah.

And suddenly this week their share prices got kicked in the guts?

It's been a few years now since we have talked much about how “June tax loss selling is smashing small stocks”.

Know why?

Until this financial year, barely anyone in small cap land had any capital gains to offset with June tax loss selling...

So... there wasn’t much June tax loss selling.

(it was more just “every month” indiscriminate selling on good, bad, average or no news.)

But THIS year... It's baaaaack.

“Capital gains” in small and micro cap stocks wasn't really a thing during the “mid-2022 to mid-2025” post-battery metals boom great (small cap) depression.

...only losses - real, paper, hope and otherwise.

I remember how exhausting and depressing it was starting nearly every Saturday note for 3 years with some variation of “another week and the small cap market continues to suck”.

June tax loss selling happens when enough people have locked in capital gains during a financial year - on which they have to pay capital gains tax...

So they decide to sell some other stocks that are below their entry price, at a loss, to offset the gain (and pay less tax).

Stocks which are fine and they may otherwise have held, still expecting it go up again.

So you could even argue that June tax loss selling is a sign (or symptom) of a bullish market...?

This FY many investors had been drawn back from the sidelines into the small end of the markets and probably locked in some gains.

They will likely be “June tax loss selling” the stocks that may have had a run earlier in the financial year but came off again and are down in May/June...

pushing these stocks down even further.

Or the investors who stuck it out during the small cap winter, the hold-outs who braved years of pain and have been rewarded with some locked in capital gains this FY... may be finally dumping a couple of their long held dogs once and for all.

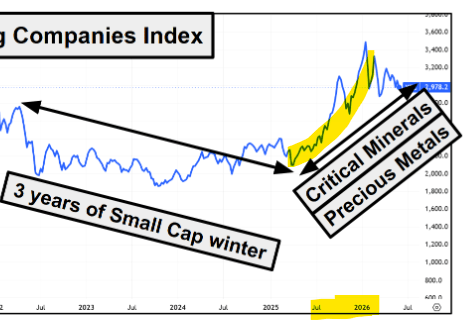

Looking at the screens, it definitely looks like some tax loss selling has kicked in this week.

(Even though the underlying global themes still feel very strong.)

So what happens next?

Again, June tax loss selling is not a thing when nobody is making any capital gains.

But the last 11 months have been broadly pretty good.

(VERY good in comparison to the hellish and barren mid-2022 to mid-2025 period.)

(source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

It was a mostly good FY (still ~ 3 weeks to go) and yes, there were a couple of bad months dotted in between bullish runs...

As we predicted in December 2024 - when we write about how the small end of the market recovery will be like recovering from a hangover (or sporting injury).

Comparing the recovery of the small end of the market to the recovery from a searing hangover.

(or a broken collarbone for those of us old enough not to binge drink anymore but silly enough to still be playing team sports on Sundays)

The point was we said that the small cap market's recovery will likely be similar to recovering from a hangover or sporting injury.

Initially it's slow moving, painful, seemingly never ever ending.

But with time passing, confidence grows, you get longer and stronger periods of strength and recovery.

Until it finally gets back to normal.

(and the risky behaviours commence again?)

Whether self-inflicted (hangover) or accidental (injury), humans need time to slowly recover and build back confidence in increasing waves before getting back to normal function.

Similar to small cap market sentiment...

In Dec 2024 we were celebrating a measly 8 consecutive weeks of positive market conditions.

And we said the market recovery would be longer and longer bullish patches, interspersed with shorter and shorter bearish patches.

So far this is exactly what we have seen since, culminating in the last 11 months being on average more bullish than bearish.

Longer and stronger bullish periods (with some limp months thrown in here and there).

Unfortunately it feels like we are currently in one of those low sentiment bearish ebbs right now, especially the last couple of trading days.

(and we are blaming June tax loss selling)

The GOOD news is:

During generally more bullish conditions like we have seen this FY, once June tax loss selling is over, July is usually when things roar back.

Sometimes even in the last week of June - if the bargain hunters can’t help themselves and swoop in to scoop up the stocks that have been hit hardest by the June tax sellers.

So while we are patting ourselves on the back for getting it right on “how the market is going to recover”...

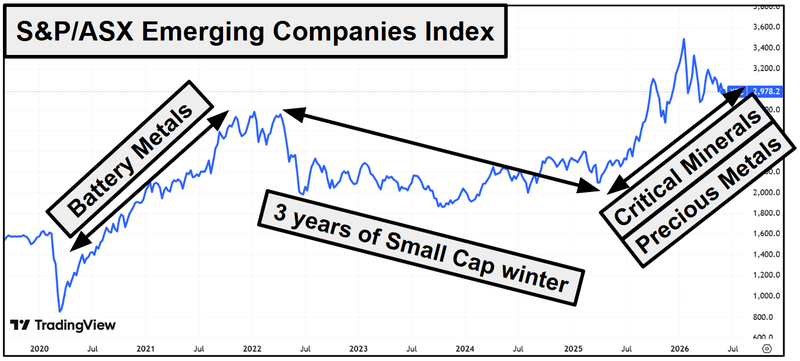

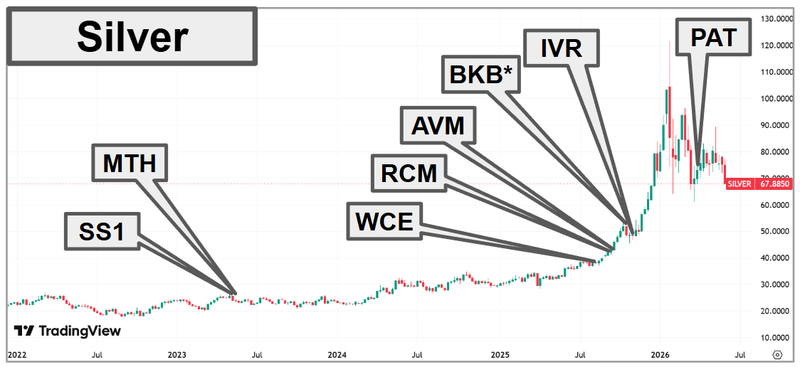

We did ALSO predict the July run at the start of the financial year back in June 2025 - our "checklist" of 6 events that could kick off a July 2025 small cap bull run.

From July 2025 to November 2025 the market delivered the longest and strongest run we had seen since 2022.

(relevant half of the above image)

Note: We are notorious “the market will run in July” predictors - a broken clock is still right twice a day...

(Also, this above image shows the run where some people would have been locking in the capital gains that need to be offset by this month.)

And YES, we reckon it's all going to kick off again in a few weeks time.

US critical minerals, silver, gold and the global AI, robotics and military buildouts driving an “all commodities boom” are still firmly in play in our opinion.

Urgent, global themes like these don’t care that a handful of Australian punters are offsetting tax gains during the Australian financial year because of Australian tax laws.

BREAKING: ~11:30pm AEST Friday night, family asleep, I’m sitting here writing this and then on my other screen gold/silver/copper prices suddenly shit the bed...

- What did he say/do now?

- Check news

- US jobs report has come in way better than expected (AI not taking jobs afterall?)

- Analysts now pricing in US rate hike instead of Trump's desired rate cuts (Baptism of fire incoming for Trump’s new hand picked US Fed guy)

- US dollar stronger, commodities and precious metals priced in USD dinged by a few %

- Potatoes priced in Euros down 26% (not really relevant, just interesting - stay focused, do not go down European potato rabbit hole)

Luckily the commodities heavy ASX is closed on Monday, so we get a full day of forced respite from this knee-jerk reaction in commodities, precious metals and European potatoes.

Anyway, the point is the small end of the market moves in phases, sometimes predictable, sometimes not.

Sometimes in line with expectations, other times defying all logic.

(and sometimes with surprise US Jobs reports or other unexpected twists and turns)

But always certainly ebbing and flowing between positive and negative sentiment.

Our model is to identify the macro Investment themes that we think will attract the most attention and capital over a ~5 year period and find the best stocks in those themes (in our opinion).

Is it annoying seeing our chosen stocks in these themes go down on a bad month? Sure.

But we aren’t short term traders so we don’t duck in and out of stocks.

(you can check our live holdings in any of our stocks any time here)

We joke that we are always 102% deployed - 100% in small and micro cap stocks and 2% committed to future tranche 2 placements in these stocks...

We don’t get shaken off from our Investment thesis by a few bad days in the market.

The other thing to note about macro Investment themes is they often have a fast, early start, a breather, then a second and even third wind.

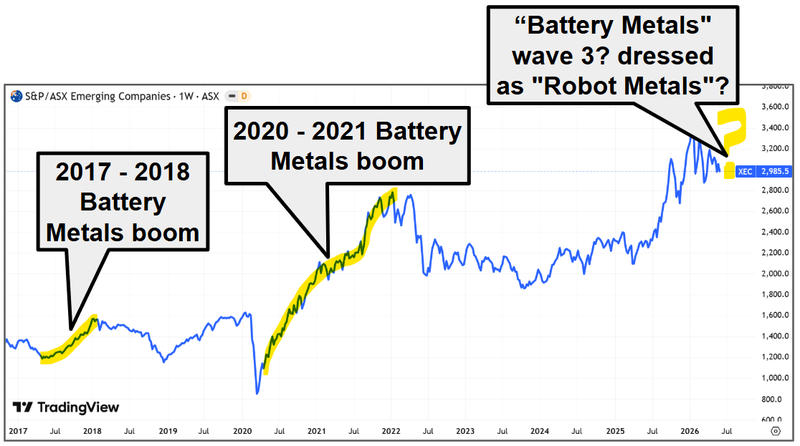

Take the battery metals boom for example - remember that “fast and early out of the blocks” battery metal run in 2017- 2018?

Before the monster one started in 2020?

(source)

Quick tangent for 20 seconds: We reckon the third battery metals wave is going to be dressed as “robot metals”

AI powered robots are basically walking, thinking electric vehicles, and we think every home, business and military unit is going to want a few.

BUT unlike electric vehicles, AI robots aren't fighting for mass adoption and market share against established petrol powered AI robots that already do the exact same job just fine...

AI Robots are a totally new item that we think everyone will want.

So the third wind for battery metals could be dressed as “Robot metals”

Both need the same core metals (lithium, nickel, cobalt, copper etc).

(we still have most of our lithium stocks... many of them have since become gold stocks, but the lithium projects are still there in the background, ready to re-appear when lithium doubles... along with the pitchdeck opening photo of an EV getting charged... or a robot)

Anyway, I digress - the point is that global macro themes come in waves too.

So we generally take a longer term view - and we have seen enough investment thematics play out over 20 years to know that major themes last many years and also ebb and flow in waves.

Was the first July 2025 to November 2025 wave just the small, “early and fast start out of the blocks” like that first 2017-2018 battery metals run?

Before the real run starts?

We hope so...

So while the market is having an “off” couple of weeks - here is a quick update on why we think our current favourite global macro Investment themes will last longer than a limp few weeks on the small end of the ASX...

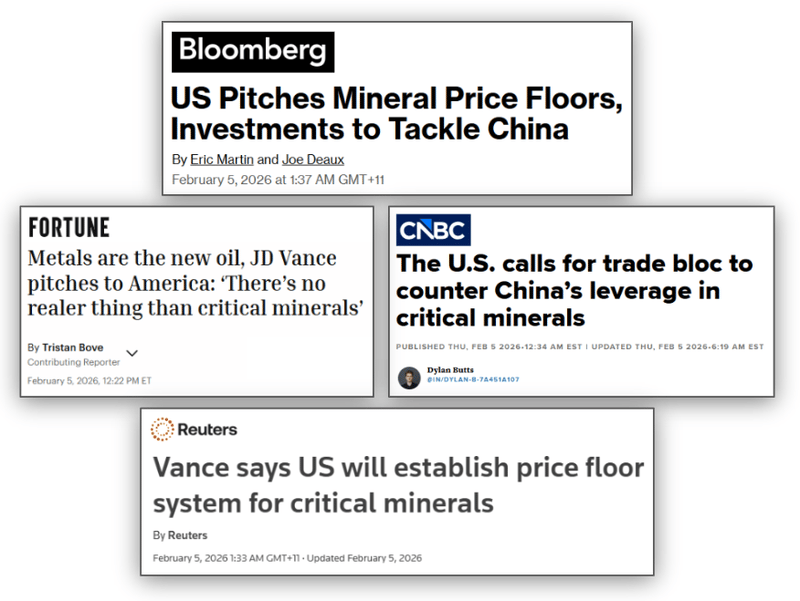

US critical minerals

The USA standoff with China won’t get resolved in a few months, or even years.

(geopolitical matters of this magnitude take 10+ years to play out)

With all the money, executive orders, and urgency coming out of the USA to “rebuild its mining industry ASAP” - we think this one hasn't even gotten started yet.

USA-metals-and-defence trade first kicked off through the back half of 2025 (and arguably in early 2026 too).

Critical minerals ran hard on the US government announcing funding deals with miners - everyone from the president, vice president to the treasury secretary made speeches talking about critical minerals at some point throughout the year.

(Key word being “announcing” - nobody has actually built a mine yet...)

The US gave control of securing supply chains to the Pentagon (Department of War) and even hired a gaggle of Wall Street bankers and dealmakers to help structure and fund mining deals - nicknamed “deal team six” (get it?)

(source)(source)(source)(source)

With all this happening over the last 11 months, we think there will be a LOT more to come on this theme very soon.

And it definitely feels more urgent than the battery metals shortages for electric vehicles (trying to replace petrol cars that already do the same thing) that drove the last big commodity boom...

Silver

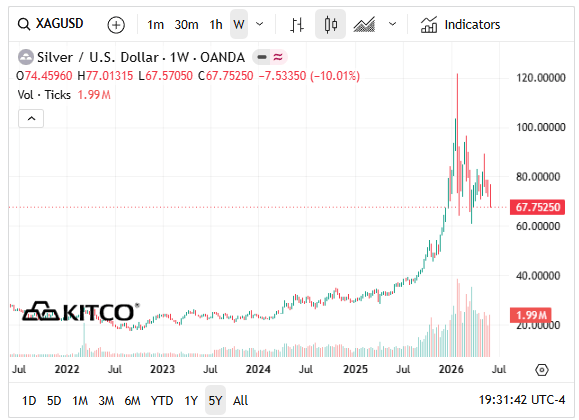

So far so good, silver gave us an incredible run in 2025, into January 2026, and has spent the last 4 months consolidating at way above its previous all time highs:

(source)

(even after the 8% whooping silver got late last night - its still broadly trading sideways at well above its historical all time highs)

We won't forget silver gapping up to US$120 per ounce while the markets were closed over the new year period.

Then watching all of our silver stocks gap up on the first open after the holidays.

It was glorious...

We are still hanging onto all our silver stocks because we think this first run in the silver price was just the preview to an even bigger run to come.

(again, macro themes come in waves)

And when silver runs, it takes silver stocks with it.

We were early on the silver move (remember “silver September 2025” when we Invested in a bunch of silver stocks):

(source)

We’ve written enough about why we think silver is going to run again - you can read more in our silver eBook here.

Now, we’ll be the first to admit we are NOT technical chart analysts...

But remember that “50 year cup and handle” silver chart formation that we casually hubris’d into during the year leading up to the silver price breakout?

Well check out this bullish pennant formation:

(source)

Right?

OK, we have no idea what we are doing here...

If you need some higher quality silver cope after last night’s 8% drop - here is our favourite technical momentum analyst discussing last night's price hit

Gold

The entire global setup seems to be pointing to another eventual leg up in gold.

The world is the most uncertain we have ever seen in our lifetime, with US global dominance being challenged by China.

And history has shown that when an incumbent world power meets a rising world power... the previous global currency can eventually get displaced or eroded.

(we have never seen this happen in our lifetime, the USA has effectively been the “world boss” since after WWII, well before any of us were born)

Gold hit its all time high ~US$5,595/oz on 29 January.

Now it's ~US$1,000/oz off that all time high - which is being reflected in small cap gold stock share prices.

How quickly gold nuts (like us) forget how happy they would have been with a US$4,500/ounce gold price 1 or 2 years ago...

(source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

We are still very bullish.

For the first time in 70 years, we're watching a genuine challenger power rub up against the dominant power.

When the world's reserve currency wobbles, the system goes looking for a new anchor - and it keeps reaching for the one it's trusted for 5,000 years - gold.

The USD's share of global reserves has slid from ~71% (2000) to ~59% - the steepest fall since the gold standard ended (source).

Central banks are still buying hundreds of tonnes a quarter. (source)

And just this week, gold replaced US treasuries as the world’s top reserve asset...

(source)

The gradual yet accelerating upending of the long established world order that is driving gold is NOT something that is going to come to a resolution any time soon...

Speaking of who will win the “global world power” race...

Global AI, robotics and military buildouts

Whichever country wins at AI, robotics and military buildouts will gain the edge to be the dominant world power

So naturally, the USA and China are spending and building all three as fast as they can.

(gonna need some metals and minerals to do that...)

The big tech companies are in a “compute war” raising billions to build data centres to run AI, and robots.

- ~US$700 billion of Big Tech AI infrastructure spend in 2026 alone, up ~60% on last year - around US$450B straight into data centres, chips and servers (source).

- OpenAI's Stargate: a US$500 billion program.

- a US$100 billion, 10-year compute deal. Anthropic:

Then there is the military spending increasing all over the world (NATO committing 5% of GDP toward defence expenditure). (source)

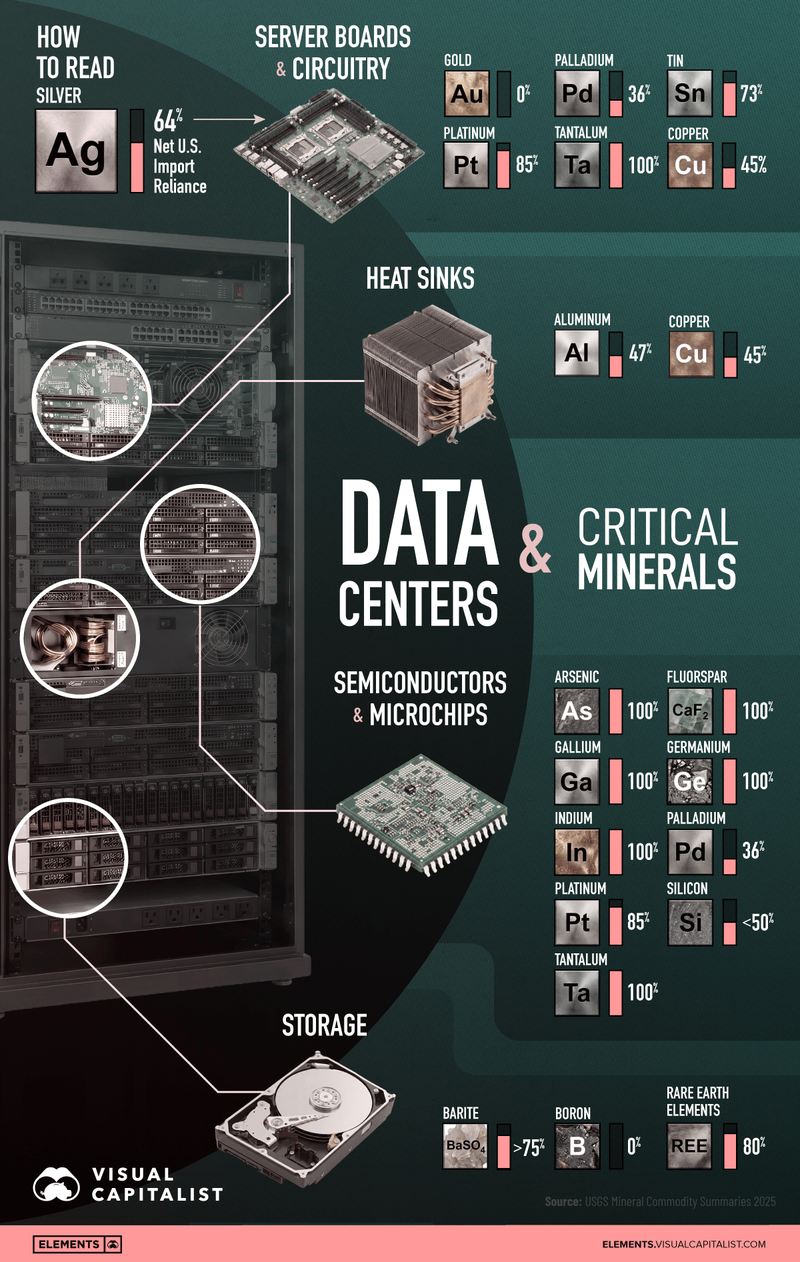

The only question that matters: where do the metals and minerals come from to be able to build all of those data centres and robots?

Things like:

- copper for the wiring

- silver for the connections

- rare earths for the magnets and cooling

- steel, aluminium and concrete for the buildings

- uranium, gas and grid to power the lot

(source)

Or all the stuff that goes into military weapons, equipment and munitions:

(source)

The race to build out AI, robots and militaries is another theme we think isn’t going away in the near to medium term.

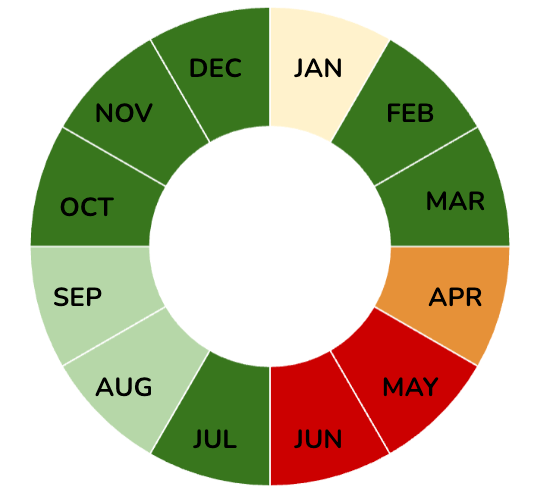

A quick look at our “small-cap calendar” - why July may bring back the good mood

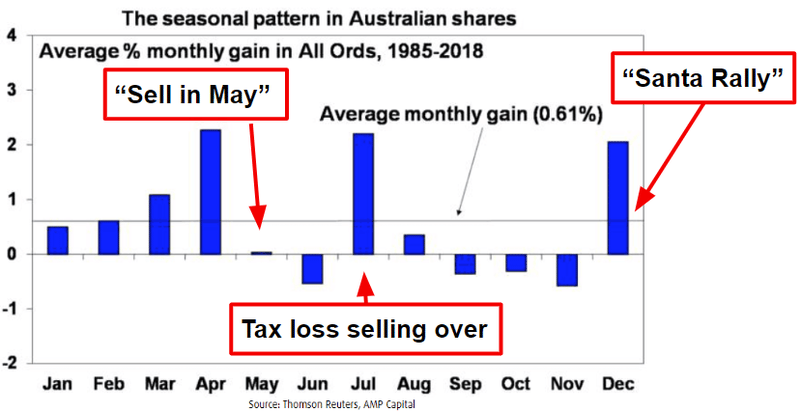

Below is a chart that tracks the seasonality of the All Ordinaries (largest 500 companies in Australia):

(Source)

The chart shows the average monthly gains in the market is highest in April, July and in December.

Small caps are a bit different.

The low liquidity on small cap stocks means one large investor who needs to sell can crush a company’s share price.

And on the upswing, a fervour of interest in a stock with a tight register can see companies’ valuations rise extremely quickly.

We have our own “activity calendar for small cap stocks” - green being generally periods of bullish trading, red being periods of generally bearish trading:

- January - Brokers return from holidays and the small cap market picks up in the second half of the month.

- February/March - expectations are high at the start of the calendar year, strong newsflow from companies as early wins are secured.

- April - Strong newsflow in the lead-up to Easter after which the market quiets down.

- May/June - Tax loss selling season.

- July - Post-tax loss selling rally.

- August/September - Annual report season, companies execute on key milestones / goals.

- October/November - Pre-Santa rally in the lead up to Christmas.

- December - Santa rally in the first two weeks of December. Companies and stockbrokers usually close up for the year after the 15th.

So May and June are usually the worst periods in the market.

Except in a long term bear market like the one we just lived through, where every month stinks.

("Sell in May and go away", for the record, is an old London saying - from the days bankers and merchants sold up and fled the city heat for summer. Somehow it stuck, and somehow it crossed the planet to apply to small cap ASX stocks.)

May usually morphs into a stand-offish June.

And then comes July - when the artificial calendar pressure lifts - usually in the first couple of weeks of July, sometimes the last few days of June - the same beaten-up names can snap back just as sharply as they fell.

None of this is guaranteed, of course.

(small caps can go down as well as up, the July bounce might not come this time, and "history usually rhymes" is a long way from "history promises" - this also means that June could still even be a positive month.)

But after three years of writing that the small-cap market sucked...

I guess it’s good to be writing about tax-loss selling again - it means capital gains are back.

(except coming from a more upbeat base... not a depressed one)

Have a great weekend.

Next Investors

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.